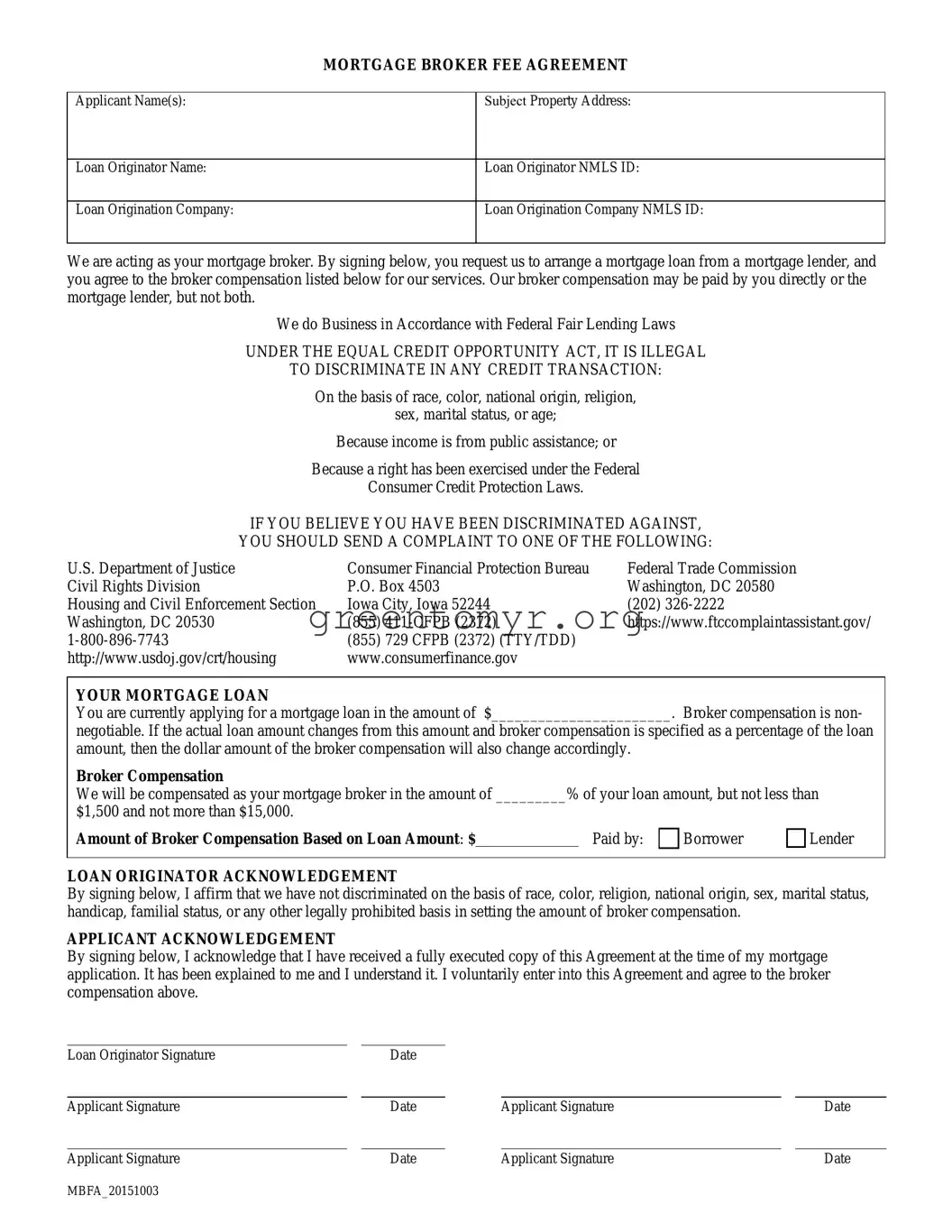

The Broker Fee Agreement form is a crucial document in the mortgage application process, helping to clarify the relationship between the applicant and the mortgage broker. This form outlines essential details such as the names of the applicants, the subject property address, and identifies the loan originator along with their credentials. At its core, the form specifies that by signing, the applicants authorize the broker to arrange a mortgage loan on their behalf while agreeing to the broker's compensation, which is clearly defined and non-negotiable. Importantly, it is highlighted that the broker's compensation may be paid either by the borrower or the lender, but not both. The form reinforces compliance with federal fair lending laws, emphasizing the prohibition against discrimination in credit transactions. If any applicant believes they have faced discrimination, the form provides clear channels for filing complaints with relevant governmental institutions. Ultimately, this agreement ensures that all parties involved understand their rights and responsibilities, paving the way for a transparent and fair mortgage lending experience.

|

MORTGAGE BROKER FEE AGREEMENT |

|

|

|

|

Applicant Name(s): |

|

Subject Property Address: |

|

|

|

Loan Originator Name: |

|

Loan Originator NMLS ID: |

|

|

|

Loan Origination Company: |

|

Loan Origination Company NMLS ID: |

|

|

|

We are acting as your mortgage broker. By signing below, you request us to arrange a mortgage loan from a mortgage lender, and you agree to the broker compensation listed below for our services. Our broker compensation may be paid by you directly or the mortgage lender, but not both.

We do Business in Accordance with Federal Fair Lending Laws

UNDER THE EQUAL CREDIT OPPORTUNITY ACT, IT IS ILLEGAL

TO DISCRIMINATE IN ANY CREDIT TRANSACTION:

On the basis of race, color, national origin, religion,

sex, marital status, or age;

Because income is from public assistance; or

Because a right has been exercised under the Federal

Consumer Credit Protection Laws.

IF YOU BELIEVE YOU HAVE BEEN DISCRIMINATED AGAINST,

YOU SHOULD SEND A COMPLAINT TO ONE OF THE FOLLOWING:

U.S. Department of Justice |

Consumer Financial Protection Bureau |

Federal Trade Commission |

|

Civil Rights Division |

P.O. Box 4503 |

Washington, DC 20580 |

|

Housing and Civil Enforcement Section |

Iowa City, Iowa 52244 |

(202) |

|

Washington, DC 20530 |

(855) |

https://www.ftccomplaintassistant.gov/ |

|

(855) |

729 CFPB (2372) (TTY/TDD) |

|

|

http://www.usdoj.gov/crt/housing |

www.consumerfinance.gov |

|

|

YOUR MORTGAGE LOAN

You are currently applying for a mortgage loan in the amount of $_______________________. Broker compensation is non-

negotiable. If the actual loan amount changes from this amount and broker compensation is specified as a percentage of the loan amount, then the dollar amount of the broker compensation will also change accordingly.

Broker Compensation

We will be compensated as your mortgage broker in the amount of _________% of your loan amount, but not less than

$1,500 and not more than $15,000.

Amount of Broker Compensation Based on Loan Amount: $ |

|

Paid by: |

Borrower |

Lender |

LOAN ORIGINATOR ACKNOWLEDGEMENT

By signing below, I affirm that we have not discriminated on the basis of race, color, religion, national origin, sex, marital status, handicap, familial status, or any other legally prohibited basis in setting the amount of broker compensation.

APPLICANT ACKNOWLEDGEMENT

By signing below, I acknowledge that I have received a fully executed copy of this Agreement at the time of my mortgage application. It has been explained to me and I understand it. I voluntarily enter into this Agreement and agree to the broker compensation above.

Loan Originator Signature |

|

Date |

|

|

|

|

|

|

|

|

|

|

|

Applicant Signature |

|

Date |

|

Applicant Signature |

|

Date |

|

|

|

|

|

|

|

Applicant Signature |

|

Date |

|

Applicant Signature |

|

Date |

MBFA_20151003

| Fact Name | Details |

|---|---|

| Purpose of the Form | This agreement outlines the terms under which a mortgage broker will be compensated for their services in arranging a mortgage loan for the applicant. |

| Broker Compensation | The broker's compensation is non-negotiable and is specified as a percentage of the loan amount. It ranges from a minimum of $1,500 to a maximum of $15,000 depending on the loan size. |

| Payment Responsibility | Broker compensation can be paid either directly by the borrower or by the lender, but it cannot be paid by both parties. |

| Equal Credit Opportunity Act | This form emphasizes compliance with the Equal Credit Opportunity Act, which prohibits discrimination in credit transactions based on various protected characteristics. |

| Receiver of Complaints | If applicants believe they have experienced discrimination, they can file a complaint with agencies including the U.S. Department of Justice and the Consumer Financial Protection Bureau. |

Filling out the Broker Fee Agreement form is a crucial step in the mortgage application process. This form outlines the agreement between you and the mortgage broker regarding the fee you will incur for their services. Getting it right is essential, as it ensures clear communication between all parties involved.

A Broker Fee Agreement is a document that outlines the relationship and compensation between a borrower and a mortgage broker. By signing this agreement, you are requesting the broker to arrange a mortgage loan on your behalf. It also details how the broker will be compensated for their services, which may come from either you or the lender, but not both.

The Broker Fee Agreement must be signed by all applicants seeking a mortgage loan. Additionally, the loan originator representing the mortgage broker also signs the agreement to confirm their understanding and commitment to the terms laid out within it.

The broker compensation is typically structured as a percentage of the total loan amount. Specifically, the document states that the broker will receive an amount between $1,500 and $15,000. The exact percentage and total will be specified in the agreement. If the loan amount changes, the broker compensation amount, calculated as a percentage, will also adjust accordingly.

No, the broker compensation outlined in the Broker Fee Agreement is non-negotiable. It's important to thoroughly review this section of the agreement before signing to ensure you are comfortable with the terms.

If you believe that you have faced discrimination in your credit transaction based on race, color, religion, national origin, sex, marital status, handicap, familial status, or any other legally protected basis, it is important to take action. You can file a complaint with one of the following organizations:

Each organization has specific procedures for submitting complaints, which can usually be found on their respective websites.

Upon signing the Broker Fee Agreement, you should receive a fully executed copy for your records. Review it carefully to ensure that you understand the agreed terms. It can be beneficial to keep this document accessible throughout the mortgage application process, as it outlines your rights and obligations.

The agreement references the Equal Credit Opportunity Act, a federal law designed to prevent discrimination in lending. This law makes it illegal to discriminate against a borrower on various grounds, including race, color, national origin, religion, sex, marital status, or age. Understanding these protections can empower you as a borrower and help you identify any unfair practices.

Filling out a Broker Fee Agreement may seem straightforward, but several common mistakes can lead to confusion or complications. Being aware of these pitfalls can help ensure a smoother loan process. One of the most frequent errors occurs when applicants fail to fill in the Applicant Name(s). This section is critical, as it identifies who is entering into the agreement. Leaving this blank makes it challenging to establish a clear record of the parties involved in the agreement.

Another common mistake is neglecting to specify the Loan Amount. Without this information, the broker team cannot provide accurate compensation estimates or details. It is essential to enter both the dollar amount and recognize that broker compensation may vary based on the final loan amount. Misunderstanding this concept can lead to surprises if the actual loan amount changes.

Additionally, applicants often overlook the importance of completing the Broker Compensation section. This area clarifies what the broker will be paid for handling your loan. Many individuals mistakenly believe that just signing the agreement concludes their financial obligation, but it’s crucial to understand and agree upon the specific compensation terms. Not specifying whether the payment is made by the borrower or lender can create further misunderstandings.

The Loan Originator Signature is another critical part that applicants might forget. Without the loan originator's signature, the agreement lacks verification from the broker. This omission could potentially render the agreement invalid and complicate future communications. Signing ensures that all parties understand and accept the terms.

Finally, applicants should remember to sign the document smoothly. Many people rush through the Applicant Acknowledgment section, where they confirm understanding and acceptance of the agreement. Skipping this can result in a lack of clarity regarding the responsibilities and obligations outlined in the agreement. Careful review and thoughtful signing mitigate potential issues down the line.

The Broker Fee Agreement is a critical document in the mortgage process, establishing the compensation that a broker will receive for their services in arranging a mortgage loan. Several other forms and documents often accompany this agreement to facilitate transparency and compliance during the loan application process.

Each of these documents plays a significant role in the mortgage process, aimed at promoting informed decision-making among borrowers and protecting all parties involved in the transaction. Completing these forms accurately and understanding their implications is essential for a successful mortgage application.

Here are ten documents that have similarities to the Broker Fee Agreement form. Each document shares certain elements regarding agreements and compensation in financial transactions. Understanding these can help clarify the purpose and nature of the Broker Fee Agreement.

When filling out the Broker Fee Agreement form, attention to detail is crucial. Here is a list outlining important dos and don'ts to consider during the process: