The FHA Amendatory Clause form plays a crucial role in real estate transactions involving properties financed through the Federal Housing Administration (FHA). This form is designed to protect buyers by ensuring that they are not obligated to proceed with a purchase unless they receive an appraisal confirming that the property's value meets or exceeds the agreed-upon sales price. Specifically, the clause stipulates that if the appraised value falls short, buyers can walk away without facing penalties, such as losing their earnest money deposits. It is important to note that the appraised value is not a guarantee of the property’s condition or worth, but rather a benchmark used by the Department of Housing and Urban Development (HUD) to determine the maximum mortgage amount it will insure. The form also includes a certification section where all parties involved—the buyer, seller, and real estate agents—attest to the accuracy of the sales contract terms. This signature confirms that any additional agreements related to the transaction are included or attached to the sales agreement. Understanding the nuances of this form is essential for all parties to ensure compliance with federal regulations and to facilitate a smooth transaction.

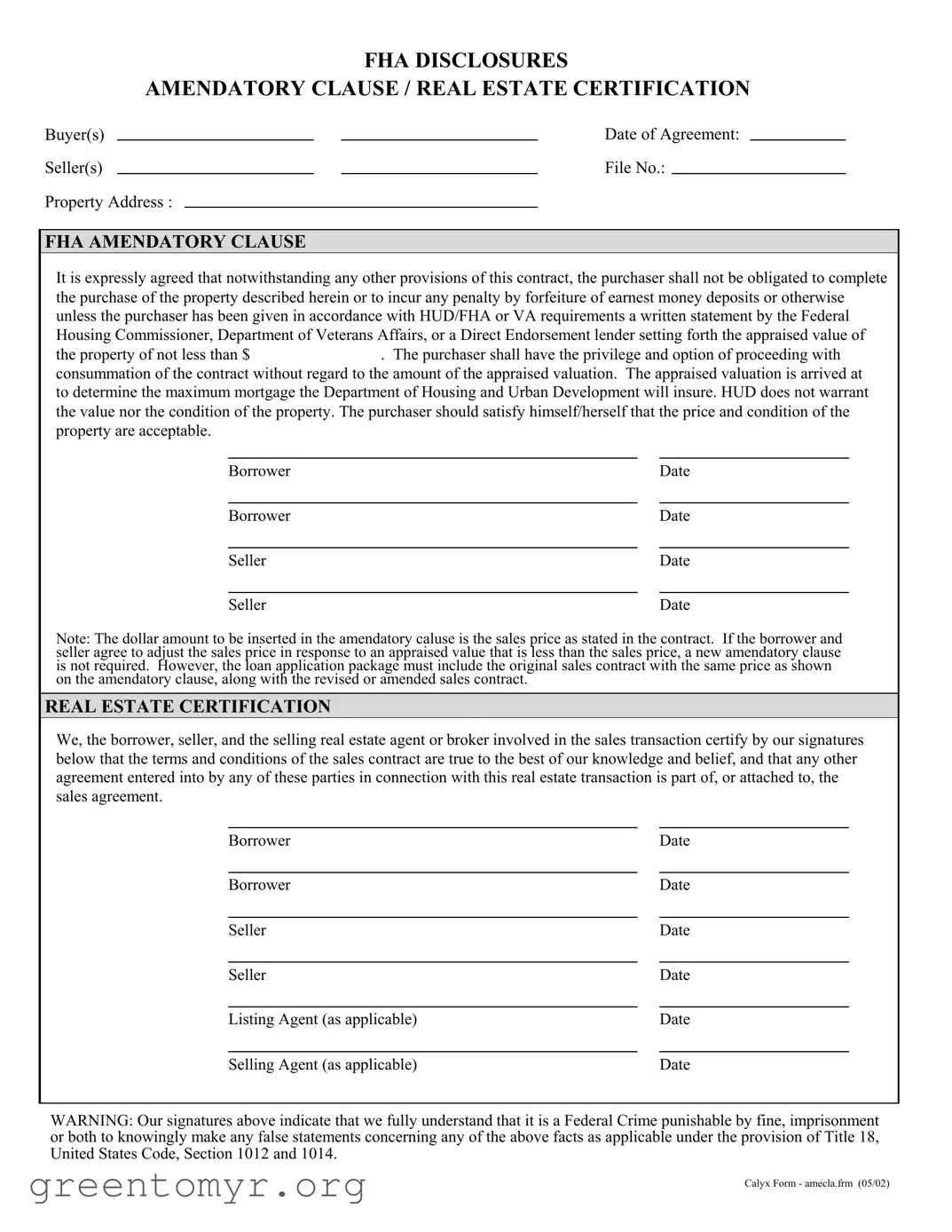

FHA DISCLOSURES

AMENDATORY CLAUSE / REAL ESTATE CERTIFICATION

Buyer(s) |

|

|

|

|

Date of Agreement: |

|

|

Seller(s) |

|

|

|

|

File No.: |

|

|

Property Address : |

|

|

|

|

|

|

|

FHA AMENDATORY CLAUSE

It is expressly agreed that notwithstanding any other provisions of this contract, the purchaser shall not be obligated to complete the purchase of the property described herein or to incur any penalty by forfeiture of earnest money deposits or otherwise unless the purchaser has been given in accordance with HUD/FHA or VA requirements a written statement by the Federal Housing Commissioner, Department of Veterans Affairs, or a Direct Endorsement lender setting forth the appraised value of

the property of not less than $. The purchaser shall have the privilege and option of proceeding with consummation of the contract without regard to the amount of the appraised valuation. The appraised valuation is arrived at to determine the maximum mortgage the Department of Housing and Urban Development will insure. HUD does not warrant the value nor the condition of the property. The purchaser should satisfy himself/herself that the price and condition of the property are acceptable.

Borrower |

Date |

|

|

|

|

Borrower |

Date |

|

|

|

|

Seller |

|

Date |

|

|

|

Seller |

|

Date |

Note: The dollar amount to be inserted in the amendatory caluse is the sales price as stated in the contract. If the borrower and seller agree to adjust the sales price in response to an appraised value that is less than the sales price, a new amendatory clause is not required. However, the loan application package must include the original sales contract with the same price as shown on the amendatory clause, along with the revised or amended sales contract.

REAL ESTATE CERTIFICATION

We, the borrower, seller, and the selling real estate agent or broker involved in the sales transaction certify by our signatures below that the terms and conditions of the sales contract are true to the best of our knowledge and belief, and that any other agreement entered into by any of these parties in connection with this real estate transaction is part of, or attached to, the sales agreement.

Borrower |

Date |

|

|

|

|

Borrower |

Date |

|

|

|

|

Seller |

|

Date |

|

|

|

Seller |

|

Date |

|

|

|

Listing Agent (as applicable) |

|

Date |

|

|

|

Selling Agent (as applicable) |

|

Date |

WARNING: Our signatures above indicate that we fully understand that it is a Federal Crime punishable by fine, imprisonment or both to knowingly make any false statements concerning any of the above facts as applicable under the provision of Title 18, United States Code, Section 1012 and 1014.

Calyx Form - amecla.frm (05/02)

| Fact Name | Description |

|---|---|

| Purpose | The FHA Amendatory Clause protects buyers by ensuring they are not obligated to complete the purchase if the appraised value is below the sales price. |

| Appraised Value Requirement | A written statement of appraised value must be provided by a Federal Housing Commissioner, Department of Veterans Affairs, or a Direct Endorsement lender. |

| Non-Obligation Clause | Buyers are not required to incur penalties, such as forfeiting earnest money, if the appraised value is insufficient. |

| Valuation Role | The appraised value determines the maximum mortgage amount that HUD will insure, but does not guarantee property value or condition. |

| Buyer's Responsibility | It is the buyer's duty to ensure that the price and condition of the property meet their expectations. |

| Sales Price Adjustment | If the sales price is adjusted due to a low appraisal, a new amendatory clause is not necessary, but the original contract must be included in the loan package. |

| Real Estate Certification | All parties involved in the transaction must certify the accuracy of the sales contract terms with their signatures. |

| Legal Warning | Providing false information in this context is a federal crime, punishable by fines or imprisonment. |

| State-Specific Forms | Different states may have specific requirements or forms, governed by their respective real estate laws. |

| Documentation | All documents must be properly completed and submitted to ensure compliance with FHA and VA guidelines. |

Once you have gathered the necessary information, you can begin filling out the FHA Amendatory Clause form. This form is essential for ensuring that both buyers and sellers are aware of the appraisal requirements and the implications of the purchase agreement. Follow these steps carefully to complete the form accurately.

After completing the form, ensure that all signatures are in place. This document will be a crucial part of your loan application package, along with the original sales contract. It's important to keep a copy for your records and to provide any required documentation to your lender promptly.

The FHA Amendatory Clause is a provision included in real estate contracts when a buyer is obtaining an FHA loan. This clause protects the buyer by allowing them to withdraw from the purchase if the appraised value of the property is less than the agreed-upon sales price. It ensures that the buyer is not financially obligated to complete the transaction under unfavorable conditions.

This clause is crucial because it safeguards the buyer's interests. If the property is appraised at a lower value than the sales price, the buyer can avoid penalties such as losing their earnest money deposit. It provides a safety net, ensuring that buyers are not overpaying for a property based on inflated valuations.

All parties involved in the transaction need to sign the FHA Amendatory Clause. This includes the buyer(s), seller(s), and any real estate agents or brokers involved. Each signature indicates agreement to the terms and understanding of the implications of the clause.

If the appraised value comes in lower than the sales price, the buyer has the option to withdraw from the purchase without facing penalties. They can choose to negotiate a new price with the seller or decide to walk away from the deal altogether.

No, a new FHA Amendatory Clause is not required if the buyer and seller agree to adjust the sales price after an appraisal. However, the loan application package must include the original sales contract with the original price and the revised sales contract reflecting the new price.

The Real Estate Certification is a statement signed by the borrower, seller, and real estate agents involved in the transaction. It certifies that the terms of the sales contract are accurate to the best of their knowledge. This certification helps ensure transparency and accountability among all parties involved.

Making false statements in the Real Estate Certification can lead to severe consequences. It is considered a federal crime under Title 18, United States Code, Sections 1012 and 1014. Penalties can include fines, imprisonment, or both, highlighting the importance of honesty in real estate transactions.

Buyers should conduct their own research and due diligence regarding the property’s value and condition. This may include hiring a separate appraiser or conducting a thorough inspection. It is essential for buyers to feel confident that the price and condition of the property meet their expectations before finalizing the purchase.

While the FHA Amendatory Clause itself cannot be modified, the terms of the sales contract can be negotiated between the buyer and seller. Any changes to the contract should be documented properly to ensure all parties are aware and in agreement with the new terms.

Filling out the FHA Amendatory Clause form can be straightforward, but mistakes often happen. Here are nine common errors to avoid.

First, many people forget to include the appraised value of the property. This value is crucial because it helps determine the maximum mortgage amount that HUD will insure. Leaving it blank can lead to confusion and delays in the transaction.

Another frequent mistake is not entering the correct sales price in the amendatory clause. The dollar amount should match the sales price stated in the contract. If these figures don’t align, it can create complications down the line.

Some individuals overlook the importance of signatures. All parties involved—buyers, sellers, and agents—must sign the form. Missing a signature can invalidate the agreement, causing unnecessary headaches.

Additionally, people sometimes fail to attach necessary documents. If the sales price changes due to a lower appraised value, the original sales contract must still be included. This ensures that all parties have a clear understanding of the terms.

Another common error is misunderstanding the implications of the FHA Amendatory Clause. Some believe it guarantees the property's value, but that’s not the case. HUD does not warrant the value or condition of the property, so buyers should do their own due diligence.

It’s also easy to misinterpret the clause's purpose. The amendatory clause protects buyers, allowing them to back out if the appraised value is less than the agreed price. Failing to grasp this can lead to unnecessary stress.

People may also neglect to double-check their information. Simple typos or incorrect dates can lead to significant issues. Always review the form before submitting it to ensure everything is accurate.

Lastly, some forget the legal implications. It’s essential to understand that providing false information can lead to serious consequences, including fines or imprisonment. Awareness of this fact can encourage honesty and diligence.

By avoiding these common mistakes, you can ensure a smoother transaction process. Take your time, review your entries, and don’t hesitate to ask for help if needed.

When navigating the complexities of real estate transactions, several documents often accompany the FHA Amendatory Clause form. Each document plays a crucial role in ensuring that all parties are informed and protected throughout the process. Below is a list of commonly used forms that work in conjunction with the FHA Amendatory Clause.

Understanding these documents and their purposes can greatly assist in making informed decisions during the home buying process. Each form contributes to a clearer picture of the transaction, ensuring that all parties are aligned and protected.

When filling out the FHA Amendatory Clause form, it is essential to follow specific guidelines to ensure accuracy and compliance. Below is a list of things you should and shouldn't do during this process.

Here are ten misconceptions about the FHA Amendatory Clause form, along with clarifications:

Here are key takeaways regarding the FHA Amendatory Clause form: