In the state of Georgia, homeowners facing the daunting prospect of foreclosure have an alternative solution that can help alleviate some of the associated stress: the Deed in Lieu of Foreclosure form. This legal document allows a homeowner to voluntarily transfer the title of their property back to the lender, effectively sidestepping the lengthy and often complicated foreclosure process. By executing this form, the homeowner can potentially mitigate the negative impact on their credit score and avoid the public auction of their home. Importantly, the Deed in Lieu of Foreclosure can also pave the way for a smoother transition into a new living situation, as it often comes with the possibility of negotiating a deficiency waiver, which means the lender may forgive any remaining debt after the property is sold. Understanding the nuances of this form is crucial for homeowners who wish to take control of their financial future and navigate the challenges of property ownership in distressing times. It is essential to consider all aspects of this option, including eligibility requirements, potential tax implications, and the overall effect on one’s financial standing.

Georgia Deed in Lieu of Foreclosure Template

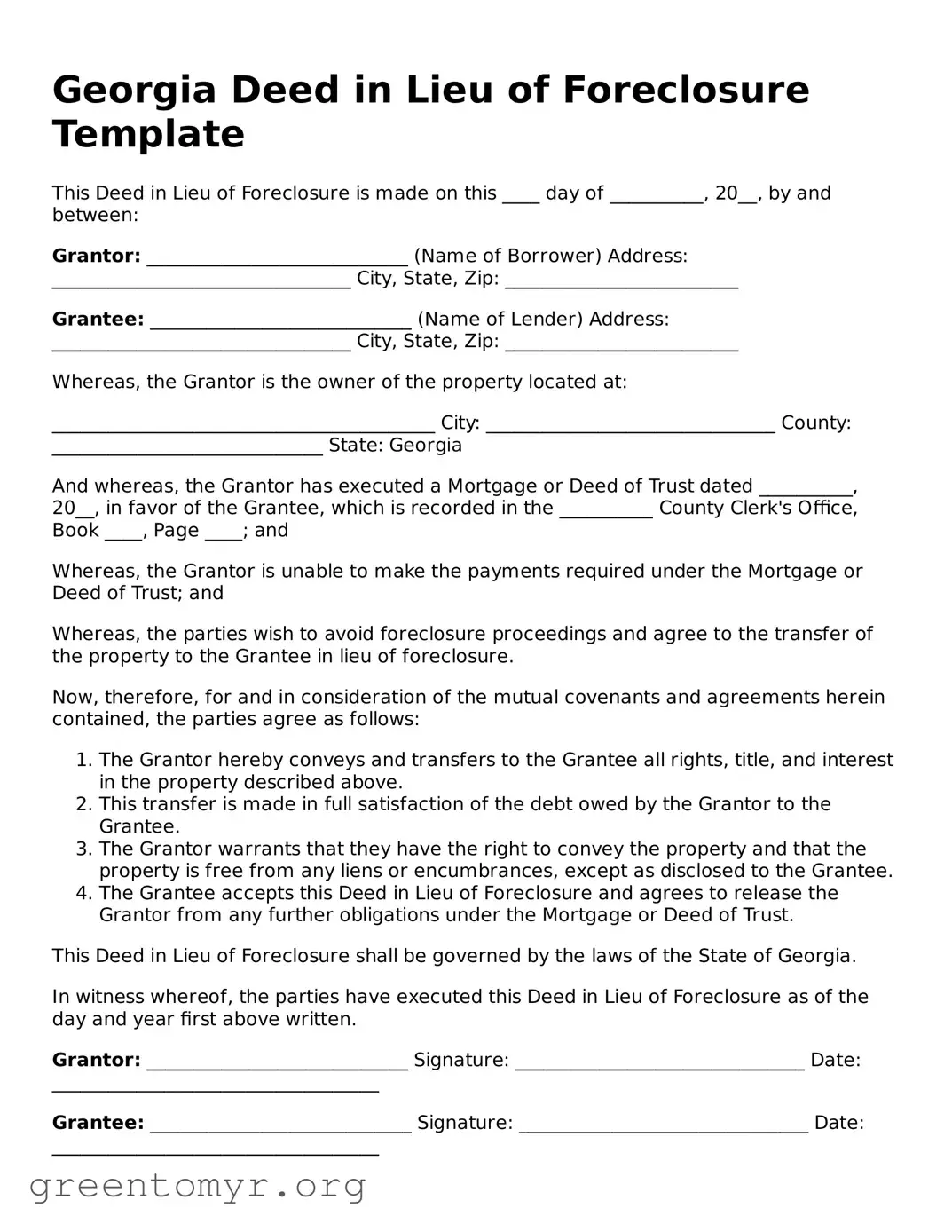

This Deed in Lieu of Foreclosure is made on this ____ day of __________, 20__, by and between:

Grantor: ____________________________ (Name of Borrower) Address: ________________________________ City, State, Zip: _________________________

Grantee: ____________________________ (Name of Lender) Address: ________________________________ City, State, Zip: _________________________

Whereas, the Grantor is the owner of the property located at:

_________________________________________ City: _______________________________ County: _____________________________ State: Georgia

And whereas, the Grantor has executed a Mortgage or Deed of Trust dated __________, 20__, in favor of the Grantee, which is recorded in the __________ County Clerk's Office, Book ____, Page ____; and

Whereas, the Grantor is unable to make the payments required under the Mortgage or Deed of Trust; and

Whereas, the parties wish to avoid foreclosure proceedings and agree to the transfer of the property to the Grantee in lieu of foreclosure.

Now, therefore, for and in consideration of the mutual covenants and agreements herein contained, the parties agree as follows:

This Deed in Lieu of Foreclosure shall be governed by the laws of the State of Georgia.

In witness whereof, the parties have executed this Deed in Lieu of Foreclosure as of the day and year first above written.

Grantor: ____________________________ Signature: _______________________________ Date: ___________________________________

Grantee: ____________________________ Signature: _______________________________ Date: ___________________________________

Witness: _______________________________ Date: ___________________________________

Notary Public: __________________________ My Commission Expires: ___________________

| Fact Name | Details |

|---|---|

| Definition | A deed in lieu of foreclosure is a legal document where a borrower voluntarily transfers ownership of their property to the lender to avoid foreclosure. |

| Governing Law | The deed in lieu of foreclosure in Georgia is governed by state law, particularly under O.C.G.A. § 44-14-233. |

| Process | The borrower must request the deed in lieu from the lender, who will then evaluate the borrower's financial situation. |

| Benefits | This process can help borrowers avoid the lengthy and costly foreclosure process, preserving their credit score to some extent. |

| Requirements | Typically, the borrower must be in default on their mortgage, and the property must be free of liens other than the mortgage being addressed. |

| Impact on Credit | While a deed in lieu of foreclosure is less damaging than a foreclosure, it can still negatively impact the borrower’s credit score. |

| Tax Implications | Borrowers may face tax consequences on any forgiven debt, as the IRS may consider it taxable income. |

| Alternatives | Other options include loan modification or short sale, which may be more favorable depending on the borrower's circumstances. |

After obtaining the Georgia Deed in Lieu of Foreclosure form, it is essential to fill it out accurately to ensure a smooth transition of property ownership. This document allows a homeowner to voluntarily transfer their property to the lender, which can help avoid the foreclosure process. Following the steps below will guide you in completing the form properly.

Once the form is completed and signed, it should be submitted to the lender for processing. The lender will then review the document and proceed with the necessary steps to finalize the transfer of ownership. It is advisable to follow up with the lender to confirm receipt and address any further requirements they may have.

A Deed in Lieu of Foreclosure is a legal agreement in which a homeowner voluntarily transfers the title of their property to the lender to avoid foreclosure. This process allows the homeowner to walk away from the mortgage obligation while the lender takes possession of the property.

Homeowners who are facing financial difficulties and are unable to keep up with mortgage payments may qualify. However, lenders typically look for the following criteria:

There are several advantages to this option, including:

Yes, there are some potential downsides, such as:

The process generally involves the following steps:

No, once the Deed in Lieu of Foreclosure is executed, the homeowner must vacate the property. The lender will take possession and may begin the process of selling it. It is important to discuss timelines with the lender.

While a Deed in Lieu of Foreclosure may be less damaging than a foreclosure, it can still negatively impact your credit score. The exact effect will depend on various factors, including your overall credit history and how your lender reports the deed to credit bureaus.

While it is not strictly required, seeking legal assistance can be beneficial. An attorney can help navigate the complexities of the process, ensure all documents are correctly completed, and address any potential legal issues that may arise.

Start by contacting your current lender. If they are unwilling to consider a Deed in Lieu of Foreclosure, you may want to explore other lenders who specialize in such arrangements. Additionally, consulting with a housing counselor or attorney can provide guidance on finding a suitable lender.

In most cases, the mortgage balance will be satisfied once the Deed in Lieu of Foreclosure is executed. However, it is crucial to confirm with the lender whether any remaining balance will be forgiven or if there are any stipulations regarding the remaining debt.

Filling out the Georgia Deed in Lieu of Foreclosure form can be a daunting task. Many individuals make critical mistakes that can complicate or delay the process. Understanding these common pitfalls is essential for a smooth transition.

One frequent error is failing to provide accurate property information. This includes not listing the correct address or legal description of the property. Inaccuracies can lead to confusion and may render the deed invalid. Always double-check these details to ensure they match official records.

Another mistake is neglecting to include all necessary signatures. Both the borrower and the lender must sign the document for it to be legally binding. Omitting a signature can lead to significant delays, as the document will need to be redone and re-signed.

People often overlook the requirement for notarization. The deed must be notarized to be accepted. Failing to have the document notarized can result in rejection by the lender or county office, which can prolong the foreclosure process unnecessarily.

Additionally, some individuals forget to provide a clear statement of intent. The purpose of the deed must be explicitly stated to avoid any ambiguity. Without this, lenders may question the legitimacy of the transaction.

Another common mistake is not understanding the tax implications. Individuals may not realize that a deed in lieu of foreclosure can have tax consequences. Consulting with a tax professional before proceeding can prevent unexpected financial burdens.

Lastly, many people fail to communicate effectively with their lender. Open lines of communication can help clarify expectations and requirements. Not keeping the lender informed can lead to misunderstandings and further complications.

By being aware of these seven mistakes, individuals can navigate the Georgia Deed in Lieu of Foreclosure process more effectively. Taking the time to understand the requirements and ensuring accuracy can save time and stress in the long run.

When navigating the process of a deed in lieu of foreclosure in Georgia, several forms and documents often accompany it. These documents help ensure that all parties understand their rights and responsibilities, and they facilitate a smoother transaction. Below is a list of commonly used forms and documents in conjunction with the Georgia Deed in Lieu of Foreclosure.

Understanding these documents can significantly aid in the process of a deed in lieu of foreclosure. Each plays a crucial role in ensuring that the transaction is clear, fair, and legally sound. Familiarity with these forms can empower borrowers and lenders alike to navigate this challenging situation more effectively.

A Deed in Lieu of Foreclosure is a significant legal document that can help both borrowers and lenders navigate the complexities of property ownership when facing financial difficulties. It is similar to several other documents in its purpose and implications. Below are four documents that share similarities with the Deed in Lieu of Foreclosure:

Understanding these documents can empower homeowners facing financial distress to make informed decisions. Each option has its own implications and may be more suitable depending on individual circumstances. Consulting with a legal professional can provide clarity and guidance tailored to specific needs.

When filling out the Georgia Deed in Lieu of Foreclosure form, it is crucial to approach the process with care and attention to detail. Here are ten important dos and don'ts to consider:

Many people have misunderstandings about the Georgia Deed in Lieu of Foreclosure form. Here are six common misconceptions:

Some believe that signing a deed in lieu of foreclosure cancels all outstanding debts. In reality, it only transfers the property back to the lender. Any remaining debts may still need to be addressed separately.

A deed in lieu of foreclosure is not the same as a short sale. In a short sale, the property is sold for less than what is owed, with lender approval. A deed in lieu simply involves handing over the property to the lender.

While some may think that a deed in lieu is a fast solution, it can still take time. The lender must review the request, assess the property, and complete necessary paperwork before finalizing the process.

Many assume that a deed in lieu of foreclosure does not affect credit scores. However, it can have a negative impact, similar to a foreclosure, and may remain on credit reports for several years.

Not everyone qualifies for a deed in lieu of foreclosure. Lenders typically require borrowers to demonstrate financial hardship and may also have specific eligibility criteria.

Some people think that signing a deed in lieu releases them from all legal obligations related to the property. However, it may not absolve them from any potential deficiencies or other obligations tied to the mortgage.

When considering the Georgia Deed in Lieu of Foreclosure form, it is essential to understand the implications and processes involved. Here are some key takeaways: