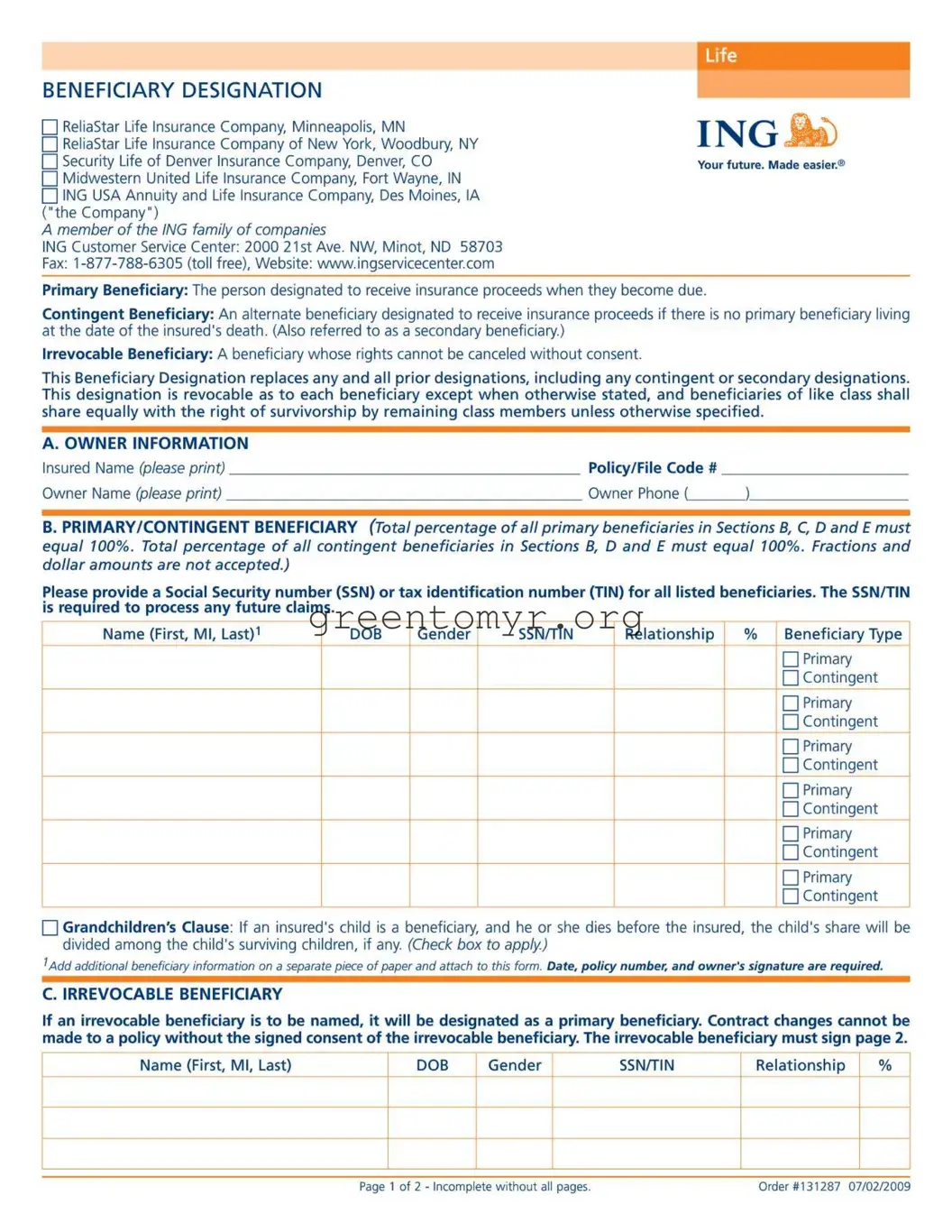

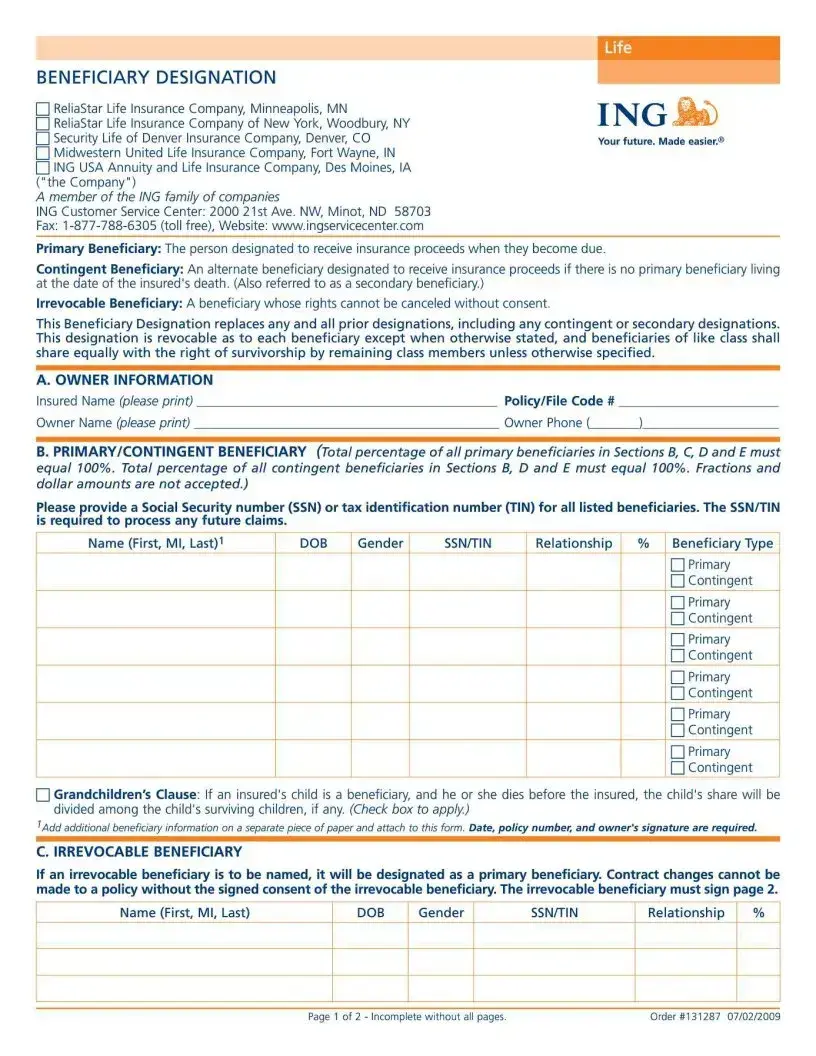

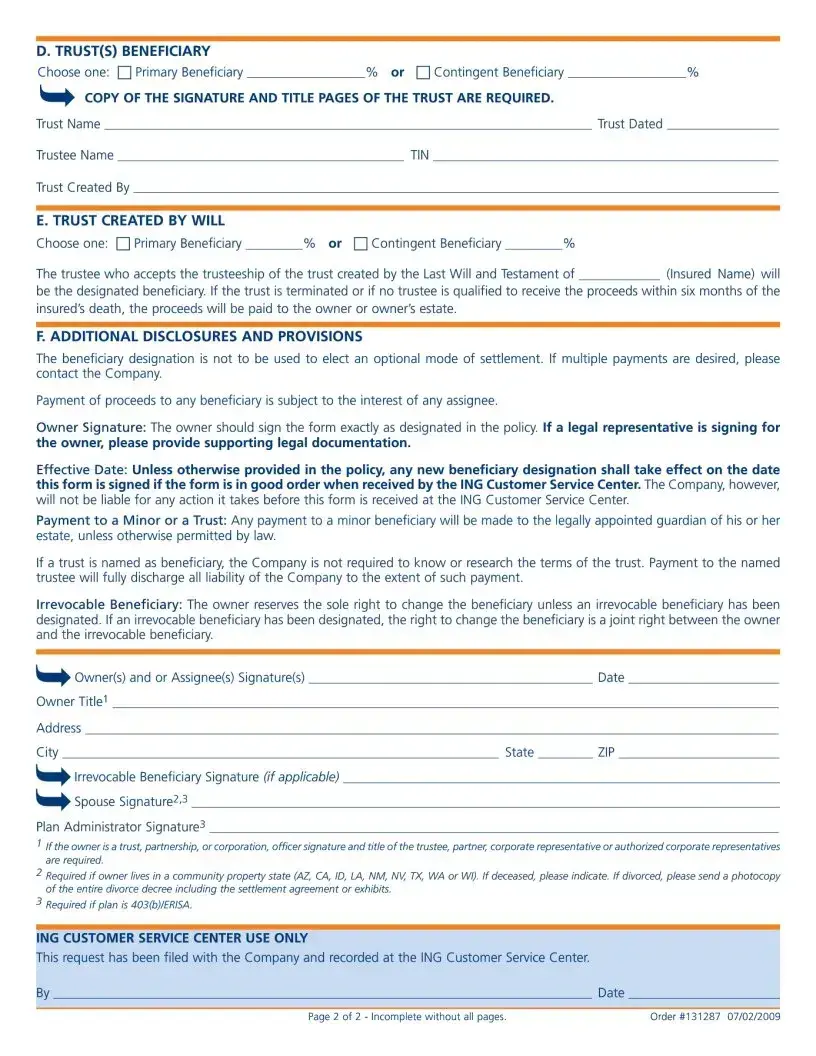

The ING Beneficiary form plays a crucial role in the management of life insurance policies and annuities, ensuring that the right individuals or entities receive benefits in case of the policyholder's passing. This form allows individuals to designate primary beneficiaries who are first in line to receive insurance proceeds, as well as contingent beneficiaries who will receive funds if the primary beneficiary is no longer living. It's essential for policy owners to understand the different types of beneficiaries: a primary beneficiary is the main recipient, while an irrevocable beneficiary cannot be changed without their consent. The form also provides space for listing trust beneficiaries, where specific legal documents related to the trust must be included. Completing the ING Beneficiary form accurately is vital, as it replaces any prior beneficiary designations and must ensure that the total percentage for all listed beneficiaries equals 100%. Additionally, the form incorporates necessary disclosures about payment procedures and obligations regarding minors or trusts. Proper completion and signatures, including potential signatures from spouses or trustees, are required to facilitate a smooth claims process in the future.

| Fact Name | Details |

|---|---|

| Primary Beneficiary | The individual designated to receive the insurance proceeds upon the insured's death. |

| Contingent Beneficiary | This is the alternate beneficiary who receives the proceeds if there is no primary beneficiary available. |

| Irrevocable Beneficiary | A beneficiary whose rights cannot be altered without their consent, ensuring protection for their interests. |

| Beneficiary Designation Replacement | This form replaces all prior beneficiary designations, making it crucial to complete it accurately. |

| Distribution among Beneficiaries | The total percentage for primary beneficiaries must equal 100%, as must the total for contingent beneficiaries. |

| Grandchildren's Clause | If a deceased child's share should be passed to their surviving children, a check box needs to be selected. |

| Effective Date | The new beneficiary designation takes effect on the date the form is signed, as long as it is properly completed. |

| Legal Documentation | If a legal representative is signing on behalf of the owner, appropriate legal documentation must accompany the form. |

Completing the ING Beneficiary form is crucial for ensuring that your insurance proceeds are distributed according to your wishes. Follow these steps carefully to fill out the form correctly. Make sure to provide all required information and double-check for accuracy before submitting it.

The ING Beneficiary form is used to designate individuals or entities to receive the insurance proceeds after the death of the insured person. It outlines who the primary and contingent beneficiaries are, allowing the insured owner to specify how the benefits will be distributed. This form helps ensure that the wishes of the owner are carried out regarding who benefits from the policy.

Beneficiaries can include individuals, such as family members or friends, as well as entities like trusts or charities. The owner of the policy has the flexibility to choose anyone they wish, as long as the designated beneficiaries are living at the time of the insured’s death for primary beneficiaries. Contingent beneficiaries can be named as alternates if the primary ones are not living.

An irrevocable beneficiary is someone whose rights to the insurance benefits cannot be changed without their consent. When a beneficiary is designated as irrevocable, the owner of the policy must seek permission from that beneficiary to make any changes to the designation. This arrangement can provide a certain level of security for the named beneficiary.

When filling out the form, the total percentage assigned to all primary beneficiaries must equal 100%. Similarly, contingent beneficiaries should also total 100%. For example, if you have two primary beneficiaries, you might designate one to receive 60% and the other to receive 40%. It’s important to make sure the percentages accurately reflect your intentions for distribution.

If a primary beneficiary dies before the insured, the benefits may be passed on to the contingent beneficiary, provided one has been named. Additionally, if there’s a grandchildren's clause indicated on the form, the deceased beneficiary's share may be distributed among their surviving children.

If you have questions or need help completing the ING Beneficiary form, you can contact the ING Customer Service Center. They can provide guidance on filling out the form and ensure that all necessary information is included. You can reach them at their address or through their website for further assistance.

Completing the ING Beneficiary form can be straightforward, but there are common mistakes that may lead to delays or complications in processing. Understanding these errors is crucial for ensuring that the beneficiary designations are correctly established.

One common mistake is failing to provide complete information for each beneficiary. Every beneficiary should have their name, date of birth, gender, Social Security number, and relationship to the insured clearly filled out. Incomplete information can lead to processing delays or the rejection of the form.

Another frequent error involves not assigning the correct percentages to primary and contingent beneficiaries. The total percentage for primary beneficiaries must equal 100%, and the same applies to contingent beneficiaries. Neglecting to ensure these totals can create complications in the distribution of proceeds after the insured's death.

People often overlook the requirement for Social Security numbers (SSNs) or tax identification numbers (TINs) for all listed beneficiaries. The form cannot be processed without this critical information, which is necessary for processing any future claims.

Not checking the Grandchildren's Clause box can also be a mistake. If an insured’s child dies before them, failing to check this option may prevent the deceased child's share from being automatically distributed to their surviving children.

Another issue arises when an irrevocable beneficiary is named. If an irrevocable beneficiary is to be included, they must be designated as a primary beneficiary, and their consent is required for any changes to the policy. Failing to understand this can lead to unexpected complications.

People frequently forget or neglect to sign the form. The owner must sign exactly as designated in the policy. If there is a legal representative, supporting legal documentation should accompany the signature to avoid any ambiguity.

Failure to attach additional beneficiary information on a separate piece of paper can also cause issues. If there are more beneficiaries than can be listed on the form, this additional information is necessary and must include the policy number and owner's signature for accuracy.

Lastly, not recognizing the provisions for payments to minors or trusts can create serious issues. Payments to minors should be directed to a legally appointed guardian unless stated otherwise. If a trust is named, the company is not required to research its terms, so clarity in naming the trustee is essential.

The ING Beneficiary form serves a crucial purpose in estate planning, ensuring that insurance proceeds go to the intended individuals or entities. Alongside this form, several other documents are frequently utilized to clarify intentions and streamline beneficiary designations. Below is a list of these related forms and documents, each with a brief description.

These documents play a vital role in ensuring that beneficiary designations are accurate, clear, and legally sound. When used in conjunction with the ING Beneficiary form, they help provide peace of mind and clarity regarding financial matters for individuals and their families.

Insurance Policy Beneficiary Form: Similar to the ING Beneficiary form, this document designates individuals who will receive the benefits of an insurance policy after the insured passes away. It typically includes sections for primary and contingent beneficiaries, as well as any necessary identification information.

Retirement Account Beneficiary Designation: This form identifies the person or entity that will inherit funds from a retirement account, like an IRA or 401(k). Much like the ING Beneficiary form, it allows for the designation of primary and contingent beneficiaries and often requires Social Security numbers.

Will: While not inherently a beneficiary designation form, a will outlines who will receive assets upon an individual's death. This document works in tandem with beneficiary forms, particularly when outlining who will inherit in the absence of living beneficiaries.

Revocable Trust Document: Similar to the ING form, this legal document designates beneficiaries who will receive assets held in the trust upon the grantor's death. It provides clarity around the distribution of assets and can replace the need for a will if properly funded.

Healthcare Proxy: This document allows an individual to designate a person to make medical decisions on their behalf if they become incapacitated. While different in function, it manages the assignment of responsibility similar to beneficiary designations.

Payable on Death (POD) Agreement: This agreement allows individuals to designate beneficiaries for bank accounts and financial assets. Similar to the ING Beneficiary form, a POD ensures that funds transfer directly to the specified beneficiaries upon the account holder's death.

Power of Attorney: This document grants someone the authority to make financial or legal decisions for another individual. It shares the fundamental purpose of designating decision-makers, akin to how beneficiaries are appointed in insurance forms.

Filling out the ING Beneficiary form is an important task and should be done with care. Here are some guidelines to help ensure you complete it correctly.

By following these simple instructions, you can ensure that the form is filled out correctly and that your intentions regarding your beneficiaries are clearly stated.

Misconception 1: The Beneficiary Designation is Unchangeable

Many people believe that once a beneficiary is named on the form, that designation is permanent. In reality, the owner of the policy retains the right to change the beneficiary at any time, unless an irrevocable beneficiary has been specified. If an irrevocable beneficiary is designated, the owner can only make changes with the consent of that beneficiary.

Misconception 2: A Primary Beneficiary is the Same as a Contingent Beneficiary

Some may think that a primary beneficiary and a contingent beneficiary serve the same function. In fact, a primary beneficiary is entitled to receive the benefits upon the insured's death, while a contingent beneficiary steps in only if the primary beneficiary is not alive at that time. This distinction is critical for ensuring that benefits are distributed as intended.

Misconception 3: An Irrevocable Beneficiary Equals a Permanent Beneficiary

While it may sound similar, an irrevocable beneficiary is not a permanent beneficiary in the sense that they cannot ever be changed. Instead, the designation requires consent from that beneficiary to make any future changes. This can lead to confusion over the nature of the designation and the rights it confers.

Misconception 4: A Trust as a Beneficiary Never Requires Documentation

Some individuals believe that naming a trust as a beneficiary is straightforward and does not require additional paperwork. However, a copy of the signature and title pages of the trust must be provided to confirm its validity. Without this documentation, the insurance company may not recognize the trust as a legitimate beneficiary.

Here are some important points to consider when filling out and using the ING Beneficiary form: