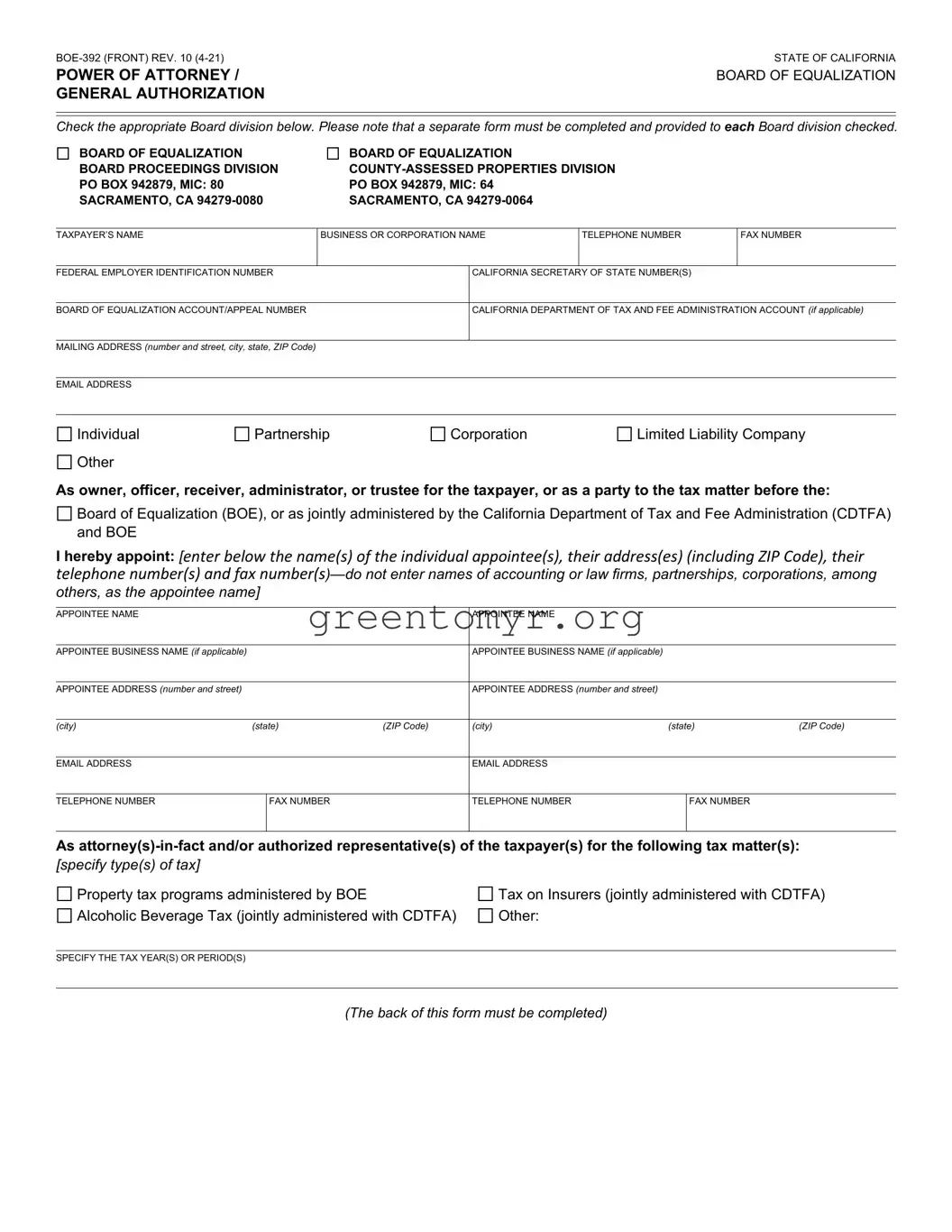

The BOE 392 form is an essential document for individuals and businesses navigating tax matters with the California Board of Equalization (BOE) and the California Department of Tax and Fee Administration (CDTFA). Designed as a Power of Attorney and General Authorization, this form allows taxpayers to appoint authorized representatives to manage their tax issues effectively. It requires key information such as the taxpayer’s name, business details, and contact information, ensuring a streamlined process for communication with the BOE. Additionally, taxpayers must specify the type of tax matters involved, such as property tax or taxes on insurers, and can grant a general authorization or specific powers to their appointees. The form also outlines the extent of authority given to representatives, including the ability to receive confidential tax information, attend meetings, and execute necessary documentation on behalf of the taxpayer. Importantly, any previous powers of attorney related to the same matters are automatically revoked upon the submission of the BOE 392, simplifying matters by ensuring there is a clear and current representation. Understanding the BOE 392 form is crucial for ensuring proper representation and compliance with California tax regulations.

STATE OF CALIFORNIA |

|

POWER OF ATTORNEY / |

BOARD OF EQUALIZATION |

GENERAL AUTHORIZATION |

|

Check the appropriate Board division below. Please note that a separate form must be completed and provided to each Board division checked.

BOARD OF EQUALIZATION BOARD PROCEEDINGS DIVISION PO BOX 942879, MIC: 80 SACRAMENTO, CA

BOARD OF EQUALIZATION

TAXPAYER’S NAME

BUSINESS OR CORPORATION NAME

TELEPHONE NUMBER

FAX NUMBER

FEDERAL EMPLOYER IDENTIFICATION NUMBER

CALIFORNIA SECRETARY OF STATE NUMBER(S)

BOARD OF EQUALIZATION ACCOUNT/APPEAL NUMBER

CALIFORNIA DEPARTMENT OF TAX AND FEE ADMINISTRATION ACCOUNT (if applicable)

MAILING ADDRESS (number and street, city, state, ZIP Code)

EMAIL ADDRESS

Individual |

Partnership |

Corporation |

Limited Liability Company |

Other |

|

|

|

As owner, officer, receiver, administrator, or trustee for the taxpayer, or as a party to the tax matter before the:

Board of Equalization (BOE), or as jointly administered by the California Department of Tax and Fee Administration (CDTFA) and BOE

Board of Equalization (BOE), or as jointly administered by the California Department of Tax and Fee Administration (CDTFA) and BOE

I hereby appoint: [enter below the name(s) of the individual appointee(s), their address(es) (including ZIP Code), their telephone number(s) and fax

others, as the appointee name]

APPOINTEE NAME

APPOINTEE NAME

APPOINTEE BUSINESS NAME (if applicable)

APPOINTEE BUSINESS NAME (if applicable)

APPOINTEE ADDRESS (number and street)

APPOINTEE ADDRESS (number and street)

(city) |

(state) |

(ZIP Code) |

(city) |

(state) |

(ZIP Code) |

EMAIL ADDRESS

EMAIL ADDRESS

TELEPHONE NUMBER

FAX NUMBER

TELEPHONE NUMBER

FAX NUMBER

As

Property tax programs administered by BOE |

Tax on Insurers (jointly administered with CDTFA) |

Alcoholic Beverage Tax (jointly administered with CDTFA) |

Other: |

SPECIFY THE TAX YEAR(S) OR PERIOD(S)

(The back of this form must be completed)

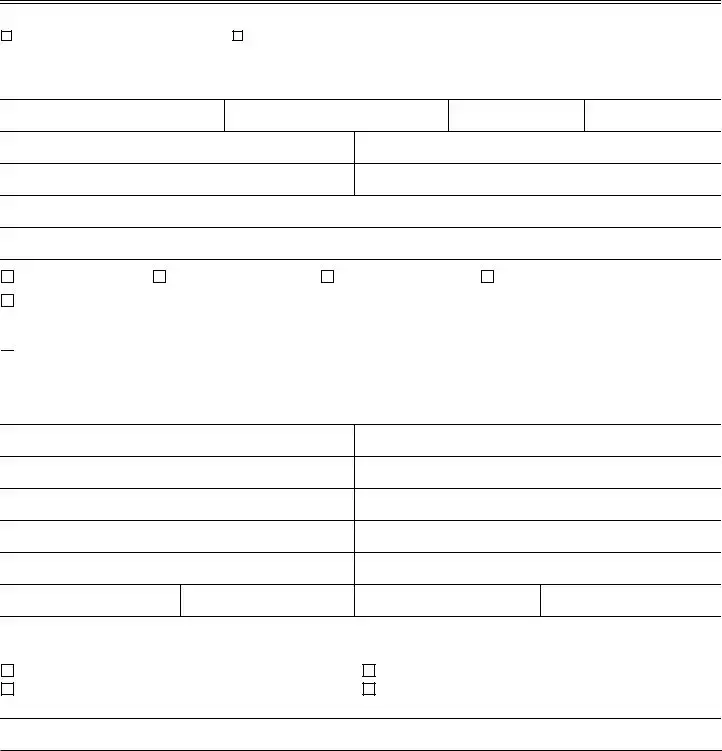

The

[check the box(es) for the power(s) granted]

General authorization (including all acts described below).

Specific authorization (selected acts described below).

To confer and resolve any assessment, claim, or collection of a deficiency or other tax matter pending before the identified Board division and attend any meetings or hearings thereto for the specified matter(s) identified above.

To receive, but not to endorse and collect, checks in payment of any refund of taxes, penalties, or interest. To execute petitions, claims for refund, and/or amendments thereto.

To execute consents extending the statutory period for assessment or determination of taxes. To delegate authority or to substitute another representative.

Other (specify):

This power of attorney/general authorization revokes all earlier power(s) of attorney/general authorizations on file with the Board of Equalization as identified above for the same matters and years or periods covered by this form, except for the following: [specify to whom granted, date and address, or refer to attached copies of earlier power(s)]

NAME

DATE POWER OF ATTORNEY/GENERAL AUTHORIZATION GRANTED

ADDRESS (number and street, city, state, ZIP Code)

Unless limited, this power of attorney will remain in effect until the final resolution of all tax matters specified herein.

(specify expiration date if limited term)

TIME LIMIT/EXPIRATION DATE (for Board of Equalization purposes)

Signature of

►IF THIS POWER OF ATTORNEY/GENERAL AUTHORIZATION IS NOT SIGNED AND DATED BY AN AUTHORIZED INDIVIDUAL, IT WILL BE RETURNED AS INVALID.

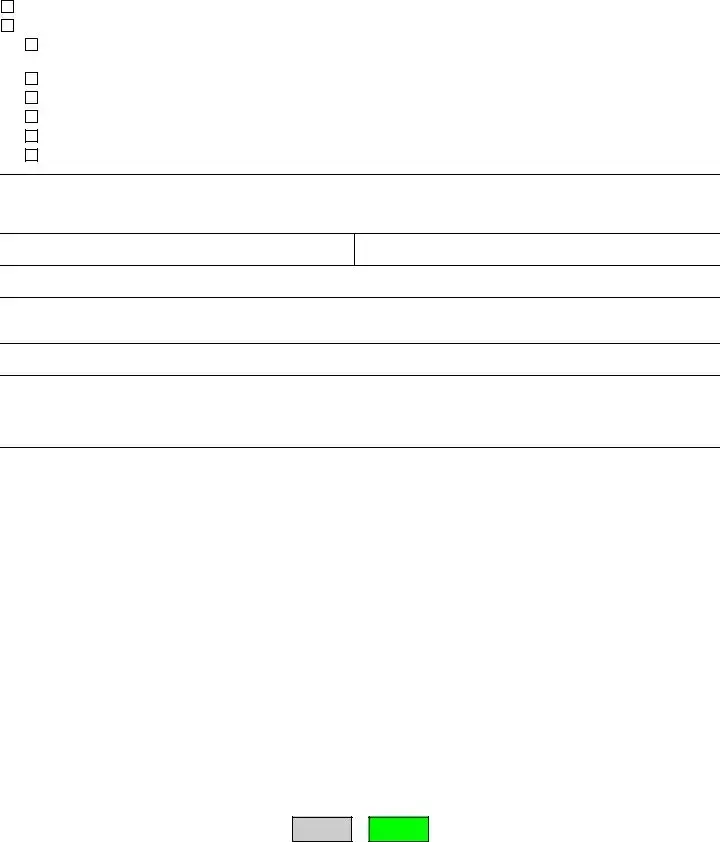

SIGNATURE |

TITLE (if applicable) |

DATE |

|

|

|

PRINT NAME |

|

TELEPHONE NUMBER |

|

|

|

SIGNATURE |

TITLE (if applicable) |

DATE |

|

|

|

PRINT NAME |

|

TELEPHONE NUMBER |

|

|

|

|

|

|

CLEAR

| Fact Name | Detail |

|---|---|

| Purpose | The BOE-392 form serves as a Power of Attorney for taxpayers, allowing designated individuals to represent them before the California State Board of Equalization. |

| Completion Requirements | Each Board division that the taxpayer seeks representation for requires a separate BOE-392 form to be filled out. |

| Governing Laws | The use and guidelines for the BOE-392 are established under California Revenue and Taxation Code, specifically regarding tax powers and representation. |

| Duration of Authorization | This Power of Attorney remains effective until the final resolution of the specified tax matters, unless an expiration date is provided. |

| Revocation Clause | Submitting a new BOE-392 form automatically revokes all prior Power of Attorney designations related to the same matters and time periods. |

Filling out the BOE-392 form requires attention to detail to ensure accuracy. This form is crucial for granting authority to another individual regarding tax matters. Follow these steps to properly complete the form and submit it appropriately.

The BOE-392 form is a Power of Attorney/General Authorization form issued by the California Board of Equalization (BOE). It allows a taxpayer to appoint an individual or individuals to act on their behalf in tax matters involving specific divisions of the BOE.

This form is necessary for individuals, partnerships, corporations, or limited liability companies. If someone wishes to authorize a representative to handle tax-related matters with the BOE, they should complete this form. It's particularly useful when dealing with complex tax issues or when the taxpayer cannot attend meetings in person.

The form requires various types of information to be filled out, including:

Yes, you can appoint multiple individuals as representatives on a single BOE-392 form. However, it's crucial to ensure that each representative's details are filled out accurately to avoid any potential issues.

The BOE-392 form encompasses a variety of tax matters including:

The authority granted through the BOE-392 form typically continues until the final resolution of all specified tax matters. If there is a need to impose a time limit, that must be specified on the form.

Yes, if the tax matter involves a joint return, both spouses must sign the BOE-392 form. This ensures that both parties authorize the appointed representative to act on their behalf.

If the BOE-392 form is not signed and dated by an authorized individual, it will be considered invalid and returned. It is vital that the individual signing the form has the authority to represent the taxpayer.

Yes, the BOE-392 form automatically revokes any previous power of attorney or authorization that overlaps with the matters and tax years specified in the new form. If there are previous authorizations that should remain valid, those must be explicitly indicated on the form.

The completed form should be mailed to the appropriate Board division you are dealing with. The mailing addresses are provided at the top of the form, along with other contact details for the specific divisions of the BOE.

When filling out the BOE-392 form, individuals often make several common mistakes that can lead to delays or complications. One frequent error involves not checking the appropriate Board division at the beginning of the form. It’s critical to ensure that the right division is selected based on the tax matter being addressed. Each division requires a separate submission, so skipping this step can result in invalid submissions. Make sure to review your selection and understand the implications of each division listed.

Another prevalent mistake is related to the incomplete or incorrect information about the taxpayer. Individuals sometimes provide inaccurate business names, telephone numbers, or federal employer identification numbers. Each of these details is vital for the Board of Equalization to process the form effectively. Double-check all entries to ensure they match your official records. Incorrect information can lead to delays in processing or even rejection of the form.

Additionally, many people neglect to complete the back of the form, which is just as essential as the front. The back section includes important authorizations that outline what the representative can do on behalf of the taxpayer. Skipping this step can undermine the authority granted and hinder the representative's ability to act effectively. Always ensure that both sides of the form are filled out thoroughly.

Another common oversight occurs when individuals fail to specify the tax matter and the relevant tax years or periods. Not clearly identifying the tax type or the period can create confusion and delays in resolution. Each matter has its particular requirements, so it's imperative to specify what you are addressing to streamline the process. Be explicit about the tax year or period to avoid any ambiguity.

Lastly, many forms are submitted without the required signature and date. The form will be deemed invalid without a proper signature from the taxpayer or authorized individual. This is a crucial step, especially if the matter involves joint representation, where both parties must sign. Don’t overlook this detail; ensure that all necessary signatures are prominently included before submission.

The BOE-392 form, a Power of Attorney used in California for tax-related matters, often requires accompanying documentation to ensure clarity and compliance with legal processes. Here are some other forms and documents frequently used alongside the BOE-392 form.

Incorporating these forms can help ensure that the appropriate representatives handle tax matters effectively, reducing errors and streamlining communications with the Board of Equalization. It's essential for taxpayers to understand which documents are needed for their specific situations to maintain compliance and protect their interests.

Form 2848 (Power of Attorney and Declaration of Representative): This document allows taxpayers to authorize an individual to represent them before the IRS. Similar to the BOE 392, it grants broad authority to the appointed representative for tax matters. Both forms require specific details about the taxpayer and appointee to ensure proper representation.

Form 8821 (Tax Information Authorization): While not a power of attorney, Form 8821 allows individuals to authorize the IRS to disclose their tax information to a designated person. Like the BOE 392, it is about managing authority concerning tax matters, but it does not allow the appointed person to act on the taxpayer's behalf.

California Form 3538 (Payment of Property Taxes): This form is similar as it deals with property tax matters within California. While the BOE 392 allows for representation in tax matters, Form 3538 is more focused on actual payment and administrative functions related to property taxes.

Form 4506 (Request for Copy of Tax Return): This form allows a taxpayer to request copies of their previous tax returns. Similar to the BOE 392 in terms of authorizing an individual to handle specific tax-related processes, both documents highlight the importance of authorized persons in managing tax documentation and obligations.

When filling out the BOE-392 form, it is important to follow specific guidelines to ensure accuracy and compliance. Here are ten things you should and shouldn’t do:

Understanding the BOE 392 form can be complex, leading to some common misconceptions. Here are seven misunderstandings about this important document:

Addressing these misconceptions can help individuals and entities navigate their tax representation needs more effectively. If there are any uncertainties, seeking guidance may prove beneficial.

Filling out and using the BOE-392 form is an important process for anyone involved in tax matters with the State of California. Here are some key takeaways to keep in mind:

Using the BOE-392 form correctly ensures that your tax matters are handled efficiently and that your rights are protected. Double-check all information before submission to avoid delays.