The Monthly Household Budget Worksheet is a vital tool designed to help individuals and families manage their finances effectively. This comprehensive form allows users to document essential monthly payments and expenses across various categories, making it easier to track where money is going and identify potential areas for savings. Each section of the form covers critical aspects of a household's financial obligations, including housing payments, transportation costs, and personal entertainment expenses. By breaking down these categories, users can gain insights into their spending habits and pinpoint areas where expenses might be reduced. The form emphasizes the importance of careful review and completion, encouraging check marks next to any areas where expense reductions are possible. This proactive approach not only aids in personal financial management but also assists service providers in finding ways to help individuals maintain their homes. With sections dedicated to food, family expenses, insurance, legal obligations, and more, the form culminates in a total calculation that highlights the overall financial picture. Urgent attention to this form can lead to significant adjustments in budgeting strategies, enabling households to achieve greater financial stability.

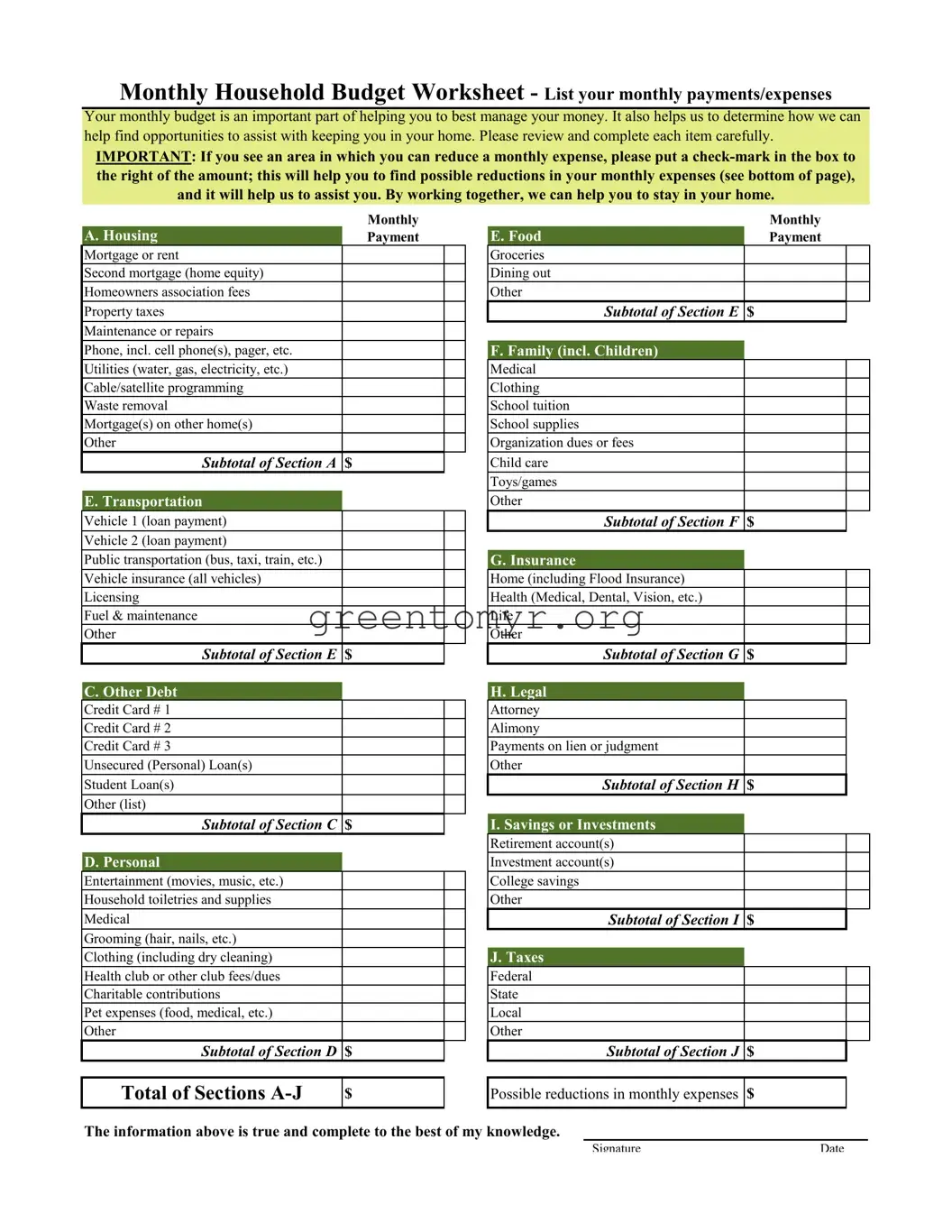

Monthly Household Budget Worksheet - List your monthly payments/expenses

Your monthly budget is an important part of helping you to best manage your money. It also helps us to determine how we can help find opportunities to assist with keeping you in your home. Please review and complete each item carefully.

IMPORTANT: If you see an area in which you can reduce a monthly expense, please put a

|

|

Monthly |

|

|

A. Housing |

Payment |

|

|

Mortgage or rent |

|

|

|

Second mortgage (home equity) |

|

|

|

Homeowners association fees |

|

|

|

Property taxes |

|

|

|

|

|

|

|

Maintenance or repairs |

|

|

|

Phone, incl. cell phone(s), pager, etc. |

|

|

|

Utilities (water, gas, electricity, etc.) |

|

|

|

Cable/satellite programming |

|

|

|

Waste removal |

|

|

|

Mortgage(s) on other home(s) |

|

|

|

Other |

|

|

SUBTOTAL OF SECTION A $

E.Transportation

Vehicle 1 (loan payment) Vehicle 2 (loan payment)

Public transportation (bus, taxi, train, etc.) Vehicle insurance (all vehicles) Licensing

Fuel & maintenance Other

SUBTOTAL OF SECTION E $

C. Other Debt

Credit Card # 1

Credit Card # 2

Credit Card # 3

Unsecured (Personal) Loan(s)

Student Loan(s)

Other (list)

SUBTOTAL OF SECTION C $

D. Personal

Entertainment (movies, music, etc.)

Household toiletries and supplies

Medical

Grooming (hair, nails, etc.)

Clothing (including dry cleaning)

Health club or other club fees/dues

Charitable contributions

Pet expenses (food, medical, etc.)

Other

SUBTOTAL OF SECTION D $

|

Monthly |

|

E. Food |

Payment |

|

Groceries |

|

|

Dining out |

|

|

Other |

|

|

SUBTOTAL OF SECTION E |

$ |

|

|

|

|

F. Family (incl. Children) |

|

|

Medical |

|

|

Clothing |

|

|

School tuition |

|

|

School supplies |

|

|

Organization dues or fees |

|

|

Child care |

|

|

Toys/games |

|

|

Other |

|

|

SUBTOTAL OF SECTION F |

$ |

|

|

|

|

G. Insurance |

|

|

Home (including Flood Insurance) |

|

|

Health (Medical, Dental, Vision, etc.) |

|

|

Life |

|

|

Other |

|

|

SUBTOTAL OF SECTION G |

$ |

|

|

|

|

H. Legal |

|

|

Attorney |

|

|

Alimony |

|

|

Payments on lien or judgment |

|

|

Other |

|

|

SUBTOTAL OF SECTION H |

$ |

|

|

|

|

I. Savings or Investments |

|

|

Retirement account(s) |

|

|

Investment account(s) |

|

|

College savings |

|

|

Other |

|

|

SUBTOTAL OF SECTION I |

$ |

|

|

|

|

J. Taxes |

|

|

Federal |

|

|

State |

|

|

Local |

|

|

Other |

|

|

SUBTOTAL OF SECTION J |

$ |

|

Total of Sections

$

Possible reductions in monthly expenses

$

The information above is true and complete to the best of my knowledge.

SignatureDate

| Fact Name | Description |

|---|---|

| Purpose of the Budget Form | This form is designed to help individuals list their monthly payments and expenses. It serves as a tool to manage finances effectively and identify potential areas of expense reduction. |

| Importance in Housing Assistance | Completing the budget form may aid in determining eligibility for services or assistance programs aimed at helping individuals maintain their housing. This can be crucial for those facing financial challenges. |

| Sections Included | The budget worksheet includes various sections for housing, transportation, debts, entertainment, food, family expenses, insurance, legal fees, savings, and taxes, allowing for a comprehensive overview of monthly finances. |

| Impact of Expense Reduction | Identifying areas where expenses can be reduced is encouraged. A checkbox is provided to indicate possible reductions, thus facilitating discussions about financial strategies and support. |

Completing your monthly budget form is an essential step in managing your finances effectively. By providing a clear snapshot of your income and expenses, you enable yourself and those helping you to identify areas where adjustments can be made. With careful attention, you can ensure that your budget reflects your actual financial situation, paving the way for potential assistance in keeping you in your home.

The Monthly Household Budget Worksheet is designed to help individuals and families manage their finances effectively. By listing and organizing all monthly expenses, it not only provides a clear picture of your financial situation but also identifies areas where savings can be made. This is particularly useful for those seeking assistance to maintain their housing situation. The information collected through the budget form can guide financial counseling and support services that may be available to you.

In the housing section, you will need to detail all housing-related expenses. This includes not only your mortgage or rent but also other costs associated with your home such as property taxes, homeowners association fees, and maintenance or repair expenses. Take your time to check each expense item name, and where applicable, provide specific amounts. If you find any expenses that can be reduced, be sure to mark them with a check, as this will aid in identifying potential savings.

When completing the transportation section, list all expenses related to vehicle ownership and public transport. This should cover items such as loan payments for your vehicles, insurance, fuel, maintenance, and any public transportation fare you regularly incur. If you own multiple vehicles, ensure that you include the costs for each one. Keeping these details accurate will help provide a more comprehensive overview of your finances.

Personal entertainment and miscellaneous expenses can sometimes be overlooked, yet they play an important role in your overall budget. By including expenses like grooming, medical costs, and entertainment, you can determine whether these costs are manageable within your budget. Identifying unnecessary expenditures in this category may reveal opportunities for savings, helping you allocate funds more effectively toward essential needs or savings.

If you identify areas where you can cut back on spending, it's essential to mark those on the budget worksheet. Placing a check-mark next to these amounts can highlight potential reductions and facilitate discussions with advisors or counselors. This proactive approach can be beneficial in creating a financial strategy that prioritizes necessary living expenses and ultimately helps maintain housing stability.

The “Total of Sections A-J” represents the overall amount of your monthly expenses across various categories, providing you with a consolidated view of your financial commitments. Meanwhile, the “Possible reductions in monthly expenses” reflects the sum of any identified savings opportunities from marked items. Analyzing these numbers can help you understand your financial health more clearly and create a plan that supports your goals for stability and growth.

Filling out a budget form accurately is crucial for effective financial management. However, many individuals make common mistakes that can lead to misunderstandings or inaccuracies in their financial assessments. Understanding these pitfalls can enhance one’s ability to manage finances wisely.

One frequent error is underestimating or omitting expenses. Many people forget to include minor but significant costs, such as phone bills or maintenance fees. Each monthly expenditure, no matter how small, contributes to the overall financial picture. By failing to account for these items, individuals may find themselves with a misleading budget that does not reflect their true financial situation.

An additional mistake involves neglecting to check for possible reductions in monthly expenses. The budget form provides a clear section for marking areas where expenses could be decreased. Surprisingly, many overlook this step. Identifying potential savings helps in creating a more realistic budget and can lead to significant financial relief.

Another common error occurs when individuals forget to categorize their debts properly. It can be tempting to list all obligations under a general heading without breaking them down into specific categories, such as credit card debt or student loans. This lack of detail can prevent better analysis and effective debt management strategies.

Additionally, some people input estimated amounts rather than actual figures. Providing precise numbers helps in gaining a clear understanding of financial conditions. Relying on guesses often leads to inaccuracies that can skew one’s financial planning.

Finally, overlooking the importance of regular updates to the budget form is a significant misstep. Financial situations can change from month to month due to unforeseen circumstances or changes in income. Regularly reviewing and adjusting the budget ensures that it remains an effective tool for managing one’s finances.

When managing finances, having a clear understanding of your budget is crucial. However, there are several other documents that work hand-in-hand with your budget form to provide a fuller picture of your financial situation. Each of these documents plays an important role in streamlining your financial planning process and can aid in making informed decisions.

By utilizing these forms along with your Budget form, you can gain a comprehensive understanding of your financial situation and make informed decisions. This holistic approach to budgeting and financial management can lead you to greater stability and peace of mind.

Expense Tracker: Similar to a budget form, an expense tracker details your spending habits. It allows users to categorize transactions, ensuring they stay aware of their financial situation.

Income Statement: This document summarizes income from various sources. Like a budget, it helps individuals recognize where money comes from and assists in planning future expenditures.

Financial Statement: A financial statement gives a complete overview of one's financial health, similar to how a budget outlines income and expenses for effective management.

Debt Repayment Plan: This plan focuses on paying off debts systematically. Just like a budget, it requires detailing amounts owed, interest rates, and minimum payments to achieve financial stability.

Savings Plan: A savings plan outlines financial goals and the strategies for achieving them. It shares similarities with a budget in its emphasis on planning for future financial needs.

Investment Plan: This document details an individual’s strategy for investing. Like a budget, it requires thorough evaluation of potential risks and returns, ensuring long-term financial growth.

Cash Flow Statement: A cash flow statement tracks cash inflows and outflows over a specific period, parallel to a budget's goal of monitoring spending versus income.

Spending Plan: A spending plan, much like a budget, helps prioritize where money should be allocated based on individual or family needs.

Financial Goals Worksheet: This worksheet identifies short-term and long-term financial objectives, similar to how a budget serves as a foundational tool for achieving those goals.

Monthly Bill Organizer: A monthly bill organizer lists all recurring payments, mirroring a budget’s function of tracking regular expenses to maintain control over finances.

When filling out the Budget form, there are essential guidelines to follow. Here is a list of what to do and what to avoid:

Misconceptions about the Budget form can lead to misunderstandings regarding its purpose and importance. Below are some common misconceptions explained:

When filling out the Budget form, consider these key takeaways: