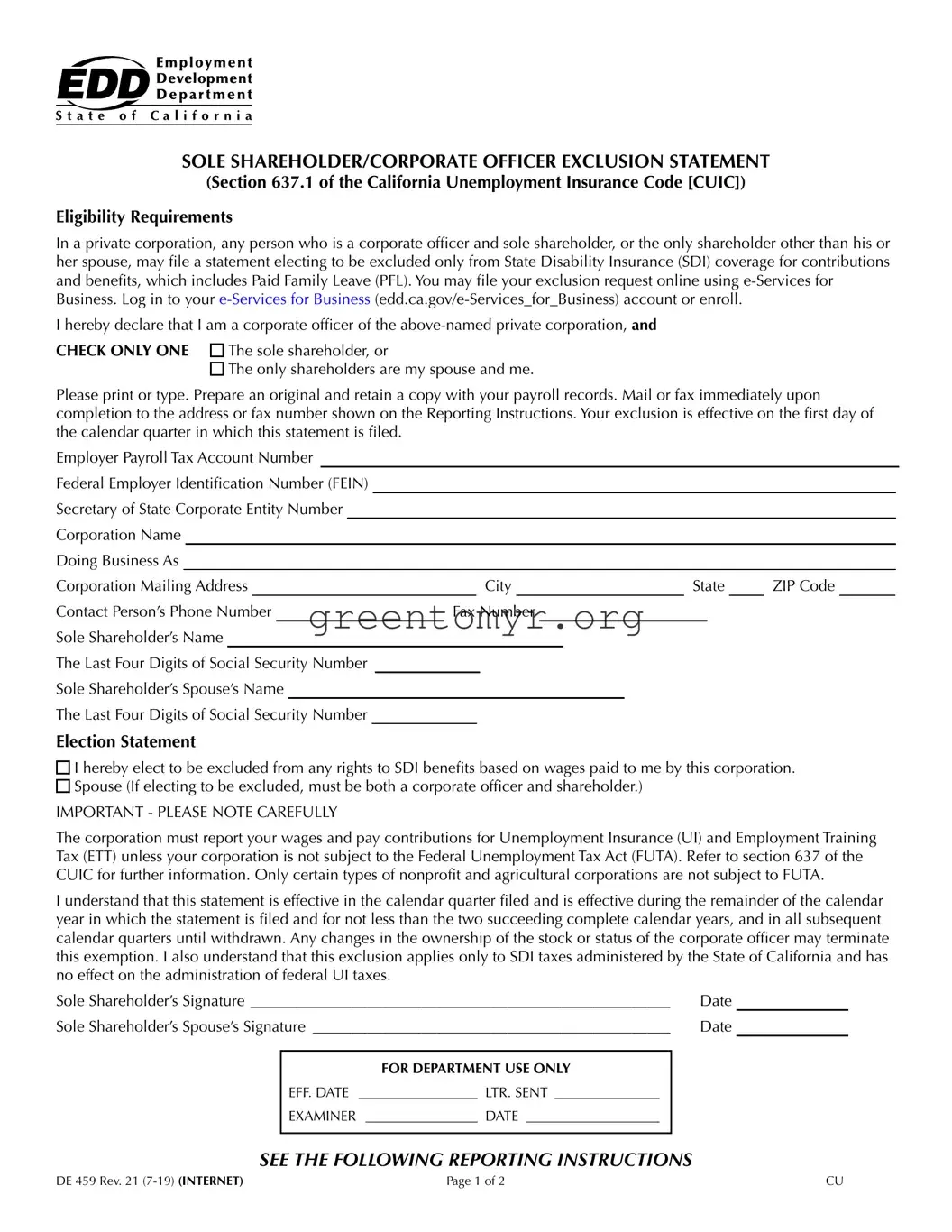

The DE 459 form serves as a critical tool for sole shareholders and corporate officers of private corporations in California who wish to opt out of State Disability Insurance (SDI) coverage. This form is specifically designed for individuals who are the sole shareholders of a corporation or those whose only other shareholder is their spouse. By filing the DE 459, these individuals can formally elect to exclude themselves from SDI contributions and benefits, which also encompasses Paid Family Leave (PFL). To streamline this process, the California Employment Development Department (EDD) provides an online platform, e-Services for Business, allowing for efficient submission and management of the form. Once filed, the exclusion becomes effective at the beginning of the calendar quarter in which the form is submitted, and it remains valid for the current calendar year plus two additional years, unless revoked due to changes in corporate ownership or officer status. This exclusion offers a layer of financial flexibility, but it is essential to understand that while the form allows for SDI exemption, it does not impact federal unemployment taxes. Thus, compliance with all state and federal reporting requirements remains necessary. Whether you are a seasoned corporate officer or newly navigating sole proprietorship, the DE 459 form can play a vital role in managing your corporate tax obligations effectively.

SOLE SHAREHOLDER/CORPORATE OFFICER EXCLUSION STATEMENT

(Section 637.1 of the California Unemployment Insurance Code [CUIC])

Eligibility Requirements

In a private corporation, any person who is a corporate officer and sole shareholder, or the only shareholder other than his or her spouse, may file a statement electing to be excluded only from State Disability Insurance (SDI) coverage for contributions and benefits, which includes Paid Family Leave (PFL). You may file your exclusion request online using

I hereby declare that I am a corporate officer of the

CHECK ONLY ONE |

The sole shareholder, or |

|

The only shareholders are my spouse and me. |

Please print or type. Prepare an original and retain a copy with your payroll records. Mail or fax immediately upon completion to the address or fax number shown on the Reporting Instructions. Your exclusion is effective on the first day of the calendar quarter in which this statement is filed.

Employer Payroll Tax Account Number Federal Employer Identification Number (FEIN) Secretary of State Corporate Entity Number Corporation Name

Doing Business As

Corporation Mailing Address |

|

|

|

City |

|

State |

|

ZIP Code |

|||||||||

Contact Person’s Phone Number |

|

Fax Number |

|

|

|

|

|

||||||||||

Sole Shareholder’s Name |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

The Last Four Digits of Social Security Number |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Sole Shareholder’s Spouse’s Name |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

The Last Four Digits of Social Security Number |

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Election Statement

I hereby elect to be excluded from any rights to SDI benefits based on wages paid to me by this corporation. Spouse (If electing to be excluded, must be both a corporate officer and shareholder.)

IMPORTANT - PLEASE NOTE CAREFULLY

The corporation must report your wages and pay contributions for Unemployment Insurance (UI) and Employment Training Tax (ETT) unless your corporation is not subject to the Federal Unemployment Tax Act (FUTA). Refer to section 637 of the CUIC for further information. Only certain types of nonprofit and agricultural corporations are not subject to FUTA.

I understand that this statement is effective in the calendar quarter filed and is effective during the remainder of the calendar year in which the statement is filed and for not less than the two succeeding complete calendar years, and in all subsequent calendar quarters until withdrawn. Any changes in the ownership of the stock or status of the corporate officer may terminate this exemption. I also understand that this exclusion applies only to SDI taxes administered by the State of California and has no effect on the administration of federal UI taxes.

Sole Shareholder’s Signature ______________________________________________________ |

Date |

|||

Sole Shareholder’s Spouse’s Signature ______________________________________________ |

Date |

|||

|

|

|

|

|

|

|

FOR DEPARTMENT USE ONLY |

|

|

|

EFF. DATE |

_________________ |

LTR. SENT _______________ |

|

|

EXAMINER |

________________ |

DATE ___________________ |

|

|

|

|

|

|

SEE THE FOLLOWING REPORTING INSTRUCTIONS

DE 459 Rev. 21 |

Page 1 of 2 |

CU |

REPORTING INSTRUCTIONS

You are required to electronically submit employment tax returns, wage reports, and payroll tax deposits using

Please follow these reporting procedures:

1.File a single Quarterly Contribution Return and Report of Wages (DE 9) for the quarter and include wages and withholdings for all of the corporation’s employees, including the sole shareholder and sole shareholder’s spouse, if electing the exclusion.

2.If you have an approved

3.When filing electronically, one DE 9C for the quarter may be used to report wages and withholdings for all the corporation’s employees, including the sole shareholder and the sole shareholder’s spouse, if electing exclusion. Insert Plan Code “R” on the wage line(s) to designate the sole shareholder wages and sole shareholder’s spouse, if electing exclusion, only when reporting on an account that is subject to UI and SDI.

GENERAL INFORMATION

NOTE: A DE 459 is not required if services performed are not subject to California law for UI, ETT, or SDI purposes. Please

refer to Information Sheet: Multistate Employment (DE 231D) (PDF) (edd.ca.gov/pdf_pub_ctr/de231d.pdf) to determine whether the services are subject to employment taxes in California.

If the corporation does not have an employer payroll tax account number, please register online through

It is important to file the form during the calendar quarter in which you want the exemption to take effect. The exemption becomes effective the first day of the calendar quarter in which it is filed. A delay in filing this form may cause your exemption to take effect in the next calendar quarter. Do not file this form as an attachment to your DE 9, DE 9C, or any other Employment Development Department (EDD) form.

The EDD reserves the right to request additional information pertaining to this form.

The exemption may be terminated at any time by a change in stock ownership or status of the corporate officer as described in section 637.1 of the CUIC.

The exemption may be voluntarily terminated after two succeeding complete calendar years have passed. The corporate officer/sole shareholder must submit a written request to the EDD for termination.

If you have any questions concerning the exemption or reporting requirements, please contact the EDD at the address below.

Attention: Specialized Coverage Desk

Employment Development Department

Taxpayer Assistance Center

PO Box 2068

Rancho Cordova, CA

Phone:

Fax:

The EDD is an equal opportunity employer/program. Auxiliary aids and services are available upon request to individuals with disabilities. Requests for services, aids, and/or alternate formats need to be made by calling

DE 459 Rev. 21 |

Page 2 of 2 |

| Fact Name | Details |

|---|---|

| Governing Law | Section 637.1 of the California Unemployment Insurance Code (CUIC) |

| Eligibility | A sole shareholder who is also a corporate officer can elect exclusion from State Disability Insurance (SDI) coverage. |

| Filing Method | Exclusion requests can be filed online through e-Services for Business. |

| Effective Date | The exclusion is effective on the first day of the calendar quarter in which the statement is filed. |

After filling out the DE 459 form, it is crucial to ensure that it is submitted promptly to avoid delays in your exclusion status. This form must be maintained with your payroll records and sent via mail or fax to the appropriate address listed in the Reporting Instructions. Timeliness will guarantee that your exclusion takes effect on the first day of the calendar quarter in which you filed.

The DE 459 form serves as a Sole Shareholder/Corporate Officer Exclusion Statement. This allows a person who is both a corporate officer and a sole shareholder, or the only shareholder aside from their spouse, to elect exclusion from State Disability Insurance (SDI) coverage. This includes benefits for Paid Family Leave (PFL) in California.

Eligibility is limited to individuals who hold the roles of corporate officer and sole shareholder in a private corporation. This can also apply to situations where the only other shareholders are the officer's spouse. Those meeting these criteria may file the form to elect exclusion from SDI.

You can submit the DE 459 form online via e-Services for Business. To do this, log in to your account or enroll if you do not already have one. It's essential to retain a copy of the completed form with your payroll records after submission.

The exclusion takes effect on the first day of the calendar quarter in which the DE 459 form is filed. If the form is submitted late, the exclusion may not become effective until the next calendar quarter.

The exemption remains effective for the remainder of the calendar year in which the form is filed, along with the two succeeding complete calendar years. It continues in subsequent quarters until a withdrawal request is made.

Yes, the exemption can be voluntarily terminated after two complete calendar years. Additionally, any change in stock ownership or the status of the corporate officer can lead to automatic termination of this exemption.

Your corporation must continue to report wages and pay contributions for Unemployment Insurance (UI) and Employment Training Tax (ETT). This applies unless the corporation is not subject to the Federal Unemployment Tax Act (FUTA).

No, a DE 459 form is not required if the services performed by the corporate officer are not subject to California laws for UI, ETT, or SDI. You may refer to the Information Sheet: Multistate Employment (DE 231D) for clarification.

If your corporation lacks a payroll tax account number, you must register for one through e-Services for Business before submitting the DE 459 form. Ensure you complete the registration before proceeding.

If you have questions, you can reach the Employment Development Department (EDD) at the Taxpayer Assistance Center. Their address is PO Box 2068, Rancho Cordova, CA 95741-2068. Phone support is available at 1-888-745-3886.

Filling out the DE459 form can be a straightforward process, but many individuals make common mistakes that can lead to delays or complications. Here are five mistakes to watch out for when completing this form.

One frequent error occurs when individuals fail to check the appropriate box regarding their shareholder status. The form allows for two choices: being the sole shareholder or being a shareholder only alongside a spouse. Not accurately indicating this status can result in significant issues with your application. Ensure that you double-check this section before submitting.

Another mistake is neglecting to include the correct Employer Payroll Tax Account Number and Federal Employer Identification Number (FEIN). These numbers are essential for processing your exemption request. Omitting or misrepresenting this information could cause the form to be rejected, which in turn delays your exemption from State Disability Insurance benefits.

Many people also overlook providing complete contact details. Including a contact person's phone number and fax number is crucial. This information allows the Employment Development Department (EDD) to reach you for any necessary clarifications or to communicate about your application status. Missing this information can lead to unnecessary complications.

Moreover, some individuals fail to retain a copy of the completed form for their records. Keeping a copy not only helps you track what you submitted but also serves as proof should any issues arise later. It is essential to maintain organized payroll records, especially when dealing with tax exemptions.

Lastly, waiting too long to submit the form can result in missed deadlines. The exemption from SDI benefits is effective only from the first day of the quarter in which the form is filed. Therefore, if you delay, you might not receive the intended benefits for the upcoming quarter. Be proactive in completing and submitting your DE459 form promptly.

The De459 form, or the Sole Shareholder/Corporate Officer Exclusion Statement, is typically accompanied by several other documents that assist in the management of payroll taxes and related matters. Below is a list of five commonly utilized forms that may support or relate to the De459.

Understanding these forms and documents can greatly help ensure compliance with California payroll tax regulations. Filing the appropriate forms accurately and on time can also aid in managing potential risks associated with tax liabilities.

The DE 459 form is a crucial document for corporate officers and sole shareholders in California regarding their exclusion from State Disability Insurance (SDI) coverage. Similar to this form, there are several other documents that also serve important purposes in different contexts. Below are five documents that share similarities with the DE 459 form:

These documents, while distinct in their purposes, each play significant roles in ensuring that individuals and corporations adhere to state and federal tax regulations.

When filling out the DE459 form, consider these important dos and don'ts:

Misconceptions about the DE 459 form often create confusion for corporate officers and sole shareholders. Here are seven common misunderstandings:

By understanding these misconceptions, corporate officers and sole shareholders can better navigate their responsibilities and rights.

Key Takeaways from the DE 459 Form: