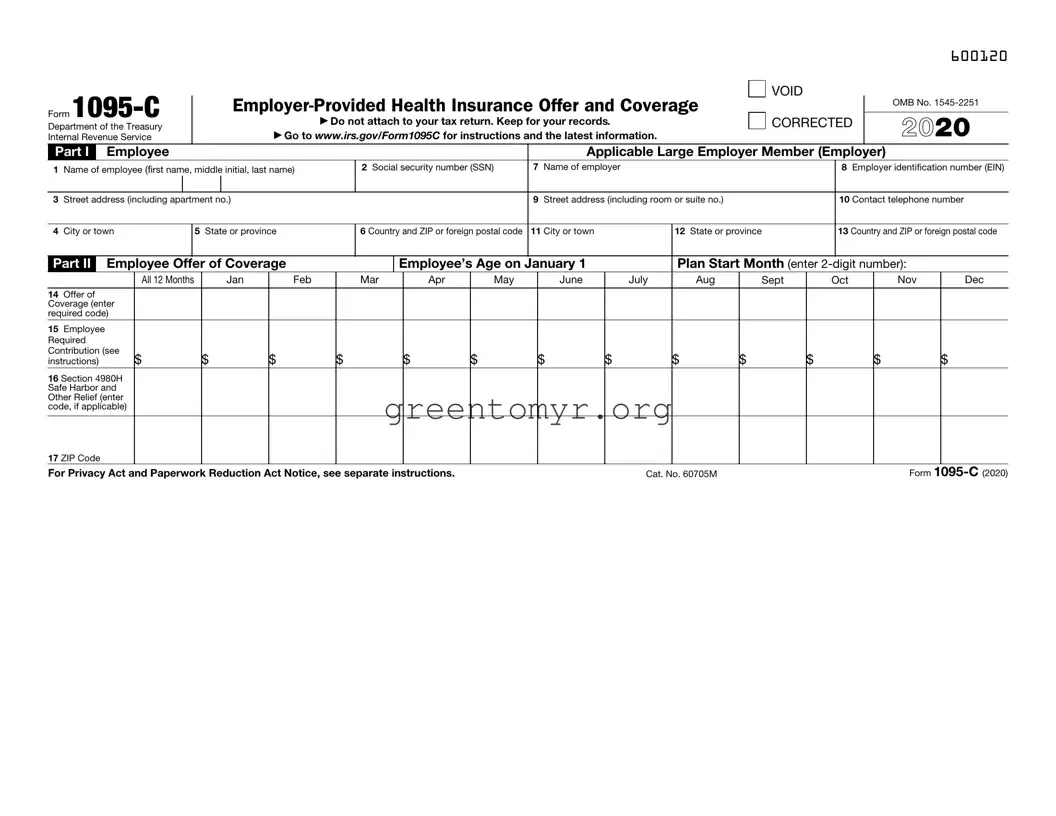

The IRS 1095-C form plays a critical role in the landscape of health care and tax reporting in the United States, particularly for large employers. Employers with 50 or more full-time employees are required to provide this form, which details the health coverage offered to employees throughout the year. The 1095-C serves not only as a record of the health insurance benefits provided but also as an essential tool for employees during tax filing season. It includes important information such as the type of coverage offered, the months during which coverage was available, and employee details to ensure compliance with the Affordable Care Act (ACA). By accurately documenting this information, the form helps the IRS enforce health insurance mandates and aids employees in understanding their health coverage status. As such, familiarity with the 1095-C is vital for both employers and employees to navigate their rights and responsibilities under federal health care laws.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

600120 |

Form |

|

|

|

|

▶ |

|

|

|

|

|

|

|

|

VOID |

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

OMB No. |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Department of the Treasury |

|

|

|

|

|

Do not attach to your tax return. Keep for your records. |

|

|

CORRECTED |

|

2020 |

|||||||||||||

Internal Revenue Service |

|

|

|

▶ Go to www.irs.gov/Form1095C for instructions and the latest information. |

|

|

|

|

|

|

||||||||||||||

Part I |

|

Employee |

|

|

|

|

|

|

|

|

|

|

Applicable Large Employer Member (Employer) |

|

|

|||||||||

1 |

Name of employee (first name, middle initial, last name) |

|

|

2 Social security number (SSN) |

7 Name of employer |

|

|

|

|

8 Employer identification number (EIN) |

||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

3 |

Street address (including apartment no.) |

|

|

|

|

|

|

9 Street address (including room or suite no.) |

|

|

|

10 Contact telephone number |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

4 |

City or town |

|

|

|

5 State or province |

|

|

6 Country and ZIP or foreign postal code |

11 City or town |

12 State or province |

|

13 Country and ZIP or foreign postal code |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

Part II |

Employee Offer of Coverage |

|

|

|

Employee’s Age on January 1 |

|

Plan Start Month (enter |

|

||||||||||||||||

|

|

|

|

All 12 Months |

|

Jan |

Feb |

|

|

Mar |

Apr |

May |

June |

July |

Aug |

|

Sept |

Oct |

Nov |

Dec |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14 |

Offer of |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Coverage (enter |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

required code) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

15 |

Employee |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Required |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Contribution (see |

$ |

|

|

$ |

|

$ |

|

$ |

|

$ |

$ |

$ |

$ |

$ |

$ |

$ |

$ |

|

$ |

|||||

instructions) |

|

|

|

|

|

|

|

|||||||||||||||||

16 Section 4980H Safe Harbor and Other Relief (enter code, if applicable)

17 ZIP Code |

|

Form |

For Privacy Act and Paperwork Reduction Act Notice, see separate instructions. |

Cat. No. 60705M |

600220

Form |

Page 2 |

Instructions for Recipient

You are receiving this Form

In addition, if you, or any other individual who is offered health coverage because of their relationship to you (referred to here as family members), enrolled in your employer’s health plan and that plan is a type of plan referred to as a

If your employer provided you or a family member health coverage through an insured health plan or in another manner, you may receive information about the coverage separately on Form

Employers are required to furnish Form

Additional information. For additional information about the tax provisions of the Affordable Care Act (ACA), including the individual shared responsibility provisions, the premium tax credit, and the employer shared responsibility provisions, visit www.irs.gov/ACA or call the IRS Healthcare Hotline for ACA questions

Part I. Employee

Lines

Line 2. This is your social security number (SSN). For your protection, this form may show only the last four digits of your SSN. However, the employer is required to report your complete SSN to the IRS.

Part I. Applicable Large Employer Member (Employer)

Lines

Line 10. This line includes a telephone number for the person whom you may call if you have questions about the information reported on the form or to report errors in the information on the form and ask that they be corrected.

Part II. Employer Offer of Coverage, Lines

Line 14. The codes listed below for line 14 describe the coverage that your employer offered to you and your spouse and dependent(s), if any. (If you received an offer of coverage through a multiemployer plan due to your membership in a union, that offer may not be shown on line 14.) The information on line 14 relates to eligibility for coverage subsidized by the premium tax credit for you, your spouse, and dependent(s). For more information about the premium tax credit, see Pub. 974.

1A. Minimum essential coverage providing minimum value offered to you with an employee required contribution for

1B. Minimum essential coverage providing minimum value offered to you and minimum essential coverage NOT offered to your spouse or dependent(s).

1C. Minimum essential coverage providing minimum value offered to you and minimum essential coverage offered to your dependent(s) but NOT your spouse.

1D. Minimum essential coverage providing minimum value offered to you and minimum essential coverage offered to your spouse but NOT your dependent(s).

1E. Minimum essential coverage providing minimum value offered to you and minimum essential coverage offered to your dependent(s) and spouse.

1F. Minimum essential coverage NOT providing minimum value offered to you, or you and your spouse or dependent(s), or you, your spouse, and dependent(s).

1G. You were NOT a

1H. No offer of coverage (you were NOT offered any health coverage or you were offered coverage that is NOT minimum essential coverage).

1I. Reserved for future use.

1J. Minimum essential coverage providing minimum value offered to you; minimum essential coverage conditionally offered to your spouse; and minimum essential coverage NOT offered to your dependent(s).

1K. Minimum essential coverage providing minimum value offered to you; minimum essential coverage conditionally offered to your spouse; and minimum essential coverage offered to your dependent(s).

1L. Individual coverage health reimbursement arrangement (HRA) offered to you only with affordability determined by using employee’s primary residence location ZIP code.

1M. Individual coverage HRA offered to you and dependent(s) (not spouse) with affordability determined by using employee’s primary residence location ZIP code.

1N. Individual coverage HRA offered to you, spouse and dependent(s) with affordability determined by using employee’s primary residence location ZIP code.

1O. Individual coverage HRA offered to you only using the employee’s primary employment site ZIP code affordability safe harbor.

1P. Individual coverage HRA offered to you and dependent(s) (not spouse) using the employee’s primary employment site ZIP code affordability safe harbor.

1Q. Individual coverage HRA offered to you, spouse and dependent(s) using the employee’s primary employment site ZIP code affordability safe harbor.

1R. Individual coverage HRA that is NOT affordable offered to you; employee and spouse or dependent(s); or employee, spouse, and dependents.

1S. Individual coverage HRA offered to an individual who was not a

1T. Reserved for future use.

1U. Reserved for future use.

1V. Reserved for future use.

1W. Reserved for future use.

1X. Reserved for future use.

1Y. Reserved for future use.

1Z. Reserved for future use.

(Continued on page 4)

600320

Form |

Page 3 |

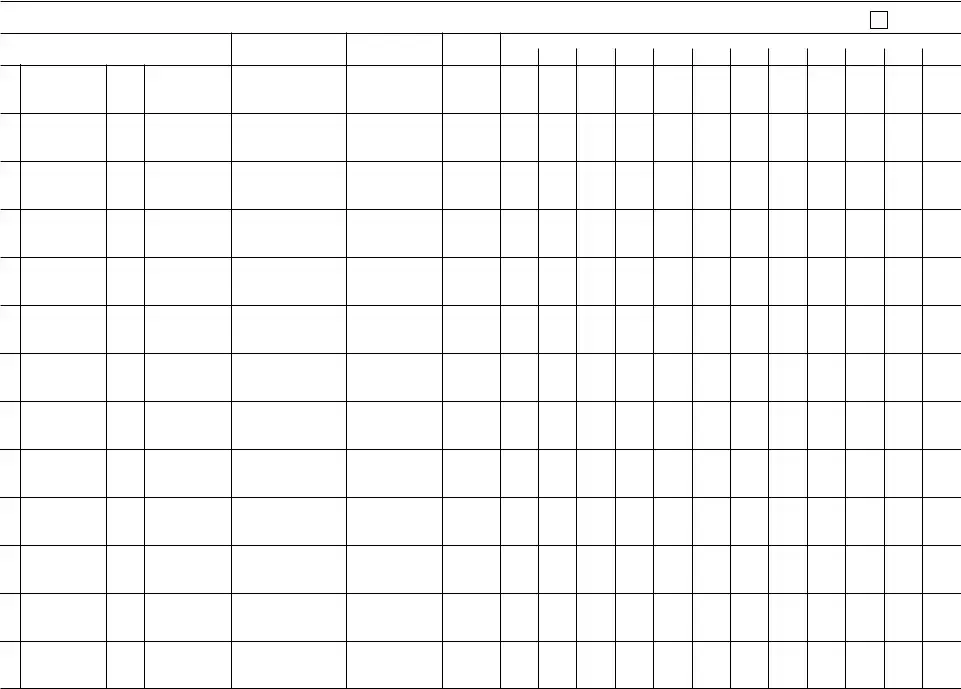

Part III Covered Individuals

If Employer provided

18

19

20

21

22

23

24

25

26

27

28

29

30

(a) Name of covered individual(s) |

(b) SSN or other TIN (c) DOB (if SSN or other |

(d) Covered |

|

|

|

|

|

|

|

|

(e) Months of coverage |

|

|

|

|

|

|

||||||||||||

First name, middle initial, last name |

TIN is not available) |

all 12 months |

|

Jan |

Feb |

Mar |

Apr |

May June July |

Aug Sept |

Oct |

Nov |

Dec |

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form

600420

Form |

Page 4 |

Instructions for Recipient (continued)

Line 15. This line reports the employee required contribution, which is the monthly cost to you for the

Line 16. This code provides the IRS information to administer the employer shared responsibility provisions. Other than a code 2C, which reflects your enrollment in your employer’s coverage, none of this information affects your eligibility for the premium tax credit. For more information about the employer shared responsibility provisions, visit IRS.gov.

Line 17. This line reports the applicable ZIP code your employer used for determining affordability if you were offered an individual coverage HRA. If code 1L, 1M, or 1N was used on line 14, this will be your primary residence location. If code 1O, 1P, or 1Q was used on line 14, this will be your primary work location. For more information about individual coverage HRAs, visit IRS.gov.

Part III. Covered Individuals, Lines

Part III reports the name, SSN (or TIN for covered individuals other than the employee listed in Part I), and coverage information about each individual (including any

| Fact Name | Description |

|---|---|

| Purpose of Form | The IRS 1095-C form provides information about health insurance coverage offered by an employer to its employees. |

| Who Receives It | Employees who worked for an Applicable Large Employer (ALE) during the year should receive this form. |

| Reporting Requirement | Employers with 50 or more full-time employees must file Form 1095-C to report health insurance coverage provided. |

| Deadline for Issuance | The form must be provided to employees by March 2 of the year following the year of reporting. |

| Tax Filing Inclusion | Employees do not need to attach Form 1095-C to their tax returns but should keep it for their records. |

| State-Specific Forms | Some states, like California and New Jersey, also require specific health coverage reporting forms under their laws. |

| Penalties for Non-Compliance | Failure to provide or file the 1095-C form correctly can result in penalties imposed by the IRS. |

| Information Included | The form includes details about the coverage offered, employee enrollment, and months of coverage. |

| Related Legislation | The Affordable Care Act (ACA) is the primary legislation governing the requirement for the 1095-C form. |

After completing the IRS 1095-C form, review it carefully for any errors. This form will be sent to the IRS and to the employees, so accuracy is essential. Below are the steps to fill out the form correctly.

The IRS 1095-C form is a document provided by applicable large employers (ALEs) to their employees. It details the health insurance coverage offered to employees, their spouses, and dependents during the year. This form is essential for employees to understand their health care options and determine if they are eligible for premium tax credits or if they need to pay a penalty for not having coverage.

Any employee who works for an applicable large employer (i.e., generally those with 50 or more full-time employees) should receive a 1095-C form. This includes full-time employees, part-time employees, and sometimes those who were employed for a short period during the year. If you were employed by an ALE for any part of the year, expect to receive your form from that employer.

Employers are required to send out the 1095-C form by March 2 of the year following the coverage year. For example, if you are looking for a 1095-C for the year 2023, it should arrive by March 2, 2024. It can be delivered by mail or electronically, depending on your employer's policy and your consent.

The information on the 1095-C form helps you when filing your federal tax return. You will need it to answer questions regarding health coverage on IRS Form 1040. Here’s how to use it:

If you find discrepancies, contact your employer for corrections.

If you haven't received your 1095-C form by early March, don't panic. First, check your email inbox and spam folder if you opted for electronic delivery. If you still can’t find it, reach out to your employer's HR or payroll department for assistance. They can confirm whether you were supposed to receive one and resend it if necessary.

The IRS 1095-C form is an important document used to report health insurance coverage. However, people often make mistakes while filling it out, leading to potential issues with the IRS. Understanding these common errors can help ensure that the form is completed correctly.

One frequent mistake is failing to provide accurate personal information. It’s essential to double-check your name, address, and Social Security number for accuracy. An incorrect detail can cause delays in processing or even result in penalties.

Another common oversight involves the section detailing the coverage offered. Individuals should carefully indicate whether they were enrolled in health coverage for the entire year or just part of it. Incomplete or incorrect information in this area can lead to confusion regarding eligibility for certain health care programs.

In some cases, people forget to fill out all required sections. Each box on the form has specific instructions, and omitting vital information can be problematic. It’s crucial to read each section carefully and ensure nothing is skipped.

It's also a mistake to overlook the deadlines. The IRS expects the 1095-C form to be submitted by a specific date each year. Late submissions can trigger unwanted attention or penalties, so it's vital to keep track of these deadlines.

Some individuals incorrectly assume that their employer will automatically submit the form on their behalf. While employers do provide the form, employees should verify they receive it and check for accuracy. Missing the form can create complications when filing taxes.

Another issue can arise from confusion about the codes used on the form. Certain codes indicate whether coverage was offered and if the employee enrolled in it. Misinterpreting these codes can lead to incorrect reporting of health coverage.

Finally, a mistake often made is not keeping a copy of the submitted form. Maintaining a record can be helpful in case the IRS requires further information or clarification about your health coverage. Being organized can prevent headaches down the line.

The IRS 1095-C form plays a crucial role in reporting health coverage offered by applicable large employers (ALEs). However, it is often accompanied by other forms and documents that provide additional context and necessary information for individuals, businesses, and tax professionals. Here are some important documents commonly associated with the 1095-C:

Understanding these documents can simplify tax filing processes and ensure compliance with health insurance reporting requirements. Each form plays a unique role, and having them readily available can prevent potential issues during tax season.

The IRS Form 1095-C is an important document related to health insurance coverage provided by certain employers. It helps individuals verify their health insurance status for tax purposes. Several other documents serve a similar purpose and provide crucial information regarding health insurance and coverage options. Below are four documents akin to the 1095-C form:

Understanding these documents in relation to the 1095-C can help clarify the health insurance landscape and ensure compliance with federal regulations. Being informed is crucial for making appropriate health care decisions and handling tax responsibilities effectively.

When filling out the IRS 1095-C form, accuracy and attention to detail are essential. The following list highlights ten important dos and don'ts to keep in mind.

The IRS Form 1095-C is often misunderstood, leading to confusion for many individuals. Below are some common misconceptions about this important document:

Many people believe that the 1095-C is a tax return that needs to be submitted during tax season. However, this form is not submitted with your tax return. Instead, it serves as a record of your health insurance coverage through your employer, specifically under the Affordable Care Act (ACA).

Some assume that only large employers, those with 50 or more full-time employees, are required to issue the 1095-C. While it is true that the requirement is primarily for these larger employers, some smaller businesses may also provide this form based on specific coverage circumstances. Therefore, it’s essential to know the details of your employer’s obligations.

Receiving this form does not guarantee that you are enrolled in health coverage. It simply reports what your employer offered you. You must actively enroll in the plan to have health insurance. Therefore, confirm your enrollment status separate from the information provided on the form.

Some individuals think that having a 1095-C form will directly influence the size of their tax refund. However, while this form does provide important information about your health coverage, it does not impact your refund amount. The crucial factor is whether you had qualifying health coverage for the entire year.

The IRS 1095-C form is essential for individuals and employers alike, particularly when dealing with health care coverage. Here are some key takeaways: