The Adverse Action form is an essential document in the realm of consumer banking, providing a formal notification when a financial institution denies a request for a deposit account. This notice must clearly outline the reasons behind the decision, typically drawing from information sourced through consumer reporting agencies like Chex Systems. With a focus on transparency, the form informs applicants of their rights under the Fair Credit Reporting Act, which permits them to access their credit reports and dispute any inaccuracies they may encounter. Various templates exist, such as those including or excluding credit score disclosures, allowing institutions to tailor their communications to comply with legal requirements while addressing specific applicant needs. Moreover, Chex Systems offers helpful materials designed to guide institutions in adhering to compliance regulations, although it is crucial to note that the responsibility remains with each institution to ensure that these forms meet all applicable laws. The information provided is not customized to fit any one institution's practices, underscoring the importance of internal review for compliance.

Chex Systems, Inc.

Notice of Adverse Action Form Samples

Release Date: January 2012

Do you need compliance assistance at the tip of your fingers?

An annual subscription with FIS Regulatory Advisory Services helps you tackle the daily challenges of compliance. As your trusted compliance advisor, we want to make your life easier by providing you with the

most honest, accurate, timely and practical advice possible, and keeping you up to date in the

trusted by regulated financial institutions and examiners alike!

By signing up today, you will have access to:

Unlimited access to our regulatory compliance experts via the hotline or

Unlimited access to our scheduled webinars on hot topics for three institution users

Unlimited access to our Web site for your entire institution, which includes the Big Orange Book, and other tools like our Mortgage Loan Disclosure Calculator, Compliance Timeline, Sample Policy Manual and much more!

Three hard copies of the Big Orange Book & Quick Reference Guides (updates and new guides at no additional cost throughout the year)

Discounts on educational seminars for any attendee you send

*Contact us for special promotional pricing!

(Regular Price is $4,995)

Call us at (866) 355 - 5150 or

email us at [email protected]

So what are you waiting for?!

Sign up today!

*Existing Regulatory Service customers can take advantage of this offer depending on renewal dates and subscription level

(i.e. Premium Member, Website Only, BOB only Subscriber). Offer only valid for a new or renewing subscription, and cannot be used on an existing contract.

Please contact Catherine Livingston at (800)

Want More Information? |

|

Visit us on the web at: |

|

www.FISregulatoryservices.com |

|

|

|

CONFIDENTIAL |

2 | P a g e |

Chex Systems, Inc. Notice of Adverse Action Form Samples (Release Date: January 2012) |

|

Copyright © 2012 Fidelity National Information Services and/or its subsidiaries. All Rights Reserved. |

|

INFORMATION ABOUT THIS DOCUMENT |

|

As a o e ie e, Che “ ste s, I . ChexSystems |

a pro ide or other ise ake a aila le to its |

customers certain sample adverse action forms, procedures, or other similar information (collectively, Materials . ChexSystems customers acknowledge and agree that the Materials were created for general

application and have not been customized to address usto ers’ specific business operations. ChexSystems does not guarantee that the Materials will comply with any applicable laws, rules or regulations, and the customer is responsible for its use of Materials and bears sole liability for any such use.

Samples in this document include:

1.ChexSystems Adverse Action Notice, without Credit Score Disclosure

2.ChexSystems Adverse Action Notice, with Credit Score Disclosure

3.ChexSystems, plus Credit Bureaus Adverse Action Notice, with Credit Score Disclosure

CHEXSYSTEMS POSITION ON THE CREDIT SCORE DISCLOSURE REQUIREMENT

ChexSystems is not taking a position on whether or not its customers are required to provide the Credit Score Disclosure to declined account applicants; rather, each financial institution is responsible for making this determination on its own behalf. As a convenience to its customers that elect to provide the Credit Score Disclosure to declined account applicants, ChexSystems is now making available the data fields necessary to support the Credit Score Disclosure requirements set forth by the

Chex Systems, Inc. (herein ChexSystems) is a consumer reporting agency and

an indirect wholly owned subsidiary of Fidelity National Information Services, Inc.

CONFIDENTIAL |

3 | P a g e |

Chex Systems, Inc. Notice of Adverse Action Form Samples (Release Date: January 2012) |

|

Copyright © 2012 Fidelity National Information Services and/or its subsidiaries. All Rights Reserved. |

|

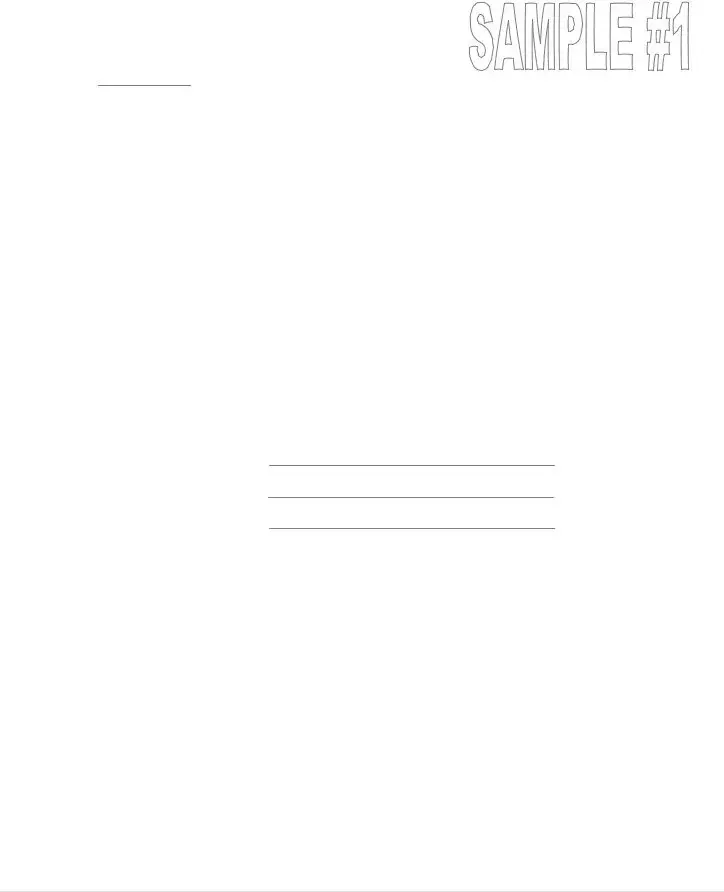

Notice of Adverse Action

Notice Date:

We are sorry but we are unable to accommodate your request to open a deposit account with our institution at this time. Our decision was based in whole or in part on information obtained in a report from the consumer reporting agency listed below. You have a right under the Fair Credit Reporting Act to know the information contained in your file at the consumer reporting agency. The reporting agency played no part in our decision and is unable to supply specific reasons why we have denied your request to open a deposit account in our institution. You also have a right to a free copy of your report from the reporting agency, if you request it no later than 60 days after you receive this notice. In addition, if you find that any information contained in the report you receive is inaccurate or incomplete, you have the right to dispute the matter with the reporting agency.

Chex Systems, Inc.

Attn: Consumer Relations

7805 Hudson Road, Suite 100

Woodbury, MN 55125

Telephone:

Fax:

Web: www.consumerdebit.com

If you have any questions regarding your consumer report, you should contact the consumer reporting agency using the contact information above.

If you have any other questions regarding this notice, you should contact:

Institution name:

Institution address:

Institution

As a convenience, Chex may provide or otherwise make available to Client certain sample adverse action forms, procedures, or other similar information (collectively,

Materials ). Clie t a k o ledges a d agrees that the Materials ere reated for ge eral appli atio a d ha e ot ee usto ized to address Clie t’s spe ifi business operations. Chex does not guarantee that the Materials will comply with any applicable laws, rules or regulations, and Client is responsible for its use of Materials and bears sole liability for any such use.

CONFIDENTIAL |

4 | P a g e |

Chex Systems, Inc. Notice of Adverse Action Form Samples (Release Date: January 2012) |

|

Copyright © 2012 Fidelity National Information Services and/or its subsidiaries. All Rights Reserved. |

|

Notice of Adverse Action

Notice Date:

We are sorry but we are unable to accommodate your request to open a deposit account with our institution at this time. Our decision was based in whole or in part on information obtained in a report from the consumer reporting agency listed below. You have a right under the Fair Credit Reporting Act to know the information contained in your file at the consumer reporting agency. The reporting agency played no part in our decision and is unable to supply specific reasons why we have denied your request to open a deposit account in our institution. You also have a right to a free copy of your report from the reporting agency, if you request it no later than 60 days after you receive this notice. In addition, if you find that any information contained in the report you receive is inaccurate or incomplete, you have the right to dispute the matter with the reporting agency.

Chex Systems, Inc.

Attn: Consumer Relations

7805 Hudson Road, Suite 100

Woodbury, MN 55125

Telephone:

Fax:

Web: www.consumerdebit.com

We also obtained your credit score from this consumer reporting agency and used it in making our credit decision. Your credit score is a number that reflects the information in your consumer report. Your credit score can change, depending on how the information in your consumer report changes.

Credit Score: |

|

Score Date: |

Scores range from a low of 100 to a high of 9999

Key factors that adversely affected your credit score (insert here the four key factors that adversely affected the credit score or if the number of recent inquiries is a key factor, insert five key factors including the number of recent inquiries):

If you have any questions regarding your credit score, you should contact the consumer reporting agency using the contact information above.

If you have any other questions regarding this notice, you should contact:

Institution name:

Institution address:

Institution

As a convenience, Chex may provide or otherwise make available to Client certain sample adverse action forms, procedures, or other similar information (collectively,

Materials ). Clie t a k o ledges a d agrees that the Materials ere reated for ge eral appli atio a d ha e ot ee usto ized to address Clie t’s spe ifi

business operations. Chex does not guarantee that the Materials will comply with any applicable laws, rules or regulations, and Client is responsible for its use of Materials and bears sole liability for any such use.

CONFIDENTIAL |

5 | P a g e |

Chex Systems, Inc. Notice of Adverse Action Form Samples (Release Date: January 2012) |

|

Copyright © 2012 Fidelity National Information Services and/or its subsidiaries. All Rights Reserved. |

|

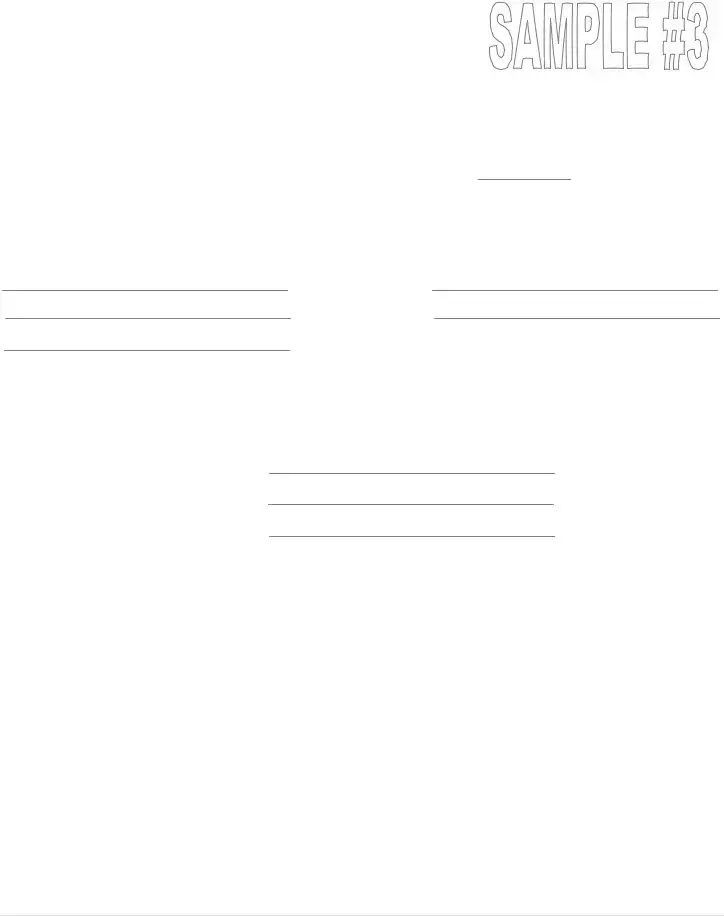

Notice of Adverse Action

Notice Date:

We are sorry but we are unable to accommodate your request to open a deposit account with our institution at this time. Our decision was based in whole or in part on information obtained in a report from one or more of the consumer reporting agencies listed below. You have a right under the Fair Credit Reporting Act to know the information contained in your file at the consumer reporting agency. The reporting agency played no part in our decision and is unable to supply specific reasons why we have denied your request to open a deposit account in our institution. You also have a right to a free copy of your report from the reporting agency, if you request it no later than 60 days after you receive this notice. In addition, if you find that any information contained in the report you receive is inaccurate or incomplete, you have the right to dispute the matter with the reporting agency.

|

|

ChexSystems |

|

|

Experian |

|

|

Equifax |

|

|

Trans Union |

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Chex Systems, Inc. |

Experian |

Equifax Credit Information Services |

TransUnion Consumer Relations |

||||||||

Attn: Consumer Relations |

PO Box 2002 |

PO Box 740241 |

PO Box 1000 |

||||||||

7805 Hudson Road, Suite 100 |

Allen, TX 75013 |

Atlanta, GA 30374 |

Chester, PA 19022 |

||||||||

Woodbury, MN 55125 |

|

|

|

|

|

|

|

|

|

||

|

|

|

Telephone: |

Telephone: |

Telephone: |

||||||

Telephone: |

Web: |

|

|

|

Web: |

||||||

Fax: |

www.experian.com/reportaccess |

|

|

|

www.transunion.com/myoptions |

||||||

Web: www.consumerdebit.com |

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

To contact ChexSystems in |

If you prefer to use a mailed |

To contact Equifax in writing, |

If you prefer to mail a request, |

||||||||

writing, forward your request |

request, send the following |

forward your request including |

please provide your first name, |

||||||||

including your full name, |

information to Experian: your full |

your name, address, former |

last name, middle initial, current |

||||||||

including middle initial, current |

name, including middle initial and |

address (if you have been at your |

address, Social Security number, |

||||||||

address, US Social Security |

generation such as SR, JR, II, etc.; |

current address less than two |

date of birth, any previous |

||||||||

number, date of birth and any |

current mailing address; Social |

years), Social Security Number |

addresses used in the past five |

||||||||

previous addresses used in the |

Security number; date of birth; |

(required) and the name of the |

years (include any PO Boxes). |

||||||||

last five years (including PO |

previous addresses for the past |

company that referred you to |

|

|

|

||||||

Boxes). |

two years; and two proofs of your |

Equifax. |

|

|

|

||||||

|

|

|

current mailing address, such as |

|

|

|

|

|

|

||

|

|

|

dri er’s li e se, utilit ill, a k or |

|

|

|

|

|

|

||

|

|

|

insurance statement, etc. |

|

|

|

|

|

|

||

As a convenience, |

Chex may provide or otherwise make available to Client certain sample adverse action forms, procedures, or other similar information (collectively, |

Materials ). Clie |

t a k o ledges a d agrees that the Materials ere reated for ge eral appli atio a d ha e ot ee usto ized to address Clie t’s spe ifi |

business operations. Chex does not guarantee that the Materials will comply with any applicable laws, rules or regulations, and Client is responsible for its use of Materials and bears sole liability for any such use.

Sample Form Continues on Next Page….

CONFIDENTIAL |

6 | P a g e |

Chex Systems, Inc. Notice of Adverse Action Form Samples (Release Date: January 2012) |

|

Copyright © 2012 Fidelity National Information Services and/or its subsidiaries. All Rights Reserved. |

|

We also obtained your credit score from this consumer reporting agency and used it in making our credit decision. Your credit score is a number that reflects the information in your consumer report. Your credit score can change, depending on how the information in your consumer report changes.

Credit Score: |

|

Score Date: |

Scores range from a low of 100 to a high of 9999

Key factors that adversely affected your credit score (insert here the four key factors that adversely affected the credit score or if the number of recent inquiries is a key factor, insert five key factors including the number of recent inquiries):

If you have any questions regarding your credit score, you should contact the consumer reporting agency using the contact information above.

If you have any other questions regarding this notice, you should contact:

Institution name:

Institution address:

Institution

As a convenience, Chex may provide or otherwise make available to Client certain sample adverse action forms, procedures, or other similar information (collectively,

Materials ). Clie t a k o ledges a d agrees that the Materials ere reated for ge eral appli atio a d ha e ot ee usto ized to address Clie t’s spe ifi business operations. Chex does not guarantee that the Materials will comply with any applicable laws, rules or regulations, and Client is responsible for its use of Materials and bears sole liability for any such use.

Contact Us |

For more information about Risk, Fraud, and Compliance Solutions |

|

|

||

|

or visit us on the Web: |

|

CONFIDENTIAL |

7 | P a g e |

Chex Systems, Inc. Notice of Adverse Action Form Samples (Release Date: January 2012) |

|

Copyright © 2012 Fidelity National Information Services and/or its subsidiaries. All Rights Reserved. |

|

| Fact Name | Description |

|---|---|

| Purpose of the Form | The Adverse Action form informs individuals when their application for a deposit account has been denied due to information obtained from a consumer reporting agency. |

| Rights of the Consumer | Consumers have the right to know the information contained in their file at the reporting agency and may request a free copy of their report within 60 days of receiving the notice. |

| Credit Score Disclosure | The form may include a disclosure about the applicant's credit score, which can affect the decision to grant an account. Institutions must determine if they are required to provide this information under the Dodd-Frank Act. |

| Legal Compliance | ChexSystems provides sample adverse action forms, but these are not guaranteed to comply with specific laws or regulations. Institutions are responsible for their own compliance. |

Completing the Adverse Action form is a straightforward process that helps ensure compliance with relevant regulations. After filling out the form, it will be sent to the applicant to inform them of the decision regarding their account request. Below are the steps you need to follow to fill out the form correctly.

An Adverse Action Form is a document used by financial institutions to notify an individual that their application for a deposit account or credit has been denied. This form provides information about the decision-making process and informs the applicant of their rights under the Fair Credit Reporting Act.

You may receive this form if your application for a bank account, loan, or credit card was denied based on information from a consumer reporting agency, such as ChexSystems. The institution must inform you of this decision in accordance with legal requirements.

The form typically includes:

Yes, under the Fair Credit Reporting Act, you have the right to request a free copy of your consumer report from the reporting agency within 60 days of receiving the Adverse Action Form. This allows you to review the information that influenced the denial.

If you find inaccuracies, you can dispute the information directly with the consumer reporting agency. The agency is required to investigate the dispute and correct any errors if they are validated.

The credit score disclosure, when included, informs you of your credit score used in the decision-making process. It may also include key factors that adversely affected your score. Understanding this can help you identify areas for improvement in your credit profile.

Not all institutions are legally required to use a specific Adverse Action Form. However, they must provide some form of communication regarding the denial and inform applicants of their rights.

While the form itself does not provide an official avenue for appeal, you can contact the financial institution to understand their policies regarding reconsideration or to check if additional documentation can support your application.

ChexSystems functions as a consumer reporting agency that provides information to financial institutions regarding an individual's banking history. Institutions may use this information to make credit decisions, leading to the issuance of an Adverse Action Form if an application is denied.

You can reach ChexSystems' Consumer Relations team at 800-428-9623 or via their website at www.consumerdebit.com for any inquiries related to your consumer report or the Adverse Action Form.

Completing the Adverse Action form may seem straightforward, but there are common pitfalls that can lead to complications. One frequent mistake is failing to include the necessary information about the consumer reporting agency used in the decision-making process. The law requires that consumers are informed about which agency provided the information influencing their application. Omitting this detail can leave applicants confused and may expose institutions to compliance issues.

Another common error is neglecting to provide the correct reasons for the adverse action. While institutions often use sample templates, it’s crucial to tailor the reasons to the specific situation of the applicant. Generic statements or vague language fail to meet legal disclosure requirements and can lead to credibility issues. Each applicant deserves clarity regarding why their application was denied to avoid misunderstandings.

Many institutions also forget to include the required timelines for the applicant to request their consumer report. If the notice doesn’t specify the 60-day window within which the applicant can request their report, it can undermine their right to access their information. This oversight not only frustrates consumers but also puts the institution at risk of regulatory scrutiny.

A final crucial mistake involves the mishandling of credit score disclosure. Institutions that are required to disclose credit scores may not provide adequate key factors that adversely affected the score. Including vague or unclear factors does not serve the applicants’ interests. Clear and specific information about key factors helps consumers understand their credit situations and empowers them to make informed decisions moving forward.

In the context of the Adverse Action process, several other important documents accompany the Adverse Action form. Each of these documents helps ensure compliance with regulations and provides consumers with essential information. Familiarity with these forms is crucial for financial institutions and their clients.

Together, these documents facilitate transparency, support compliance, and protect both consumers and institutions during the adverse action process. Proper management of these materials can help maintain trust and uphold regulatory standards.

When completing the Adverse Action form, consider the following guidelines:

This form is required whenever an application is denied based on information from a consumer reporting agency, regardless of the context, such as opening a deposit account.

The Adverse Action form serves as an official notification. You will receive this notice explaining why your request was denied and your rights to dispute any erroneous information.

The form must indicate that your decision was influenced by the information obtained from a consumer reporting agency. This transparency is essential for compliance.

You have the right to dispute any inaccuracies in the consumer report that influenced the adverse action. The notice instructs you on how to do this.

The consumer reporting agency merely provides information. Your financial institution makes the final decision, which must be communicated to you through the Adverse Action form.

You should receive the notice promptly after a decision is made. Timely communication is a requirement under the law.

When dealing with the Adverse Action form, keep these key takeaways in mind: