When entering into a loan agreement in Illinois, it’s essential to have a clear and comprehensive understanding of the terms involved. This agreement serves as a legally binding document between the lender and borrower, outlining the specifics of the loan, including the principal amount, interest rate, repayment schedule, and any applicable fees. It also addresses important aspects such as default conditions, collateral requirements, and the rights and responsibilities of both parties. By clearly defining these elements, the Illinois Loan Agreement form helps protect the interests of both the lender and borrower, ensuring that everyone is on the same page. Whether you’re borrowing money for personal use, business expansion, or any other purpose, having a well-structured loan agreement can provide peace of mind and clarity throughout the lending process.

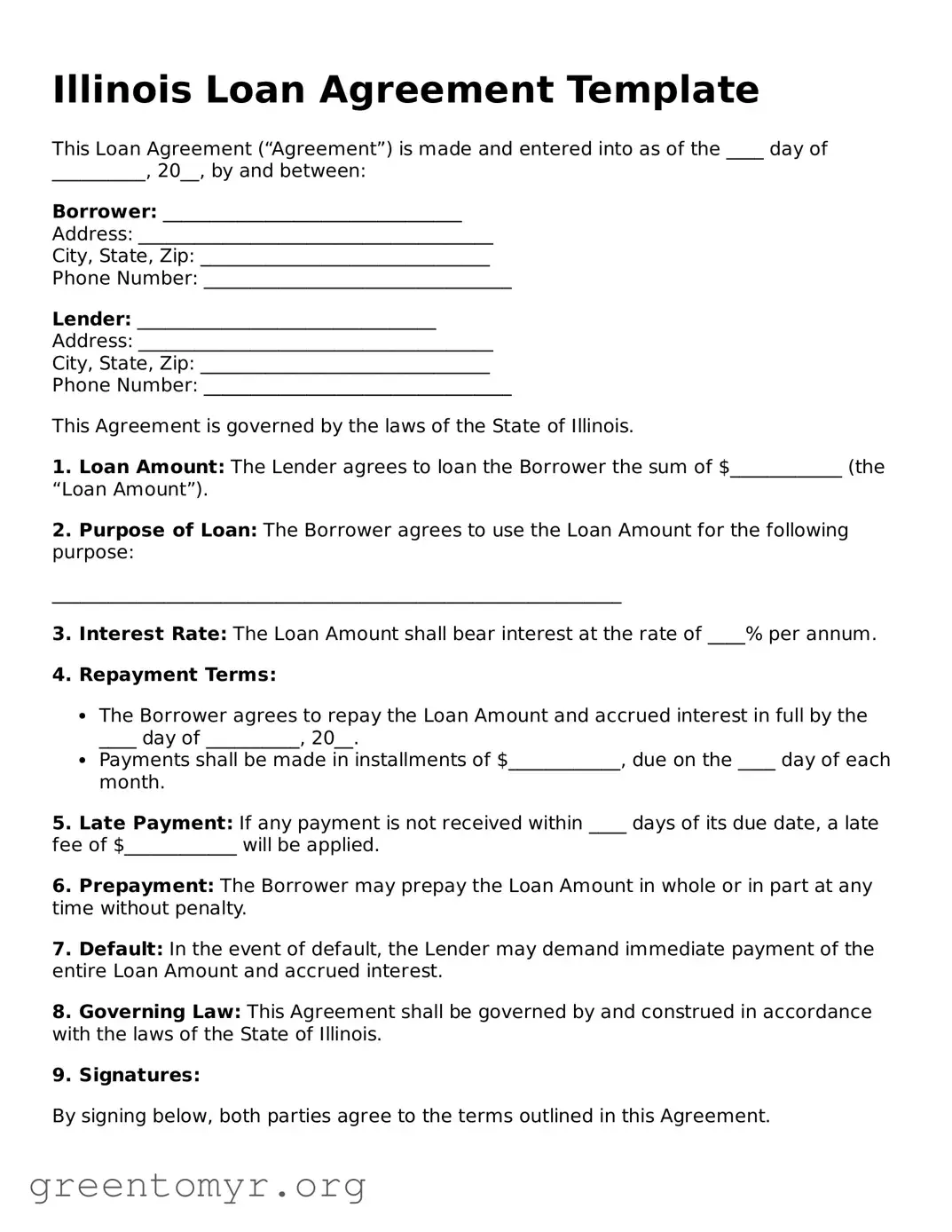

Illinois Loan Agreement Template

This Loan Agreement (“Agreement”) is made and entered into as of the ____ day of __________, 20__, by and between:

Borrower: ________________________________

Address: ______________________________________

City, State, Zip: _______________________________

Phone Number: _________________________________

Lender: ________________________________

Address: ______________________________________

City, State, Zip: _______________________________

Phone Number: _________________________________

This Agreement is governed by the laws of the State of Illinois.

1. Loan Amount: The Lender agrees to loan the Borrower the sum of $____________ (the “Loan Amount”).

2. Purpose of Loan: The Borrower agrees to use the Loan Amount for the following purpose:

_____________________________________________________________

3. Interest Rate: The Loan Amount shall bear interest at the rate of ____% per annum.

4. Repayment Terms:

5. Late Payment: If any payment is not received within ____ days of its due date, a late fee of $____________ will be applied.

6. Prepayment: The Borrower may prepay the Loan Amount in whole or in part at any time without penalty.

7. Default: In the event of default, the Lender may demand immediate payment of the entire Loan Amount and accrued interest.

8. Governing Law: This Agreement shall be governed by and construed in accordance with the laws of the State of Illinois.

9. Signatures:

By signing below, both parties agree to the terms outlined in this Agreement.

Borrower Signature: ________________________________

Date: ________________________________

Lender Signature: ________________________________

Date: ________________________________

| Fact Name | Description |

|---|---|

| Governing Law | The Illinois Loan Agreement is governed by the laws of the State of Illinois. |

| Parties Involved | The agreement typically involves a lender and a borrower. |

| Loan Amount | The form specifies the total amount of money being loaned. |

| Interest Rate | The agreement outlines the interest rate applicable to the loan. |

| Repayment Terms | It details the schedule and terms for repayment of the loan. |

| Default Provisions | The form includes conditions under which the borrower may default on the loan. |

Completing the Illinois Loan Agreement form requires careful attention to detail. Each section must be filled out accurately to ensure the agreement is valid and enforceable. Below are the steps to guide you through the process.

The Illinois Loan Agreement form is a legal document that outlines the terms and conditions of a loan between a lender and a borrower. This form specifies the amount borrowed, the interest rate, repayment schedule, and any collateral involved. It serves to protect both parties by clearly defining their rights and obligations.

This form is suitable for individuals or businesses looking to formalize a loan arrangement in Illinois. Whether you are lending money to a friend, family member, or a business partner, using this agreement can help prevent misunderstandings and disputes in the future. It is advisable for both parties to sign the agreement to ensure clarity and enforceability.

A comprehensive Illinois Loan Agreement should include the following key elements:

While it is not legally required to notarize a loan agreement in Illinois, doing so can add an extra layer of protection. A notary public verifies the identities of the parties involved and confirms that they are signing the document willingly. This can be particularly useful in case of disputes, as a notarized document is often considered more credible in court.

If the borrower fails to make payments as agreed, the lender has several options. They may choose to contact the borrower to discuss the situation and potentially renegotiate terms. If necessary, the lender can pursue legal action to recover the owed amount, especially if the loan is secured by collateral. The specifics will depend on the terms outlined in the loan agreement.

Yes, the terms of the loan agreement can be modified, but both parties must agree to any changes. It’s essential to document these modifications in writing and have both parties sign the updated agreement. This ensures that everyone is on the same page and helps prevent future disputes.

You can find an Illinois Loan Agreement form through various sources, including online legal document services, local law libraries, or by consulting with a legal professional. Ensure that the form you choose is up-to-date and complies with Illinois state laws to ensure its validity.

Filling out the Illinois Loan Agreement form can seem straightforward, but many people make common mistakes that can lead to confusion or even legal issues. One frequent error is the omission of essential personal information. Borrowers often forget to include their full name, address, or contact details. This information is crucial for identifying the parties involved and ensuring that the agreement is legally binding.

Another mistake involves the incorrect listing of loan amounts. Some individuals may miscalculate the total amount they intend to borrow or fail to specify whether the amount is in dollars or another currency. This can lead to misunderstandings between the lender and borrower regarding the terms of the loan.

Additionally, many people neglect to read the terms and conditions thoroughly. Skimming through the fine print can result in overlooking important clauses related to interest rates, repayment schedules, or penalties for late payments. Understanding these terms is vital for both parties to avoid disputes in the future.

Another common issue is failing to sign and date the agreement properly. Some individuals may forget to sign the document entirely or may not date it correctly. Without proper signatures and dates, the agreement may not hold up in court, leaving both parties vulnerable.

Lastly, individuals often do not keep a copy of the signed agreement for their records. After completing the form, it is essential to retain a copy for future reference. This helps both parties remember the terms of the agreement and serves as evidence if any disputes arise.

When entering into a loan agreement in Illinois, several additional documents may be necessary to ensure clarity and protection for both parties involved. These documents can help outline the terms of the loan, provide security for the lender, and facilitate a smooth transaction. Below is a list of forms commonly used alongside the Illinois Loan Agreement.

Utilizing these forms in conjunction with the Illinois Loan Agreement can help protect both lenders and borrowers. Clear documentation fosters trust and understanding throughout the lending process.

Promissory Note: This document outlines the borrower's promise to repay a loan, detailing the amount borrowed, interest rate, and repayment terms. Like a loan agreement, it formalizes the borrowing relationship.

Mortgage Agreement: A mortgage agreement secures a loan with property as collateral. Similar to a loan agreement, it specifies terms and conditions, but it also includes the property details being used as security.

Security Agreement: This document establishes collateral for a loan, ensuring that the lender has rights to specific assets if the borrower defaults. It shares the purpose of protecting the lender, much like a loan agreement.

Lease Agreement: A lease agreement outlines the terms under which one party rents property from another. It shares similarities with a loan agreement in that both involve obligations and rights over a specified duration.

Credit Agreement: This document details the terms under which a lender extends credit to a borrower. It is similar to a loan agreement as it defines the borrower's obligations and the lender's rights.

Debt Settlement Agreement: This agreement outlines the terms under which a borrower settles a debt for less than the full amount owed. Like a loan agreement, it establishes terms, but it focuses on resolving existing debt rather than creating new obligations.

Partnership Agreement: In a partnership agreement, terms of collaboration and financial contributions among partners are detailed. It mirrors a loan agreement in that it sets forth obligations and expectations among parties.

Business Loan Agreement: This is a specific type of loan agreement tailored for business purposes. It includes terms related to business operations and financial projections, similar to standard loan agreements.

Personal Loan Agreement: This document outlines the terms for loans made between individuals, often involving family or friends. It serves a similar purpose to a loan agreement, emphasizing repayment terms and conditions.

Installment Agreement: An installment agreement allows a borrower to repay a debt in scheduled payments over time. Like a loan agreement, it specifies repayment terms, but it often pertains to tax debts or other obligations.

When filling out the Illinois Loan Agreement form, attention to detail is crucial. Here are five important actions to take and avoid:

When it comes to the Illinois Loan Agreement form, many people hold misconceptions that can lead to confusion or misinformed decisions. Understanding the truth behind these beliefs is crucial for anyone entering into a loan agreement. Below are seven common misconceptions along with clarifications to help you navigate this important document.

By understanding these misconceptions, you can approach the Illinois Loan Agreement form with greater confidence and clarity. Always take the time to review any loan agreement thoroughly and seek clarification on any points that seem unclear.

When filling out and using the Illinois Loan Agreement form, it is essential to keep several key points in mind:

By following these key takeaways, parties can navigate the Illinois Loan Agreement form more effectively and ensure a smoother lending process.