In Colorado, the Promissory Note form serves as a vital tool for individuals and businesses alike when it comes to borrowing and lending money. This straightforward document outlines the terms of a loan, specifying the amount borrowed, the interest rate, and the repayment schedule. It also includes crucial details such as the identities of the borrower and lender, ensuring that both parties are clear about their roles and responsibilities. Additionally, the form may address what happens in the event of default, providing a safety net for the lender. By using this form, both parties can establish a mutual understanding, reducing the potential for disputes down the road. Understanding the components of the Colorado Promissory Note is essential for anyone looking to engage in a loan agreement, as it lays the groundwork for a smooth transaction and fosters trust between the involved parties.

Colorado Promissory Note Template

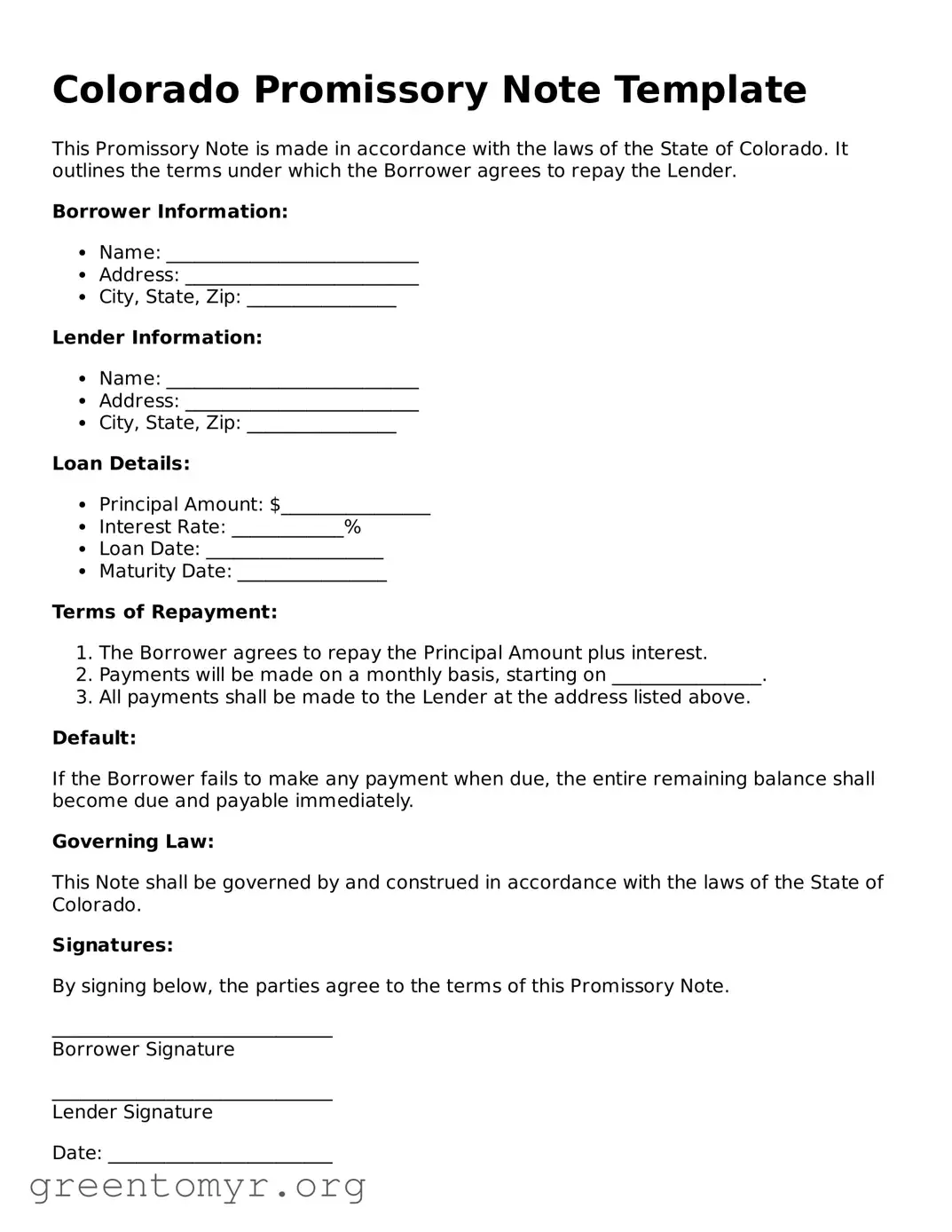

This Promissory Note is made in accordance with the laws of the State of Colorado. It outlines the terms under which the Borrower agrees to repay the Lender.

Borrower Information:

Lender Information:

Loan Details:

Terms of Repayment:

Default:

If the Borrower fails to make any payment when due, the entire remaining balance shall become due and payable immediately.

Governing Law:

This Note shall be governed by and construed in accordance with the laws of the State of Colorado.

Signatures:

By signing below, the parties agree to the terms of this Promissory Note.

______________________________

Borrower Signature

______________________________

Lender Signature

Date: ________________________

| Fact Name | Description |

|---|---|

| Definition | A promissory note is a written promise to pay a specified amount of money to a designated party at a certain time. |

| Governing Law | The Colorado Uniform Commercial Code governs promissory notes in Colorado. |

| Parties Involved | Typically, the borrower (maker) and the lender (payee) are the two parties involved in a promissory note. |

| Interest Rate | The note can specify an interest rate, which may be fixed or variable, depending on the agreement. |

| Payment Terms | Payment terms must be clearly outlined, including the due date and any installment amounts. |

| Default Provisions | The note should include provisions for what happens in case of default, such as late fees or acceleration of the debt. |

| Signatures | Both parties must sign the promissory note for it to be legally binding. |

| Notarization | While notarization is not required, it can provide additional legal protection for the parties involved. |

Once you have the Colorado Promissory Note form in front of you, it is time to complete it accurately. This form will require specific information from both the borrower and the lender. After filling it out, both parties will need to sign the document to ensure its validity.

After completing these steps, ensure that both parties retain a copy of the signed document for their records. This will serve as a reference for the terms agreed upon in the loan agreement.

A Colorado Promissory Note is a written agreement in which one party promises to pay a specific amount of money to another party at a defined time or on demand. This document outlines the terms of the loan, including the interest rate, payment schedule, and consequences of default. It serves as a legal record of the debt and can be enforced in court if necessary.

Any individual or business can use a Promissory Note in Colorado. This includes private lenders, friends, family members, or businesses providing loans. It is essential for both parties to understand the terms and implications of the note, regardless of the relationship.

A typical Colorado Promissory Note includes several important components:

Including these elements helps ensure clarity and reduces the potential for disputes.

Yes, a Promissory Note is legally binding in Colorado, provided it meets the necessary legal requirements. Both parties must agree to the terms, and the document must be signed by the borrower. In some cases, having the note notarized can add an extra layer of legitimacy, although it is not always required.

If the borrower defaults, meaning they fail to make payments as agreed, the lender has several options. They can attempt to negotiate a new payment plan, charge late fees, or take legal action to recover the owed amount. The specific consequences should be outlined in the Promissory Note itself, making it crucial for both parties to understand these terms before signing.

Yes, a Promissory Note can be modified after it is signed, but both parties must agree to the changes. It is advisable to document any modifications in writing and have both parties sign the amended note. This helps prevent misunderstandings and ensures that all parties are aware of the new terms.

Templates for Colorado Promissory Notes can be found online through legal websites, law libraries, or local legal aid organizations. It is essential to ensure that any template used complies with Colorado laws and suits the specific needs of the parties involved. Consulting with a legal professional can also provide guidance and ensure that the document is appropriately tailored.

When filling out the Colorado Promissory Note form, individuals often make several common mistakes that can lead to complications down the line. One frequent error is failing to clearly state the loan amount. Without a precise figure, the terms of the agreement can become ambiguous, leading to potential disputes between the lender and borrower.

Another common mistake involves neglecting to include the interest rate. The Promissory Note should specify whether the loan is interest-free or what the applicable interest rate is. Omitting this detail can create confusion regarding repayment expectations and may result in legal issues later.

Additionally, individuals sometimes forget to include the due date for repayment. This date is crucial, as it establishes a timeline for when the borrower must repay the loan. Without a clear due date, both parties may have differing interpretations of the agreement, which can complicate enforcement.

Providing inaccurate personal information is another mistake that can lead to complications. It is essential that both the lender's and borrower's names, addresses, and contact information are correct. Errors in this section can hinder communication and create difficulties in legal proceedings if they arise.

Lastly, individuals may overlook the need for signatures. Both the lender and borrower must sign the Promissory Note to validate the agreement. Failure to do so renders the document ineffective, leaving both parties without legal recourse should a dispute occur.

When entering into a loan agreement in Colorado, the Promissory Note is a critical document. However, it is often accompanied by other forms and documents that help clarify the terms of the loan and protect the interests of both parties involved. Understanding these additional documents can be crucial for ensuring a smooth transaction.

By familiarizing yourself with these additional documents, you can navigate the lending process more effectively. Each plays a vital role in ensuring that both parties are protected and informed, ultimately leading to a more successful agreement.

A Promissory Note is a financial document that outlines a promise to pay a specific amount of money to a designated person or entity. Several other documents share similarities with a Promissory Note. Here are seven of those documents:

When filling out the Colorado Promissory Note form, it’s important to pay attention to detail. Here are some guidelines to help you navigate the process effectively:

Following these tips can help ensure that your Promissory Note is clear, complete, and legally sound.

Understanding the Colorado Promissory Note form is crucial for anyone involved in lending or borrowing money. However, several misconceptions can lead to confusion. Here are ten common misconceptions about this form:

Clearing up these misconceptions can help individuals navigate their lending and borrowing experiences more effectively. Always consider consulting with a professional for personalized advice.

When filling out and using the Colorado Promissory Note form, consider the following key takeaways: