The IRS 12153 form plays a crucial role for taxpayers seeking to contest an IRS notice of intent to levy or to seize their assets. Designed specifically for those who want to request a Collection Due Process (CDP) hearing, this form allows individuals to present their case and potentially stop collection actions. It is essential for taxpayers to understand the timelines involved; submitting Form 12153 must be done within 30 days of receiving certain notices, such as the Notice of Federal Tax lien. The form requires key information, including personal details, the type of hearing requested, and the reason for the request, ensuring taxpayers have the opportunity to articulate their concerns. Completing this form accurately is vital, as errors may delay the hearing process or lead to unfavorable outcomes. Moreover, the IRS provides guidance on the associated rights and options available after filing, making it imperative to be fully aware of the implications before submitting the form. Understanding these aspects can empower taxpayers to navigate the complexities of tax collection processes effectively.

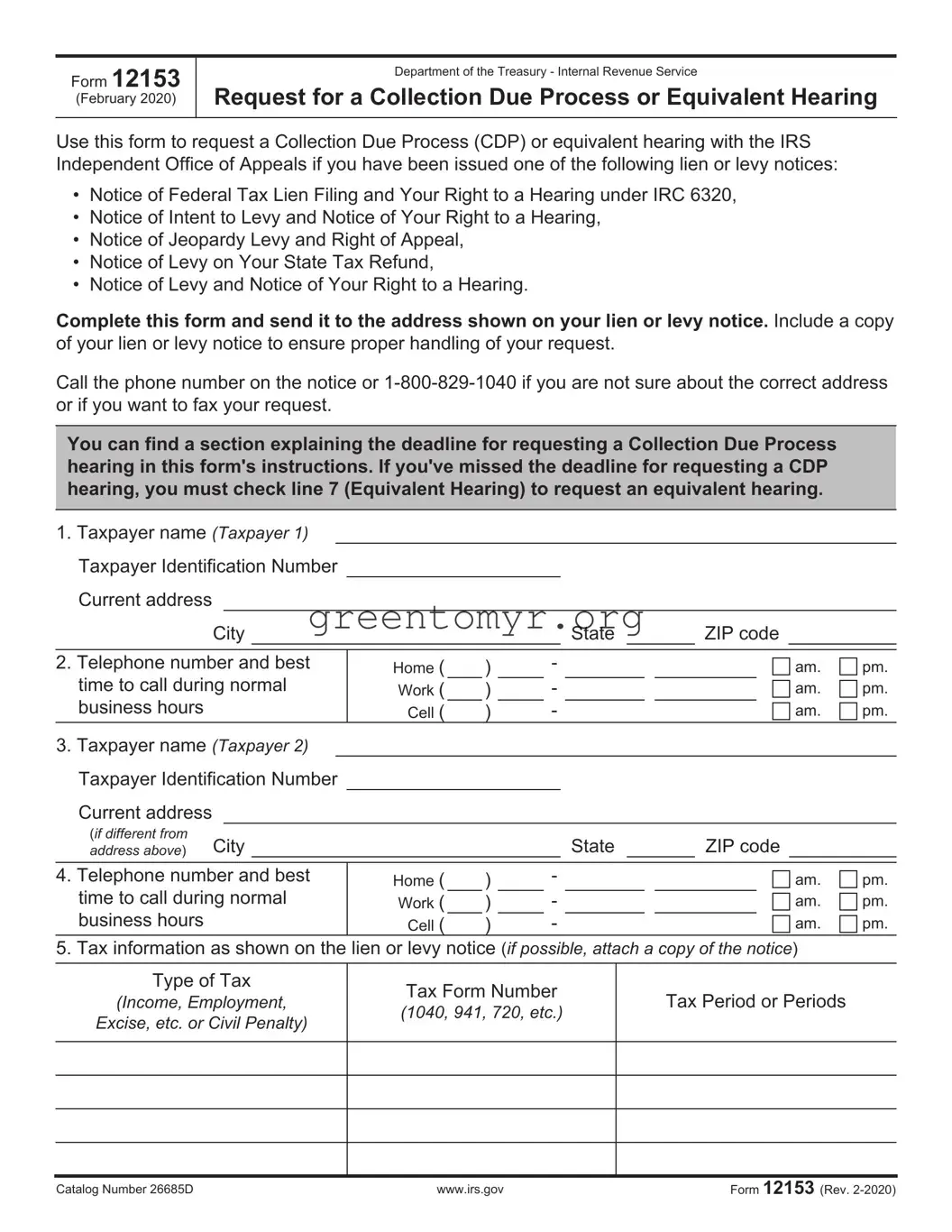

Form 12153

(February 2020)

Department of the Treasury - Internal Revenue Service

Request for a Collection Due Process or Equivalent Hearing

Use this form to request a Collection Due Process (CDP) or equivalent hearing with the IRS Independent Office of Appeals if you have been issued one of the following lien or levy notices:

•Notice of Federal Tax Lien Filing and Your Right to a Hearing under IRC 6320,

•Notice of Intent to Levy and Notice of Your Right to a Hearing,

•Notice of Jeopardy Levy and Right of Appeal,

•Notice of Levy on Your State Tax Refund,

•Notice of Levy and Notice of Your Right to a Hearing.

Complete this form and send it to the address shown on your lien or levy notice. Include a copy of your lien or levy notice to ensure proper handling of your request.

Call the phone number on the notice or

You can find a section explaining the deadline for requesting a Collection Due Process hearing in this form's instructions. If you've missed the deadline for requesting a CDP hearing, you must check line 7 (Equivalent Hearing) to request an equivalent hearing.

1.Taxpayer name (Taxpayer 1) Taxpayer Identification Number Current address

|

|

City |

|

|

|

|

|

|

State |

|

ZIP code |

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2. |

Telephone number and best |

Home ( |

) |

- |

|

|

|

|

|

|

|

am. |

pm. |

||||||

|

time to call during normal |

Work ( |

|

) |

|

- |

|

|

|

|

|

|

|

am. |

pm. |

||||

|

business hours |

|

|

|

|

Cell ( |

|

) |

|

- |

|

|

|

|

|

|

|

am. |

pm. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

3. |

Taxpayer name (Taxpayer 2) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

Taxpayer Identification Number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Current address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(if different from |

City |

|

|

|

|

|

|

State |

|

ZIP code |

|

|||||||

|

address above) |

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4. |

Telephone number and best |

Home ( |

) |

- |

|

|

|

|

|

|

|

am. |

pm. |

||||||

|

time to call during normal |

Work ( |

|

) |

|

- |

|

|

|

|

|

|

|

am. |

pm. |

||||

|

business hours |

|

|

|

|

Cell ( |

|

) |

|

- |

|

|

|

|

|

|

|

am. |

pm. |

|

|

|

|

|

|

|

|

|

|

|

|||||||||

5. |

Tax information as shown on the |

lien or levy notice (if possible, attach a copy of the notice) |

|

||||||||||||||||

Type of Tax

(Income, Employment,

Excise, etc. or Civil Penalty)

Tax Form Number

(1040, 941, 720, etc.)

Tax Period or Periods

Catalog Number 26685D |

www.irs.gov |

Form 12153 (Rev. |

Page 2

6.Basis for hearing request (both boxes can be checked if you have received both a lien and levy notice)

Filed Notice of Federal Tax Lien |

Proposed Levy or Actual Levy |

7.Equivalent Hearing (see the instructions for more information on Equivalent Hearings)

I would like an Equivalent Hearing - I would like a hearing equivalent to a CDP Hearing if my request for a CDP hearing does not meet the requirements for a timely CDP Hearing.

8.Check the most appropriate box for the reason you disagree with the filing of the lien or the levy. See page 4 of this form for examples. You can add more pages if you don't have enough space.

If, during your CDP Hearing, you think you would like to discuss a Collection Alternative to the action proposed by the Collection function it is recommended you submit a completed Form 433A (Individual) and/or Form 433B (Business), as appropriate, with this form. See www.irs.gov for copies of the forms. Generally, the IRS Independent Office of Appeals will ask the Collection Function to review, verify and provide their opinion on any new information you submit. We will share their comments with you and give you the opportunity to respond.

Collection alternative |

Installment Agreement |

Offer in Compromise |

I Cannot Pay Balance |

Lien |

Subordination |

Discharge |

Withdrawal |

Explain |

|

|

|

My spouse is responsible  Innocent Spouse Relief (attach Form 8857, Request for Innocent Spouse

Innocent Spouse Relief (attach Form 8857, Request for Innocent Spouse

Relief, to your request)

Other (for examples, see page 4)

Reason (you must provide a reason for the dispute or your request for a CDP hearing will not be honored. Use as much space as you need to explain the reason for your request. Attach extra pages if necessary)

9. Signatures

I understand the CDP hearing and any subsequent judicial review will suspend the statutory period of limitations for collection action. I also understand my representative or I must sign and date this request before the IRS Independent Office of Appeals can accept it. If you are signing as an officer of a company, add your title (president, secretary, etc.) behind your signature.

SIGN HERE |

Taxpayer 1's signature |

Date

Taxpayer 2's signature (if a joint request, both must sign)

Date

I request my CDP hearing be held with my authorized representative (attach a copy of Form 2848)

Authorized Representative's signature |

Authorized Representative's name |

Telephone number |

|

|

|

IRS Use Only

IRS employee (print) |

Employee telephone number |

IRS received date |

|

|

|

Catalog Number 26685D |

www.irs.gov |

Form 12153 (Rev. |

Page 3

Information You Need To Know When Requesting A Collection Due Process Hearing

What Is the Deadline for Requesting a Timely Collection Due Process (CDP) Hearing?

•Your request for a CDP hearing about a Federal Tax Lien filing must be postmarked by the date indicated in the Notice of Federal Tax Lien Filing and Your Right to a Hearing under IRC 6320 (lien notice).

•Your request for a CDP hearing about a levy must be postmarked within 30 days after the date of the Notice of Intent to Levy and Notice of Your Right to a Hearing (levy notice) or Notice of Your Right to a Hearing After an Actual Levy.

Your timely request for a CDP hearing will prohibit levy action in most cases. A timely request for CDP hearing will also suspend the

You can go to court to appeal the CDP determination the IRS Independent Office of Appeals makes about your disagreement.

What Is an Equivalent Hearing?

If you still want a hearing with the IRS Independent Office of Appeals after the deadline for requesting a timely CDP hearing has passed, you can use this form to request an equivalent hearing. You must check the Equivalent Hearing box on line 7 of the form to request an equivalent hearing. An equivalent hearing request does not prohibit levy or suspend the

•Lien

•Levy

•Your request for a CDP levy hearing, whether timely or Equivalent, does not prohibit the Service from filing a Notice of Federal Tax Lien.

Where Should You File Your CDP or Equivalent Hearing Request?

File your request by mail at the address on your lien notice or levy notice. You may also fax your request. Call the telephone number on the lien or levy notice to ask for the fax number. Do not send your CDP or equivalent hearing request directly to the IRS Independent Office of Appeals, it must be sent to the address on the lien or levy notice. If you send your request directly to Appeals it may result in your request not being considered a timely request. Depending upon your issue the originating function may contact you in an attempt to resolve the issue(s) raised in your request prior to forwarding your request to Appeals.

Where Can You Get Help?

You can call the telephone number on the lien or levy notice with your questions about requesting a hearing. The contact person listed on the notice or other representative can access your tax information and answer your questions.

In addition, you may qualify for representation by a

If you are experiencing economic harm, the Taxpayer Advocate Service (TAS) may be able to help you resolve your problems with the IRS. TAS cannot extend the time you have to request a CDP or equivalent hearing. See Publication 594, The IRS Collection Process, or visit

You can get copies of tax forms, schedules, instructions, publications, and notices at www.irs.gov, at your local IRS office, or by calling

Catalog Number 26685D |

www.irs.gov |

Form 12153 (Rev. |

Page 4

What Are Examples of Reasons for Requesting a Hearing?

You will have to explain your reason for requesting a hearing when you make your request. Below are examples of reasons for requesting a hearing.

You want a collection alternative— “I would like to propose a different way to pay the money I owe.” Common collection alternatives include:

•Full

•Installment

•Offer in

“I cannot pay my taxes.” Some possible reasons why you cannot pay your taxes are: (1) you have a terminal illness or excessive medical bills; (2) your only source of income is Social Security payments, welfare payments, or unemployment benefit payments; (3) you are unemployed with little or no income; (4) you have reasonable expenses exceeding your income; or (5) you have some other hardship condition. The IRS Independent Office of Appeals may consider freezing collection action until your circumstances improve. Penalty and interest will continue to accrue on the unpaid balance.

You want action taken about the filing of the tax lien against your

When you request lien subordination, you are asking the IRS to make a Federal Tax Lien secondary to a

When you request a lien discharge, you are asking the IRS to remove a Federal Tax Lien from a specific property. For example, you may ask for a discharge of the Federal Tax Lien in order to sell your house if you use all of the sale proceeds to pay your taxes even though the sale proceeds will not fully pay all of the tax you owe.

When you request a lien withdrawal, you are asking the IRS to remove the Notice of Federal Tax Lien (NFTL) information from public records because you believe the NFTL should not have been filed. For example, you may ask for a withdrawal of the filing of the NFTL if you believe the IRS filed the NFTL prematurely or did not follow procedures, or you have entered into an installment agreement and the installment agreement does not provide for the filing of the NFTL. A withdrawal does not remove the lien from your IRS records.

Your spouse is

Other

“I do not believe I should be responsible for penalties.” The IRS Independent Office of Appeals may remove all or part of the penalties if you have a reasonable cause for not paying or not filing on time. See Notice 746, Information About Your Notice, Penalty and Interest for what is reasonable cause for removing penalties.

“I have already paid all or part of my taxes.” You disagree with the amount the IRS says you haven't paid if you think you have not received credit for payments you have already made.

See Publication 594, The IRS Collection Process, for more information on the following topics: Installment Agreements and Offers in Compromise; Lien Subordination, Discharge, and Withdrawal; Innocent Spouse Relief; Temporarily Delay Collection; and belief that tax bill is wrong.

Catalog Number 26685D |

www.irs.gov |

Form 12153 (Rev. |

| Fact Name | Details |

|---|---|

| Purpose | The IRS Form 12153 is used to request a collection due process hearing. |

| Eligibility | Taxpayers can file this form if they receive a notice of federal tax lien or a notice of levy. |

| Submission Deadline | The form must be submitted within 30 days of receiving the notice to maintain the right to a hearing. |

| Where to Submit | The completed form should be sent to the address listed on the notice received. |

| Impact | Submitting Form 12153 can temporarily halt collection actions until the hearing is resolved. |

| Related Code | This form is governed under Section 6320 of the Internal Revenue Code. |

| Decision Timeline | The IRS will generally issue a determination within 45 days of the hearing request. |

Completing the IRS Form 12153 is a vital step when seeking to appeal a tax decision made by the IRS. After filling out the form, it will be submitted to the appropriate IRS office for consideration. Follow these straightforward steps to ensure your form is completed accurately.

The IRS Form 12153, also known as the Request for a Collection Due Process or Equivalent Hearing, allows taxpayers to request a hearing when the IRS intends to levy their assets or garnish wages. This form is a critical tool for those wishing to challenge the IRS's actions regarding their tax debts. By filling out this form, taxpayers can ensure they have a chance to discuss their situation with an IRS representative before collection actions proceed.

If you have received a final notice of intent to levy (often called a "Notice of Intent to Levy and Notice of Your Right to a Hearing"), you should file Form 12153. This form is relevant for individuals facing collections, as well as businesses that might have tax liabilities. Essentially, anyone whose taxes are being actively pursued through collection efforts should consider this form as a means to present their case.

When filling out Form 12153, you will need to provide several pieces of information, including:

Completing this form accurately is vital to ensure that your request is processed smoothly and efficiently.

After you submit Form 12153, the IRS will schedule a hearing, typically conducted by an Appeals Officer. You may discuss your case, present any supporting documentation, and explain your reasons for disputing the levy. The officer will review the information presented and make an impartial decision regarding your case. This hearing can be held by phone or in person, depending on the specifics of your situation and your preference.

Filing Form 12153 must occur within 30 days of receiving the final notice of intent to levy. If you miss this deadline, the IRS may proceed with the levy, and you'll lose your right to a hearing. However, in certain cases, you might still have other options available, such as appealing or seeking an Offer in Compromise, although these can involve more complex procedures. It's advisable to act quickly if you miss the deadline to understand what other alternatives may be available to you.

You absolutely can represent yourself when filing Form 12153 and during the hearings. However, many taxpayers choose to work with a tax professional, such as a CPA or tax attorney, who can provide guidance and support. If you feel unsure about the process or how to effectively argue your case, seeking professional assistance can be immensely beneficial in navigating the complexities of tax law.

Completing the IRS Form 12153, commonly known as the Request for a Collection Due Process or Equivalent Hearing, can be a crucial step in addressing disputes with the IRS. Many individuals make mistakes during this process, which can hinder their ability to resolve tax-related issues effectively. Understanding these common errors can facilitate a smoother submission process.

One common mistake is neglecting to provide complete and accurate personal information. Taxpayers must ensure that their name, address, and Social Security number are correct. Any discrepancies can delay the processing of the request or lead to miscommunication with the IRS.

Another frequent error is failing to clearly specify the type of hearing requested. The form allows for different types of hearings, and the request for a Collection Due Process hearing must be explicitly indicated. Omitting this detail can result in the IRS treating the request as a general inquiry rather than taking the necessary actions.

Taxpayers often overlook the importance of checking all applicable boxes on the form. Each section pertains to specific rights and appeals. Ignoring certain sections might imply the taxpayer is forfeiting those rights or not fully understanding their situation, which can significantly impact their case.

Inadequate justification for requesting the hearing also poses a problem. Providing detailed explanations of the reasons behind the appeal is crucial. Without clarity and support for one's position, the IRS may deny the request or dismiss it outright.

Many people fail to include the required supporting documentation with their Form 12153 submission. Supporting documents help validate claims and provide essential context. The absence of these materials can weaken a taxpayer's case or lead to delays.

Missing deadlines represents another critical mistake. Form 12153 must be submitted within specific timeframes following certain IRS notices. Failure to meet these deadlines can result in losing the right to appeal or worse, facing immediate collection actions.

Lastly, neglecting to retain copies of submitted forms can have long-term implications. Keeping a record of all correspondence with the IRS is vital for future reference and potential follow-ups. Without a record, taxpayers may find it challenging to track their case or reference prior communications.

The IRS 12153 form, also known as the Request for a Collection Due Process or Equivalent Hearing, is often used by taxpayers facing tax collection actions. Understanding other relevant documents can streamline the process and help in effectively managing tax-related issues. Here are five forms and documents commonly associated with the IRS 12153 form.

Familiarity with these forms can be beneficial for anyone dealing with IRS collection actions. Knowing what documents may be needed or helpful can empower taxpayers in navigating the complex realities of tax administration and compliance.

The IRS Form 12153 is a Request for a Collection Due Process or Equivalent Hearing. This form allows taxpayers to appeal certain IRS collection actions. While it has its specific purpose, there are several other IRS documents that share similarities in function or intention.

These forms all facilitate communication and help taxpayers manage their tax obligations by appealing decisions or correcting errors. Understanding these similarities can help individuals navigate their options effectively.

Filling out IRS Form 12153 can seem daunting, but taking the right steps can make the process smoother. Here’s a list of five things to do and five things to avoid when completing this important form.

By following these do's and don'ts, you can improve your chances of a favorable outcome in your IRS dealings.

There are several misconceptions about the IRS Form 12153, which is used to request a collection due process hearing. Clarifying these misunderstandings can help taxpayers navigate the process more easily.

In reality, anyone facing IRS collection actions can use Form 12153, regardless of their financial situation.

While the form requests a hearing, it does not automatically halt collection activities. Taxpayers should be aware of what happens after submission.

Taxpayers can file Form 12153 on their own. However, seeking help can be beneficial for complex situations.

The IRS does have time limits, but these can vary. It is crucial to verify the specific deadlines for each situation.

Not every request for a hearing will be granted. The IRS reviews each case before making a decision.

While it may seem straightforward, the process can take time and requires careful attention to detail.

The IRS Form 12153 is essential when requesting a hearing regarding a tax issue. Here are eight key takeaways about filling out and using this form: