The BOS DTF-802 form plays a vital role in the realm of tax compliance for businesses in the United States. This form is specifically designed to facilitate the reporting and documentation of tax obligations, ensuring that organizations adhere to federal and state tax regulations. Individuals and businesses alike must navigate the complexities of tax codes, and the BOS DTF-802 provides a structured way to capture important financial data. Key information required on the form may include identification details, income statements, and deductions. Accurate completion of the BOS DTF-802 is essential not only for meeting legal requirements but also for optimizing potential tax benefits and avoiding penalties. Understanding this form empowers businesses to manage their tax responsibilities effectively, ensuring compliance and fostering financial health.

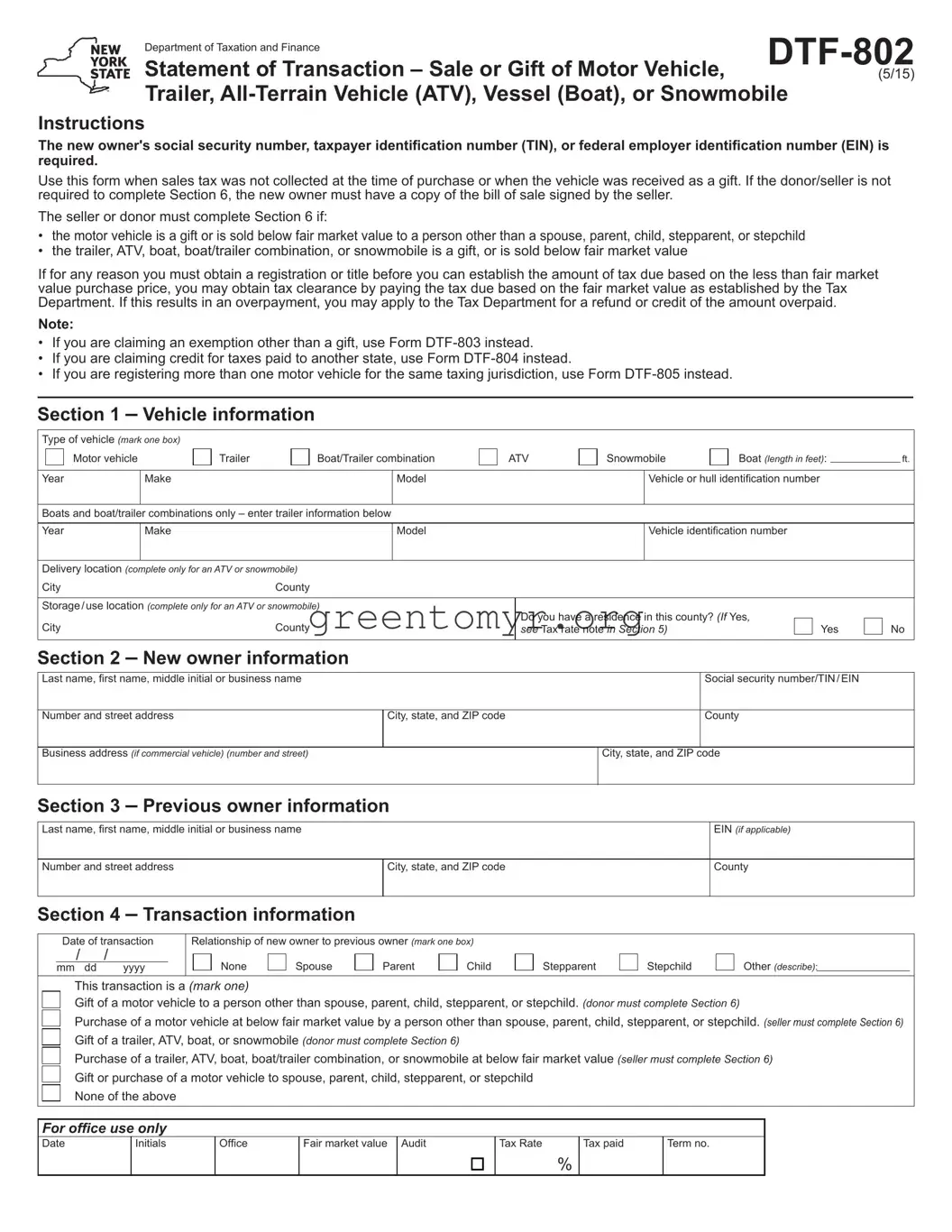

Department of Taxation and Finance

Statement of Transaction – Sale or Gift of Motor Vehicle,

Trailer,

Instructions

The new owner's social security number, taxpayer identification number (TIN), or federal employer identification number (EIN) is required.

Use this form when sales tax was not collected at the time of purchase or when the vehicle was received as a gift. If the donor/seller is not required to complete Section 6, the new owner must have a copy of the bill of sale signed by the seller.

The seller or donor must complete Section 6 if:

•the motor vehicle is a gift or is sold below fair market value to a person other than a spouse, parent, child, stepparent, or stepchild

•the trailer, ATV, boat, boat/trailer combination, or snowmobile is a gift, or is sold below fair market value

If for any reason you must obtain a registration or title before you can establish the amount of tax due based on the less than fair market value purchase price, you may obtain tax clearance by paying the tax due based on the fair market value as established by the Tax Department. If this results in an overpayment, you may apply to the Tax Department for a refund or credit of the amount overpaid.

Note:

•If you are claiming an exemption other than a gift, use Form

•If you are claiming credit for taxes paid to another state, use Form

•If you are registering more than one motor vehicle for the same taxing jurisdiction, use Form

Section 1 – Vehicle information

Type of vehicle (mark one box) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

Motor vehicle |

|

Trailer |

|

|

Boat/Trailer combination |

|

|

ATV |

|

Snowmobile |

|

|

Boat (length in feet): |

|

|

ft. |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Year |

|

Make |

|

|

|

|

|

|

Model |

|

|

|

|

Vehicle or hull identification number |

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Boats and boat/trailer combinations only – enter trailer information below |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Year |

|

Make |

|

|

|

|

|

|

Model |

|

|

|

|

Vehicle identification number |

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Delivery location (complete only for an ATV or snowmobile) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

City |

|

|

|

County |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Storage/use location (complete only for an ATV or snowmobile) |

|

Do you have a residence in this county? (If Yes, |

|

|

|

|

|

|

|||||||||||||||||||

City |

|

|

|

County |

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

see Tax rate note in Section 5) |

|

|

|

|

Yes |

|

No |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Section 2 – New owner information |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

Last name, first name, middle initial or business name |

|

|

|

|

|

|

|

|

|

|

Social security number/TIN/EIN |

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

Number and street address |

|

|

|

|

|

City, state, and ZIP code |

|

|

|

|

|

County |

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

Business address (if commercial vehicle) (number and street) |

|

|

|

|

|

|

|

|

City, state, and ZIP code |

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

Section 3 – Previous owner information |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

Last name, first name, middle initial or business name |

|

|

|

|

|

|

|

|

|

|

|

EIN (if applicable) |

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

Number and street address |

|

|

|

|

|

City, state, and ZIP code |

|

|

|

|

|

|

County |

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Section 4 – Transaction information

Date of transaction

/ /

mm dd yyyy

Relationship of new owner to previous owner (mark one box)

None |

|

Spouse |

|

Parent |

|

Child |

Stepparent

Stepchild

Other (describe):

This transaction is a (mark one)

Gift of a motor vehicle to a person other than spouse, parent, child, stepparent, or stepchild. (donor must complete Section 6)

Purchase of a motor vehicle at below fair market value by a person other than spouse, parent, child, stepparent, or stepchild. (seller must complete Section 6) Gift of a trailer, ATV, boat, or snowmobile (donor must complete Section 6)

Purchase of a trailer, ATV, boat, boat/trailer combination, or snowmobile at below fair market value (seller must complete Section 6) Gift or purchase of a motor vehicle to spouse, parent, child, stepparent, or stepchild

None of the above

For office use only

Date

Initials

Office

Fair market value Audit

Tax Rate

%

Tax paid

Term no.

Page 2 of 2

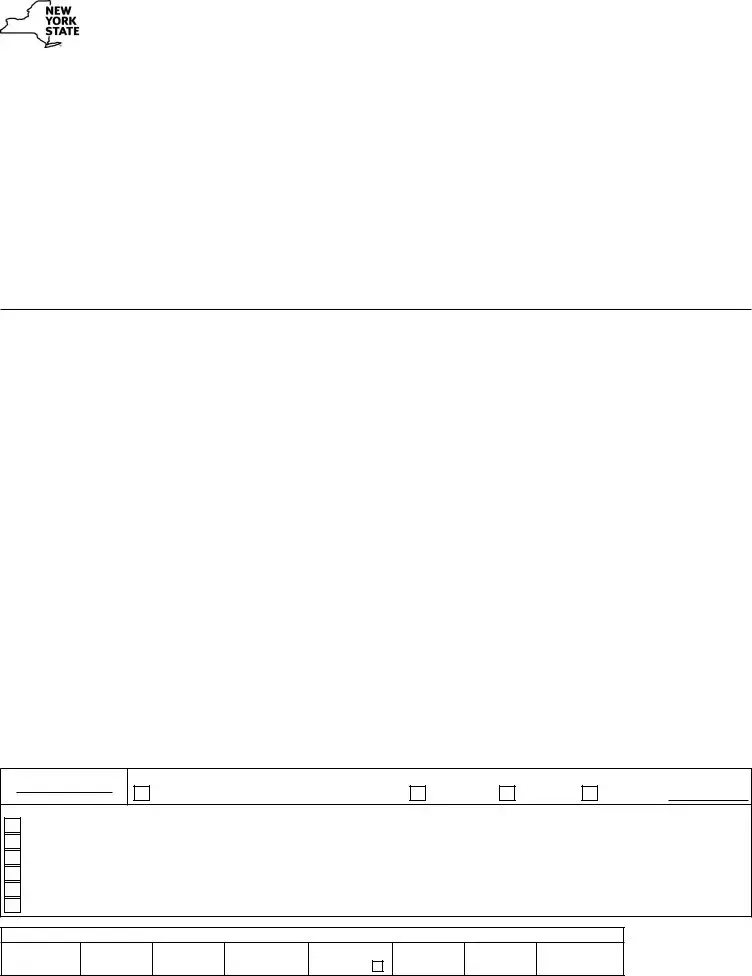

Section 5 – Purchase information

1 Purchase price |

|

Value |

|

a. Amount of cash payment |

1a |

$ |

|

b. Balance of payments assumed |

1b |

$ |

|

c. Value of property given, traded, or swapped, or services performed instead of cash payment... |

1c |

$ |

|

.......................................................................................................d. Purchase price (total of lines 1a, 1b, and 1c) |

|

1d |

$ |

Boats and boat/trailer combinations: For purchases or uses on or after June 1, 2015, tax only applies to the first $230,000 of the purchase price. Do not enter more than $230,000 on line 1d.

2Was this transaction the purchase or gift of a motor vehicle

|

from your spouse, parent, child, stepparent, or stepchild? |

|

|

Yes (enter 0 on line 4; no tax is due) |

|

No (continue to line 3) |

||

3 |

Tax rate* (enter as a decimal) |

|

|

|

|

|

|

|

|

|

|

|

3 |

|

|||

4 |

..................................................................................................................Sales tax due (multiply line 1d by line 3) |

|

|

|

|

4 |

$ |

|

5Is the amount on line 1d lower than fair market value?

* |

|

|

Yes (seller/donor must complete Section 6) |

|

No (sign certification below) |

|

N/A (Sale of boat for more than $230,000) |

Tax rate note: For a motor vehicle, trailer, boat, or boat/trailer combination use the tax rate of the new owner's place of residence. If the purchaser is a resident in two |

|||||||

or more counties in the state, use the rate in effect in the place where the motor vehicle, trailer, boat, or boat/trailer combination will be principally used or garaged. If the new owner is a business, use the tax rate of the place of business. If the business has locations in two or more counties in the state, use the rate in effect in the place where the motor vehicle, trailer, or boat will be principally used or garaged. For an ATV or snowmobile, use the higher rate of where the new owner took delivery, or where the vehicle is stored or used if new owner has a residence in storage/use locality.

Purchaser certification – I certify that the above statements are true and complete; and I make these statements with the knowledge that willfully issuing a false or fraudulent statement with the intent to evade tax is a misdemeanor under Tax Law section 1817(b), and Penal Law section 210.45, punishable by a fine up to $10,000 for an individual and $20,000 for a corporation.

Signature

Date

If this form is submitted by someone other than the new owner/lessee, provide the following:

Name/business name

Social security number, TIN, or federal EIN

Address

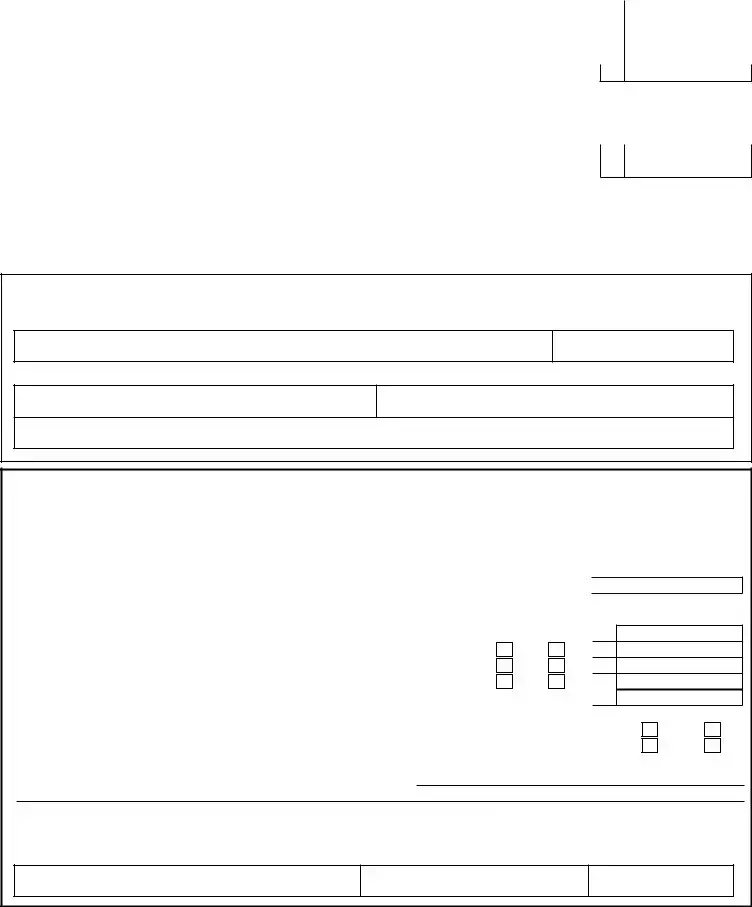

Section 6 – Affidavit of sale or gift of a motor vehicle, trailer, ATV, vessel (boat), or snowmobile

The seller or donor must complete if:

•the motor vehicle is a gift to a person other than a spouse, parent, child, stepparent, or stepchild

•the motor vehicle is sold below fair market value to a person other than a spouse, parent, child, stepparent, or stepchild

•the trailer, ATV, boat, or snowmobile is a gift

•the trailer, ATV, boat, boat/trailer combination, or snowmobile is sold below fair market value

6 Cash payment received |

6 |

$ |

7If, as a condition for the sale or gift of the vehicle or boat, the purchaser/recipient did any of the following in addition to, or in lieu of, a cash payment, mark an X in the appropriate box and indicate the value of the service or goods you received.

Value

a Performed any service |

Yes |

No |

7a $ |

|

b Assumed any debt |

Yes |

No |

7b $ |

|

c Traded/swapped a vehicle or other property |

Yes |

No |

7c $ |

|

d Total selling price (total of lines 6, 7a, 7b and 7c) |

|

|

|

|

|

7d $ |

|||

8Complete only if a corporation or business is the seller/donor

a |

Was or is the purchaser/recipient an employee, officer, or stockholder of the company/corporation? |

Yes |

b |

Was the transaction part of any terms of employment, employment contract, or termination agreement? |

Yes |

9If you answered Yes to any part of line 7 or line 8, provide an explanation:

No No

Seller/Donor certification – I have reviewed the information on Form

Signature

Name (printed or typed)

Date

Privacy notification – See our Web site at www.tax.ny.gov or Publication 54, Privacy Notification.

| Fact Name | Description |

|---|---|

| Form Purpose | The BOS DTF-802 form is used for tax reporting in specific situations, primarily related to sales and use tax in New York State. |

| Governing Law | This form is governed by New York State Tax Law, particularly under Title 11 of Article 28. |

| Submission Requirement | Businesses are required to submit this form depending on their sales tax obligations and filing status. |

| Tax Identification | The form requests a taxpayer identification number, ensuring proper identification of the entity involved. |

| Use Case | Commonly utilized for purchases involving certain exemptions from sales tax, such as certain goods or services. |

| Form Availability | The BOS DTF-802 form can be accessed online through the New York State Department of Taxation and Finance website. |

| Filing Method | Forms can typically be filed electronically or printed and mailed, depending on the specific instructions provided by the state. |

| Record Keeping | Taxpayers are advised to keep copies of the form and any documentation for at least three years for audit purposes. |

| Common Mistakes | Failing to complete all required sections or providing incorrect tax ID information can lead to processing delays. |

| Deadline | There are specific deadlines for submitting the BOS DTF-802 form, which align with the taxpayer's overall filing requirements. |

Filling out the BOS DTF-802 form is an important process that individuals and businesses may need to complete for various administrative reasons. Following the right steps will help ensure accuracy and completeness, ultimately aiding in a smooth submission process. Here’s how you can fill out the form correctly.

After submission, you may want to keep a copy of the completed form for your records. Doing so helps maintain clarity in any future correspondence related to the matter at hand.

The BOS DTF-802 form is a document used in the business and tax sectors. It serves specific purposes related to tax obligations in certain contexts, often covering various types of tax assessments or credits.

Typically, businesses or individuals involved in specific taxable activities must complete this form. This may include those who are filing for tax exemptions or seeking special treatment under certain tax regulations.

The due date for the BOS DTF-802 form generally aligns with your tax filing deadlines. For many, this is the same as their regular income tax filing deadline, but check the specific guidelines for your situation to be sure.

You can usually find the BOS DTF-802 form on the official website of your local tax authority or state’s department of taxation. It might also be available through tax preparation services or accountants.

To fill out the form, start by gathering all necessary financial information related to your tax situation. Follow the instructions carefully, and ensure that you fill in all required fields accurately. You may want assistance from a tax professional if you find any section confusing.

Some jurisdictions may allow e-filing for the BOS DTF-802 form, while others may require a paper submission. Check with your local tax authority to see what options are available to you.

If you realize you made a mistake after submitting the form, it’s important to correct it. You can typically do this by filing an amendment or correction form, depending on the guidelines provided by your tax authority.

Filing the BOS DTF-802 form itself may not incur a direct fee. However, if hiring a tax professional to assist you, there could be associated costs. Always check with your local tax authority for any potential fees related to your specific situation.

The submission address for the BOS DTF-802 form depends on your local tax authority's guidelines. Generally, it may be submitted electronically through their online portal, by mail, or in person at designated offices.

If you need help, consider these resources:

When filling out the BOS DTF-802 form, individuals often encounter a variety of challenges that can lead to mistakes. One common error is neglecting to provide complete and accurate contact information. This includes not only names and addresses but also phone numbers and email addresses. Omitting these vital details can delay processing or lead to communication issues.

Another frequent mistake involves misunderstanding the requirements for supporting documentation. Applicants may not realize that specific forms of identification or proof of eligibility are necessary for their applications to be accepted. Missing documentation can result in considerable delays or even the outright rejection of an application.

People sometimes fail to thoroughly read the instructions accompanying the form. Skipping this crucial step can lead to incorrect or incomplete entries. Each section of the BOS DTF-802 has detailed guidelines that are designed to assist in accurate completion. Ignoring these can lead to errors that often prove costly and time-consuming to rectify.

Additionally, errors in financial information are quite common. Applicants might enter incorrect amounts or make mathematical errors when calculating totals. Such discrepancies can raise red flags during the review process, requiring additional clarification and potentially slowing down approval.

Moreover, individuals may not date their forms correctly. While this might seem trivial, submitting a form without a date can be seen as an incomplete submission. Every signature and each section should reflect the date of completion to ensure everything is processed smoothly.

Finally, many people overlook the final review stage before submitting their forms. Taking an extra moment to check for errors in spelling, grammar, and missing signatures can make a significant difference. A thorough final check helps to ensure that all requirements are met, reducing the likelihood of needing to resubmit the form.

The BOS DTF-802 form is an essential document used primarily for tax purposes, particularly concerning the sale or transfer of vehicles in New York State. In conjunction with this form, there are several other documents that often accompany it. Below is a list of some commonly used forms and documents that you may encounter when dealing with vehicle transactions.

Understanding these accompanying forms can significantly enhance the vehicle transfer process, ensuring that all legal requirements are met and that both the buyer and seller are adequately protected. It is always advisable to double-check with local regulations to ensure compliance and to gather all necessary documentation before finalizing any vehicle transaction.

The BOS DTF-802 form serves specific purposes within the realm of legal and financial documentation. There are several documents that share similarities with the BOS DTF-802 form, primarily in terms of function or information required. Here’s a list highlighting six comparable documents:

When filling out the BOS DTF-802 form, it's essential to approach the task with care and attention to detail. Here’s a guide on what you should and shouldn’t do:

These tips can help ensure a smoother filing process and reduce the chances of any issues arising later on.

The BOS DTF-802 form is often misunderstood. Below are eight common misconceptions about this form.

Understanding these misconceptions can help individuals navigate the complexities associated with the BOS DTF-802 form more successfully.

When filling out and using the BOS DTF-802 form, keep the following key points in mind:

Taking the time to carefully complete the BOS DTF-802 form can significantly impact your financial situation. Your attention to detail is crucial for a smooth process.