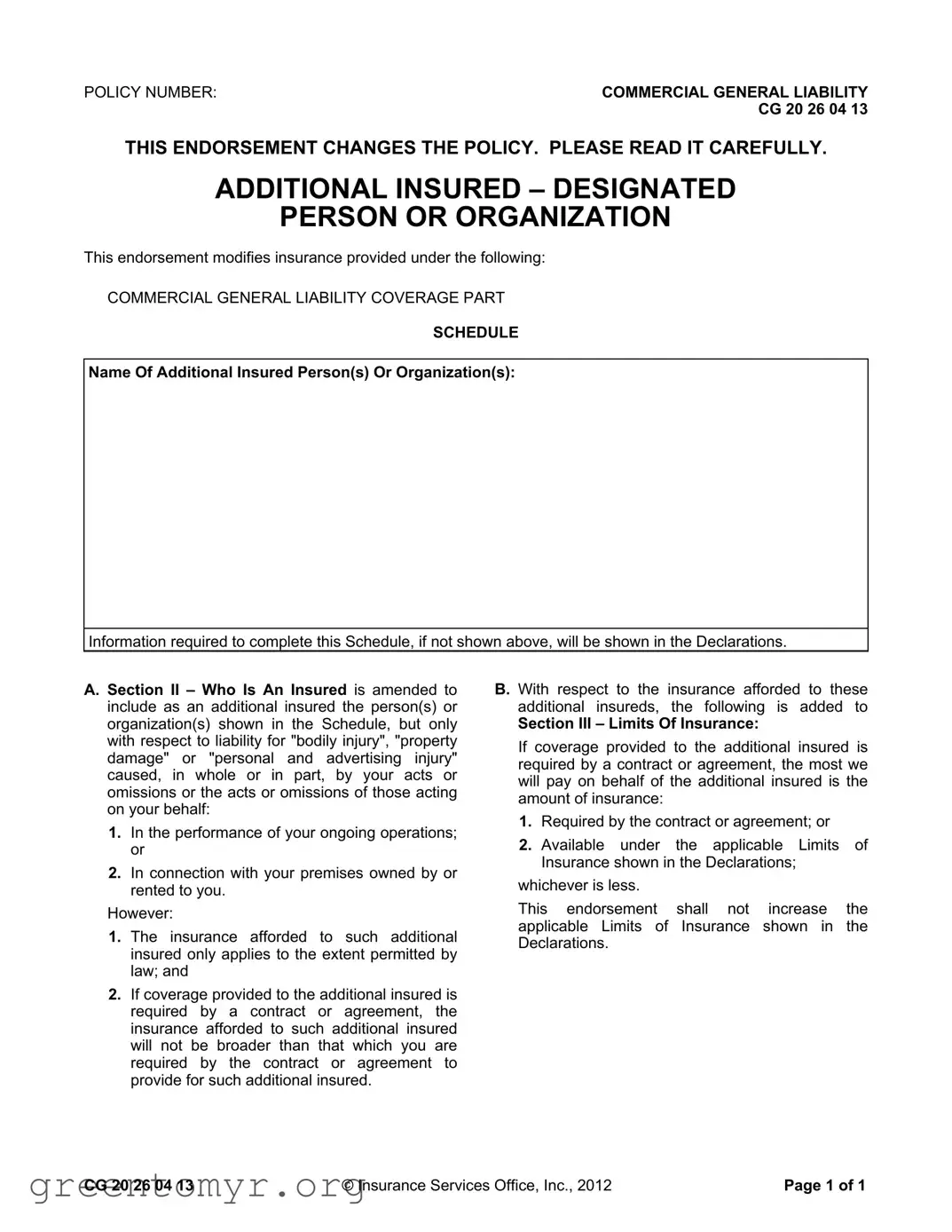

The CG 20 26 04 13 form is an important endorsement that modifies the Commercial General Liability (CGL) policy, specifically addressing the inclusion of additional insured parties. This form is designed to extend coverage to certain individuals or organizations, ensuring they are protected against liabilities arising from bodily injury, property damage, or personal and advertising injury linked to the actions of the primary insured. It’s crucial to note that this endorsement applies only under specific circumstances, particularly in relation to ongoing operations or premises owned or rented by the insured. The form outlines that while additional insureds gain coverage, it is limited to what is permitted by law and cannot exceed the terms outlined in any relevant contracts. Furthermore, the endorsement stipulates that the maximum payout for claims involving these additional insureds will either be the amount specified in the contract or the limits of insurance stated in the policy declarations, whichever is lower. Understanding the nuances of the CG 20 26 04 13 form can help businesses navigate their liability insurance needs more effectively.

POLICY NUMBER: |

COMMERCIAL GENERAL LIABILITY |

|

CG 20 26 04 13 |

THIS ENDORSEMENT CHANGES THE POLICY. PLEASE READ IT CAREFULLY.

ADDITIONAL INSURED – DESIGNATED

PERSON OR ORGANIZATION

This endorsement modifies insurance provided under the following:

COMMERCIAL GENERAL LIABILITY COVERAGE PART

SCHEDULE

Name Of Additional Insured Person(s) Or Organization(s):

Information required to complete this Schedule, if not shown above, will be shown in the Declarations.

A. Section II – Who Is An Insured is amended to include as an additional insured the person(s) or organization(s) shown in the Schedule, but only with respect to liability for "bodily injury", "property damage" or "personal and advertising injury" caused, in whole or in part, by your acts or omissions or the acts or omissions of those acting on your behalf:

1.In the performance of your ongoing operations; or

2.In connection with your premises owned by or rented to you.

However:

1.The insurance afforded to such additional insured only applies to the extent permitted by law; and

2.If coverage provided to the additional insured is required by a contract or agreement, the insurance afforded to such additional insured will not be broader than that which you are required by the contract or agreement to provide for such additional insured.

B. With respect to the insurance afforded to these additional insureds, the following is added to

Section III – Limits Of Insurance:

If coverage provided to the additional insured is required by a contract or agreement, the most we will pay on behalf of the additional insured is the amount of insurance:

1.Required by the contract or agreement; or

2.Available under the applicable Limits of Insurance shown in the Declarations;

whichever is less.

This endorsement shall not increase the applicable Limits of Insurance shown in the Declarations.

CG 20 26 04 13 |

© Insurance Services Office, Inc., 2012 |

Page 1 of 1 |

| Fact Name | Details |

|---|---|

| Form Purpose | This form adds additional insured status to a person or organization under a commercial general liability policy. |

| Governing Law | The governing laws may vary by state. For example, in California, the relevant law is the California Insurance Code. |

| Scope of Coverage | The coverage applies to bodily injury, property damage, or personal and advertising injury caused by your actions or those acting on your behalf. |

| Limitations | Coverage for the additional insured will not exceed what is required by contract or the limits in the policy declarations. |

| Conditions | Insurance for additional insureds is only effective to the extent permitted by law. |

| Contractual Requirement | If coverage is required by a contract, it cannot be broader than what the contract specifies. |

Completing the CG 20 26 04 13 form is a straightforward process. This endorsement is used to add additional insured parties to a Commercial General Liability policy. Ensure that all required information is accurate and complete before submission.

The CG 20 26 04 13 form serves as an endorsement to a Commercial General Liability policy. It adds specific individuals or organizations as additional insureds, providing them with coverage for certain liabilities. This endorsement is crucial for protecting both the policyholder and the additional insured in the event of claims related to bodily injury, property damage, or personal and advertising injury.

The form allows you to name any person or organization as an additional insured, as specified in the Schedule section. This could include contractors, subcontractors, or clients. It’s important to ensure that the additional insureds are relevant to your business operations and that their inclusion is appropriate based on your contractual obligations.

This endorsement covers liability for:

These liabilities must be caused, either wholly or partially, by your actions or those of individuals acting on your behalf during ongoing operations or in relation to premises you own or rent.

Yes, there are limitations. The coverage for additional insureds is only effective to the extent permitted by law. Additionally, if the coverage is required by a contract, it cannot exceed what is specified in that contract. This means that you should review any agreements carefully to understand the extent of coverage needed.

The CG 20 26 04 13 form does not increase the overall limits of insurance outlined in your policy. If coverage for the additional insured is mandated by a contract, the maximum amount payable will be the lesser of:

This ensures that the coverage remains within the scope of what you have already agreed to in your policy.

To add an additional insured, you should complete the Schedule section of the form with the required information. Make sure to specify the names accurately and ensure that the addition aligns with any existing contracts or agreements. Once completed, submit the form to your insurance provider for processing.

Yes, you can remove an additional insured, but this typically requires a formal request to your insurance provider. It's advisable to check your policy and any relevant contracts to ensure that removing the additional insured does not violate any agreements or obligations.

When filling out the CG 20 26 04 13 form, individuals often make several common mistakes that can lead to complications in their insurance coverage. One frequent error is failing to accurately list the additional insured parties. This section is crucial as it determines who is covered under the policy. Omitting a name or misspelling it can result in denied claims.

Another mistake is not referencing the correct policy number. Each policy has a unique identifier, and entering the wrong number can cause delays or confusion when processing claims. Always double-check that the policy number matches the one on your insurance documents.

Some individuals neglect to include specific details about the operations that the additional insureds are involved in. The form requires clarity on whether the coverage applies to ongoing operations or specific premises. Failing to provide this information can limit the effectiveness of the coverage.

Additionally, people often misunderstand the limits of insurance section. It is essential to know that the coverage for additional insureds cannot exceed what is stipulated in the contract or agreement. Misinterpreting this can lead to expectations that are not supported by the policy.

Another common oversight is not reviewing the endorsements carefully. Each endorsement modifies the original policy, and not understanding these changes can lead to gaps in coverage. Reading the entire document thoroughly is vital for comprehension.

Some individuals also forget to sign and date the form. An unsigned form is typically considered incomplete and may not be processed. Ensure that all required signatures are present before submission.

Moreover, individuals sometimes fail to consult their insurance agent when completing the form. Agents can provide valuable insights and help clarify any uncertainties regarding coverage. Ignoring this resource can result in errors that might have been easily avoided.

Finally, many people do not keep a copy of the completed form for their records. Having a copy can be beneficial for future reference, especially if any issues arise later. Always retain a copy to ensure that you have documentation of what was submitted.

When dealing with the CG 20 26 04 13 form, it's essential to understand that it often works in conjunction with several other documents. These forms help clarify the terms of insurance coverage and the responsibilities of all parties involved. Here’s a brief overview of six other forms and documents you might encounter:

Each of these documents plays a vital role in the broader context of insurance and liability management. Familiarizing yourself with them can enhance your understanding of your coverage and obligations, ensuring you are well-prepared for any situation that may arise.

The CG 20 26 04 13 form is an endorsement that modifies a Commercial General Liability (CGL) policy to include additional insureds. This type of document is not unique and shares similarities with several other insurance forms and endorsements. Here are ten documents that are similar to the CG 20 26 04 13 form, along with a brief explanation of how they relate:

Understanding these documents can help policyholders better navigate their insurance needs and ensure adequate protection for additional insured parties.

When filling out the CG 20 26 04 13 form, it is important to follow certain guidelines to ensure accuracy and compliance. Below is a list of things you should and shouldn't do:

Understanding the CG 20 26 04 13 form is essential for anyone involved in commercial general liability insurance. Unfortunately, several misconceptions can lead to confusion. Here’s a breakdown of ten common misunderstandings about this endorsement:

Clarifying these misconceptions can help ensure that businesses and individuals understand the true nature of the coverage provided by the CG 20 26 04 13 form. Awareness of these details is crucial for effective risk management and legal compliance.

When filling out and using the CG 20 26 04 13 form, consider the following key takeaways: