The IRS 1041 form, officially known as the "U.S. Income Tax Return for Estates and Trusts," plays a critical role in the tax process for fiduciaries managing estates or trusts. It facilitates the reporting of income, deductions, gains, and losses incurred during the tax year within these entities. This form is particularly important for estates and trusts with gross income of $600 or more or any estate that has a decedent who was a non-resident alien. By filing the 1041, fiduciaries must disclose the specific financial activities of the estate or trust, ensuring accurate tax calculations and compliance with federal tax regulations. Moreover, it’s necessary to provide beneficiaries with Schedule K-1 forms that detail each beneficiary's share of the income or deductions. Completing the form requires careful attention to diverse sources of income such as interest, dividends, and rental income. Understanding the nuances of the 1041 is paramount for effective estate management and proper tax filing, allowing fiduciaries to uphold their responsibilities while adhering to the IRS guidelines.

Note: The form, instructions, or publication you are looking

for begins after this coversheet.

Please review the updated information below.

Reporting Excess Deductions on Termination of an Estate or Trust on Forms 1040,

Under Proposed Regulations

For tax year 2019, an excess deduction for IRC section 67(e) expenses is reported as a

For tax year 2018, an excess deduction for IRC section 67(e) expenses is reported as a

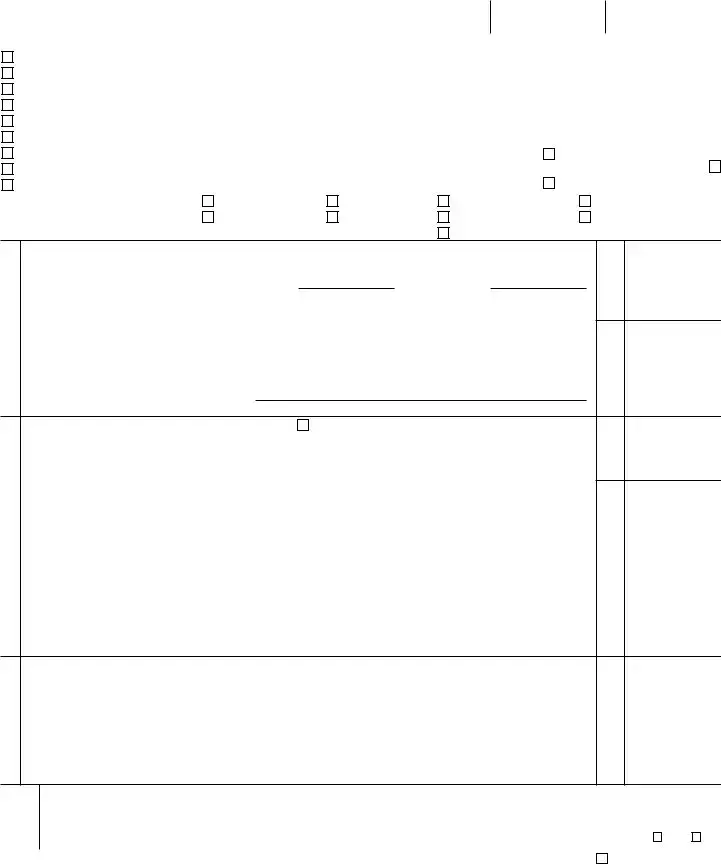

Form

1041 |

Department of the |

U.S. Income Tax Return for Estates and Trusts |

|

Go to www.irs.gov/Form1041 for instructions and the latest information. |

2019

OMB No.

A Check all that apply: |

For calendar year 2019 or fiscal year beginning |

, 2019, and ending |

, 20 |

||||

Decedent’s estate |

Name of estate or trust (If a grantor type trust, see the instructions.) |

|

C |

Employer identification number |

|||

Simple trust |

|

|

|

|

|

|

|

Complex trust |

Name and title of fiduciary |

|

|

D |

Date entity created |

||

Qualified disability trust |

|

|

|

|

|

|

|

ESBT (S portion only) |

Number, street, and room or suite no. (If a P.O. box, see the instructions.) |

|

E Nonexempt charitable and |

||||

Grantor type trust |

|

|

|

|

|

trusts, check applicable box(es). |

|

|

|

|

|

|

See instructions. |

||

Bankruptcy |

|

|

|

|

|

Described in sec. 4947(a)(1). Check here |

|

Bankruptcy |

City or town, state or province, country, and ZIP or foreign postal code |

|

|

if not a private foundation . . |

|||

Pooled income fund |

|

|

|

|

|

Described in sec. 4947(a)(2) |

|

B Number of Schedules |

F Check |

Initial return |

Final return |

Amended return |

|

Net operating loss carryback |

|

attached (see |

applicable |

Change in trust’s name |

Change in fiduciary |

Change in fiduciary’s name |

Change in fiduciary’s address |

||

instructions) |

boxes: |

||||||

G Check here if the estate or filing trust made a section 645 election |

Trust TIN |

|

|

||||

Income

Deductions

Tax and Payments

1 |

Interest income |

1 |

|

|

2a |

Total ordinary dividends |

2a |

||

b |

Qualified dividends allocable to: (1) Beneficiaries |

(2) Estate or trust |

|

|

3 |

Business income or (loss). Attach Schedule C (Form 1040 or |

3 |

|

|

4 |

Capital gain or (loss). Attach Schedule D (Form 1041) |

4 |

|

|

5Rents, royalties, partnerships, other estates and trusts, etc. Attach Schedule E (Form 1040 or

|

5 |

||

6 |

Farm income or (loss). Attach Schedule F (Form 1040 or |

6 |

|

7 |

Ordinary gain or (loss). Attach Form 4797 |

7 |

|

8 |

Other income. List type and amount |

|

8 |

9 |

Total income. Combine lines 1, 2a, and 3 through 8 |

9 |

|

10 |

Interest. Check if Form 4952 is attached |

. . . . . . . . . . . . . . . . . |

10 |

11 |

Taxes |

11 |

|

12 |

Fiduciary fees. If only a portion is deductible under section 67(e), see instructions |

12 |

|

13 |

Charitable deduction (from Schedule A, line 7) |

13 |

|

14Attorney, accountant, and return preparer fees. If only a portion is deductible under section 67(e),

|

see instructions |

14 |

|

||||

15a |

Other deductions (attach schedule). See instructions for deductions allowable under section 67(e) |

15a |

|||||

b |

Net operating loss deduction. See instructions |

15b |

|||||

16 |

Add lines 10 through 15b |

16 |

|

||||

17 |

Adjusted total income or (loss). Subtract line 16 from line 9 |

. . |

. . . |

17 |

|

|

|

18 |

Income distribution deduction (from Schedule B, line 15). Attach Schedules |

18 |

|

||||

19 |

Estate tax deduction including certain |

19 |

|

||||

20 |

Qualified business income deduction. Attach Form 8995 or |

20 |

|

||||

21 |

Exemption |

21 |

|

||||

22 |

Add lines 18 through 21 |

22 |

|

||||

23 |

Taxable income. Subtract line 22 from line 17. If a loss, see instructions |

23 |

|

||||

24 |

Total tax (from Schedule G, Part I, line 9) |

24 |

|

||||

25 |

2019 net 965 tax liability paid from Form |

25 |

|

||||

26 |

Total payments (from Schedule G, Part II, line 17) |

26 |

|

||||

27 |

Estimated tax penalty. See instructions |

27 |

|

||||

28 |

Tax due. If line 26 is smaller than the total of lines 24, 25, and 27, enter amount owed . . . . |

28 |

|

||||

29 |

Overpayment. If line 26 is larger than the total of lines 24, 25, and 27, enter amount overpaid . . |

29 |

|

||||

30 |

Amount of line 29 to be: a Credited to 2020 |

; |

b Refunded |

30 |

|

||

Sign Here

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

F |

|

|

|

|

May the IRS discuss this return |

||

|

|

|

|||||

|

|

|

|

with the preparer shown below? |

|||

Signature of fiduciary or officer representing fiduciary |

Date |

EIN of fiduciary if a financial institution |

|

See Instr. |

Yes |

No |

|

Paid |

Print/Type preparer’s name |

Preparer’s signature |

|

Date |

|

Check |

if |

PTIN |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|||

Preparer |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

Firm’s name |

|

|

|

Firm’s EIN |

|

|

|

||

Use Only |

|

|

|

|

|

|

|||

Firm’s address |

|

|

|

Phone no. |

|

|

|

||

|

|

|

|

|

|

|

|||

For Paperwork Reduction Act Notice, see the separate instructions. |

Cat. No. 11370H |

|

|

|

Form 1041 (2019) |

|

|||

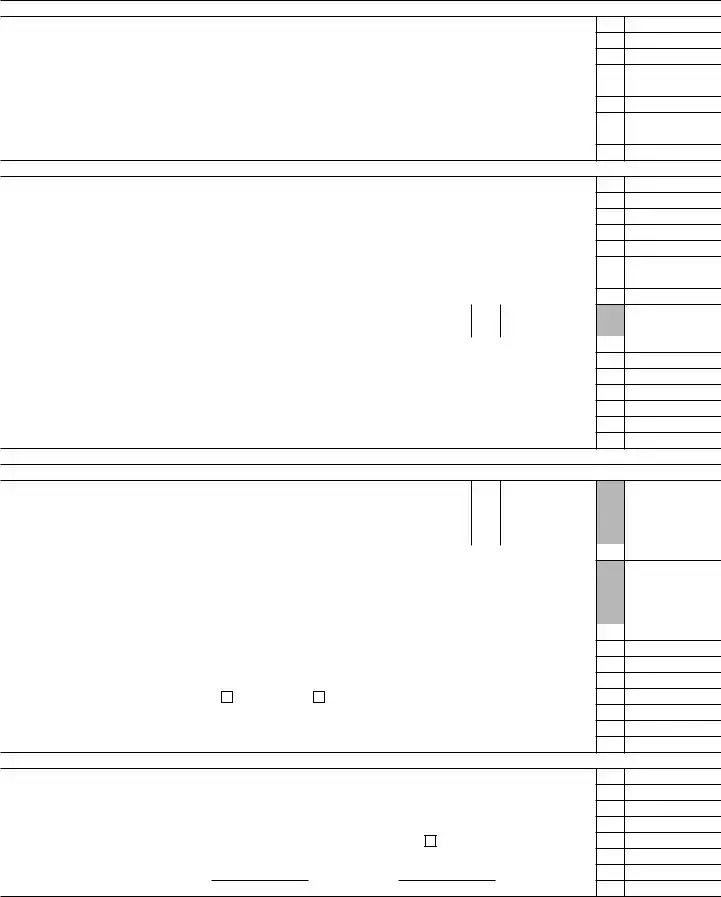

Form 1041 (2019) |

Page 2 |

Schedule A Charitable Deduction. Don’t complete for a simple trust or a pooled income fund.

1Amounts paid or permanently set aside for charitable purposes from gross income. See instructions

2 |

|

3 |

Subtract line 2 from line 1 |

4Capital gains for the tax year allocated to corpus and paid or permanently set aside for charitable

purposes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

5 Add lines 3 and 4 . . . . . . . . . . . . . . . . . . . . . . . . . . . .

6Section 1202 exclusion allocable to capital gains paid or permanently set aside for charitable purposes. See instructions . . . . . . . . . . . . . . . . . . . . . . . . .

7 Charitable deduction. Subtract line 6 from line 5. Enter here and on page 1, line 13 . . . . . .

1

2

3

4

5

6

7

Schedule B Income Distribution Deduction

1 |

Adjusted total income. See instructions |

2 |

Adjusted |

3 |

Total net gain from Schedule D (Form 1041), line 19, column (1). See instructions |

4 |

Enter amount from Schedule A, line 4 (minus any allocable section 1202 exclusion) |

5 |

Capital gains for the tax year included on Schedule A, line 1. See instructions |

6Enter any gain from page 1, line 4, as a negative number. If page 1, line 4, is a loss, enter the loss as a

positive number . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

7 Distributable net income. Combine lines 1 through 6. If zero or less, enter

8If a complex trust, enter accounting income for the tax year as determined

|

under the governing instrument and applicable local law |

8 |

9 |

Income required to be distributed currently |

|

10 |

Other amounts paid, credited, or otherwise required to be distributed |

|

11 |

Total distributions. Add lines 9 and 10. If greater than line 8, see instructions |

|

12 |

Enter the amount of |

|

13 |

Tentative income distribution deduction. Subtract line 12 from line 11 |

|

14 |

Tentative income distribution deduction. Subtract line 2 from line 7. If zero or less, enter |

|

15 |

Income distribution deduction. Enter the smaller of line 13 or line 14 here and on page 1, line 18 . |

|

1

2

3

4

5

6

7

9

10

11

12

13

14

15

Schedule G Tax Computation and Payments (see instructions)

Part I — Tax Computation

1Tax:

a |

Tax on taxable income. See instructions |

1a |

|||

b |

Tax on |

1b |

|||

c |

Alternative minimum tax (from Schedule I (Form 1041), line 54) |

1c |

|||

d |

Total. Add lines 1a through 1c |

||||

2a |

Foreign tax credit. Attach Form 1116 |

2a |

|

||

b |

General business credit. Attach Form 3800 |

2b |

|

||

c |

Credit for prior year minimum tax. Attach Form 8801 |

2c |

|

||

d |

Bond credits. Attach Form 8912 |

2d |

|

||

e |

Total credits. Add lines 2a through 2d |

||||

3 |

Subtract line 2e from line 1d. If zero or less, enter |

||||

4 |

Tax on the ESBT portion of the trust (from ESBT Tax Worksheet, line 17). See instructions . . . . |

||||

5 |

Net investment income tax from Form 8960, line 21 |

||||

6 |

Recapture taxes. Check if from: |

Form 4255 |

Form 8611 |

||

7 |

Household employment taxes. Attach Schedule H (Form 1040 or |

||||

8 |

Other taxes and amounts due |

||||

9 |

Total tax. Add lines 3 through 8. Enter here and on page 1, line 24 |

||||

1d

2e

3

4

5

6

7

8

9

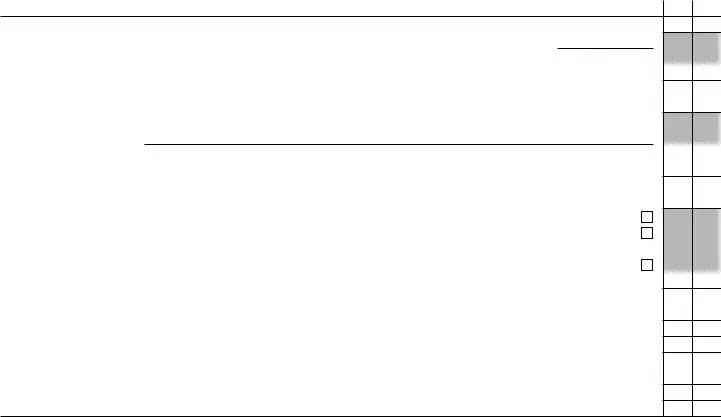

Part II — Payments

10 2019 estimated tax payments and amount applied from 2018 return . . . . . . . . . . .

11Estimated tax payments allocated to beneficiaries (from Form

12 |

Subtract line 11 from line 10 |

||

13 |

Tax paid with Form 7004. See instructions |

||

14 |

Federal income tax withheld. If any is from Form(s) 1099, check here |

. . . . . . . . . |

|

15 |

2019 net 965 tax liability from Form |

||

16 |

Other payments: a Form 2439 |

; b Form 4136 |

; Total . . |

17 |

Total payments. Add lines 12 through 15 and 16c. Enter here and on page 1, line 26 |

||

10

11

12

13

14

15

16c

17

Form 1041 (2019)

Form 1041 (2019) |

Page 3 |

Other Information |

Yes No |

1Did the estate or trust receive

Enter the amount of |

$ |

2Did the estate or trust receive all or any part of the earnings (salary, wages, and other compensation) of any

individual by reason of a contract assignment or similar arrangement? . . . . . . . . . . . . . . .

3At any time during calendar year 2019, did the estate or trust have an interest in or a signature or other authority over a bank, securities, or other financial account in a foreign country? . . . . . . . . . . . . . .

See the instructions for exceptions and filing requirements for FinCEN Form 114. If “Yes,” enter the name of the foreign country

4During the tax year, did the estate or trust receive a distribution from, or was it the grantor of, or transferor to, a

foreign trust? If “Yes,” the estate or trust may have to file Form 3520. See instructions . . . . . . . . .

5Did the estate or trust receive, or pay, any qualified residence interest on

the instructions for the required attachment . . . . . . . . . . . . . . . . . . . . . . .

6 If this is an estate or a complex trust making the section 663(b) election, check here. See instructions . .

7 To make a section 643(e)(3) election, attach Schedule D (Form 1041), and check here. See instructions . .

8If the decedent’s estate has been open for more than 2 years, attach an explanation for the delay in closing the

estate, and check here . . . . . . . . . . . . . . . . . . . . . . . . . . . .

9 Are any present or future trust beneficiaries skip persons? See instructions . . . . . . . . . . . . .

10Was the trust a specified domestic entity required to file Form 8938 for the tax year (see the Instructions for

Form 8938)? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

11a Did the estate or trust distribute S corporation stock for which it made a section 965(i) election? . . . . . .

bIf “Yes,” did each beneficiary enter into an agreement to be liable for the net tax liability? See instructions . . .

12Did the estate or trust make a section 965(i) election for S corporation stock held on the last day of the tax year?

See instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

13 ESBTs only. Does the ESBT have a nonresident alien grantor? If “Yes,” see instructions . . . . . . . .

14ESBTs only. Did the S portion of the trust claim a qualified business income deduction? If “Yes,” see instructions

Form 1041 (2019)

| Fact Name | Details |

|---|---|

| Purpose | The IRS Form 1041 is used to report income, deductions, gains, losses, and to calculate the tax for estates and trusts. |

| Filing Requirement | Form 1041 must be filed if the estate has a gross income of $600 or more during the tax year. |

| Due Date | The form is due on the 15th day of the fourth month following the close of the estate's tax year. |

| Beneficiaries' Income | Income distributed to beneficiaries is reported on Schedule K-1, which is part of Form 1041. |

| Tax Identification Number | Estates and trusts must obtain an Employer Identification Number (EIN) for filing Form 1041. |

| Form Complexity | The form can be complex, with numerous schedules for detailing income, deductions, and distributions. |

| State Filings | States may require their own forms for trusts and estates; for example, California requires Form 541, governed by California Revenue and Taxation Code. |

| Deductions | Common deductions include funeral expenses, legal fees, and administrative expenses associated with estate management. |

| Amendments | If a mistake is found on Form 1041, taxpayers can file an amended return using Form 1041-X. |

| Penalties | Failure to file Form 1041 on time may incur penalties, which can add frustration to an already difficult process. |

Completing the IRS Form 1041 is a critical task for fiduciaries managing estates and trusts. This process requires careful attention to detail to ensure compliance and proper reporting. Following these steps will guide you through filling out the form accurately.

After you have completed these steps, the next part involves reviewing your entries for any errors or omissions, gathering additional documentation as needed, and determining your submission method—whether you will file electronically or by mail. Being methodical now can save you complications later.

The IRS Form 1041 is a federal income tax return filed by estates and trusts in the United States. This form is used to report income, deductions, gains, losses, and other information relevant to the estate or trust. When an estate or trust generates income during its tax year, Form 1041 must be filed to provide the IRS with the necessary information on tax liability.

Not every estate or trust must file Form 1041. Generally, a fiduciary must file if the estate or trust has gross income of $600 or more for the tax year. Additionally, if the beneficiary of the estate or trust is a non-resident alien, a return must also be filed regardless of the income level. Special circumstances may apply, so consulting with a tax professional is advisable if there is uncertainty.

To effectively complete Form 1041, certain information is required, including:

Gathering these documents and details can help ensure accurate reporting.

Failing to file Form 1041 as required can lead to significant penalties. The IRS typically imposes a penalty for late filing, which can be a percentage of the unpaid tax amount. Additionally, failure to pay any taxes owed may result in further penalties and interest accrual. It is critical to address any outstanding tax returns promptly to mitigate these fines.

Yes, Form 1041 can be filed electronically through various tax software programs that are IRS-approved. Electronic filing can offer several benefits, including faster processing times and confirmation of submission. However, certain restrictions may apply depending on the specific circumstances of the estate or trust, so checking the IRS guidelines is recommended before proceeding.

Form 1041 is generally due on the 15th day of the fourth month following the end of the tax year. For estates, this means April 15 for a calendar year tax return. Trusts, depending on their tax year, may have different due dates. If the due date falls on a weekend or holiday, the deadline will typically extend to the next business day. Filing an extension is possible if additional time is required but should be done before the original due date.

Filling out the IRS 1041 form can be a complex task, and minor mistakes can lead to delays or issues with tax compliance. One common error is neglecting to include all necessary supporting documents. Individuals often forget to attach schedules or statements that provide crucial details about the estate or trust's income. This can result in the IRS requesting additional information, further complicating the process.

Another frequent mistake is incorrect identification of the filing status. Some people may not understand whether the form should be filed as an estate or a trust. Misclassifying the status can lead to incorrect tax calculations and penalties.

Many taxpayers also overlook the importance of accurately reporting income. All sources of income must be reported, including interest, dividends, and capital gains. Failing to report any income can trigger an audit or additional fines.

Additionally, some filers make the error of not properly identifying beneficiaries. When the beneficiaries’ names and addresses are incorrect or missing, it complicates the distribution process and can create issues for both the estate and the beneficiaries.

Another mistake people make involves the calculations themselves. Errors in math or miscalculating deductions can lead to an incorrect tax liability. It's crucial to double-check calculations to avoid surprises down the road.

Many also forget to sign and date the form before submission. An unsigned form is considered invalid and can lead to delays in processing. Remembering this simple step can save time and stress.

Neglecting to maintain accurate records is another significant pitfall. Filers need to keep thorough documentation of all transactions, income, and expenses. If the IRS questions any part of the return, having detailed records can make answering their inquiries much easier.

One mistake that can be particularly costly is ignoring the deadline. Each year, the IRS sets specific deadlines for filing the 1041 form. Missing this deadline can result in penalties and interest on unpaid taxes.

Finally, misunderstanding the estimated tax payment process leads some to underestimate their obligations. Trusts and estates may owe estimated taxes, and failing to make these payments can result in additional penalties.

Being aware of these common mistakes can help ensure a smoother process when filing the IRS 1041 form. Taking the time to review and ensure accuracy can alleviate many potential headaches.

The IRS Form 1041, also known as the U.S. Income Tax Return for Estates and Trusts, is a crucial document for managing the income tax obligations of estates and trusts. However, several other forms and documents are often used in conjunction with the 1041 to provide a complete overview of financial activities. Each document serves a specific purpose, helping to ensure compliance with tax laws and providing necessary information for accurate reporting.

Understanding these documents and their interconnections is vital for ensuring that both estates and trusts comply with tax regulations. Properly managing these forms can help prevent potential issues with the IRS and make the tax filing process smoother for all parties involved.

The IRS Form 1041 is a crucial document for estate and trust taxation. There are several other forms and documents that share similarities in purpose or procedure. Here is a list of those documents:

These documents contribute to a comprehensive framework for tax reporting related to different financial aspects, whether for individuals, estates, or organizations.

When filling out the IRS Form 1041, it's crucial to handle the process with care to ensure accuracy and compliance. Here are some essential dos and don'ts to guide you:

The IRS Form 1041, also known as the U.S. Income Tax Return for Estates and Trusts, often leads to confusion. Below are some common misconceptions about this form:

Understanding the IRS 1041 form is crucial for fiduciaries managing estates and trusts. Here are some key takeaways regarding its use and completion:

Completing the IRS 1041 form properly can help avoid penalties and ensure compliance with tax laws. It is advisable to consult with a tax professional for guidance tailored to specific situations.