When it comes to managing personal finances, a credit report plays a crucial role in determining one’s creditworthiness. However, inaccuracies in these reports can lead to significant challenges, including higher interest rates and denied loan applications. To address these discrepancies, individuals have the option to utilize a Credit Report Dispute form. This form serves as a formal mechanism to challenge errors or outdated information contained in a credit report. Key aspects of the form include the requirement to provide personal identification details, a clear description of the disputed information, and any supporting documentation that can substantiate the claim. Additionally, the form typically allows individuals to specify the desired outcome, whether it be correction of the error or removal of the incorrect entry. By understanding how to effectively complete this form, consumers can take proactive steps to ensure their credit reports accurately reflect their financial history.

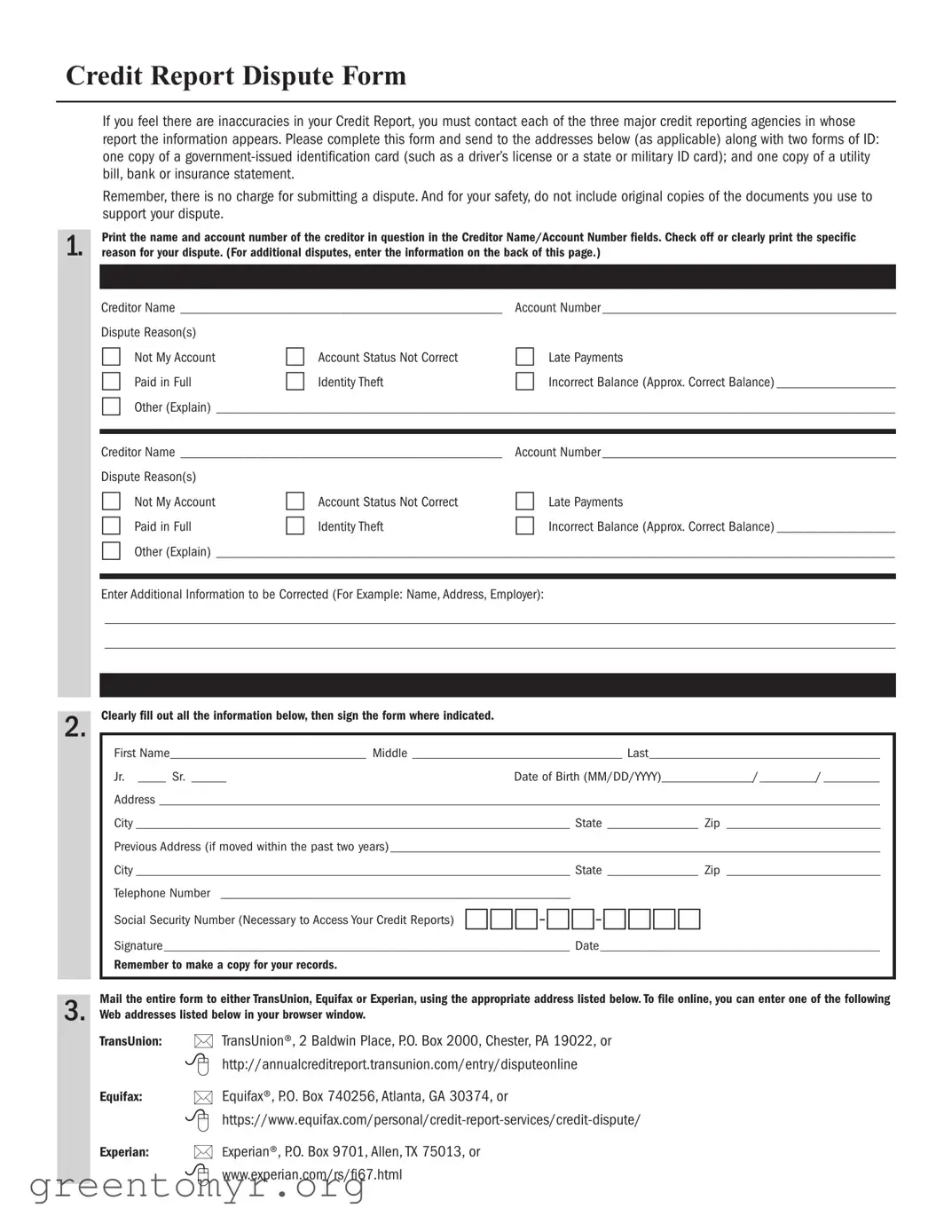

Credit Report Dispute Form

If you feel there are inaccuracies in your Credit Report, you must contact each of the three major credit reporting agencies in whose report the information appears. Please complete this form and send to the addresses below (as applicable) along with two forms of ID: one copy of a

Remember, there is no charge for submitting a dispute. And for your safety, do not include original copies of the documents you use to support your dispute.

Print the name and account number of the creditor in question in the Creditor Name/Account Number fields. Check off or clearly print the specific

1. reason for your dispute. (For additional disputes, enter the information on the back of this page.)

2.

Creditor Name ______________________________________________ |

Account Number __________________________________________ |

|

Dispute Reason(s) |

|

|

□ Not My Account |

□ Account Status Not Correct |

□ Late Payments |

□ Paid in Full |

□ Identity Theft |

□ Incorrect Balance (Approx. Correct Balance) _________________ |

□Other (Explain) _________________________________________________________________________________________________

Creditor Name ______________________________________________ |

Account Number __________________________________________ |

|

Dispute Reason(s) |

|

|

□ Not My Account |

□ Account Status Not Correct |

□ Late Payments |

□ Paid in Full |

□ Identity Theft |

□ Incorrect Balance (Approx. Correct Balance) _________________ |

□Other (Explain) _________________________________________________________________________________________________

Enter Additional Information to be Corrected (For Example: Name, Address, Employer):

_________________________________________________________________________________________________________________

_________________________________________________________________________________________________________________

Clearly fill out all the information below, then sign the form where indicated.

First Name____________________________ Middle ______________________________ Last_________________________________

Jr. ____ Sr. _____Date of Birth (MM/DD/YYYY)_____________/________/ ________

Address _______________________________________________________________________________________________________

City ______________________________________________________________ State _____________ Zip ______________________

Previous Address (if moved within the past two years) ______________________________________________________________________

City ______________________________________________________________ State _____________ Zip ______________________

Telephone Number __________________________________________________

Social Security Number (Necessary to Access Your Credit Reports)

Signature __________________________________________________________ Date________________________________________

Remember to make a copy for your records.

Mail the entire form to either TransUnion, Equifax or Experian, using the appropriate address listed below. To file online, you can enter one of the following

3. Web addresses listed below in your browser window.

TransUnion:

Equifax:

Experian:

•TransUnion®, 2 Baldwin Place, P.O. Box 2000, Chester, PA 19022, or

•http://annualcreditreport.transunion.com/entry/disputeonline

•Equifax®, P.O. Box 740256, Atlanta, GA 30374, or

•

•Experian®, P.O. Box 9701, Allen, TX 75013, or

•www.experian.com/rs/fi67.html

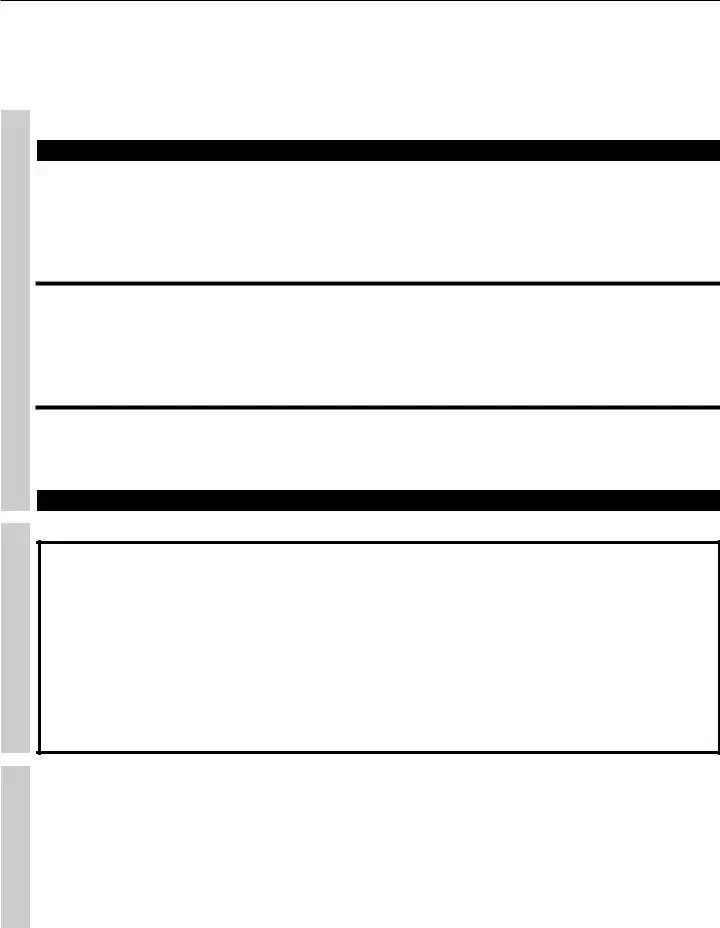

Creditor Name ________________________________________________ |

Account Number_______________________________________________ |

|

Dispute Reason(s) |

|

|

□ Not My Account |

□ Account Status Not Correct |

□ Late Payments |

□ Paid in Full |

□ Identity Theft |

□ Incorrect Balance (Approx. Correct Balance) ______________________ |

□Other (Explain) ________________________________________________________________________________________________________

Creditor Name ________________________________________________ |

Account Number_______________________________________________ |

|

Dispute Reason(s) |

|

|

□ Not My Account |

□ Account Status Not Correct |

□ Late Payments |

□ Paid in Full |

□ Identity Theft |

□ Incorrect Balance (Approx. Correct Balance) ______________________ |

□Other (Explain) ________________________________________________________________________________________________________

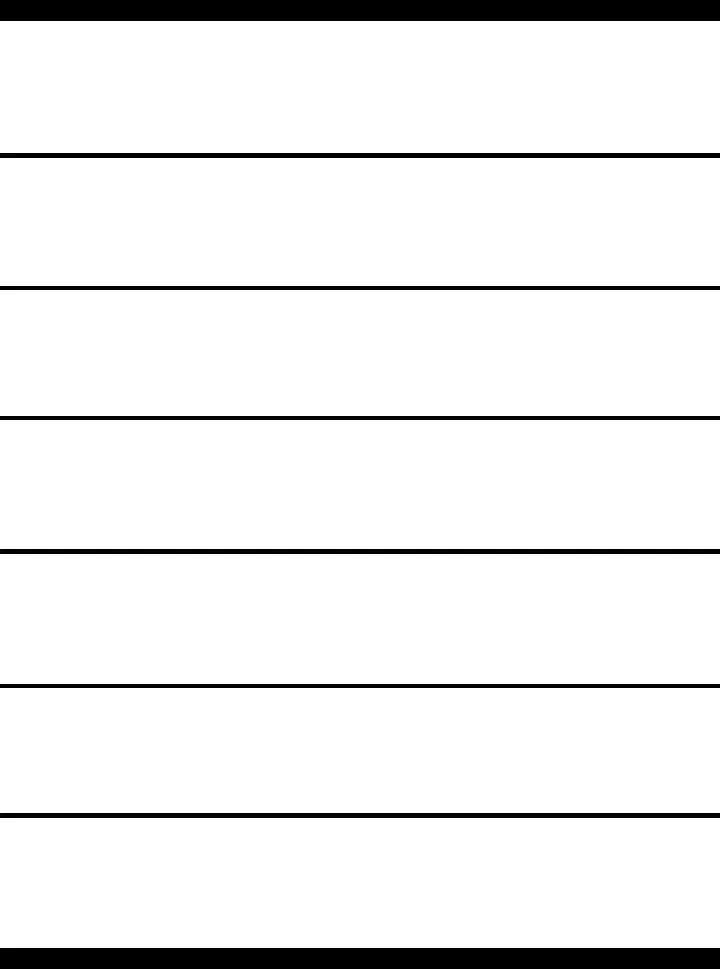

Creditor Name ________________________________________________ |

Account Number_______________________________________________ |

|

Dispute Reason(s) |

|

|

□ Not My Account |

□ Account Status Not Correct |

□ Late Payments |

□ Paid in Full |

□ Identity Theft |

□ Incorrect Balance (Approx. Correct Balance) ______________________ |

□Other (Explain) ________________________________________________________________________________________________________

Creditor Name ________________________________________________ |

Account Number_______________________________________________ |

|

Dispute Reason(s) |

|

|

□ Not My Account |

□ Account Status Not Correct |

□ Late Payments |

□ Paid in Full |

□ Identity Theft |

□ Incorrect Balance (Approx. Correct Balance) ______________________ |

□Other (Explain) ________________________________________________________________________________________________________

Creditor Name ________________________________________________ |

Account Number_______________________________________________ |

|

Dispute Reason(s) |

|

|

□ Not My Account |

□ Account Status Not Correct |

□ Late Payments |

□ Paid in Full |

□ Identity Theft |

□ Incorrect Balance (Approx. Correct Balance) ______________________ |

□Other (Explain) ________________________________________________________________________________________________________

Creditor Name ________________________________________________ |

Account Number_______________________________________________ |

|

Dispute Reason(s) |

|

|

□ Not My Account |

□ Account Status Not Correct |

□ Late Payments |

□ Paid in Full |

□ Identity Theft |

□ Incorrect Balance (Approx. Correct Balance) ______________________ |

□Other (Explain) ________________________________________________________________________________________________________

Creditor Name ________________________________________________ |

Account Number_______________________________________________ |

|

Dispute Reason(s) |

|

|

□ Not My Account |

□ Account Status Not Correct |

□ Late Payments |

□ Paid in Full |

□ Identity Theft |

□ Incorrect Balance (Approx. Correct Balance) ______________________ |

□Other (Explain) ________________________________________________________________________________________________________

| Fact Name | Description |

|---|---|

| Purpose | The Credit Report Dispute form is used by individuals to formally challenge inaccuracies or errors found in their credit reports. |

| Eligibility | Anyone who has a credit report can file a dispute if they believe there is incorrect information affecting their credit score. |

| Governing Laws | In the United States, the Fair Credit Reporting Act (FCRA) governs the process of disputing credit report inaccuracies. |

| Submission Process | Disputes can typically be submitted online, by mail, or over the phone, depending on the credit reporting agency's policies. |

After you complete the Credit Report Dispute form, it will be submitted for review. The next steps involve the credit reporting agency investigating your claim and responding to you within a specified timeframe.

A Credit Report Dispute form is a document that individuals can use to challenge inaccuracies or errors found in their credit report. These inaccuracies can include wrong account information, incorrect balances, or accounts that do not belong to you. By filing this form, you initiate a process to correct these errors, which can positively impact your credit score and overall financial health.

Anyone who has a credit report can file a dispute. This includes individuals who have recently checked their credit reports and found discrepancies. Whether you are applying for a loan, a credit card, or simply reviewing your financial standing, if you notice something amiss, you have the right to dispute it.

Filling out the Credit Report Dispute form is straightforward. Here are the steps you should follow:

Make sure to keep a copy of the completed form for your records.

Once you submit your dispute, the credit reporting agency will investigate the claim. They typically have 30 days to respond. During this time, they will contact the creditor involved to verify the information. If they find that the information is indeed inaccurate, they will correct it on your report. You will receive a copy of the results once the investigation is complete.

Yes, you can dispute multiple items on your credit report in a single submission. When filling out the Credit Report Dispute form, clearly list each item you are disputing. Be as detailed as possible for each entry. This will help ensure that the credit reporting agency understands your concerns and can address them efficiently.

No, there is no fee to file a Credit Report Dispute. This process is free of charge, as consumers have the right to challenge inaccuracies in their credit reports without incurring any costs. It’s important to take advantage of this right to protect your financial standing.

Filling out the Credit Report Dispute form can be straightforward, but many people make common mistakes that can delay the process. One frequent error is failing to provide accurate personal information. It is essential to ensure that your name, address, and Social Security number are correct. Inaccuracies can lead to confusion and may result in the dispute being dismissed.

Another mistake is not clearly stating the reason for the dispute. Simply marking a box without providing details does not give the credit bureau enough information to investigate. A well-explained reason helps facilitate a quicker resolution. Providing specific details about what is incorrect and why is crucial.

Some individuals overlook the importance of including supporting documentation. If you claim an error, it is helpful to attach any relevant documents that support your position. This could include payment receipts, account statements, or correspondence with creditors. Without this evidence, the dispute may not be taken seriously.

Additionally, people often forget to keep a copy of the completed form for their records. This step is vital for tracking the dispute's progress. Having a copy allows you to reference your initial submission if needed later on.

Another common issue is submitting the form to the wrong credit bureau. Each bureau operates independently, and disputes must be sent to the bureau that reported the error. Double-checking which bureau has the incorrect information can save time and effort.

Some individuals fail to respond promptly to any follow-up requests from the credit bureau. If additional information is needed, responding quickly can help resolve the dispute faster. Ignoring these requests can lead to delays or even a dismissal of the dispute.

People may also underestimate the importance of following up on the dispute. After submitting the form, it is advisable to check back with the credit bureau to ensure that the investigation is underway. Regular follow-ups can help keep the process on track.

Finally, some individuals do not understand the time frame for dispute resolution. The credit bureau typically has 30 days to investigate. Being aware of this timeline can help manage expectations and allow for appropriate follow-up actions if necessary.

When disputing inaccuracies on a credit report, several forms and documents can assist in the process. Each of these documents serves a specific purpose, helping to clarify the dispute and support your claims. Below is a list of common documents often used alongside the Credit Report Dispute form.

Gathering these documents can significantly enhance your dispute's effectiveness. Each piece plays a vital role in ensuring that your credit report accurately reflects your financial history. By being thorough and organized, you can navigate the dispute process more smoothly.

The Credit Report Dispute form serves a specific purpose in helping individuals address inaccuracies in their credit reports. However, there are several other documents that share similarities in function or intent. Here are eight documents that are akin to the Credit Report Dispute form:

Each of these documents plays a crucial role in managing your credit and financial health. Understanding their similarities can empower you to take informed actions regarding your credit report and overall financial situation.

When filling out a Credit Report Dispute form, it's important to approach the process carefully. Here are some essential dos and don'ts to keep in mind:

By following these guidelines, you can improve your chances of successfully resolving discrepancies in your credit report.

Understanding the Credit Report Dispute form can be challenging, especially with the many misconceptions that exist. Here are six common misunderstandings that people often have:

By clarifying these misconceptions, individuals can approach the Credit Report Dispute process with a more informed perspective, ultimately leading to better outcomes.

Filling out and using the Credit Report Dispute form can significantly impact your credit score and financial health. Here are some key takeaways to keep in mind:

By keeping these points in mind, you can navigate the dispute process more effectively and work towards correcting any inaccuracies on your credit report.