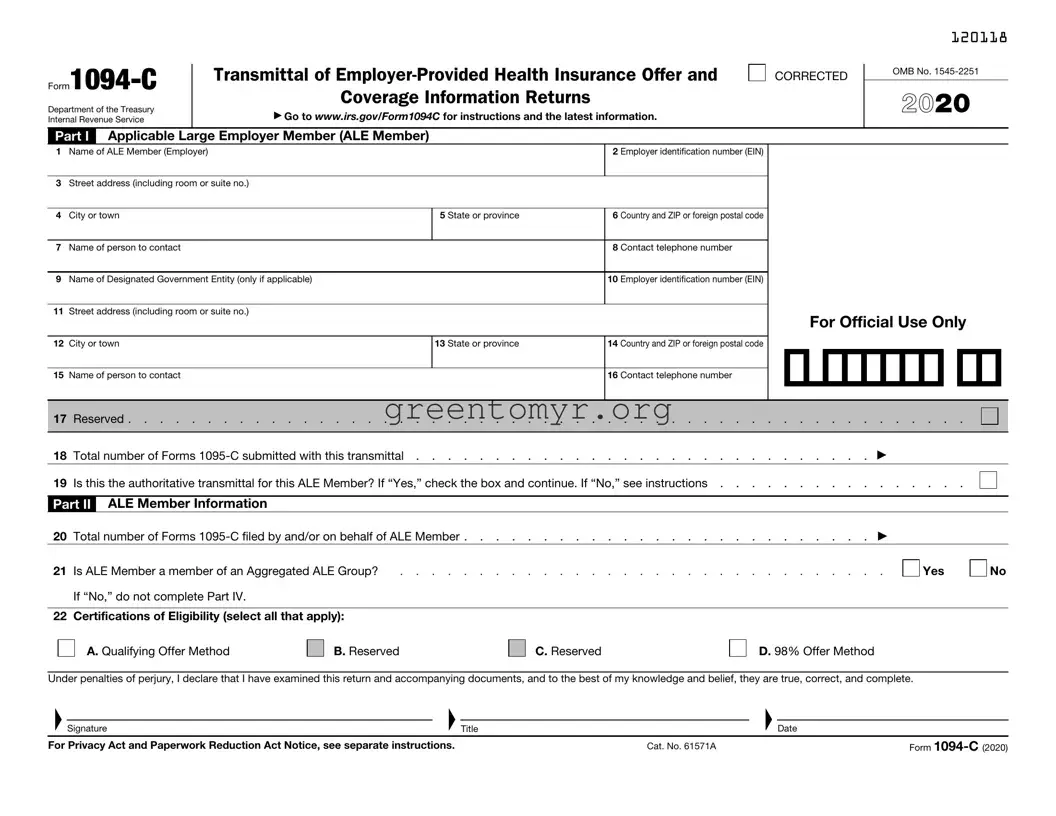

The IRS 1094-C form plays a crucial role in the Affordable Care Act's reporting requirements for applicable large employers (ALEs). Primarily, this form serves as a transmittal document that provides the IRS with information about the health insurance coverage offered to employees and their dependents. Employers must accurately complete this form to report not only the number of full-time employees but also the months in which health coverage was available to those employees. The 1094-C encompasses various sections that outline details such as employer information, the total number of Form 1095-C submissions, and the type of health coverage provided. By doing so, ALEs can demonstrate compliance with the health coverage mandate, thereby avoiding potential penalties. Timely submission of the 1094-C is essential, particularly since deadlines align with other tax reporting schedules, and errors can lead to complications with the IRS. Understanding the nuances of this form is vital for businesses to ensure compliance and maintain good standing with tax regulations.

|

Transmittal of |

||

|

|||

Department of the Treasury |

|

Coverage Information Returns |

|

|

▶ Go to www.irs.gov/Form1094C for instructions and the latest information. |

||

Internal Revenue Service |

|

||

|

|

|

|

Part I |

Applicable Large Employer Member (ALE Member) |

||

CORRECTED

120118

OMB No.

2020

1 Name of ALE Member (Employer) |

2 Employer identification number (EIN) |

|

|

3Street address (including room or suite no.)

4 |

City or town |

5 State or province |

6 |

Country and ZIP or foreign postal code |

|

|

|

|

|

7 |

Name of person to contact |

|

8 |

Contact telephone number |

|

|

|

|

|

9 |

Name of Designated Government Entity (only if applicable) |

|

10 |

Employer identification number (EIN) |

|

|

|

|

|

11Street address (including room or suite no.)

12 City or town |

13 State or province |

14 Country and ZIP or foreign postal code |

|

|

|

For Official Use Only

15Name of person to contact

16 Contact telephone number

17 |

Reserved |

|

|

|

|

|

|||

|

|

|

|

|

18 |

Total number of Forms |

|||

19 |

|

|

||

Is this the authoritative transmittal for this ALE Member? If “Yes,” check the box and continue. If “No,” see instructions |

|

|

||

Part II ALE Member Information

20 |

Total number of Forms |

. . . |

. |

. |

. . . . . . . |

▶ |

|

||||

21 |

Is ALE Member a member of an Aggregated ALE Group? |

. . . |

. |

. |

. . . . . . . |

. |

Yes |

||||

|

If “No,” do not complete Part IV. |

|

|

|

|

|

|

|

|

|

|

22 |

Certifications of Eligibility (select all that apply): |

|

|

|

|

|

|

|

|

||

|

A. Qualifying Offer Method |

|

B. Reserved |

|

C. Reserved |

|

|

|

D. 98% Offer Method |

|

|

|

|

|

|

|

|

|

|

||||

Under penalties of perjury, I declare that I have examined this return and accompanying documents, and to the best of my knowledge and belief, they are true, correct, and complete.

▲ |

|

▲ |

|

▲Date |

Signature |

Title |

No

For Privacy Act and Paperwork Reduction Act Notice, see separate instructions. |

Cat. No. 61571A |

Form |

|

|

|

|

|

|

|

|

120218 |

Form |

|

|

|

|

Page 2 |

|||

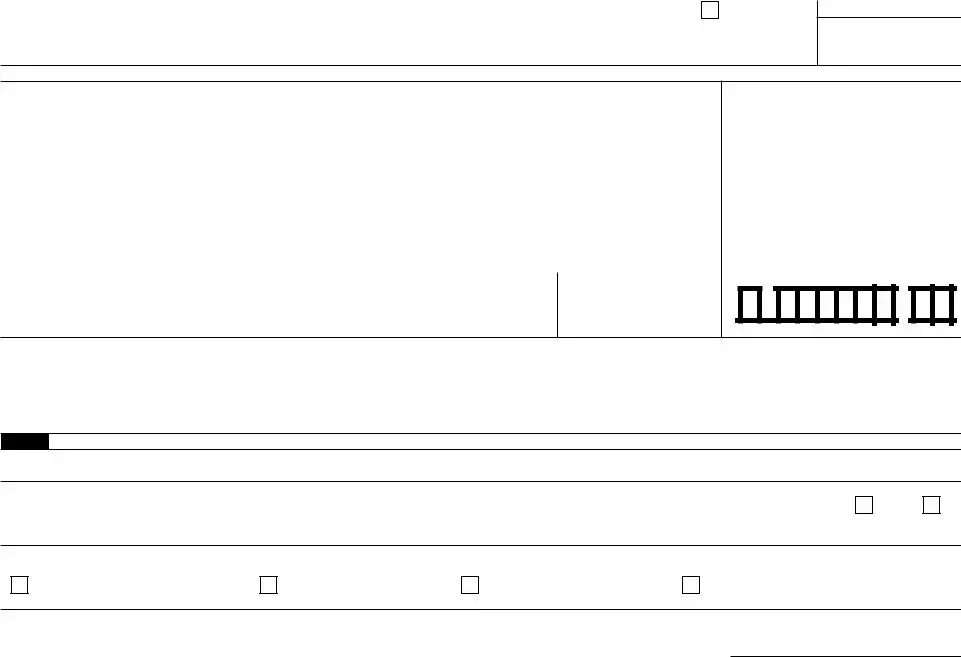

Part III |

ALE Member |

|

|

|

|

|

||

|

|

(a) Minimum Essential Coverage |

(b) Section 4980H |

(c) Total Employee Count |

(d) Aggregated |

(e) Reserved |

||

|

|

Offer Indicator |

|

|||||

|

|

|

Employee Count for ALE Member |

for ALE Member |

Group Indicator |

|

||

|

|

|

|

|

|

|||

|

|

Yes |

|

No |

|

|

|

|

23 |

All 12 Months |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

24 |

Jan |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

25 |

Feb |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

26 |

Mar |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

27 |

Apr |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

28 |

May |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

29 |

June |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

30 |

July |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

31 |

Aug |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

32 |

Sept |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

33 |

Oct |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

34 |

Nov |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

35 |

Dec |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form

|

|

120316 |

Form |

Page 3 |

|

Part IV |

Other ALE Members of Aggregated ALE Group |

|

Enter the names and EINs of Other ALE Members of the Aggregated ALE Group (who were members at any time during the calendar year).

Name |

EIN |

Name |

36 |

|

51 |

|

||

37 |

|

52 |

38 |

|

53 |

39 |

|

54 |

40 |

|

55 |

41 |

|

56 |

42 |

|

57 |

43 |

|

58 |

44 |

|

59 |

45 |

|

60 |

46 |

|

61 |

47 |

|

62 |

48 |

|

63 |

49 |

|

64 |

50 |

|

65 |

|

|

|

EIN

Form

| Fact Name | Description |

|---|---|

| Purpose | The IRS 1094-C form is used by applicable large employers to report health coverage information to the IRS. |

| Filing Requirement | Employers with 50 or more full-time equivalent employees must file this form. |

| Frequency | The form must be filed annually, typically by February 28 or March 31 if e-filing. |

| Information Included | The 1094-C includes data about the employer, the total number of full-time employees, and the months each employee had coverage. |

| Transmittal Form | The 1094-C serves as a transmittal for the 1095-C forms, which detail health coverage given to employees. |

| Penalties | Failure to file can result in significant penalties for employers, based on the number of days late. |

| State-Specific Forms | Some states, like California and Massachusetts, require additional state-specific forms in conjunction with the 1094-C. |

| Governing Law | ACA (Affordable Care Act) provisions govern the filing and requirements of the 1094-C. |

| Electronic Filing | Employers are encouraged to e-file the 1094-C, especially if filing more than 250 forms. |

| Form Availability | The IRS provides the form online on their official website for download and printing. |

Filling out the IRS 1094-C form is an important task for employers who need to report information about health coverage offered to their employees. Following the steps below will guide you through the process to ensure accuracy and compliance.

The IRS 1094-C form serves as a transmittal document for employers to report information about their offers of health coverage to employees. This form is particularly important for applicable large employers (ALEs), those with 50 or more full-time employees, as part of the Affordable Care Act (ACA) requirements.

Applicable large employers, defined as those with 50 or more full-time employees or full-time equivalent employees, are required to file the 1094-C form. This also includes any entity that is part of a controlled group of corporations or affiliated service groups, which share membership for health coverage purposes.

The deadline for filing the 1094-C form is generally the last day of February of the year following the calendar year to which the form pertains. If filing electronically, this deadline extends to March 31. It's crucial to check the IRS website for any specific updates on deadlines.

The 1094-C form requests various pieces of information, including:

This data helps the IRS assess compliance with ACA regulations concerning health coverage.

The form can be filed either on paper or electronically. If filing on paper, a completed 1094-C must be mailed to the IRS. When filing electronically, employers can use the IRS’s e-file system or third-party software that supports ACA reporting.

Failing to file the 1094-C form can lead to penalties from the IRS. These penalties may vary based on the number of days late and the size of the employer. It's essential to file on time to avoid these financial consequences.

Yes, if you discover an error after filing, you can submit a corrected form. Be sure to follow the IRS instructions for corrections, which may require marking the corrected form appropriately to indicate changes.

Employers must provide a copy of the 1095-C form, which is related to the 1094-C, to each full-time employee. This can be done electronically or by mailing paper copies, but employees must consent to receive electronic forms.

For further assistance, visit the IRS website, where detailed instructions and resources are available. You may also consult a tax professional or legal expert for specific questions related to your situation.

Completing the IRS 1094-C form can be complicated, and many people make mistakes that can lead to issues with their tax submissions. One common error is failing to include accurate employer information. The form requires the correct name, address, and Employer Identification Number (EIN). Missing or incorrect details can result in delays or even penalties.

Many individuals also misinterpret the employee count. It’s essential to report the total number of full-time employees accurately. Including part-time employees in this count can trigger misunderstandings with the IRS and may affect healthcare coverage requirements.

Another frequent mistake is omitting the necessary offer of coverage details. The form asks for information about the health coverage provided to employees. Be sure to specify whether the coverage meets minimum value and affordability standards. Neglecting to provide this information can lead to compliance issues.

Inadequate identification of controlled groups is yet another pitfall. Organizations that are part of controlled groups must report combined employee counts and coverage offers accurately. Failing to recognize this can cause discrepancies in submitted data.

People often underestimate the importance of signing and dating the form. A signed and dated form is crucial for it to be considered valid. Not doing so can lead to rejections or delays in processing.

Improperly identifying Applicable Large Employers (ALE) can complicate the entire process. It’s essential to determine if your organization meets the criteria for being classified as an ALE. Misclassification could amplify tax liabilities or compliance penalties.

Using previous years' data is another common error. Each year's guidelines and requirements for the 1094-C form can change significantly. Relying on outdated information can lead to a host of issues down the line.

Providing incomplete coverage details is also a significant concern. Employers must furnish comprehensive information about the coverage they offered, including the months the coverage was available. Leaving any gaps in this information can result in compliance problems.

Another mistake is misreporting the plan year. Ensure that the correct plan year is indicated. This is especially critical if your organization operates on a non-calendar plan year, as discrepancies can confuse the IRS.

Lastly, failure to retain copies of submitted forms can present problems in the future. Keeping a record of all forms filed is necessary for reference and can help in case any questions arise from the IRS down the line.

The IRS 1094-C form is a crucial document for employers to report health coverage information to the Internal Revenue Service. It serves as a transmittal form for the 1095-C forms, which detail the individual employee's health insurance coverage status. Along with the 1094-C, other documents are often used to ensure compliance with the Affordable Care Act (ACA) and to provide accurate reporting of health insurance offerings. Below are some of the key documents frequently associated with the 1094-C form.

Understanding these documents in relation to the IRS 1094-C form is essential for employers to maintain compliance with health care reporting requirements. Proper documentation helps ensure that both employers and employees fulfill their obligations under the ACA, ultimately contributing to a smoother tax filing process.

When filling out the IRS 1094-C form, it’s essential to be careful and thorough. Here are ten do's and don'ts to keep in mind:

The IRS 1094-C form plays a crucial role in reporting information about health coverage offered by applicable large employers (ALEs). However, several misconceptions exist regarding its purpose and requirements. Below is a list of common misunderstandings related to Form 1094-C.

The IRS 1094-C form serves as a transmittal form to report information about applicable large employers (ALEs) and their compliance with the Affordable Care Act (ACA).

Ensure accuracy while filling out the form; mistakes can lead to penalties or delays in processing.

Collect all necessary records beforehand. You'll need information about your employee counts and health coverage offerings.

Make sure to include your Employer Identification Number (EIN), as it is crucial for proper identification and processing of your form.

Failing to file by the deadline can result in significant fines, so keep track of submission dates.

The form must be submitted electronically if you are filing 250 or more forms. Smaller employers can file by mail.

Keep a copy of the submitted form and any correspondence with the IRS, as you may need it for future reference or audits.