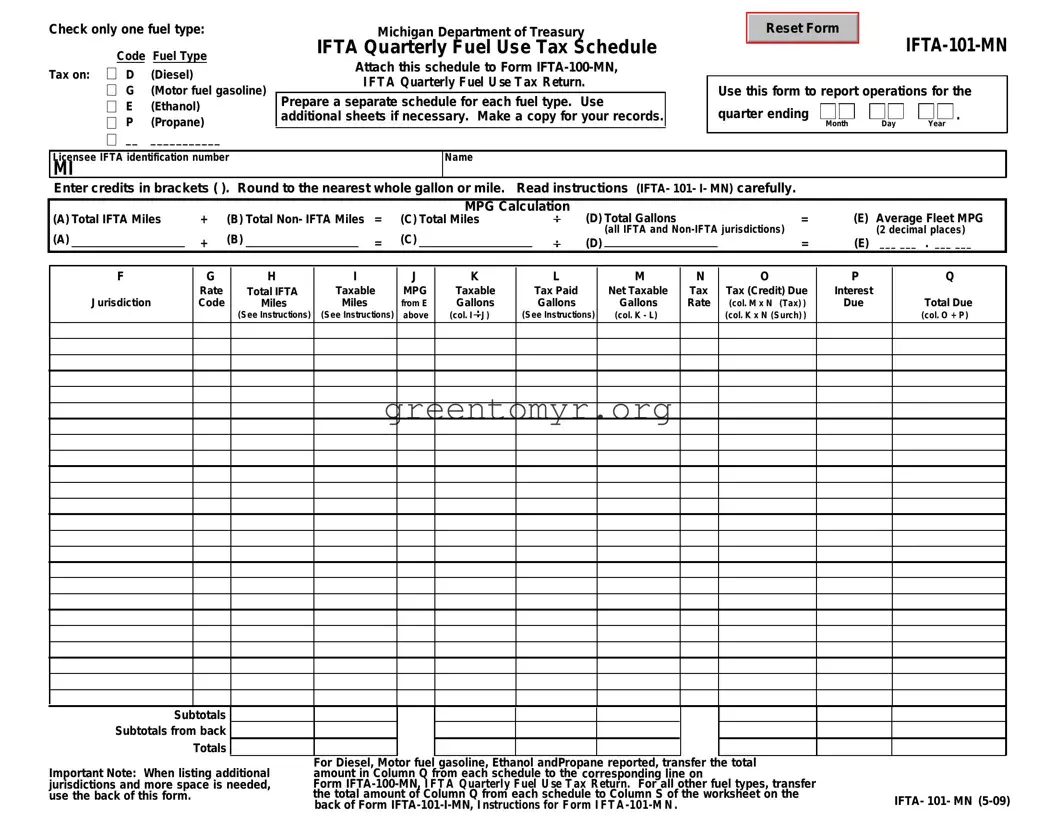

The IFTA 101Mn form plays a critical role in the reporting process for the International Fuel Tax Agreement (IFTA). It is specifically designed for carriers operating in multiple jurisdictions with various fuel types, including diesel, motor gasoline, ethanol, and propane. This quarterly fuel use tax schedule is mandatory for those seeking to accurately report their fuel tax liabilities and utilizes specific codes to distinguish between the fuel types. Each form must be attached to the IFTA-100-MN, which serves as the primary vehicle for filing tax returns under IFTA guidelines. Users will calculate their total miles driven in IFTA and non-IFTA jurisdictions, total gallons of fuel used, and the applicable tax rates. Additionally, the form requires detailed breakdowns for various fuel types, necessitating separate schedules for each. Accuracy is paramount, not only in the reporting details but also in calculating tax credits and dues. Understanding the intricacies of the IFTA 101Mn form and ensuring timely submission is vital for compliance and can prevent potential penalties associated with late filings. Keeping thorough records as prompted in the instructions can facilitate smoother reporting and compliance, thereby safeguarding the interests of motor carriers.

Check only one fuel type:

Tax on: |

Code Fuel Type |

|

D |

(Diesel) |

|

|

G |

(Motor fuel gasoline) |

|

E |

(Ethanol) |

|

P |

(Propane) |

|

__ |

___________ |

Michigan Department of Treasury

IFTA Quarterly Fuel Use Tax Schedule

Attach this schedule to Form

Prepare a separate schedule for each fuel type. Use additional sheets if necessary. Make a copy for your records.

|

Reset Form |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Use this form to report operations for the |

|||

quarter ending Month |

Day |

Year . |

|

Licensee IFTA identification number |

|

|

|

Name |

|

|

|

|

|

|

|

|

|||||

MI |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Enter credits in brackets ( ). Round to the nearest whole gallon or mile. |

Read instructions |

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

MPG Calculation |

|

|

|

|

(E) |

Average Fleet MPG |

||

(A) Total IFTA Miles |

+ |

(B) Total |

= |

(C) Total Miles |

|

: |

(D) Total Gallons |

= |

|||||||||

(A) |

|

|

(B) |

|

|

|

(C) |

|

|

|

|

|

(all IFTA and |

|

|

(2 decimal places) |

|

|

+ |

|

|

= |

|

|

|

: |

(D) |

|

|

= |

(E) |

___ ___ . ___ ___ |

|||

|

|

|

|

|

|||||||||||||

F

Jurisdiction

G

Rate Code

H |

I |

Total IFTA |

Taxable |

Miles |

Miles |

(See Instructions) |

(See Instructions) |

J

MPG

from E above

K

Taxable Gallons

(col. I : J)

L

Tax Paid

Gallons

(See Instructions)

M

Net Taxable

Gallons

(col. K - L)

N

Tax Rate

O

Tax (Credit) Due

(col. M x N (Tax) ) (col. K x N (Surch) )

P

Interest

Due

Q

Total Due

(col. O + P)

Subtotals

Subtotals from back

Totals

Important Note: When listing additional jurisdictions and more space is needed, use the back of this form.

For Diesel, Motor fuel gasoline, Ethanol andPropane reported, transfer the total |

|

amount in Column Q from each schedule to the corresponding line on |

|

Form |

|

the total amount of Column Q from each schedule to Column S of the worksheet on the |

|

back of Form |

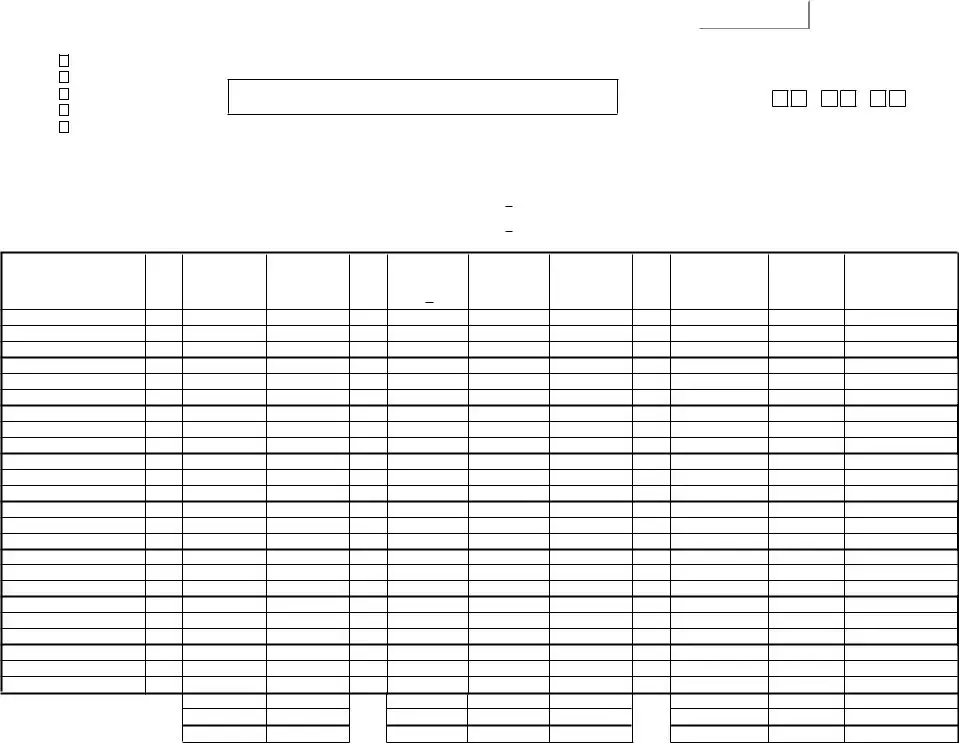

IFTA- |

|

F |

|

||

101- |

|

Jurisdiction |

MN (4/08) (back) |

|

|

|

|

|

Transfer the subtotal amounts to the front of this schedule.

G |

H |

I |

J |

K |

L |

M |

N |

O |

P |

Q |

||

Rate |

Total IFTA |

Taxable |

MPG |

Taxable |

Tax Paid |

Net Taxable |

Tax |

Tax (Credit) Due |

Interest |

Total Due |

||

Code |

Miles |

Miles |

from E |

Gallons |

Gallons |

Gallons |

Rate |

(col. M x N (Tax)) |

Due |

|||

|

(See Instructions) (See Instructions) |

on front |

(col. I |

: |

J) |

(See Instructions) |

(col. K - L) |

|

(col. K x N (Surch)) |

|

(col. O + P) |

|

Subtotals

Instructions for Form |

|

IFTA Quarterly Fuel Use Tax Schedule |

|

A separate Form

Enter your licensee IFTA identification number. This is your federal employer identification number, social security number or other jurisdiction assigned identification number as it appears on your IFTA license.

Enter your legal name as it appears on your IFTA License.

(A) Total IFTA Miles - Enter the total miles traveled in IFTA jurisdictions by all qualified motor vehicles in your fleet using the fuel type indicated on each form/schedule (total from column H). Report all miles traveled whether the miles are taxable or nontaxable. Round mileage to the nearest whole miles

(e.g., 1234.5 = 1235).

(B) Total

(C)Total Miles - Add the amount in item (A) and the amount in item (B) to determine total miles traveled by all qualified motor vehicles in your fleet.

(D)Total Gallons - Enter the total gallons of fuel placed in the propulsion tank in both IFTA and

(e.g., 123.4 = 123).

(E)Average Fleet MPG - Divide item (C) by item (D). Round to 2 decimal places (e.g., 4.567 = 4.57).

Column F - Enter the name of each IFTA jurisdiction that you operated in during the period. Enter the jurisdiction's name on two(2) consecutive lines if the traveled jurisdiction administers a surcharge1in addition to their regular fuel tax. Enter the jurisdiction's two letter abbreviation from Form

Column G - Enter the rate code of the appropriate fuel type for each IFTA jurisdiction from Form

Column H - Enter the total miles traveled (taxable and nontaxable) in each IFTA jurisdiction for this fuel type only. Enter '0' on a surcharge line. Round mileage to the nearest whole miles (e.g., 1234.5 = 1235).

Column I - Enter the IFTA taxable miles for each IFTA jurisdiction. Do not include fuel use trip permit miles. Enter '0' on a surcharge line. Round mileage to the nearest whole miles (e.g., 1234.5 = 1235).

Column J - Enter your average fleet miles per gallon (mpg) from item (E) above. Enter '0' on a surcharge line.

1Jurisdictions with surcharge: Indiana, Kentucky and Virginia.

Column K - Divide the amount in column I by the amount in column J to determine the total taxable gallons of fuel consumed in each IFTA jurisdiction. For surcharge1taxable gallons, enter the taxable gallons from the same jurisdiction's fuel use tax line, Column K. Round gallons to the nearest whole gallon

(e.g., 123.4 = 123.).

Column L - Enter the total

Round gallons to the nearest whole gallon (e.g., 123.4 = 123). Column M - Subtract the amounts in column L from column K for each jurisdiction. Enter '0' on a surcharge line.

-If column K is greater than column L, enter the taxable gallons.

-If column L is greater than column K, enter the credit gallons. Use brackets to indicate credit gallons.

Column N - Enter the rate for the appropriate fuel type from Form

Column O - Multiply the amount in column M by the tax rate for that jurisdiction in column N to determine the tax or credit. Enter any credit amount in brackets. Where a surcharge1is applicable, multiply the amount in Column K by the surcharge rate for that jurisdiction in Column N. Column P - If you file late, compute interest on any tax due for each jurisdiction for each fuel type indicated on each form/schedule. Interest is computed on tax due from the due date of the return until the date payment is received. Interest is computed at 1% per month or part of a month, to a maximum of 12% per year. Returns must be postmarked no later than the last day of the month following the end of the quarter to be timely.

Column Q - For each jurisdiction add the amounts in column O and column P, and enter the total dollar amount due or credit amount. Enter any credit amount in brackets. Subtotals - Add the amounts in columns H, O, P and Q on the front of the schedule and enter on the Subtotals line in the appropriate columns. Add the amounts in columns H, O, P and Q on the back of the schedule and enter in the applicable columns on the Subtotals line below. Enter these amounts in the applicable columns on the front of the schedule on the Subtotals from back line.

Totals - Add the Subtotals and the Subtotals from back to determine the Totals. The total in column Q is the difference of all credits and taxes due for all jurisdictions. Transfer the Totals from Column Q for each fuel type reported to the corresponding line of Form

Make a copy of this return for your records.

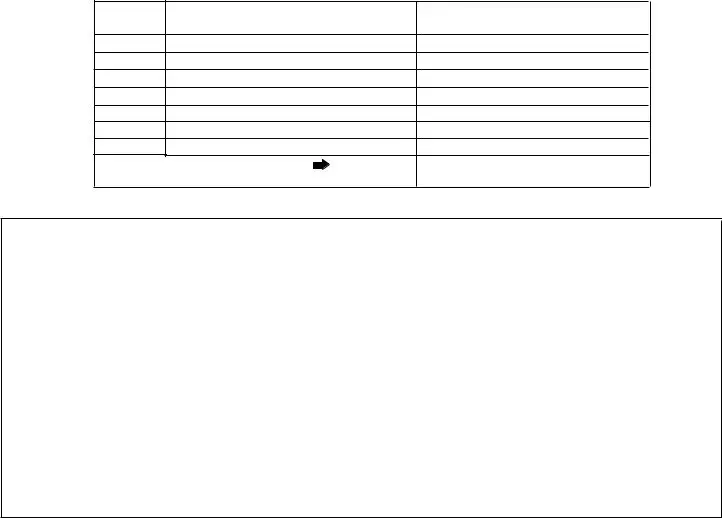

(All Other) Fuel Types Worksheet

Worksheet Instuctions

For each fuel type listed below, enter the total for that fuel from column Q of Form

Fuel Type |

(R) |

(S) |

Code |

(Other) Fuel Type |

Total from Column (Q) of |

C |

CNG |

|

A |

|

|

B |

|

|

F |

|

|

H |

Gasohol |

|

L |

LNG |

|

M |

Methanol |

|

|

TOTAL AMOUNT |

|

Transfer this amount to line 5 of Form |

|

|

Need Help?

The Michigan Department of Treasury has compiled a manual with additional information on IFTA credentials, record keeping and tax reporting, payments and refunds and other frequently asked questions. This manual is available on our Web site at www.michigan.gov/treasury. Select Motor Carrier forms and then form #2838 under Related Documents.

If you have questions or need assistance, contact the Motor Carrier section at (517)

Requests for refunds under $1.00 will carry forward to your next return.

If you need to write, address your letter to:

MICHIGANMichigan DepartmentDEPARTMENTof OFTreasuryTREASURY

SPECIALCustomerTAXESContactDIVISIONDivision, Special Taxes

PP.OO. BOXBox 30474

LANSING,Lansing MI

| Fact Name | Description |

|---|---|

| Fuel Types | The IFTA 101Mn form allows reporting for four fuel types: Diesel (D), Motor Fuel Gasoline (G), Ethanol (E), and Propane (P). |

| Purpose | This form is used to report fuel usage and tax liabilities for the IFTA jurisdictions for a specified quarter. |

| Jurisdictions | Report all miles traveled in both IFTA and non-IFTA jurisdictions to accurately calculate tax owed. |

| Mileage Calculation | The form requires calculations of Total IFTA Miles, Total Non-IFTA Miles, and Total Miles. |

| Taxable Gallons | Taxable gallons are calculated by dividing the total IFTA taxable miles by the average fleet miles per gallon (MPG). |

| State-Specific Laws | The form operates under Michigan law and adheres to regulations set by the Michigan Department of Treasury. |

| Filing Frequency | This form must be completed quarterly, covering the operation quarter ending on the specified month and year. |

| Record Keeping | It's essential to maintain copies of all completed forms and supporting documentation, including fuel receipts. |

To complete the IFTA 101Mn form accurately, follow the outlined steps carefully. This guide provides a clear sequence for filling in required information on each section of the form, ensuring compliance and proper reporting.

After filling out the IFTA 101Mn form, it must be attached to Form IFTA-100-MN for submission. Ensure that all figures are accurate and properly rounded as specified, and remember to keep copies for your own records. Review the instructions for detailed guidance on any additional steps necessary for specific fuel types or circumstances.

The IFTA 101Mn Form, known as the IFTA Quarterly Fuel Use Tax Schedule, is used to report fuel usage for International Fuel Tax Agreement (IFTA) jurisdictions. It allows motor carriers to document their fuel consumption and the miles traveled in various jurisdictions for the relevant quarter. This form must be completed and submitted alongside Form IFTA-100-MN, the IFTA Quarterly Fuel Use Tax Return.

To complete the IFTA 101Mn Form, follow these steps:

Each section includes specific calculations and entries based on the fuel type and the jurisdiction. Refer to the accompanying instructions for detailed guidance.

You can report the following fuel types on the IFTA 101Mn Form:

For each fuel type, a separate IFTA 101Mn form should be completed. If you are reporting a fuel type not listed, indicate this by checking the box next to the blank line and entering the fuel type code and name.

If additional space is required to list jurisdictions, you may use the back of the IFTA 101Mn Form. Ensure that you transfer the totals from the back to the appropriate lines on the front of the form. This maintains accuracy for your reporting.

The Average Fleet MPG (miles per gallon) is calculated by dividing the total miles traveled (IFTA and non-IFTA) by the total gallons of fuel used. This figure should be rounded to two decimal places. For example, if your total miles are 10,000 and total gallons are 1,000, your calculation would be:

Average Fleet MPG = Total Miles / Total Gallons = 10,000 / 1,000 = 10.00 MPG.

If you file the IFTA 101Mn Form late, interest will apply to any tax due. The interest is computed at 1% per month or part of a month, up to a maximum of 12% per year. To avoid additional charges, file your return before the due date, which is the last day of the month following the quarter ending.

Your completed IFTA 101Mn Form should be attached to the IFTA 100-MN form and submitted to:

MICHIGAN DEPARTMENT OF TREASURY

SPECIAL TAXES DIVISION

P.O. BOX 30474

LANSING, MI 48909-7974

For further assistance, the Michigan Department of Treasury offers a manual with more detailed information about IFTA credentials, record keeping, and tax reporting. This manual is accessible on their website. You can also contact the Motor Carrier section directly at (517) 636-4580 for further inquiries. For TDD assistance, dial (517) 636-4999. Their office hours are Monday through Friday, from 8:00 a.m. to 5:00 p.m.

Completing the IFTA 101Mn form can be straightforward, but many individuals make common mistakes that lead to errors in their fuel tax reporting. Here are eight frequent pitfalls to avoid.

First, many people forget to check only one fuel type box. The form explicitly requires the selection of a single fuel type, such as Diesel, Gasoline, Ethanol, or Propane. Omitting this crucial step can lead to misunderstandings and delays in processing the return.

Second, failing to round numbers correctly is another mistake. The instructions specify rounding fuel gallons and miles to the nearest whole number. For instance, if you traveled 1234.5 miles, this should be rounded to 1235. Ignoring this guideline can result in inaccurate calculations that affect tax liabilities.

Another common error involves incorrectly reporting jurisdictions. Each jurisdiction where fuel was used must be accurately listed. Not providing complete and correct names or abbreviations can lead to significant discrepancies in mileage reporting.

Fourth, many individuals overlook the requirement to keep detailed records of fuel purchases. Failing to gather receipts for tax-paid gallons means losing the ability to substantiate claims on the form. Keeping meticulous records is essential for a successful audit trail.

A fifth mistake is miscalculating the Average Fleet MPG. This calculation requires dividing total miles by total gallons. This figure must also be rounded to two decimal places. Any error in this calculation will affect taxable gallons, leading to possible overpayment or underpayment of taxes.

Additionally, some people forget to sign the form before submission. A missing signature could result in the return being rejected, prompting unnecessary delays and paperwork to rectify the situation.

Another area of confusion lies in the transfer of totals between forms. People may incorrectly transfer total amounts from Column Q of the IFTA 101Mn form to the IFTA 100-MN return. Accurate totals are critical for ensuring that tax credits and debits are calculated correctly.

Lastly, failing to read the instructions carefully can lead to multiple mistakes. Each section of the IFTA 101Mn form has specific requirements. Not adhering to the instructions can result in missing important details that will ultimately hinder your tax filing process.

By being aware of these mistakes and taking the necessary precautions, individuals can simplify the completion of the IFTA 101Mn form and ensure compliance with tax regulations.

When filing your IFTA (International Fuel Tax Agreement) paperwork, it is essential to include several other forms and documents that complement the IFTA 101-MN form. Each of these is designed to help ensure accurate reporting and compliance, while also providing clarity in your fuel tax obligations. Below is a list of commonly required documents.

In conclusion, understanding and carefully preparing the necessary forms and documents are critical steps in complying with IFTA requirements. By ensuring that all associated paperwork is thorough and accurate, you can streamline your reporting process and minimize the risk of complications in the future.

The IFTA 101Mn form is one of several documents related to the reporting of fuel use for tax purposes. Below is a list of ten other forms that share similarities with the IFTA 101Mn form, along with explanations of these similarities:

Things you should do when filling out the IFTA 101Mn form:

Things you shouldn't do when filling out the IFTA 101Mn form:

When it comes to the IFTA 101MN form, many people have misunderstandings that can lead to errors in filing. Here are nine common misconceptions along with clarifications to help ensure that you complete the form accurately.

Being well-informed about the IFTA 101MN form can significantly streamline your filing process. Taking the time to understand these misconceptions will not only ease your burden but also help you avoid potential pitfalls associated with improper filings.

Understanding the IFTA 101Mn form is crucial for accurate fuel tax reporting. Here are ten key takeaways.

Following these takeaways can help streamline your IFTA reporting process and keep you compliant with tax laws. Stay organized and proactive.