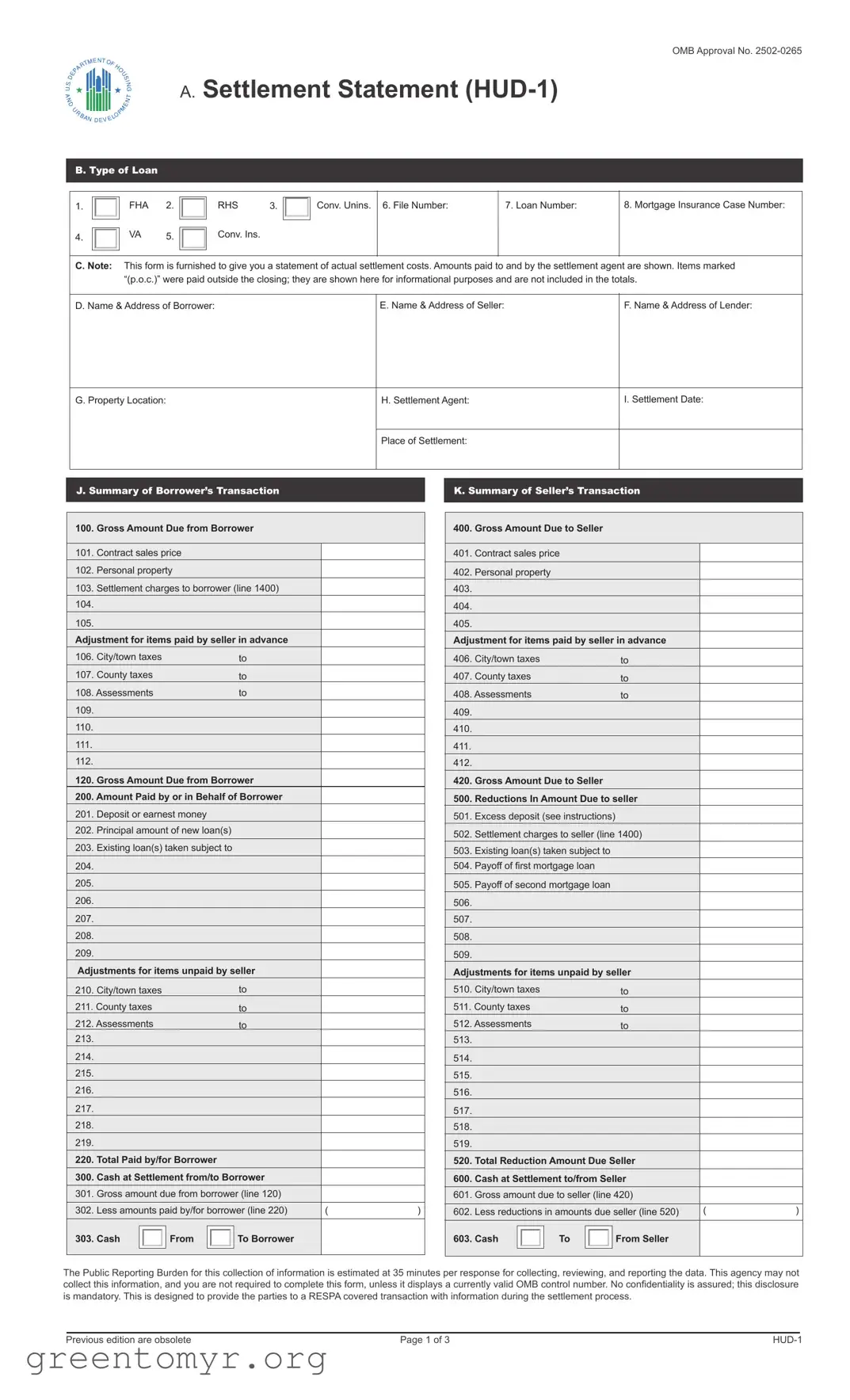

The HUD-1 Settlement Statement is a crucial document in the home buying and refinancing process, serving as a detailed summary of the financial transaction between the buyer and seller. It outlines all the costs associated with the purchase of real estate, including the loan amount, closing costs, and any adjustments made for taxes or other fees. This form provides transparency, ensuring that both parties understand their financial obligations. Each section of the HUD-1 breaks down specific expenses, such as loan origination fees, title insurance, and property taxes, enabling buyers to see exactly where their money is going. Additionally, it includes information about the seller’s proceeds from the sale, giving a complete picture of the transaction. The form is typically prepared by the settlement agent and must be provided to the buyer and seller at least one day before closing, allowing them to review all details thoroughly. Understanding the HUD-1 Settlement Statement is essential for anyone involved in real estate transactions, as it helps prevent misunderstandings and ensures a smoother closing process.

OMB Approval No.

A. Settlement Statement

B. Type of Loan

1. |

|

FHA |

2. |

|

|

RHS |

3. |

|

Conv. Unins. |

6. File Number: |

|

7. Loan Number: |

8. Mortgage Insurance Case Number: |

|

|

|

|

|

|||||||||

4. |

|

VA |

5. |

|

|

Conv. Ins. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C. Note: |

This form is furnished to give you a statement of actual settlement costs. Amounts paid to and by the settlement agent are shown. Items marked |

||||||||||||

|

|

“(p.o.c.)” were paid outside the closing; they are shown here for informational purposes and are not included in the totals. |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

D. Name & Address of Borrower: |

|

|

|

|

E. Name & Address of Seller: |

|

F. Name & Address of Lender: |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

G. Property Location: |

|

|

|

|

|

|

|

H. Settlement Agent: |

|

I. Settlement Date: |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Place of Settlement: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

J. Summary of Borrower’s Transaction

K. Summary of Seller’s Transaction

100.Gross Amount Due from Borrower

101.Contract sales price

102. |

Personal property |

|

|

|

|||

103. |

Settlement charges to borrower (line 1400) |

|

|

||||

104. |

|

|

|

|

|

|

|

105. |

|

|

|

|

|

|

|

Adjustment for items paid by seller in advance |

|

|

|||||

106. |

City/town taxes |

|

|

to |

|

|

|

107. |

County taxes |

|

|

to |

|

|

|

108. Assessments |

|

|

to |

|

|

||

109. |

|

|

|

|

|

|

|

110. |

|

|

|

|

|

|

|

111. |

|

|

|

|

|

|

|

112. |

|

|

|

|

|

|

|

120. Gross Amount Due from Borrower |

|

|

|||||

200. Amount Paid by or in Behalf of Borrower |

|

|

|||||

201. |

Deposit or earnest money |

|

|

|

|||

202. |

Principal amount of new loan(s) |

|

|

|

|||

|

|

|

|

|

|

|

|

203. |

Existing loan(s) taken subject to |

|

|

|

|||

204. |

|

|

|

|

|

|

|

205. |

|

|

|

|

|

|

|

206. |

|

|

|

|

|

|

|

207. |

|

|

|

|

|

|

|

208. |

|

|

|

|

|

|

|

209. |

|

|

|

|

|

|

|

Adjustments for items unpaid by seller |

|

|

|||||

210. |

City/town taxes |

|

|

to |

|

|

|

211. County taxes |

|

|

to |

|

|

||

212. Assessments |

|

|

to |

|

|

||

213. |

|

|

|

|

|

|

|

214. |

|

|

|

|

|

|

|

215. |

|

|

|

|

|

|

|

216. |

|

|

|

|

|

|

|

217. |

|

|

|

|

|

|

|

218. |

|

|

|

|

|

|

|

219. |

|

|

|

|

|

|

|

220. |

Total Paid by/for Borrower |

|

|

|

|||

300. |

Cash at Settlement from/to Borrower |

|

|

||||

301. |

Gross amount due from borrower (line 120) |

|

|

||||

|

|

|

|

|

|

|

|

302. |

Less amounts paid by/for borrower (line 220) |

( |

) |

||||

|

|

|

|

|

|

|

|

303. Cash |

|

From |

|

To Borrower |

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

400.Gross Amount Due to Seller

401.Contract sales price

402. |

Personal property |

|

|

|

|

|

|

||

403. |

|

|

|

|

|

|

|

|

|

404. |

|

|

|

|

|

|

|

|

|

405. |

|

|

|

|

|

|

|

|

|

Adjustment for items paid by seller in advance |

|

|

|||||||

406. |

City/town taxes |

|

|

|

to |

|

|

||

407. |

County taxes |

|

|

|

to |

|

|

||

408. Assessments |

|

|

|

to |

|

|

|||

409. |

|

|

|

|

|

|

|

|

|

410. |

|

|

|

|

|

|

|

|

|

411. |

|

|

|

|

|

|

|

|

|

412. |

|

|

|

|

|

|

|

|

|

420. Gross Amount Due to Seller |

|

|

|

||||||

500. |

Reductions In Amount Due to seller |

|

|

||||||

501. |

Excess deposit (see instructions) |

|

|

|

|||||

502. |

Settlement charges to seller (line 1400) |

|

|

||||||

503. |

Existing loan(s) taken subject to |

|

|

|

|||||

504. |

Payoff of first mortgage loan |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

505. |

Payoff of second mortgage loan |

|

|

|

|||||

506. |

|

|

|

|

|

|

|

|

|

507. |

|

|

|

|

|

|

|

|

|

508. |

|

|

|

|

|

|

|

|

|

509. |

|

|

|

|

|

|

|

|

|

Adjustments for items unpaid by seller |

|

|

|||||||

510. |

City/town taxes |

|

|

|

to |

|

|

||

511. County taxes |

|

|

|

to |

|

|

|||

512. Assessments |

|

|

|

to |

|

|

|||

513. |

|

|

|

|

|

|

|

|

|

514. |

|

|

|

|

|

|

|

|

|

515. |

|

|

|

|

|

|

|

|

|

516. |

|

|

|

|

|

|

|

|

|

517. |

|

|

|

|

|

|

|

|

|

518. |

|

|

|

|

|

|

|

|

|

519. |

|

|

|

|

|

|

|

|

|

520. |

Total Reduction Amount Due Seller |

|

|

||||||

600. |

Cash at Settlement to/from Seller |

|

|

||||||

601. |

Gross amount due to seller (line 420) |

|

|

||||||

|

|

|

|

|

|

|

|

||

602. |

Less reductions in amounts due seller (line 520) |

( |

) |

||||||

603. Cash |

|

|

To |

|

|

From Seller |

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

The Public Reporting Burden for this collection of information is estimated at 35 minutes per response for collecting, reviewing, and reporting the data. This agency may not collect this information, and you are not required to complete this form, unless it displays a currently valid OMB control number. No confidentiality is assured; this disclosure is mandatory. This is designed to provide the parties to a RESPA covered transaction with information during the settlement process.

|

|

|

|

Previous edition are obsolete |

Page 1 of 3 |

||

L. Settlement Charges

700. |

Total Real Estate Broker Fees |

Paid From |

Paid From |

|

|

Division of commission (line 700) as follows : |

Borrower’s |

Seller’s |

|

701. |

$ |

to |

Funds at |

Funds at |

Settlement |

Settlement |

|||

702. |

$ |

to |

|

|

703. |

Commission paid at settlement |

|

|

|

704. |

|

|

|

|

|

|

|

|

|

800. |

Items Payable in Connection with Loan |

|

|

|

|

|

|

|

801. |

Our origination charge |

|

|

|

$ |

(from GFE #1) |

|

|

802. |

Your credit or charge (points) for the specific interest rate chosen |

|

$ |

(from GFE #2) |

|

|

||

803. |

Your adjusted origination charges |

|

|

|

|

(from GFE #A) |

|

|

804. Appraisal fee to |

|

|

|

|

(from GFE #3) |

|

|

|

805. |

Credit report to |

|

|

|

|

(from GFE #3) |

|

|

806. |

Tax service to |

|

|

|

|

(from GFE #3) |

|

|

807. |

Flood certification to |

|

|

|

|

(from GFE #3) |

|

|

808. |

|

|

|

|

|

|

|

|

809. |

|

|

|

|

|

|

|

|

810. |

|

|

|

|

|

|

|

|

811. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

900. Items Required by Lender to be Paid in Advance |

|

|

|

|

|

|||

901. |

Daily interest charges from |

to |

@ $ |

/day |

|

(from GFE #10) |

|

|

902. |

Mortgage insurance premium for |

|

months to |

|

|

(from GFE #3) |

|

|

903. |

Homeowner’s insurance for |

|

years to |

|

|

(from GFE #11) |

|

|

904. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1000. |

Reserves Deposited with Lender |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1001. |

Initial deposit for your escrow account |

|

|

(from GFE #9) |

|

|

|

1002. |

Homeowner’s insurance |

|

months @ $ |

per month |

$ |

|

|

1003. |

Mortgage insurance |

|

months @ $ |

per month |

$ |

|

|

|

|

|

|

|

|

|

|

1004. |

Property Taxes |

|

months @ $ |

per month |

$ |

|

|

1005. |

|

|

months @ $ |

per month |

$ |

|

|

1006. |

|

|

months @ $ |

per month |

$ |

|

|

|

|

|

|

|

|

|

|

1007. Aggregate Adjustment |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1100. Title Charges |

|

|

|

|

|

|

|

1101. Title services and lender’s title insurance |

|

|

(from GFE #4) |

|

|

||

1102. Settlement or closing fee |

|

|

|

$ |

|

|

|

1103. Owner’s title insurance |

|

|

|

(from GFE #5) |

|

|

|

1104. Lender’s title insurance |

|

|

|

$ |

|

|

|

1105. Lender’s title policy limit $ |

|

|

|

|

|

|

|

1106. Owner’s title policy limit $ |

|

|

|

|

|

|

|

1107. Agent’s portion of the total title insurance premium to |

|

$ |

|

|

|||

1108. Underwriter’s portion of the total title insurance premium to |

|

$ |

|

|

|||

1109. |

|

|

|

|

|

|

|

1110. |

|

|

|

|

|

|

|

1111. |

|

|

|

|

|

|

|

|

|

|

|

|

|||

1200. Government Recording and Transfer Charges |

|

|

|

|

|||

1201. |

Government recording charges |

|

|

(from GFE #7) |

|

|

|

1202. |

Deed $ |

Mortgage $ |

|

Release $ |

|

|

|

1203. Transfer taxes |

|

|

|

(from GFE #8) |

|

|

|

1204. |

City/County tax/stamps |

Deed $ |

Mortgage $ |

|

|

|

|

1205. |

State tax/stamps |

Deed $ |

Mortgage $ |

|

|

|

|

1206. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1300. Additional Settlement Charges |

|

|

|

|

|

||

1301. |

Required services that you can shop for |

|

|

(from GFE #6) |

|

|

|

1302. |

|

|

|

$ |

|

|

|

1303. |

|

|

|

$ |

|

|

|

1304. |

|

|

|

|

|

|

|

1305. |

|

|

|

|

|

|

|

1400. Total Settlement Charges (enter on lines 103, Section J and 502, Section K)

|

|

|

|

Previous edition are obsolete |

Page 2 of 3 |

||

Comparison of Good Faith Estimate (GFE) and

Charges That Cannot Increase |

|

Our origination charge |

# 801 |

Your credit or charge (points) for the specific interest rate chosen |

# 802 |

Your adjusted origination charges |

# 803 |

Transfer taxes |

# 1203 |

|

|

Good Faith Estimate

Charges That In Total Cannot Increase More Than 10% |

|

|

|

|

|

|

|

Good Faith Estimate |

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Government recording charges |

|

|

# 1201 |

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

# |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

# |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

# |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

# |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

# |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

# |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

# |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

|

|

|

|

|

|

|

|

|

|

Increase between GFE and |

|

$ |

|

|

or |

% |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Charges That Can Change |

|

|

|

|

|

|

|

|

|

Good Faith Estimate |

|

|

||||

Initial deposit for your escrow account |

|

# 1001 |

|

|

|

|

|

|

|

|

|

|

||||

Daily interest charges |

$ |

/day |

# 901 |

|

|

|

|

|

|

|

|

|

|

|||

Homeowner’s insurance |

|

|

# 903 |

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

# |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

# |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

# |

|

|

|

|

|

|

|

|

|

|

|

|

Loan Terms |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Your initial loan amount is |

|

|

$ |

|

|

|

|

|

|

|

|

|

|

|

||

Your loan term is |

|

|

|

|

|

years |

|

|

|

|

|

|

|

|

||

Your initial interest rate is |

|

|

|

|

|

% |

|

|

|

|

|

|

|

|

||

Your initial monthly amount owed for principal, interest, and any |

$ |

|

|

includes |

|

|

|

|

|

|

|

|

||||

mortgage insurance is |

|

|

|

|

Principal |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

Interest |

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

Mortgage Insurance |

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Can your interest rate rise? |

|

|

|

|

No |

|

Yes, it can rise to a maximum of |

%. The first change will be on |

||||||||

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

and can change again every |

|

|

after |

|

. Every change date, your |

||||||

|

|

|

|

|

interest rate can increase or decrease by |

|

%. Over the life of the loan, your interest rate is |

|||||||||

|

|

|

|

|

guaranteed to never be lower than |

% or higher than |

%. |

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

||||||

Even if you make payments on time, can your loan balance rise? |

|

|

No |

|

Yes, it can rise to a maximum of $ |

|

|

|

|

|||||||

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Even if you make payments on time, can your monthly |

|

|

No |

|

Yes, the first increase can be on |

and the monthly amount |

||||||||||

|

|

|

||||||||||||||

amount owed for principal, interest, and mortgage insurance rise? |

|

owed can rise to $ |

. The maximum it can ever rise to is $ |

. |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Does your loan have a prepayment penalty? |

|

|

|

No |

|

Yes, your maximum prepayment penalty is $ |

|

|

|

|||||||

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Does your loan have a balloon payment? |

|

|

|

No |

|

Yes, you have a balloon payment of $ |

|

due in |

years |

|||||||

|

|

|

|

|

||||||||||||

|

|

|

|

|

on |

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

Total monthly amount owed including escrow account payments |

|

|

You do not have a monthly escrow payment for items, such as property taxes and |

|||||||||||||

|

|

|||||||||||||||

|

|

|

|

|

|

homeowner’s insurance. You must pay these items directly yourself. |

|

|||||||||

|

|

|

|

|

|

You have an additional monthly escrow payment of $ |

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

that results in a total initial monthly amount owed of $ |

|

. This includes |

||||||||

|

|

|

|

|

|

principal, interest, any mortagage insurance and any items checked below: |

|

|||||||||

|

|

|

|

|

|

Property taxes |

|

|

|

|

Homeowner’s insurance |

|

||||

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

Flood insurance |

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Note: If you have any questions about the Settlement Charges and Loan Terms listed on this form, please contact your lender.

|

|

|

|

Previous edition are obsolete |

Page 3 of 3 |

||

| Fact Name | Description |

|---|---|

| Purpose | The HUD-1 Settlement Statement is used to itemize all charges and credits to the buyer and seller in a real estate transaction. |

| History | This form was created by the Department of Housing and Urban Development (HUD) in the 1970s to promote transparency in real estate transactions. |

| Standardization | The HUD-1 form is standardized, which means it is the same across the country, ensuring consistency in how settlement costs are presented. |

| Use Cases | It is primarily used for transactions involving federally related mortgage loans, such as FHA or VA loans. |

| Disclosure Requirements | Federal law requires that the HUD-1 be provided to the borrower at least one day before the closing of the loan. |

| Sections | The form contains sections for itemizing the buyer's and seller's financial obligations, including loan fees, title insurance, and other closing costs. |

| State-Specific Forms | Some states have their own versions or additional forms that must be used alongside the HUD-1, governed by state-specific real estate laws. |

| Transition to Closing Disclosure | Since 2015, the HUD-1 has largely been replaced by the Closing Disclosure form for most transactions, but it is still used for certain types of loans. |

| Accuracy Importance | It is crucial that all information on the HUD-1 is accurate, as discrepancies can lead to legal issues or delays in the closing process. |

| Record Keeping | Both buyers and sellers should keep a copy of the HUD-1 for their records, as it serves as an important document for tax purposes and future reference. |

Filling out the HUD-1 Settlement Statement form is an important step in the real estate transaction process. Once completed, this form will provide a clear overview of all financial aspects related to the closing of a property. It is essential to ensure that every section is filled out accurately to avoid any complications later on.

After completing the HUD-1 Settlement Statement, it is crucial to review the form for accuracy. Any discrepancies should be addressed immediately to ensure a smooth closing process. Once verified, the form will serve as a vital record of the transaction for both the buyer and the seller.

The HUD-1 Settlement Statement is a document used in real estate transactions, primarily for federally related mortgage loans. It outlines all the costs and fees associated with the purchase of a property. Both buyers and sellers receive a copy of this statement at closing.

The settlement agent, often a title company or attorney, prepares the HUD-1 Settlement Statement. They gather all necessary information from the parties involved in the transaction and ensure that all costs are accurately listed.

The HUD-1 includes various details, such as:

Each item is itemized, allowing both parties to see how funds are allocated.

The HUD-1 Settlement Statement is typically provided to both the buyer and seller at least one day before the closing. This allows both parties to review the document and ask questions about any charges or fees listed.

If you believe there is an error on the HUD-1, contact the settlement agent as soon as possible. Review the statement thoroughly and provide any supporting documentation to back up your claim. The agent can help resolve discrepancies before closing.

The HUD-1 is primarily used for reverse mortgages and certain transactions. For most other residential transactions, the Closing Disclosure form has replaced the HUD-1. However, it is still important for those specific cases.

Yes, you can request a copy of the HUD-1 Settlement Statement from your settlement agent or lender after closing. It is advisable to keep this document for your records, as it contains important information regarding your transaction.

If you have questions, reach out to your real estate agent, attorney, or the settlement agent. They can provide clarification on any line items and help you understand the document better.

When filling out the HUD-1 Settlement Statement form, many individuals make common mistakes that can lead to confusion or delays. One frequent error is inaccurate information entry. Buyers and sellers often rush through the process and input incorrect names, addresses, or amounts. This can result in significant issues down the line, especially when it comes to legal documentation and financial transactions.

Another mistake is failing to understand the purpose of each line item on the form. The HUD-1 is detailed, with various fees and charges that may be unfamiliar to those not well-versed in real estate transactions. Misinterpreting these items can lead to overestimating costs or missing essential fees, which can affect the final settlement amount.

People also overlook the importance of reviewing the document thoroughly before signing. It’s crucial to take the time to read through the entire form. Skipping this step can mean agreeing to terms or fees that were not fully understood. This oversight can lead to disputes later, which could have been avoided with careful review.

Lastly, many forget to keep a copy of the completed HUD-1 Settlement Statement for their records. This document is essential for future reference, especially when filing taxes or addressing any potential disputes. Not having a copy can complicate matters if questions arise later regarding the transaction.

The HUD-1 Settlement Statement is a crucial document in real estate transactions, particularly in the context of federally related mortgage loans. It provides a detailed breakdown of the costs associated with the closing of a property. Alongside this form, several other documents are commonly utilized to ensure a smooth transaction process. Below is a list of these documents, each serving a specific purpose in the closing procedure.

Each of these documents plays a vital role in the real estate closing process. Together, they help protect the interests of all parties involved and ensure that the transaction proceeds smoothly and transparently.

When filling out the HUD-1 Settlement Statement form, it's essential to follow specific guidelines to ensure accuracy and compliance. Here’s a helpful list of things to do and avoid:

By following these guidelines, you can help ensure a smooth and efficient transaction process.

The HUD-1 Settlement Statement form is an important document in real estate transactions, particularly for buyers and sellers. However, several misconceptions surround this form, which can lead to confusion during the closing process. Here are four common misconceptions:

Understanding these misconceptions can help individuals navigate the closing process more effectively and ensure that all parties are well-informed about their financial responsibilities.

The HUD-1 Settlement Statement is an important document in real estate transactions. Here are some key takeaways to keep in mind when filling it out and using it: