The Additional Insured form is a crucial component in the realm of commercial general liability insurance, particularly for businesses that engage in contracting or subcontracting work. This endorsement, identified as CG 20 37 04 13, modifies the existing insurance policy to extend coverage to additional parties, such as owners, lessees, or contractors, for completed operations. It specifies the names of those additional insureds and outlines the locations and descriptions of the completed operations that fall under this coverage. The endorsement clarifies that the additional insureds are protected against liability for bodily injury or property damage that arises from the work performed for them. However, it also sets boundaries, stating that the coverage is only as extensive as required by law or as stipulated in any relevant contracts. Importantly, the limits of insurance for these additional insureds cannot exceed what is mandated by the contract or the limits outlined in the policy's declarations. This ensures that while additional parties are covered, the primary insured's obligations and liabilities remain clear and manageable.

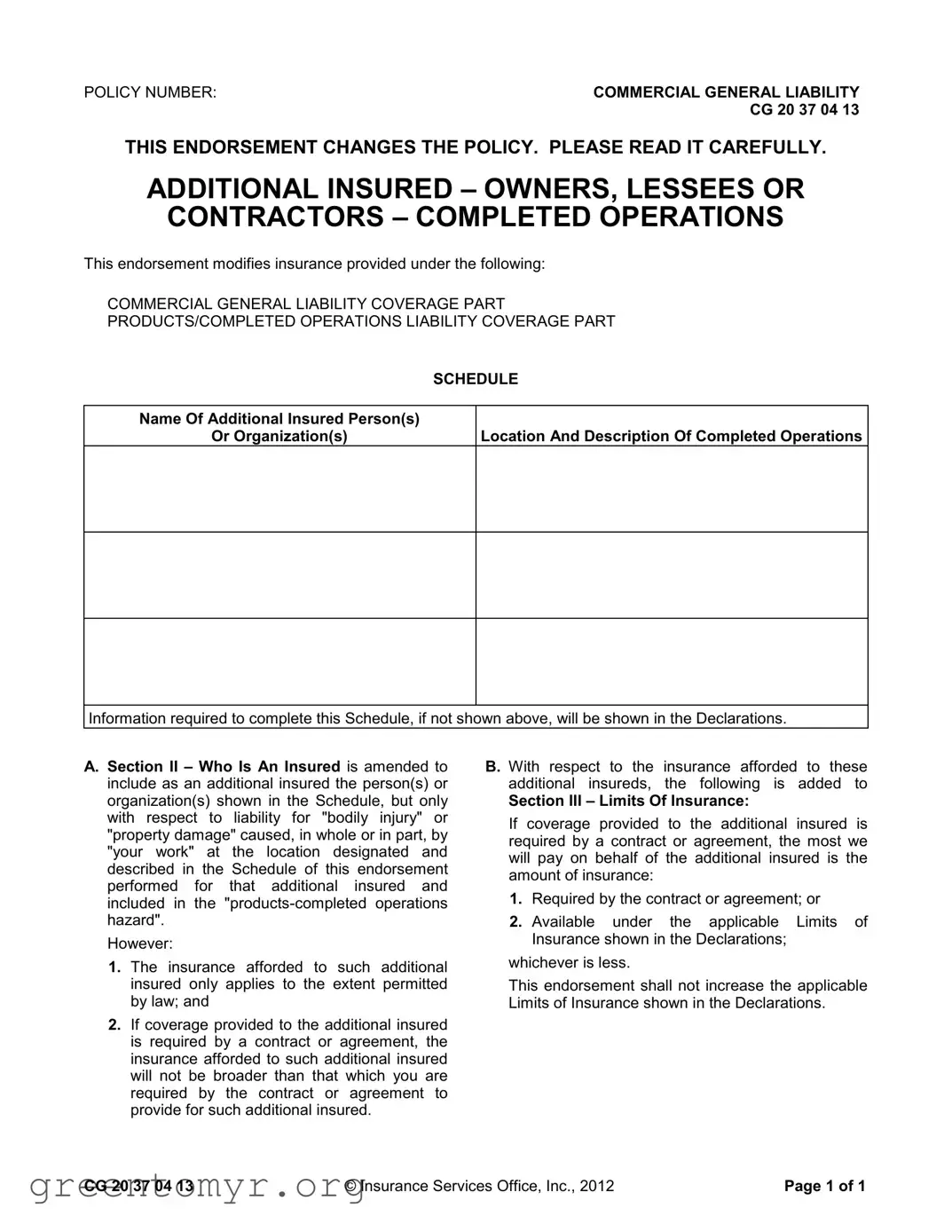

POLICY NUMBER: |

COMMERCIAL GENERAL LIABILITY |

|

CG 20 37 04 13 |

THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY.

ADDITIONAL INSURED – OWNERS, LESSEES OR CONTRACTORS – COMPLETED OPERATIONS

This endorsement modifies insurance provided under the following:

COMMERCIAL GENERAL LIABILITY COVERAGE PART

PRODUCTS/COMPLETED OPERATIONS LIABILITY COVERAGE PART

SCHEDULE

Name Of Additional Insured Person(s)

Or Organization(s)

Location And Description Of Completed Operations

Information required to complete this Schedule, if not shown above, will be shown in the Declarations.

A.Section II – Who Is An Insured is amended to include as an additional insured the person(s) or organization(s) shown in the Schedule, but only with respect to liability for "bodily injury" or "property damage" caused, in whole or in part, by "your work" at the location designated and described in the Schedule of this endorsement performed for that additional insured and included in the

However:

1.The insurance afforded to such additional insured only applies to the extent permitted by law; and

2.If coverage provided to the additional insured is required by a contract or agreement, the insurance afforded to such additional insured will not be broader than that which you are required by the contract or agreement to provide for such additional insured.

B. With respect to the insurance afforded to these additional insureds, the following is added to

Section III – Limits Of Insurance:

If coverage provided to the additional insured is required by a contract or agreement, the most we will pay on behalf of the additional insured is the amount of insurance:

1.Required by the contract or agreement; or

2.Available under the applicable Limits of Insurance shown in the Declarations;

whichever is less.

This endorsement shall not increase the applicable Limits of Insurance shown in the Declarations.

CG 20 37 04 13 |

© Insurance Services Office, Inc., 2012 |

Page 1 of 1 |

| Fact Name | Description |

|---|---|

| Definition | The Additional Insured form, specifically CG 20 37 04 13, adds coverage for other parties, such as owners or contractors, under a primary policyholder's general liability insurance. |

| Coverage Scope | This endorsement covers liability for bodily injury or property damage resulting from the named insured's work, specifically in completed operations. |

| Schedule Requirement | The form requires a schedule that identifies the additional insured parties and the specific operations covered. |

| Legal Limitations | Coverage is limited to the extent permitted by law, ensuring compliance with state regulations. |

| Contractual Limitations | If a contract mandates coverage for the additional insured, the insurance provided cannot exceed what is required by that contract. |

| Limits of Insurance | The maximum amount payable on behalf of the additional insured is the lesser of the contract requirement or the available limits in the policy declarations. |

| Exclusion of Increased Limits | This endorsement does not increase the overall limits of insurance stated in the policy declarations. |

| State-Specific Forms | Some states may have specific forms or requirements for additional insured endorsements, governed by local insurance laws. |

| Importance in Contracts | Including additional insured provisions in contracts can protect parties from liability arising from completed operations. |

| Review Requirement | Policyholders should carefully review the endorsement to ensure it meets their contractual obligations and coverage needs. |

Filling out the Additional Insured form is a straightforward process. It requires specific information to ensure that all parties are accurately represented and covered under the insurance policy. Follow these steps carefully to complete the form correctly.

An Additional Insured form is a document that extends liability coverage to other parties, such as owners, lessees, or contractors, under your commercial general liability insurance policy. This form is particularly important in situations where your work may lead to bodily injury or property damage. By including others as additional insureds, you help protect them from claims that may arise from your operations.

The individuals or organizations that can be named as additional insureds are typically specified in the endorsement schedule. These may include:

It is crucial to ensure that the additional insureds are listed in the endorsement to guarantee coverage.

The coverage provided by the Additional Insured form is limited to liability arising from your work at the specified location. This includes:

However, the coverage is only applicable to the extent permitted by law and cannot exceed what is stipulated in any contract or agreement.

Yes, there are limits to the coverage provided to additional insureds. The amount payable on behalf of the additional insured will be the lesser of:

This means that the coverage will not increase the overall limits of your insurance policy.

Including an Additional Insured form is essential for risk management. It protects both you and the additional insured from potential legal claims. By ensuring that all parties involved are adequately covered, you foster stronger business relationships and reduce the likelihood of disputes arising from incidents related to your work.

Filling out the Additional Insured form can be a straightforward process, but several common mistakes can lead to complications. One significant error is failing to include the correct policy number. The policy number is essential for identifying the specific coverage being modified. Without it, there may be confusion regarding which policy the endorsement applies to.

Another mistake is not specifying the name of the additional insured accurately. This includes using incorrect spellings or abbreviations that do not match the legal name of the organization or individual. Such discrepancies can lead to disputes over coverage, as the insurer may deny claims based on incorrect information.

People often overlook the location and description of completed operations. This section must clearly describe where the work was performed and what operations were completed. Vague or incomplete descriptions can cause issues when a claim arises, as it may be unclear whether the incident is covered under the policy.

In some cases, individuals forget to review the limits of insurance applicable to the additional insured. The form specifies that coverage cannot exceed the limits outlined in the declarations or those required by contract. Failing to understand these limits can result in inadequate coverage during a claim.

Another common error is not recognizing that the insurance provided is only applicable to the extent permitted by law. This means that even if the endorsement is filled out correctly, there may be legal limitations on the coverage that could affect the additional insured’s ability to make a claim.

Some individuals mistakenly believe that the coverage provided to the additional insured is automatically broader than what is required by contract. It is crucial to understand that if a contract specifies certain coverage, the insurance offered cannot exceed that requirement. Misinterpretation of this can lead to significant gaps in protection.

Additionally, people sometimes neglect to consult the declarations page for necessary information. The declarations page contains vital details about the policy that may affect the endorsement. Ignoring this information can lead to incomplete or incorrect submissions.

Another frequent oversight is failing to include any additional information required in the schedule. If the form requires specific details that are not provided, the endorsement may be deemed invalid. Always double-check that all required fields are filled out completely.

Individuals may also misinterpret the term "your work." This term refers specifically to the work performed for the additional insured, and not all operations may fall under this definition. Misunderstanding this can lead to disputes regarding liability.

Lastly, some people do not keep a copy of the completed form for their records. Retaining a copy is important for future reference, especially if a claim arises. Without documentation, it may be challenging to prove the terms of the endorsement.

The Additional Insured form is a crucial document in many insurance transactions. It helps extend coverage to other parties involved in a contract. Alongside this form, several other documents are commonly used to ensure comprehensive coverage and compliance. Below is a list of these documents with brief descriptions of each.

Understanding these documents can help ensure that all parties are adequately protected and compliant with contractual obligations. Always review and confirm that the necessary forms are in place before commencing any work.

The Additional Insured form serves a specific purpose in liability insurance, particularly in the context of commercial general liability policies. It is similar to several other documents that also address coverage and liability issues. Below are six documents that share similarities with the Additional Insured form:

Understanding these documents is crucial for parties involved in contracts requiring insurance coverage. Each serves a unique function but shares the common goal of clarifying liability and coverage responsibilities.

When filling out the Additional Insured form, it is important to follow specific guidelines to ensure accuracy and compliance. Below is a list of things you should and shouldn't do:

Following these guidelines can help ensure that the Additional Insured form is completed correctly and efficiently.

There are several misconceptions about the Additional Insured form that can lead to confusion. Here are six common misunderstandings:

Here are key takeaways about filling out and using the Additional Insured form: