When homeowners face the prospect of foreclosure, they often seek alternatives to mitigate the negative impacts on their financial future and emotional well-being. One such alternative is the Deed in Lieu of Foreclosure, a legal process through which a homeowner voluntarily transfers their property to the lender in exchange for the cancellation of the mortgage debt. This form is crucial in avoiding the lengthy and challenging foreclosure process, providing a more amicable resolution for both parties. By submitting a completed Deed in Lieu of Foreclosure form, homeowners can potentially safeguard their credit score from the harsh consequences of foreclosure. Lenders, on the other hand, gain the opportunity to reclaim the property without having to go through the judicial system, which can be time-consuming and costly. The form itself encapsulates essential details, such as the property address, the names of the parties involved, and the date of execution. Homeowners must also ensure there are no outstanding liens, as this can complicate the process. Understanding the implications and requirements of this form is key to making informed decisions during financial distress.

Deed in Lieu of Foreclosure Template - [State Name]

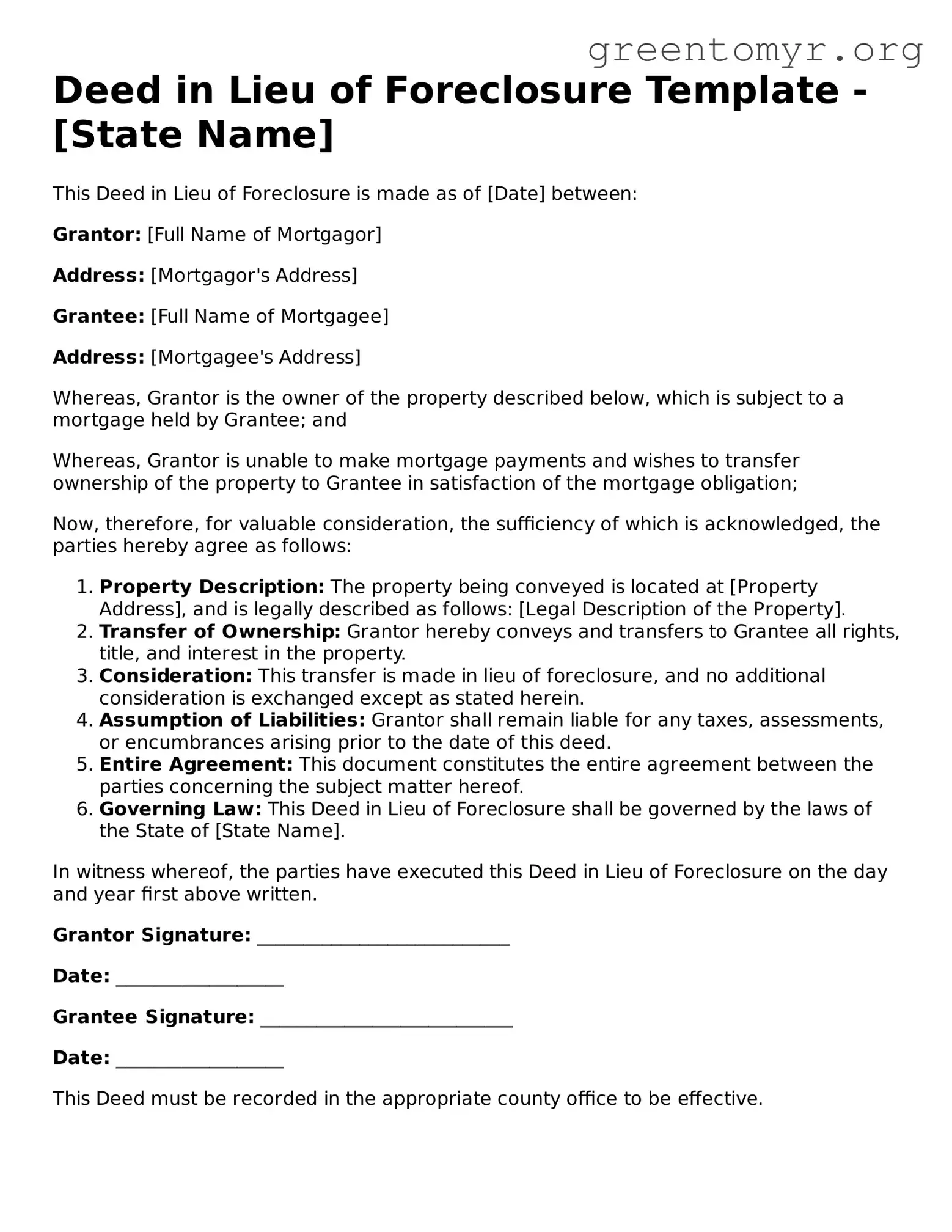

This Deed in Lieu of Foreclosure is made as of [Date] between:

Grantor: [Full Name of Mortgagor]

Address: [Mortgagor's Address]

Grantee: [Full Name of Mortgagee]

Address: [Mortgagee's Address]

Whereas, Grantor is the owner of the property described below, which is subject to a mortgage held by Grantee; and

Whereas, Grantor is unable to make mortgage payments and wishes to transfer ownership of the property to Grantee in satisfaction of the mortgage obligation;

Now, therefore, for valuable consideration, the sufficiency of which is acknowledged, the parties hereby agree as follows:

In witness whereof, the parties have executed this Deed in Lieu of Foreclosure on the day and year first above written.

Grantor Signature: ___________________________

Date: __________________

Grantee Signature: ___________________________

Date: __________________

This Deed must be recorded in the appropriate county office to be effective.

| Fact Name | Description |

|---|---|

| Definition | A deed in lieu of foreclosure is a legal agreement where a homeowner voluntarily transfers ownership of their property to the lender to avoid foreclosure. |

| Benefits | This approach can help homeowners avoid the lengthy foreclosure process and mitigate damage to their credit score. |

| State-Specific Forms | Each state may have specific requirements or forms that need to be completed for a deed in lieu of foreclosure. Always check local laws. |

| Governing Laws | The governing laws vary by state. It’s essential to understand these before proceeding. For example, California Civil Code Section 2938 outlines procedures in California. |

| Impact on Credit | While a deed in lieu may be less damaging than a foreclosure, it can still affect credit scores, typically appearing on a report for up to seven years. |

| Eligibility Requirements | Lenders often require homeowners to demonstrate financial hardship and provide supporting documentation before accepting a deed in lieu. |

Once you have decided to complete the Deed in Lieu of Foreclosure form, it's important to carefully follow a series of steps to ensure all necessary information is accurately entered. After submitting the form, you can expect the lender to review it. If they accept the deed, the property will be transferred back to them, relieving you from future mortgage payments.

A Deed in Lieu of Foreclosure is a legal document that allows a borrower to transfer ownership of their property to the lender to avoid foreclosure. In this arrangement, the borrower voluntarily gives up their rights to the property in exchange for the cancellation of the mortgage debt. This option can help borrowers avoid the lengthy and painful foreclosure process, as well as minimize damage to their credit score.

Any homeowner facing financial hardship and struggling to keep up with mortgage payments may consider this option. However, it typically works best for those who are unable to sell their home and are facing imminent foreclosure. Lenders usually prefer this method when the property has little or no equity, and when they believe that the costs of foreclosure would be higher than accepting the deed.

Several benefits may come with choosing a Deed in Lieu of Foreclosure:

There are some drawbacks to consider before proceeding with a Deed in Lieu of Foreclosure:

To initiate a Deed in Lieu of Foreclosure, follow these steps:

In many cases, once the deed is transferred, the borrower can be released from further liability on the mortgage. However, this is not guaranteed. It is essential to negotiate the terms with the lender and ensure that there is a mutual understanding regarding any remaining debt obligations. Always confirm the terms in writing to avoid unexpected responsibilities.

The impact on your credit report can be less severe compared to a foreclosure. Generally, a Deed in Lieu of Foreclosure is reported as a settled account, which can result in a less negative mark on your credit compared to a foreclosure. However, the specifics of individual credit reports can vary widely, so it is essential to obtain guidance from a credit expert or financial advisor for personalized advice.

Filling out a Deed in Lieu of Foreclosure form is a significant step that can help homeowners avoid foreclosure. However, mistakes made during this process can complicate matters. Here are seven common mistakes to watch out for.

First, people often fail to provide accurate property details. When filling out the form, it’s crucial to include the correct legal description of the property. Omitted or incorrect information can lead to confusion or delays in processing.

Next, many individuals neglect to disclose all lienholders. If there are multiple loans secured by the property, listing them is essential. Failing to mention all lienholders can create problems later on, as all parties need to agree for the deed to be valid.

Also, misunderstanding the implications of a Deed in Lieu can be problematic. Some homeowners mistakenly believe this process will not impact their credit score. In reality, it can still lead to negative credit consequences, which should be taken into account before proceeding.

Another common mistake involves not seeking legal or financial advice. Many individuals fill out the form without consulting a professional. This can lead to oversights and decisions that may not be in the homeowner's best interest.

Additionally, people sometimes rush through the process. Taking time to thoroughly review all entries in the form is important. Errors can result from hasty decisions and may require resubmission, prolonging resolution.

People may also forget to gather necessary supporting documentation. This includes proof of financial hardship or the original loan documents. Missing documents can slow down the process, making it critical to include all required paperwork upfront.

Lastly, homeowners often overlook the importance of communicating with their lender. Before submitting the Deed in Lieu form, it’s advisable to keep open lines of communication with the lender. Not doing so can lead to misunderstandings about the process and the homeowner's intentions.

A Deed in Lieu of Foreclosure is an important step in the process of resolving mortgage delinquency. Alongside this form, several other documents may be required to ensure the process is complete and legally binding. These additional forms help clarify the intentions of both parties and protect their rights throughout the transition.

Gathering all relevant documents is essential for facilitating a smooth transition during a deed in lieu of foreclosure. By being prepared and informed, individuals can navigate through this process with confidence and clarity.

When filling out the Deed in Lieu of Foreclosure form, it's important to follow certain guidelines. Below is a list of things you should and shouldn't do to ensure the process goes smoothly.

Following these guidelines can help facilitate a more efficient process in handling your Deed in Lieu of Foreclosure.

When dealing with troubled mortgages, a Deed in Lieu of Foreclosure can seem like a straightforward solution. However, various misconceptions surround this option. Understanding these myths is vital for homeowners facing potential foreclosure.

Recognizing and addressing these misconceptions can empower homeowners to make informed decisions in challenging situations. The more you know, the better equipped you are to navigate your options.

The Deed in Lieu of Foreclosure form can be an important tool for homeowners facing foreclosure. Here are some key takeaways to consider:

New Jersey Quitclaim Deed Form - This deed is often used between familiar parties, like family members or friends.