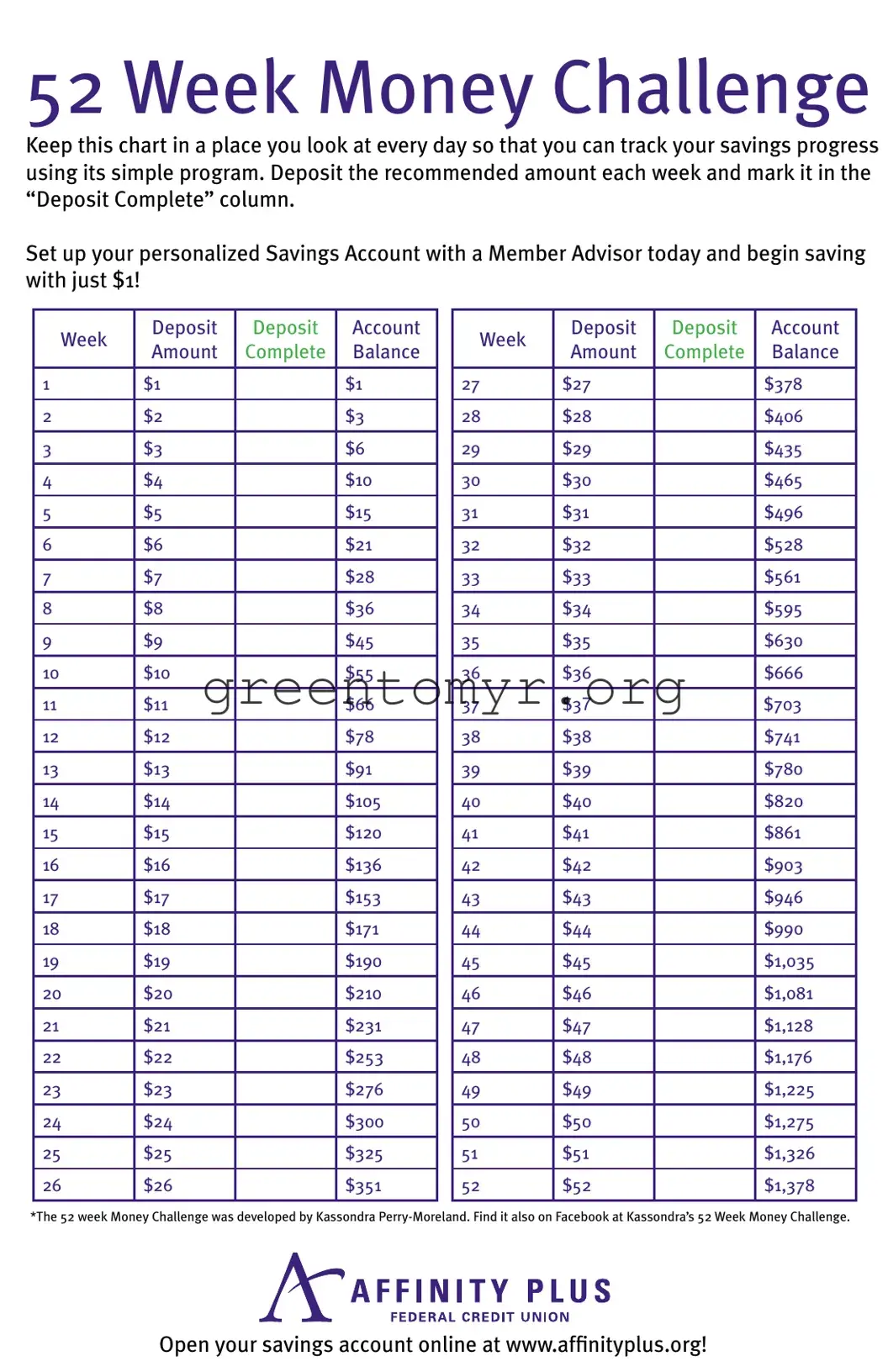

The 52 Week Money Challenge has gained popularity as a practical way to build savings over the course of a year. This simple strategy encourages individuals to set aside a specific amount of money each week, gradually increasing the deposit to maximize savings potential. For example, participants begin by saving $1 during the first week, and by the final week, the amount saved increases to $52. The structure of the challenge allows for flexibility, so individuals can start at any week of the year. By the end of 52 weeks, a total of $1,378 can be saved, providing a solid financial boost. The form serves as a helpful tool for tracking progress, making it easy to record deposits and monitor savings over time. Accessibility is a key benefit, as anyone can join the challenge regardless of their starting point, fostering a sense of accountability and motivation.

52 Week Money Challenge

Keep this chart in a place you look at every day so that you can track your savings progress using its simple program. Deposit the recommended amount each week and mark it in the “Deposit Complete” column.

Set up your personalized Savings Account with a Member Advisor today and begin saving with just $1!

Week |

Deposit |

Deposit |

Account |

|

Amount |

Complete |

Balance |

||

|

||||

|

|

|

|

|

1 |

$1 |

|

$1 |

|

|

|

|

|

|

2 |

$2 |

|

$3 |

|

|

|

|

|

|

3 |

$3 |

|

$6 |

|

|

|

|

|

|

4 |

$4 |

|

$10 |

|

|

|

|

|

|

5 |

$5 |

|

$15 |

|

|

|

|

|

|

6 |

$6 |

|

$21 |

|

|

|

|

|

|

7 |

$7 |

|

$28 |

|

|

|

|

|

|

8 |

$8 |

|

$36 |

|

|

|

|

|

|

9 |

$9 |

|

$45 |

|

|

|

|

|

|

10 |

$10 |

|

$55 |

|

|

|

|

|

|

11 |

$11 |

|

$66 |

|

|

|

|

|

|

12 |

$12 |

|

$78 |

|

|

|

|

|

|

13 |

$13 |

|

$91 |

|

|

|

|

|

|

14 |

$14 |

|

$105 |

|

|

|

|

|

|

15 |

$15 |

|

$120 |

|

|

|

|

|

|

16 |

$16 |

|

$136 |

|

|

|

|

|

|

17 |

$17 |

|

$153 |

|

|

|

|

|

|

18 |

$18 |

|

$171 |

|

|

|

|

|

|

19 |

$19 |

|

$190 |

|

|

|

|

|

|

20 |

$20 |

|

$210 |

|

|

|

|

|

|

21 |

$21 |

|

$231 |

|

|

|

|

|

|

22 |

$22 |

|

$253 |

|

|

|

|

|

|

23 |

$23 |

|

$276 |

|

|

|

|

|

|

24 |

$24 |

|

$300 |

|

|

|

|

|

|

25 |

$25 |

|

$325 |

|

|

|

|

|

|

26 |

$26 |

|

$351 |

|

|

|

|

|

Week |

Deposit |

Deposit |

Account |

|

Amount |

Complete |

Balance |

||

|

||||

|

|

|

|

|

27 |

$27 |

|

$378 |

|

|

|

|

|

|

28 |

$28 |

|

$406 |

|

|

|

|

|

|

29 |

$29 |

|

$435 |

|

|

|

|

|

|

30 |

$30 |

|

$465 |

|

|

|

|

|

|

31 |

$31 |

|

$496 |

|

|

|

|

|

|

32 |

$32 |

|

$528 |

|

|

|

|

|

|

33 |

$33 |

|

$561 |

|

|

|

|

|

|

34 |

$34 |

|

$595 |

|

|

|

|

|

|

35 |

$35 |

|

$630 |

|

|

|

|

|

|

36 |

$36 |

|

$666 |

|

|

|

|

|

|

37 |

$37 |

|

$703 |

|

38 |

$38 |

|

$741 |

|

|

|

|

|

|

39 |

$39 |

|

$780 |

|

|

|

|

|

|

40 |

$40 |

|

$820 |

|

|

|

|

|

|

41 |

$41 |

|

$861 |

|

|

|

|

|

|

42 |

$42 |

|

$903 |

|

|

|

|

|

|

43 |

$43 |

|

$946 |

|

|

|

|

|

|

44 |

$44 |

|

$990 |

|

|

|

|

|

|

45 |

$45 |

|

$1,035 |

|

|

|

|

|

|

46 |

$46 |

|

$1,081 |

|

|

|

|

|

|

47 |

$47 |

|

$1,128 |

|

|

|

|

|

|

48 |

$48 |

|

$1,176 |

|

|

|

|

|

|

49 |

$49 |

|

$1,225 |

|

|

|

|

|

|

50 |

$50 |

|

$1,275 |

|

|

|

|

|

|

51 |

$51 |

|

$1,326 |

|

|

|

|

|

|

52 |

$52 |

|

$1,378 |

|

|

|

|

|

*The 52 week Money Challenge was developed by Kassondra

Open your savings account online at www.affinityplus.org!

| Fact Name | Description |

|---|---|

| Overview | The 52 Week Money Challenge is a savings plan that encourages individuals to set aside a specified amount of money each week for a year. |

| Savings Growth | Participants can potentially save a total of $1,378 by the end of the 52 weeks, starting from $1 in the first week. |

| Weekly Commitment | Each week, the amount saved increases by $1, beginning with $1 in the first week and reaching $52 in the last week. |

| Flexibility | Participants can adjust the challenge according to their financial capacity, such as changing the start amount or the weekly increment. |

| Community Engagement | The challenge can be undertaken as a group or community initiative, fostering a sense of accountability and shared motivation. |

| Tracking Progress | Individuals can use various methods to track their savings, including spreadsheets or dedicated savings apps. |

| State-Specific Considerations | Some states may require adherence to specific financial regulations; always review local laws related to personal savings methods. |

| Tax Implications | Interest earned on savings may be subject to taxation, so individuals should consider their tax obligations at the end of the year. |

| Motivational Aspect | Individuals often find motivation through visual progress indicators, such as charts or completion marks, which enhance the saving experience. |

| Longevity | The challenge can be repeated each year, allowing individuals to build sustainable savings habits over time. |

Completing the 52 Week Money Challenge form requires careful attention to detail and organization. Once the form is filled out, it will guide your savings journey effectively.

The 52 Week Money Challenge is a popular savings program designed to help individuals save a specific amount of money over the course of a year. Participants start with a small amount in the first week and gradually increase their savings each week. At the end of the year, individuals will have saved a total of $1,378.

The challenge begins with saving $1 in the first week, then $2 in the second week, and continues increasing by $1 each week for 52 weeks. For example:

At the end of week 52, your total savings will amount to $1,378.

The 52 Week Money Challenge helps develop a consistent savings habit. It allows participants to gradually increase their savings without feeling overwhelmed. Additionally, it provides a clear goal and a visual representation of progress, making saving feel more achievable and rewarding.

Yes, the 52 Week Money Challenge can begin at any point during the year. You do not need to wait for the beginning of the year. Start whenever it feels right for you, adapting the weekly savings amount according to your budget.

If you miss a week, consider two options: catch up by saving double in the next week or adjust your savings plan to meet the end goal. The key is to keep moving forward and establish a sustainable savings routine that works for you.

Yes, many websites and financial blogs offer printable forms for the 52 Week Money Challenge. You can use these forms to track your savings progress. Look for options that suit your preference, whether digital or physical formats.

While it is a flexible savings method, the challenge might be challenging for those with limited income or financial obligations. Adjust the weekly savings amounts based on your financial situation to ensure it is feasible for you.

Setting milestones or rewards can boost motivation. Celebrate small achievements along the way, like completing a month. Visual reminders and tracking your progress can also help keep your goals in sight and encourage adherence to the challenge.

At the end of the challenge, you can use your savings for various purposes, such as creating an emergency fund, making a large purchase, investing, or planning a special trip. The choice is entirely yours, based on your financial needs and goals.

Involving family or friends can add accountability and increase motivation. You can create a group challenge, share progress, and support each other along the way. This communal approach can make saving more enjoyable and engaging.

The 52 Week Money Challenge is a simple yet effective way to improve one’s savings habit. However, participants often encounter mistakes that can hinder their progress. One common mistake is underestimating the amount they need to save each week. Many begin with the intention of saving a small amount but find themselves overwhelmed by the actual total at the end of the year. Setting a realistic start point is crucial for maintaining motivation throughout the challenge.

Another frequent error is failing to keep track of contributions. Without a proper record-keeping system, it’s easy to forget how much has already been saved. People may lose track of their progress, which can lead to discouragement. Implementing a simple tracking method, whether through an app or a written journal, can help participants stay accountable.

Some individuals misinterpret the goal of the challenge, treating it as a one-size-fits-all program. It's important to adjust the weekly savings amounts according to personal financial circumstances. Those with fluctuating incomes or unexpected expenses should feel empowered to modify the challenge to suit their needs. Flexibility is key to making this journey successful.

Additionally, many challengers overlook the importance of setting aside a designated savings account. Saving money in a separate account can help prevent the temptation to dip into those funds for everyday expenses. This distinction allows participants to clearly see their progress, boosting motivation and commitment to the challenge.

Participating without having a plan for emergencies can also lead to setbacks. Life is unpredictable, and unexpected expenses can quickly derail the savings goal. Anticipating potential financial hurdles and having a strategy to address them can provide peace of mind. For example, having a small emergency fund can keep participants on track.

Another mistake is not involving family or friends in the challenge. Sharing goals with loved ones can create a support system that encourages consistent savings. Knowing that others are aware of your commitment makes it easier to stick to the challenge, especially when the going gets tough.

People often forget to review and celebrate their achievements throughout the year. Not acknowledging progress can lead to feelings of stagnation or boredom. Regularly reflecting on milestones—such as completing a month of savings—provides a sense of accomplishment that fuels motivation to continue.

Overcommitting is yet another common pitfall. Participants may initially dive in with enthusiasm but quickly realize that the weekly contributions amount to more than they can sustainably afford. It’s essential to find a balance between ambition and feasibility. Setting smaller, achievable targets and gradually increasing savings over time can yield better long-term results.

Moreover, relying solely on the challenge for savings can lead to an incomplete financial picture. Individuals should consider other methods of saving or investing to enhance their overall financial health. The 52 Week Money Challenge can serve as a foundation, but it shouldn't be the only savings strategy in play.

Lastly, many assume the challenge will be easy and underestimate the dedication required. Building a habit takes time and perseverance, and participants may face lapses in motivation. Recognizing that challenges will arise and having a strategy for maintaining focus can help individuals push through tough times and achieve their financial goals.

The 52 Week Money Challenge is an engaging way to save money gradually over the course of a year. To make the most of your saving journey, there are several forms and documents that can complement this challenge. Each plays its own unique role in helping you track and plan your finances effectively. Here’s a brief overview of these useful documents:

Using these documents in conjunction with the 52 Week Money Challenge creates a comprehensive financial strategy. It not only makes saving money more manageable but also instills discipline and promotes a brighter financial future. By being organized and proactive, you can achieve your financial dreams more effectively.

The Budget Plan is similar to the 52 Week Money Challenge form as both serve the purpose of tracking and managing finances. Each document encourages individuals to allocate funds and prioritize savings over time, allowing for a structured approach to financial health.

The Savings Tracker acts in a manner akin to the 52 Week Money Challenge form by providing a way to monitor savings progress. It typically includes a detailed record of contributions, helping individuals see how their savings accumulate.

A Debt Repayment Plan shares similarities with the 52 Week Money Challenge in that it emphasizes discipline in financial habits. Both documents require regular payments or contributions, promoting a steady path towards achieving financial goals, whether in saving or repaying debts.

The Investment Portfolio Tracker resembles the 52 Week Money Challenge form through its focus on growth over time. While the money challenge emphasizes saving, the investment tracker concentrates on how investments perform, both documents offering a snapshot of long-term financial planning.

The Monthly Expense Report is similar in its aim to create awareness about financial habits. Like the 52 Week Money Challenge, it encourages reflective practice by detailing spending patterns, ultimately guiding better financial decisions.

When completing the 52 Week Money Challenge form, it is important to follow guidelines to ensure accuracy and effectiveness. Below are key dos and don'ts:

The 52 Week Money Challenge has gained popularity as a straightforward method for saving money. However, several misconceptions exist regarding how it works and its effectiveness. Below are seven common misconceptions about the challenge:

Understanding these misconceptions can provide clarity and encourage individuals to engage with the 52 Week Money Challenge in a way that suits their financial goals.

Here are key takeaways about filling out and using the 52 Week Money Challenge form:

This structured approach can help anyone looking to develop a regular savings habit.