The IRS 1310 form plays a crucial role in the complex landscape of tax filings, particularly when it comes to addressing the financial matters of a deceased person. Essential for ensuring that the rightful beneficiaries receive the tax refund owed to the departed individual, this form serves as a declaration of the taxpayer's death and establishes the right of the person claiming the refund. Typically used by a surviving spouse or an executor of the estate, the IRS 1310 form requires specific information, such as the decedent’s name, Social Security number, and date of death. In addition, it helps ease the process by clarifying the status of the beneficiary, allowing for the smooth transfer of potential refunds. Understanding how to accurately complete this form is vital, as any mistakes could delay the process or even prevent the refund from being issued altogether. Proper documentation, including proof of death, may also need to be submitted alongside the form, making it essential for claimants to gather the necessary materials ahead of time.

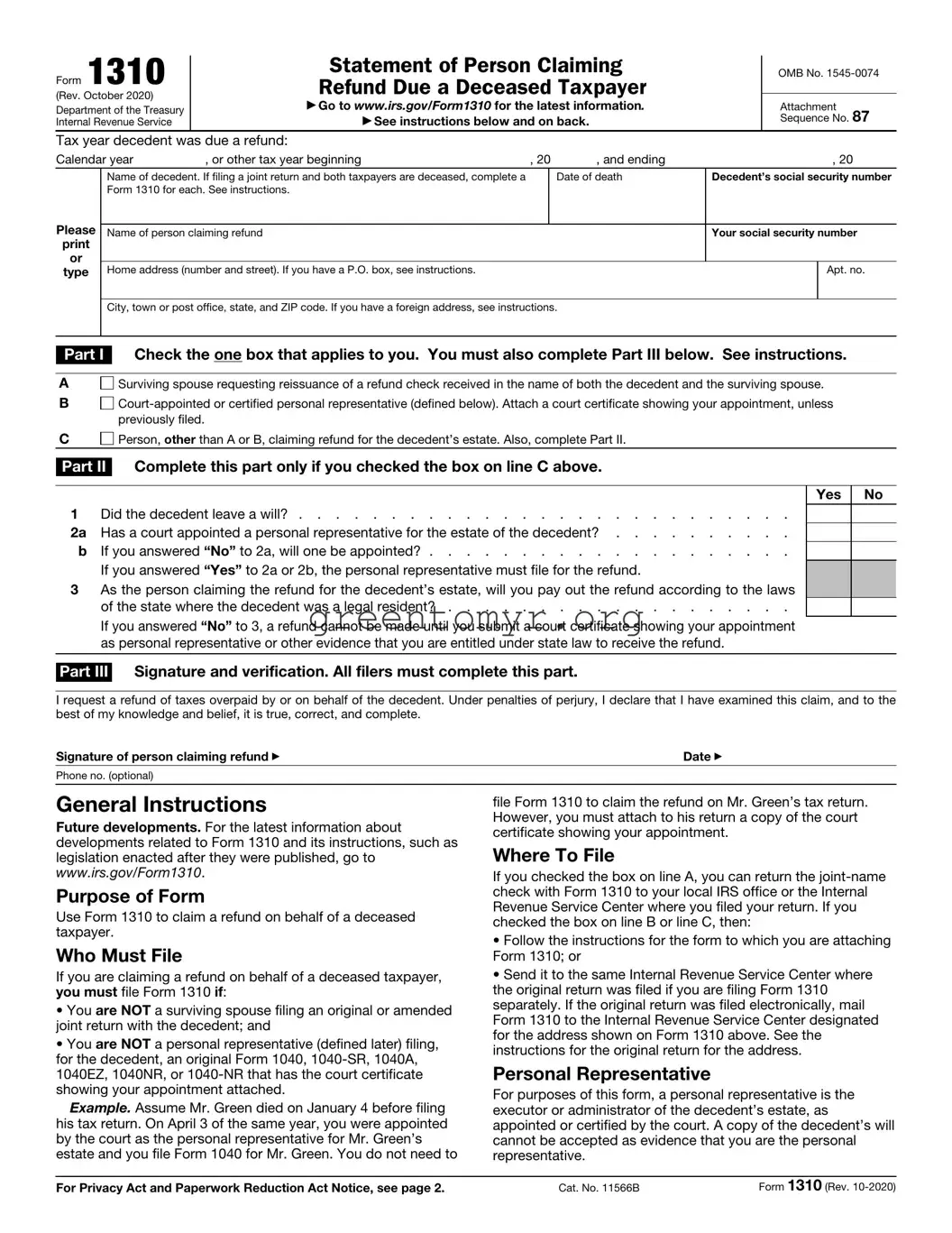

Form 1310

(Rev. October 2020)

Department of the Treasury

Internal Revenue Service

Statement of Person Claiming Refund Due a Deceased Taxpayer

▶Go to www.irs.gov/Form1310 for the latest information.

▶See instructions below and on back.

OMB No.

Attachment Sequence No. 87

Tax year decedent was due a refund:

Calendar year |

, or other tax year beginning |

, 20 |

, and ending |

, 20 |

Please

or

type

Name of decedent. If filing a joint return and both taxpayers are deceased, complete a |

Date of death |

Decedent’s social security number |

|

Form 1310 for each. See instructions. |

|

|

|

|

|

|

|

Name of person claiming refund |

|

Your social security number |

|

|

|

|

|

Home address (number and street). If you have a P.O. box, see instructions. |

|

|

Apt. no. |

|

|

|

|

City, town or post office, state, and ZIP code. If you have a foreign address, see instructions.

Part I Check the one box that applies to you. You must also complete Part III below. See instructions.

A |

Surviving spouse requesting reissuance of a refund check received in the name of both the decedent and the surviving spouse. |

B

C Person, other than A or B, claiming refund for the decedent’s estate. Also, complete Part II.

Person, other than A or B, claiming refund for the decedent’s estate. Also, complete Part II.

Part II Complete this part only if you checked the box on line C above.

1 |

Did the decedent leave a will? |

2a |

Has a court appointed a personal representative for the estate of the decedent? |

b |

If you answered “No” to 2a, will one be appointed? |

|

If you answered “Yes” to 2a or 2b, the personal representative must file for the refund. |

3As the person claiming the refund for the decedent’s estate, will you pay out the refund according to the laws

of the state where the decedent was a legal resident? . . . . . . . . . . . . . . . . . . .

If you answered “No” to 3, a refund cannot be made until you submit a court certificate showing your appointment as personal representative or other evidence that you are entitled under state law to receive the refund.

Yes

No

Part III Signature and verification. All filers must complete this part.

I request a refund of taxes overpaid by or on behalf of the decedent. Under penalties of perjury, I declare that I have examined this claim, and to the best of my knowledge and belief, it is true, correct, and complete.

Signature of person claiming refund ▶ |

Date ▶ |

Phone no. (optional)

General Instructions

Future developments. For the latest information about developments related to Form 1310 and its instructions, such as legislation enacted after they were published, go to www.irs.gov/Form1310.

Purpose of Form

Use Form 1310 to claim a refund on behalf of a deceased taxpayer.

Who Must File

If you are claiming a refund on behalf of a deceased taxpayer, you must file Form 1310 if:

•You are NOT a surviving spouse filing an original or amended joint return with the decedent; and

•You are NOT a personal representative (defined later) filing, for the decedent, an original Form 1040,

Example. Assume Mr. Green died on January 4 before filing his tax return. On April 3 of the same year, you were appointed by the court as the personal representative for Mr. Green’s estate and you file Form 1040 for Mr. Green. You do not need to

file Form 1310 to claim the refund on Mr. Green’s tax return. However, you must attach to his return a copy of the court certificate showing your appointment.

Where To File

If you checked the box on line A, you can return the

•Follow the instructions for the form to which you are attaching Form 1310; or

•Send it to the same Internal Revenue Service Center where the original return was filed if you are filing Form 1310 separately. If the original return was filed electronically, mail Form 1310 to the Internal Revenue Service Center designated for the address shown on Form 1310 above. See the instructions for the original return for the address.

Personal Representative

For purposes of this form, a personal representative is the executor or administrator of the decedent’s estate, as appointed or certified by the court. A copy of the decedent’s will cannot be accepted as evidence that you are the personal representative.

For Privacy Act and Paperwork Reduction Act Notice, see page 2. |

Cat. No. 11566B |

Form 1310 (Rev. |

Form 1310 (Rev. |

Page 2 |

Additional Information

For more details, see Death of a Taxpayer in the instructions for your return, or get Pub. 559, Survivors, Executors, and Administrators.

Specific Instructions

Name of Decedent

If you are filing a joint return for spouses who are both deceased and you are required to file Form 1310 (see Who Must File, earlier), you must do the following.

•Complete a separate Form 1310 for each spouse.

•Attach both of these completed Forms 1310 to the return.

Note: If a refund is due, following these steps will assist in the timely release of the refund.

P.O. Box

Enter your box number only if your post office does not deliver mail to your home.

Foreign Address

If your address is outside the United States or its possessions or territories, enter the information in the following order: city, province or state, and country. Follow the country’s practice for entering the postal code. Do not abbreviate the country name.

Line A

Check the box on line A only if you received a refund check in your name and your deceased spouse’s name. You can return the

Line B

Check the box on line B only if you are the decedent’s court- appointed or certified personal representative claiming a refund for the decedent on Form 1040X

Line C

Check the box on line C if you are not a surviving spouse requesting reissuance of a refund check received in your name and your deceased spouse’s name and if there is not a court- appointed or certified personal representative. You must also complete Part II. If you check the box on line C, you must have proof of death.

The proof of death is a copy of either of the following.

•The death certificate.

•The formal notification from the appropriate government office (for example, Department of Defense) informing the next of kin of the decedent’s death.

Do not attach the death certificate or other proof of death to Form 1310. Instead, keep it for your records and provide it if requested.

Example. Your father died on August 25. You are his sole survivor. Your father did not have a will and the court did not appoint a personal representative for his estate. Your father is entitled to a $300 refund. To get the refund, you must complete and attach Form 1310 to your father’s final return. You should check the box on Form 1310, line C; answer all the questions in Part II; and sign your name in Part III. You must also keep a copy of the death certificate or other proof of death for your records.

Lines

If you checked the box on line C, you must complete lines 1 through 3.

Privacy Act and Paperwork Reduction Act Notice

We ask for the information on this form to carry out the Internal Revenue laws of the United States. This information will be used to determine your eligibility pursuant to Internal Revenue Code section 6012 to claim the refund due the decedent. Code section 6109 requires you to provide your social security number and that of the decedent. You are not required to claim the refund due the decedent, but if you do so, you must provide the information requested on this form. Failure to provide this information may delay or prevent processing of your claim. Providing false or fraudulent information may subject you to penalties. Routine uses of this information include providing it to the Department of Justice for use in civil and criminal litigation, to the Social Security Administration for the administration of Social Security programs, and to cities, states, the District of Columbia, and U.S. commonwealths and possessions for use in administering their tax laws. We may also disclose this information to other countries under a tax treaty, to federal and state agencies to enforce federal nontax criminal laws, or to federal law enforcement and intelligence agencies to combat terrorism. You do not have to provide your phone number.

You are not required to provide the information requested on a form unless the form displays a valid OMB control number. Books or records relating to a form or its instructions must be retained as long as their contents may become material in the administration of any Internal Revenue law. Generally, tax returns and return information are confidential, as required by Code section 6103.

The average time and expenses required to complete and file this form will vary depending on individual circumstances. For the estimated averages, see the instructions for your income tax return.

If you have suggestions for making this form simpler, we would be happy to hear from you. See the instructions for your income tax return.

| Fact Name | Description |

|---|---|

| Purpose of Form | The IRS Form 1310, also known as the Statement of Person Claiming Refund Due a Deceased Taxpayer, is used to claim a tax refund on behalf of a deceased person. |

| Eligibility | You can use this form if you are the spouse, child, or legal representative of the deceased taxpayer who is entitled to a tax refund for a tax year. |

| Filing Requirement | Form 1310 must be filed along with the deceased person’s final tax return to claim any refund due. |

| Documentation Needed | When submitting this form, you may need to provide additional documentation, such as a death certificate or proof of relationship to the deceased taxpayer. |

| Submission Instructions | Send Form 1310 along with the final tax return to the address specified in the filing instructions for that return, ensuring all forms are accurate and complete. |

Completing the IRS Form 1310 is an important task if you're dealing with a deceased person’s tax matters. This form ensures that the rightful person receives any refund due to the decedent. Follow these steps carefully to ensure that the process runs smoothly.

After submitting the form and the associated documents, monitor your tax account for any updates. The IRS may take some time to process your claim, so be patient. Ensure that you keep copies of everything you send for your records.

IRS Form 1310 is used when claiming a refund on behalf of a deceased taxpayer. If someone passed away and is entitled to a tax refund, the surviving spouse, personal representative, or another authorized individual can file this form. Its primary purpose is to ensure that any refund owed to the deceased can be correctly and legally claimed by the appropriate party.

The form should be filed by individuals who are entitled to claim a tax refund on behalf of a deceased taxpayer. This includes:

If you're in one of these positions, submitting Form 1310 along with the deceased taxpayer's tax return will help facilitate the refund process.

When filling out Form 1310, you will need to provide various pieces of information, including:

Ensure all information is accurate for a smooth and expedient processing of the refund.

Where to send Form 1310 depends on how the tax return of the deceased is filed. If you're mailing a paper return, you generally send it to the address listed in the instructions provided with the tax forms for the respective tax year. If you're filing electronically, the system may automatically process the form. Always check the IRS website or the instructions for the most current mailing addresses to avoid any delays.

Filling out the IRS 1310 form can be a straightforward process, but many people inadvertently make mistakes that can delay their refunds or complicate their tax situation. One common error is forgetting to sign the form. When it comes to formal documents, a signature is crucial. Without it, the IRS might reject the form, resulting in unnecessary delays.

Another mistake often seen is incorrect personal information. The IRS requires specific details like the name and Social Security number of the deceased taxpayer. If these are entered incorrectly, it can lead to confusion and potential rejections. Always double-check the details before submitting.

Many individuals also fail to complete the section concerning the relationship to the deceased. This part is essential for establishing the validity of the claim. An omission or an inaccurate description could raise questions about your authority to file the claim.

It's also not uncommon for people to overlook the need for additional documentation. Depending on the situation, you may need to include the death certificate or other official documents. Skipping this step can stall the processing of your form.

Another frequent mistake is misunderstanding the filing requirements. Some assume that they can submit the IRS 1310 form only when they are due a refund. In reality, there are specific instances when this form is necessary, regardless of whether a refund is expected.

Lastly, timing plays a crucial role in the overall success of your filing. Submitting the form late can hinder the refund process. Ensure the IRS 1310 form is filed in a timely manner to avoid potential issues. Taking a little extra time to review and verify your submissions can save you headaches down the road.

The IRS Form 1310 is used to claim a refund on behalf of a deceased taxpayer. When filing this form, there are other documents that may be necessary to support the claim. The following is a list of forms and documents that are often used alongside IRS Form 1310.

By preparing these documents along with the IRS Form 1310, the process of claiming a tax refund can be done more smoothly. Proper organization of these forms can help alleviate some of the stress during an already challenging time.

IRS Form 4506: This form requests a copy of a tax return. Similar to Form 1310, it involves submitting information regarding taxes, but it is used to obtain prior tax records rather than for claiming an estate refund.

IRS Form 1040: The standard individual income tax return. Like Form 1310, it deals with the tax responsibilities of individuals, but it’s focused on reporting current income rather than dealing with refunds from deceased taxpayer estates.

IRS Form 4868: This form requests an automatic extension of time to file a tax return. It is similar in that it involves submitting specific information to the IRS; however, it is not related to estate matters.

IRS Form W-2: This shows wages and tax withheld for employees. While it provides details about income, it does not address claims regarding a deceased taxpayer, distinguishing it from Form 1310.

IRS Form 1041: This is the income tax return for estates and trusts. It’s similar because it relates to taxation after death, but it specifically deals with the income generated by the estate rather than claiming refunds for the deceased taxpayer.

IRS Form 8821: This grants power of attorney for tax matters. Similar to Form 1310, both involve representation in front of the IRS; however, Form 8821 is a contract rather than a claim for refund.

IRS Form 709: This is used to report gifts and calculate gift tax. It is similar as it pertains to tax obligations, but it focuses on gifting rather than refunds after death.

IRS Form 1099: This form reports various types of income other than wages. It shares a common theme of tax reporting with Form 1310 but does not specifically address issues related to deceased taxpayers.

IRS Form 4506-T: This is a request for a transcript of a tax return. Like Form 1310, it involves tax records, but it is used to obtain summaries rather than claims for refunds.

IRS Form 1040-X: This is used for amending a tax return. While it shares the aspect of revising tax information, it is geared toward correcting existing returns rather than addressing a deceased person's refund.

When filling out the IRS 1310 form, it is crucial to approach this task with care. Here are some important dos and don’ts to consider:

The IRS Form 1310, also known as the Statement of Person Claiming Refund Due a Deceased Taxpayer, is often surrounded by misunderstandings. Here are ten common misconceptions about this form, along with explanations to clarify each one.

Understanding these misconceptions can aid in navigating the process related to Form 1310 more effectively. It is always advisable to consult with a tax professional if there are any questions or uncertainties regarding specific situations.

Filling out and using the IRS Form 1310 is important when dealing with the estate of a deceased person. Here are some key takeaways: