The IRS 1065 form is a crucial document for partnerships operating in the United States. It serves as an informational return that reports the income, deductions, gains, and losses from the partnership's operations throughout the tax year. While this form does not require the partnership itself to pay taxes, it allows each partner to report their share of the profits and losses on their individual tax returns. The form must be filed annually, typically by March 15 for calendar year partnerships, and it includes details such as the partnership’s name, address, and tax identification number. Additionally, partnerships must provide information about each partner's capital contributions and their share of partnership profit or loss. It is essential for partnerships to accurately complete the 1065 form; doing so ensures compliance with tax laws and helps prevent potential penalties that may arise from incorrect filings. The accompanying Schedule K-1, provided to each partner, details their specific share of the partnership's income, allowing for transparent and precise reporting on personal tax returns.

Note: The form, instructions, or publication you are looking

for begins after this coversheet.

Please review the updated information below.

Form 1065 BBA Partnerships Filing Amended Returns for CARES Act

Relief

For tax years beginning in 2018 or 2019, BBA partnerships which filed Form 1065 and furnished all required Schedules

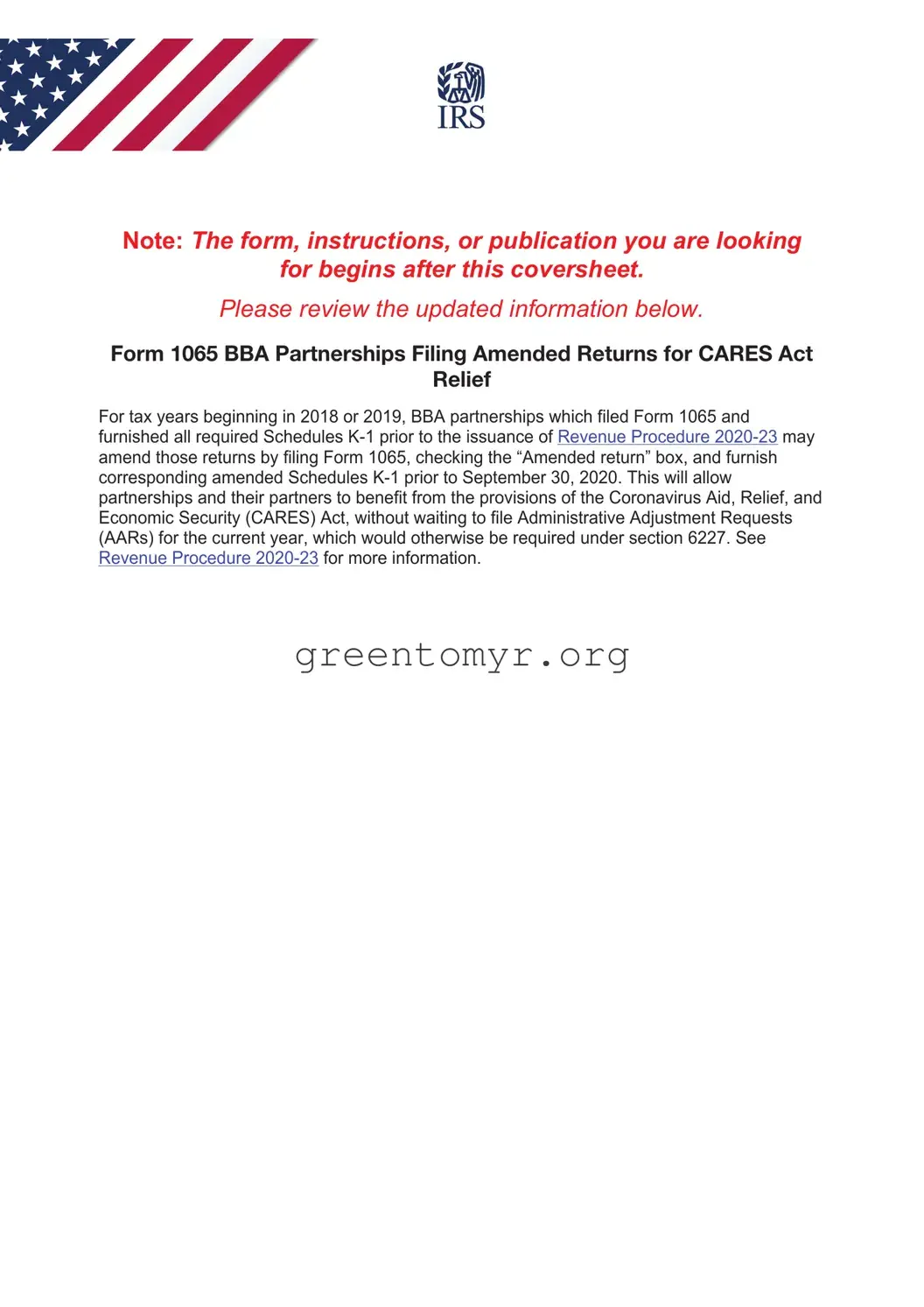

Form 1065

Department of the Treasury Internal Revenue Service

U.S. Return of Partnership Income

For calendar year 2019, or tax year beginning |

, 2019, ending |

, 20 |

. |

Go to www.irs.gov/Form1065 for instructions and the latest information.

OMB No.

2019

APrincipal business activity

BPrincipal product or service

CBusiness code number

Type

or

Name of partnership |

D Employer identification number |

|

|

Number, street, and room or suite no. If a P.O. box, see instructions. |

E Date business started |

|

|

City or town, state or province, country, and ZIP or foreign postal code |

F Total assets |

|

(see instructions) |

|

$ |

|

|

G |

Check applicable boxes: |

(1) |

Initial return |

(2) |

Final return |

(3) |

Name change (4) |

Address change (5) |

Amended return |

H |

Check accounting method: |

(1) |

Cash |

(2) |

Accrual |

(3) |

Other (specify) |

|

|

INumber of Schedules

J |

Check if Schedules C and |

||

K |

Check if partnership: (1) |

Aggregated activities for section 465 |

Grouped activities for section 469 passive activity purposes |

Caution: Include only trade or business income and expenses on lines 1a through 22 below. See instructions for more information.

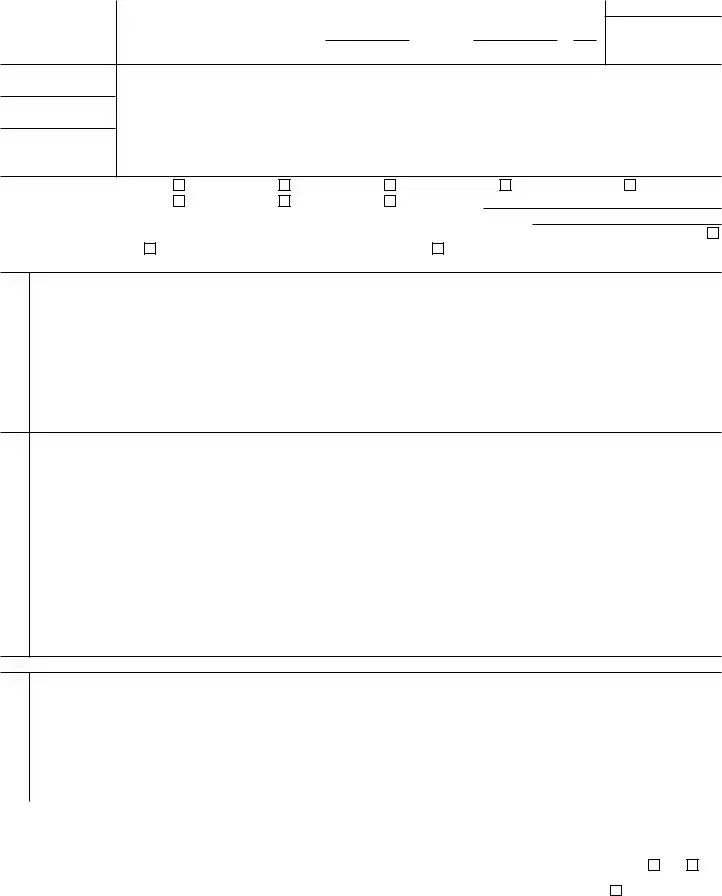

Income

Tax and Payment Deductions (see instructions for limitations)

1a |

Gross receipts or sales |

1a |

|

|

|

b |

Returns and allowances |

1b |

|

|

|

c |

Balance. Subtract line 1b from line 1a |

1c |

|

||

2 |

Cost of goods sold (attach Form |

2 |

|

||

3 |

Gross profit. Subtract line 2 from line 1c |

3 |

|

||

4 |

Ordinary income (loss) from other partnerships, estates, and trusts (attach statement) . . . . |

4 |

|

||

5 |

Net farm profit (loss) (attach Schedule F (Form 1040 or |

5 |

|

||

6 |

Net gain (loss) from Form 4797, Part II, line 17 (attach Form 4797) |

6 |

|

||

7 |

Other income (loss) (attach statement) |

7 |

|

||

8 |

Total income (loss). Combine lines 3 through 7 |

8 |

|

||

9 |

Salaries and wages (other than to partners) (less employment credits) |

9 |

|

||

10 |

Guaranteed payments to partners |

10 |

|

||

11 |

Repairs and maintenance |

11 |

|

||

12 |

Bad debts |

12 |

|

||

13 |

Rent |

13 |

|

||

14 |

Taxes and licenses |

14 |

|

||

15 |

Interest (see instructions) |

15 |

|

||

16a |

Depreciation (if required, attach Form 4562) |

16a |

|

|

|

b |

Less depreciation reported on Form |

16b |

|

16c |

|

17 |

Depletion (Do not deduct oil and gas depletion.) |

17 |

|

||

18 |

Retirement plans, etc |

18 |

|

||

19 |

Employee benefit programs |

19 |

|

||

20 |

Other deductions (attach statement) |

20 |

|

||

21 |

Total deductions. Add the amounts shown in the far right column for lines 9 through 20 . . . |

21 |

|

||

22 |

Ordinary business income (loss). Subtract line 21 from line 8 |

22 |

|

||

23 |

Interest due under the |

23 |

|

||

24 |

Interest due under the |

24 |

|

||

25 |

BBA AAR imputed underpayment (see instructions) |

25 |

|

||

26 |

Other taxes (see instructions) |

26 |

|

||

27 |

Total balance due. Add lines 23 through 26 |

27 |

|

||

28 |

Payment (see instructions) |

28 |

|

||

29 |

Amount owed. If line 28 is smaller than line 27, enter amount owed |

29 |

|

||

30 |

Overpayment. If line 28 is larger than line 27, enter overpayment |

30 |

|

||

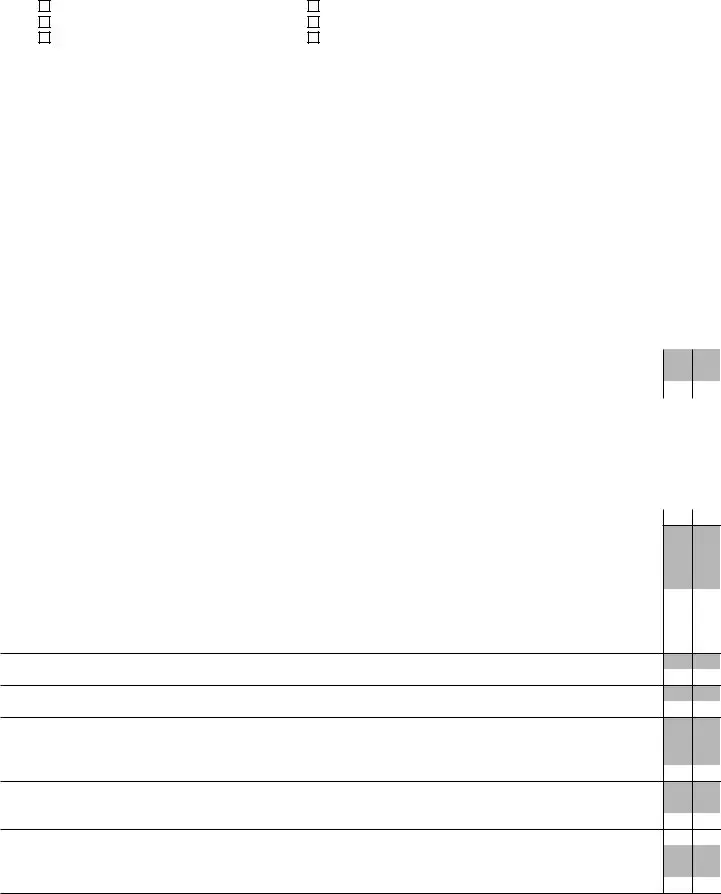

|

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge |

|||||||||||

Sign |

and belief, it is true, correct, and complete. Declaration of preparer (other than partner or limited liability company member) is based on all information of |

|||||||||||

which preparer has any knowledge. |

|

|

|

|

|

|

|

|

|

|

||

Here |

|

|

|

|

|

|

|

May the IRS discuss this return |

||||

|

|

|

|

|

|

|

with the preparer shown below? |

|||||

|

|

|

|

|

|

|

|

See instructions. |

Yes |

No |

||

|

F Signature of partner or limited liability company member |

F |

Date |

|

||||||||

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Paid |

Print/Type preparer’s name |

Preparer’s signature |

|

|

Date |

|

Check |

if |

|

PTIN |

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|||

Preparer |

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

Firm’s name |

|

|

|

|

Firm’s EIN |

|

|

|

|

|||

Use Only |

|

|

|

|

|

|

|

|

||||

Firm’s address |

|

|

|

|

Phone no. |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

||||

For Paperwork Reduction Act Notice, see separate instructions. |

|

Cat. No. 11390Z |

|

|

Form 1065 (2019) |

|||||||

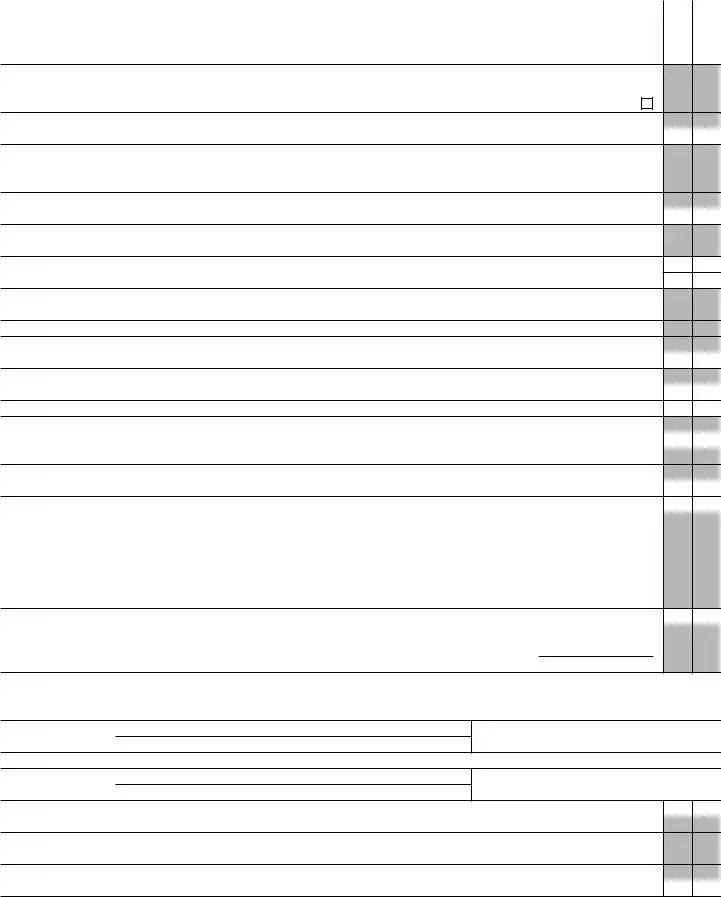

Form 1065 (2019) |

|

|

|

|

|

|

|

Page 2 |

|||

Schedule B |

Other Information |

|

|

|

|

|

|

|

|

|

|

1 What type of entity is filing this return? Check the applicable box: |

|

|

Yes |

No |

|||||||

a |

Domestic general partnership |

b |

Domestic limited partnership |

|

|

|

|

|

|||

c |

Domestic limited liability company |

d |

Domestic limited liability partnership |

|

|

|

|

||||

e |

Foreign partnership |

f |

Other |

|

|

|

|

|

|||

2 At the end of the tax year: |

|

|

|

|

|

|

|

|

|

||

a Did any foreign or domestic corporation, partnership (including any entity treated as a partnership), trust, or tax- |

|

|

|

||||||||

|

exempt organization, or any foreign government own, directly or indirectly, an interest of 50% or more in the profit, |

|

|

|

|||||||

|

loss, or capital of the partnership? For rules of constructive ownership, see instructions. If “Yes,” attach Schedule |

|

|

|

|||||||

|

|

|

|

||||||||

b Did any individual or estate own, directly or indirectly, an interest of 50% or more in the profit, loss, or capital of |

|

|

|||||||||

|

|

|

|||||||||

|

the partnership? For rules of constructive ownership, see instructions. If “Yes,” attach Schedule |

|

|

|

|||||||

|

on Partners Owning 50% or More of the Partnership |

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

||

3 At the end of the tax year, did the partnership: |

|

|

|

|

|

|

|

|

|

||

a Own directly 20% or more, or own, directly or indirectly, 50% or more of the total voting power of all classes of |

|

|

|

||||||||

|

stock entitled to vote of any foreign or domestic corporation? For rules of constructive ownership, see instructions. |

|

|

|

|||||||

|

If “Yes,” complete (i) through (iv) below |

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(i) Name of Corporation |

|

|

(ii) Employer Identification |

|

(iii) Country of |

(iv) Percentage |

|||

|

|

|

|

|

Number (if any) |

|

Incorporation |

Owned in Voting Stock |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

bOwn directly an interest of 20% or more, or own, directly or indirectly, an interest of 50% or more in the profit, loss, or capital in any foreign or domestic partnership (including an entity treated as a partnership) or in the beneficial interest of a trust? For rules of constructive ownership, see instructions. If “Yes,” complete (i) through (v) below . .

(i) Name of Entity |

(ii) Employer |

(iii) Type of |

(iv) Country of |

(v) Maximum |

|

Identification |

Percentage Owned in |

||||

|

Entity |

Organization |

|||

|

Number (if any) |

Profit, Loss, or Capital |

|||

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 Does the partnership satisfy all four of the following conditions? |

Yes No |

aThe partnership’s total receipts for the tax year were less than $250,000.

bThe partnership’s total assets at the end of the tax year were less than $1 million.

cSchedules

d |

The partnership is not filing and is not required to file Schedule |

|

|

If “Yes,” the partnership is not required to complete Schedules L, |

|

|

or item L on Schedule |

|

5 |

Is this partnership a publicly traded partnership, as defined in section 469(k)(2)? |

|

6During the tax year, did the partnership have any debt that was canceled, was forgiven, or had the terms modified

so as to reduce the principal amount of the debt? . . . . . . . . . . . . . . . . . . . . .

7Has this partnership filed, or is it required to file, Form 8918, Material Advisor Disclosure Statement, to provide

information on any reportable transaction? . . . . . . . . . . . . . . . . . . . . . . . .

8At any time during calendar year 2019, did the partnership have an interest in or a signature or other authority over a financial account in a foreign country (such as a bank account, securities account, or other financial account)? See instructions for exceptions and filing requirements for FinCEN Form 114, Report of Foreign Bank and Financial Accounts (FBAR). If “Yes,” enter the name of the foreign country

9At any time during the tax year, did the partnership receive a distribution from, or was it the grantor of, or transferor to, a foreign trust? If “Yes,” the partnership may have to file Form 3520, Annual Return To Report Transactions With Foreign Trusts and Receipt of Certain Foreign Gifts. See instructions . . . . . . . . .

10a Is the partnership making, or had it previously made (and not revoked), a section 754 election? . . . . . .

See instructions for details regarding a section 754 election.

bDid the partnership make for this tax year an optional basis adjustment under section 743(b) or 734(b)? If “Yes,”

attach a statement showing the computation and allocation of the basis adjustment. See instructions . . . .

Form 1065 (2019)

Form 1065 (2019) |

|

|

Page 3 |

Schedule B |

Other Information (continued) |

|

|

c Is the partnership required to adjust the basis of partnership assets under section 743(b) or 734(b) because of a |

|

Yes No |

|

substantial |

|

||

734(d))? If “Yes,” attach a statement showing the computation and allocation of the basis adjustment. See |

|

||

instructions |

|

||

11Check this box if, during the current or prior tax year, the partnership distributed any property received in a like- kind exchange or contributed such property to another entity (other than disregarded entities wholly owned by the

partnership throughout the tax year) . . . . . . . . . . . . . . . . . . . . . . . .

12At any time during the tax year, did the partnership distribute to any partner a

undivided interest in partnership property? . . . . . . . . . . . . . . . . . . . . . . . .

13If the partnership is required to file Form 8858, Information Return of U.S. Persons With Respect To Foreign Disregarded Entities (FDEs) and Foreign Branches (FBs), enter the number of Forms 8858 attached. See

instructions . . . . . . . . . . . . . . . . . . . . . . . . . .

14Does the partnership have any foreign partners? If “Yes,” enter the number of Forms 8805, Foreign Partner’s

Information Statement of Section 1446 Withholding Tax, filed for this partnership . . .

15Enter the number of Forms 8865, Return of U.S. Persons With Respect to Certain Foreign Partnerships, attached

to this return . . . . . . . . . . . . . . . . . . . . . . . . . .

16a |

Did you make any payments in 2019 that would require you to file Form(s) 1099? See instructions |

b |

If “Yes,” did you or will you file required Form(s) 1099? |

17Enter the number of Forms 5471, Information Return of U.S. Persons With Respect To Certain Foreign

Corporations, attached to this return . . . . . . . . . . . . . . . . . .

18 Enter the number of partners that are foreign governments under section 892 . . . .

19During the partnership’s tax year, did the partnership make any payments that would require it to file Form 1042 and

20Was the partnership a specified domestic entity required to file Form 8938 for the tax year? See the Instructions

for Form 8938 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

21Is the partnership a section 721(c) partnership, as defined in Regulations section

22During the tax year, did the partnership pay or accrue any interest or royalty for which the deduction is not allowed

under section 267A? See instructions . . . . . . . . . . . . . . . . . . . . . . . . .

If “Yes,” enter the total amount of the disallowed deductions |

$ |

23Did the partnership have an election under section 163(j) for any real property trade or business or any farming

business in effect during the tax year? See instructions . . . . . . . . . . . . . . . . . . . .

24 Does the partnership satisfy one or more of the following? See instructions . . . . . . . . . . . . .

aThe partnership owns a

bThe partnership’s aggregate average annual gross receipts (determined under section 448(c)) for the 3 tax years preceding the current tax year are more than $26 million and the partnership has business interest.

cThe partnership is a tax shelter (see instructions) and the partnership has business interest expense. If “Yes” to any, complete and attach Form 8990.

25Is the partnership electing out of the centralized partnership audit regime under section 6221(b)? See instructions.

If “Yes,” the partnership must complete Schedule

If “No,” complete Designation of Partnership Representative below.

Designation of Partnership Representative (see instructions)

Enter below the information for the partnership representative (PR) for the tax year covered by this return.

Name of PR

U.S. address of PR

F

U.S. phone number of

PR

F

If the PR is an entity, name of the designated individual for the PR

U.S. address of |

F |

designated individual |

U.S. phone number of designated individual

F

26 Is the partnership attaching Form 8996 to certify as a Qualified Opportunity Fund? . . . . . . . . . .

If “Yes,” enter the amount from Form 8996, line 14 |

$ |

27Enter the number of foreign partners subject to section 864(c)(8) as a result of transferring all or a portion of an interest in the partnership or of receiving a distribution from the partnership . . . . .

28At any time during the tax year, were there any transfers between the partnership and its partners subject to the disclosure requirements of Regulations section

Form 1065 (2019)

Form 1065 (2019) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Page 4 |

|||

Schedule K |

Partners’ Distributive Share Items |

|

|

|

|

|

|

Total amount |

||||||||||||||

|

|

|

1 |

Ordinary business income (loss) (page 1, line 22) |

. . . . . . . |

1 |

|

|||||||||||||||

|

|

|

2 |

Net rental real estate income (loss) (attach Form 8825) |

. . . . . . . |

2 |

|

|||||||||||||||

|

|

|

3a |

Other gross rental income (loss) |

|

3a |

|

|

|

|||||||||||||

|

|

|

b |

Expenses from other rental activities (attach statement) |

|

3b |

|

|

|

|||||||||||||

|

|

|

c |

Other net rental income (loss). Subtract line 3b from line 3a |

. . . . . . . |

3c |

|

|||||||||||||||

|

(Loss) |

|

4 |

Guaranteed payments: a Services |

|

4a |

|

|

|

|

|

b Capital |

|

4b |

|

|

|

|||||

|

|

|

c Total. Add lines 4a and 4b |

. . . . . . . |

4c |

|

||||||||||||||||

|

|

|

|

|

||||||||||||||||||

|

|

|

5 |

Interest income |

. . . . . . . |

5 |

|

|||||||||||||||

|

Income |

|

6 |

Dividends and dividend equivalents: |

a Ordinary dividends |

. . . . . . . |

6a |

|

||||||||||||||

|

|

|

b Qualified dividends |

6b |

|

|

|

|

|

|

|

c Dividend equivalents |

|

6c |

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

7 |

Royalties |

. . . . . . . |

7 |

|

|||||||||||||||

|

|

|

8 |

Net |

. . . . . . . |

8 |

|

|||||||||||||||

|

|

|

9a |

Net |

. . . . . . . |

9a |

|

|||||||||||||||

|

|

|

b |

Collectibles (28%) gain (loss) |

|

9b |

|

|

|

|||||||||||||

|

|

|

c |

Unrecaptured section 1250 gain (attach statement) |

|

9c |

|

|

|

|||||||||||||

|

|

|

10 |

Net section 1231 gain (loss) (attach Form 4797) |

. . . . . . . |

10 |

|

|||||||||||||||

|

|

|

11 |

Other income (loss) (see instructions) |

Type |

|

|

|

|

|

|

11 |

|

|||||||||

|

Deductions |

|

d |

Other deductions (see instructions) |

Type |

|

|

|

|

. . . . . . . |

13d |

|

||||||||||

|

|

|

12 |

Section 179 deduction (attach Form 4562) |

12 |

|

||||||||||||||||

|

|

|

13a |

Contributions |

. . . . . . . |

13a |

|

|||||||||||||||

|

|

|

b |

Investment interest expense |

. . . . . . . |

13b |

|

|||||||||||||||

|

|

|

c |

Section 59(e)(2) expenditures: |

(1) |

Type |

|

|

|

|

|

(2) Amount |

13c(2) |

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

- |

|

14a |

Net earnings (loss) from |

. . . . . . . |

14a |

|

|||||||||||||||

Self- |

Employ |

ment |

|

|||||||||||||||||||

c |

Gross nonfarm income |

. . . . . . . |

14c |

|

||||||||||||||||||

|

|

|

b |

Gross farming or fishing income |

. . . . . . . |

14b |

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

15a |

. . . . . . . |

15a |

|

||||||||||||||||

|

Credits |

|

b |

. . . . . . . |

15b |

|

||||||||||||||||

|

|

c |

Qualified rehabilitation expenditures (rental real estate) (attach Form 3468, if applicable) . . |

15c |

|

|||||||||||||||||

|

|

|

|

|||||||||||||||||||

|

|

|

d |

Other rental real estate credits (see instructions) |

|

Type |

|

|

|

|

15d |

|

||||||||||

|

|

|

e |

Other rental credits (see instructions) |

Type |

|

|

|

|

|

|

15e |

|

|||||||||

|

|

|

f |

Other credits (see instructions) |

Type |

|

|

|

|

|

|

|

|

|

|

15f |

|

|||||

|

|

|

16a |

Name of country or U.S. possession |

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

b |

Gross income from all sources |

. . . . . . . |

16b |

|

|||||||||||||||

|

Transactions |

|

c |

Gross income sourced at partner level |

. . . . . . . |

16c |

|

|||||||||||||||

|

|

i |

Interest expense |

|

|

|

j Other |

. . . . . . |

16j |

|

||||||||||||

|

|

|

|

Foreign gross income sourced at partnership level |

|

|

|

|

|

|

|

|||||||||||

|

|

|

d |

Reserved for future use |

|

|

|

|

|

|

|

|

e Foreign branch category |

16e |

|

|||||||

|

|

|

f |

Passive category |

g General category |

|

h Other (attach statement) |

16h |

|

|||||||||||||

|

|

|

|

Deductions allocated and apportioned at partner level |

|

|

|

|

|

|

||||||||||||

|

Foreign |

|

|

Deductions allocated and apportioned at partnership level to foreign source income |

|

|

||||||||||||||||

|

|

|

|

|

||||||||||||||||||

|

|

|

k |

Reserved for future use |

|

|

|

|

|

|

|

|

l |

Foreign branch category |

. . . . . |

16l |

|

|||||

|

|

|

m |

Passive category |

n General category |

|

o Other (attach statement) |

16o |

|

|||||||||||||

|

|

|

p |

Total foreign taxes (check one): |

|

Paid |

Accrued |

. . . . |

|

. . . . . . . |

16p |

|

||||||||||

|

|

|

q |

Reduction in taxes available for credit (attach statement) |

. . . . . . . |

16q |

|

|||||||||||||||

|

|

|

r |

Other foreign tax information (attach statement) |

|

|

|

|

|

|

|

|

||||||||||

Alternative |

TaxMinimum |

Items(AMT) |

17a |

. . . . . . . |

17a |

|

||||||||||||||||

b |

Adjusted gain or loss |

. . . . . . . |

17b |

|

||||||||||||||||||

|

|

|

|

|||||||||||||||||||

|

|

|

c |

Depletion (other than oil and gas) |

. . . . . . . |

17c |

|

|||||||||||||||

|

|

|

d |

Oil, gas, and geothermal |

. . . . . . . |

17d |

|

|||||||||||||||

|

|

|

e |

Oil, gas, and geothermal |

. . . . . . . |

17e |

|

|||||||||||||||

|

|

|

f |

Other AMT items (attach statement) |

. . . . . . . |

17f |

|

|||||||||||||||

|

Information |

|

18a |

. . . . . . . |

18a |

|

||||||||||||||||

|

|

b |

Other |

. . . . . . . |

18b |

|

||||||||||||||||

|

|

|

|

|||||||||||||||||||

|

|

|

c |

Nondeductible expenses |

. . . . . . . |

18c |

|

|||||||||||||||

|

|

|

19a |

Distributions of cash and marketable securities |

. . . . . . . |

19a |

|

|||||||||||||||

|

|

|

b |

Distributions of other property |

. . . . . . . |

19b |

|

|||||||||||||||

|

Other |

|

20a |

Investment income |

. . . . . . . |

20a |

|

|||||||||||||||

|

|

b |

Investment expenses |

. . . . . . . |

20b |

|

||||||||||||||||

|

|

|

|

|||||||||||||||||||

|

|

|

c |

Other items and amounts (attach statement) |

|

|

|

|

|

|

|

|

||||||||||

Form 1065 (2019)

Form 1065 (2019) |

Page 5 |

Analysis of Net Income (Loss)

1Net income (loss). Combine Schedule K, lines 1 through 11. From the result, subtract the sum of

|

Schedule K, lines 12 through 13d, and 16p |

. |

. . |

1 |

|

||||

2 |

Analysis by |

(i) Corporate |

(ii) Individual |

(iii) Individual |

(iv) Partnership |

(v) |

Exempt |

|

(vi) |

|

partner type: |

|

(active) |

(passive) |

|

Organization |

Nominee/Other |

||

aGeneral partners b Limited partners

Schedule L |

|

Balance Sheets per Books |

Beginning of tax year |

|

End of tax year |

|||||

|

|

|

Assets |

|

(a) |

(b) |

(c) |

|

(d) |

|

1 |

Cash |

|

|

|

|

|

|

|||

2a |

Trade notes and accounts receivable |

|

|

|

|

|

|

|||

b |

Less allowance for bad debts |

|

|

|

|

|

|

|||

3 |

Inventories |

|

|

|

|

|

|

|||

4 |

U.S. government obligations |

|

|

|

|

|

|

|||

5 |

|

|

|

|

|

|

||||

6 |

Other current assets (attach statement) |

|

|

|

|

|

|

|||

7a |

Loans to partners (or persons related to partners) . |

|

|

|

|

|

|

|||

b |

Mortgage and real estate loans |

|

|

|

|

|

|

|||

8 |

Other investments (attach statement) |

|

|

|

|

|

|

|||

9a |

Buildings and other depreciable assets |

|

|

|

|

|

|

|||

b |

Less accumulated depreciation |

|

|

|

|

|

|

|||

10a |

Depletable assets |

|

|

|

|

|

|

|||

b |

Less accumulated depletion |

|

|

|

|

|

|

|||

11 |

Land (net of any amortization) |

|

|

|

|

|

|

|||

12a |

Intangible assets (amortizable only) |

|

|

|

|

|

|

|||

b |

Less accumulated amortization |

|

|

|

|

|

|

|||

13 |

Other assets (attach statement) |

|

|

|

|

|

|

|||

14 |

Total assets |

|

|

|

|

|

|

|||

|

|

|

Liabilities and Capital |

|

|

|

|

|

||

15 |

Accounts payable |

|

|

|

|

|

|

|||

16 |

Mortgages, notes, bonds payable in less than 1 year |

|

|

|

|

|

|

|||

17 |

Other current liabilities (attach statement) . . . . |

|

|

|

|

|

|

|||

18 |

All nonrecourse loans |

|

|

|

|

|

|

|||

19a |

Loans from partners (or persons related to partners) . |

|

|

|

|

|

|

|||

b |

Mortgages, notes, bonds payable in 1 year or more . |

|

|

|

|

|

|

|||

20 |

Other liabilities (attach statement) |

|

|

|

|

|

|

|||

21 |

Partners’ capital accounts |

|

|

|

|

|

|

|||

22 |

Total liabilities and capital |

|

|

|

|

|

||||

Schedule |

Reconciliation of Income (Loss) per Books With Income (Loss) per Return |

|

|

|||||||

Note: The partnership may be required to file Schedule

1Net income (loss) per books . . . .

2Income included on Schedule K, lines 1, 2, 3c, 5, 6a, 7, 8, 9a, 10, and 11, not recorded on books this year (itemize):

3Guaranteed payments (other than health

insurance) . . . . . . . . . .

4Expenses recorded on books this year not included on Schedule K, lines 1 through 13d, and 16p (itemize):

aDepreciation $

bTravel and entertainment $

5 Add lines 1 through 4 . . . . . .

6Income recorded on books this year not included on Schedule K, lines 1 through 11 (itemize):

a

7Deductions included on Schedule K, lines 1 through 13d, and 16p, not charged against book income this year (itemize):

aDepreciation $

8 Add lines 6 and 7 . . . . . . . .

9Income (loss) (Analysis of Net Income (Loss), line 1). Subtract line 8 from line 5

Schedule

1 |

Balance at beginning of year . . . |

2 |

Capital contributed: a Cash . . . |

|

b Property . . |

3Net income (loss) per books . . . .

4 Other increases (itemize):

5 Add lines 1 through 4 . . . . . .

6 Distributions: a Cash . . . . . .

b Property . . . . .

7Other decreases (itemize):

8 Add lines 6 and 7 . . . . . . . .

9Balance at end of year. Subtract line 8 from line 5

Form 1065 (2019)

| Fact Name | Description |

|---|---|

| Purpose | The IRS Form 1065 is used by partnerships to report income, deductions, gains, losses, and other financial information. |

| Filing Requirement | Partnerships must file Form 1065 annually, regardless of whether they have income or not. |

| Due Date | Form 1065 is typically due on March 15th following the end of the partnership's tax year. |

| State-Specific Forms | Many states require additional forms, governed by their specific tax laws. For example, California requires Form 565. |

| Pass-Through Taxation | Partnerships themselves do not pay income tax. Instead, profits and losses pass through to individual partners and are reported on their personal tax returns. |

Filling out the IRS 1065 form is an essential task for partnerships to report their income, deductions, and other important tax-related information. Once you have the form ready, you'll need to gather your financial documents. Understanding what is required can simplify the process, making it more manageable.

After submission, keep a copy of the completed form and supporting documents for your records. This practice can assist in future dealings with the IRS, as well as in maintaining clear records of the partnership's financial activities.

The IRS 1065 form is a tax document used by partnerships to report income, gains, losses, and other financial information to the Internal Revenue Service (IRS). This form does not require the partnership itself to pay taxes on its income. Instead, the profits and losses are passed through to the individual partners who report them on their personal tax returns.

Any partnership, including limited liability companies (LLCs) treated as partnerships for tax purposes, must file Form 1065. If the business has more than one owner, filing is generally required. Certain exceptions may apply, so it is wise to consult a tax professional if there is uncertainty.

Form 1065 is typically due on March 15th of the year following the close of the partnership's tax year. If the partnership operates on a calendar year basis, the form must be filed by March 15th of the following year. However, extensions can be requested, providing additional time to file.

Form 1065 requires various pieces of information, including:

Each partner receives a Schedule K-1 (Form 1065) from the partnership. This document details each partner's share of the partnership's income, deductions, and credits. Partners must report this information on their personal tax returns, typically using IRS Form 1040.

Yes, Form 1065 can be electronically filed. Many software programs support e-filing for partnerships. Using e-filing can expedite processing times and facilitate easier tracking of the filing status.

Penalties can apply for not filing Form 1065 on time. Penalties vary based on the size of the partnership and the duration of the delay. If a partnership fails to file on time, it may face fines per partner for each month the return is late, up to a maximum amount.

Yes, many states have their own filing requirements for partnerships, independent of federal requirements. Partnerships must check with their state tax agency to understand if they need to file additional forms or pay state taxes.

Even if a partnership had no income or operations during the tax year, it is still required to file Form 1065 and report its activities. A “no income” return must clearly indicate that no income was generated, ensuring compliance with filing rules.

Form 1065 can be downloaded from the IRS website. It is available in PDF format and can be printed for completion. Additionally, many tax preparation software programs offer access to the form and provide step-by-step guidance for filling it out.

When filling out the IRS 1065 form, many partnerships encounter common mistakes that can lead to delays, penalties, or even audits. Understanding these pitfalls can help ensure that your filing is accurate and compliant with IRS regulations.

One frequent error occurs with the partnership’s identification information. Each partner must be accurately listed, including Social Security Numbers or Employer Identification Numbers. Missing or incorrect information can raise red flags and trigger an audit.

Another common mistake is failing to include all sources of income. Partnerships often have multiple revenue streams. Omitting any income can result in incomplete reporting, which may lead to penalties.

Incorrectly calculating deductions is also a prevalent issue. Partnerships can deduct various business expenses, but not understanding what qualifies can lead to errors. Ensuring that only valid deductions are claimed is critical to maintaining compliance.

A significant number of filers overlook the importance of checking math calculations. Simple arithmetic errors can lead to complications. Double-checking all figures can help avoid unnecessary issues and corrections later on.

Some partnerships fail to list all partners correctly. Each partner’s percentage of ownership must be disclosed accurately. Errors in this section can misrepresent the financial standing of the partnership, which may have legal implications.

Another mistake is not reviewing the instructions. Each year, there may be updates to the form or changes in tax laws that affect how the 1065 is completed. Keeping informed about current requirements will lead to a smoother filing process.

Missing or failing to sign the form is also a common oversight. The IRS requires that each partner or authorized representative signs the 1065. Without these signatures, the form may be rejected.

Partnerships sometimes confuse the deadlines for filing. Filing late can incur penalties, so it is crucial to be aware of the deadline. This timing ensures that all forms are submitted promptly to avoid issues.

Lastly, many filers do not keep copies of their submitted documents. It is advisable to retain copies of the filed 1065 and supporting documents for future reference. This practice is essential in case of any disputes or audits.

The IRS Form 1065 is essential for partnerships to report their income, deductions, and other financial information. However, it’s not the only document that may be needed to accompany this form. Here are a few other important forms and documents that partnerships often use along with the Form 1065:

When it comes to tax filings, being thorough and organized is crucial. Each of these forms plays a significant role in the tax compliance process for partnerships, ensuring that both the partnership and its partners meet their obligations accurately and on time.

The IRS Form 1065 is utilized by partnerships to report their income, deductions, and other tax-related information. This form plays a crucial role in ensuring that partnerships comply with tax regulations. Several other documents serve similar purposes, aiding in the reporting of income and other financial information. Below is a list of documents that share similarities with the IRS Form 1065:

Each of these forms has unique features tailored to specific types of entities or situations, yet they all share the common goal of ensuring transparency and compliance in reporting financial information to the IRS.

When filling out the IRS Form 1065, it is important to follow certain guidelines to ensure accuracy and compliance. Here are some recommendations on what to do and what to avoid:

Filling out the IRS 1065 form is essential for partnerships to report their income, deductions, gains, and losses. Here are some key takeaways to keep in mind: