The IRS Form 2210 is an important document for tax filers who may not have paid enough taxes throughout the year. Understanding the implications of underpayment can help individuals avoid unnecessary penalties. The form allows taxpayers to calculate their required annual payment, examining if they have met the thresholds set by the IRS. It is particularly useful for those who have non-wage income or who may not receive taxes withheld from their earnings. By submitting Form 2210, filers can demonstrate their reliance on safe harbor provisions to avoid penalties or, alternatively, calculate their actual underpayment amount due. Thus, it serves as both a shield against penalties and a way to ensure compliance with tax obligations. Knowing when and how to fill out this form can help you maintain good standing with the IRS and manage your tax responsibilities effectively.

Form 2210 |

|

Underpayment of Estimated Tax by |

|

OMB No. |

|

|

Individuals, Estates, and Trusts |

|

2019 |

||

Department of the Treasury |

|

Go to www.irs.gov/Form2210 for instructions and the latest information. |

|

||

|

|

|

|

Attachment |

|

Internal Revenue Service |

|

Attach to Form 1040, |

|

Sequence No. 06 |

|

Name(s) shown on tax return |

|

|

Identifying number |

||

|

|

|

|

|

|

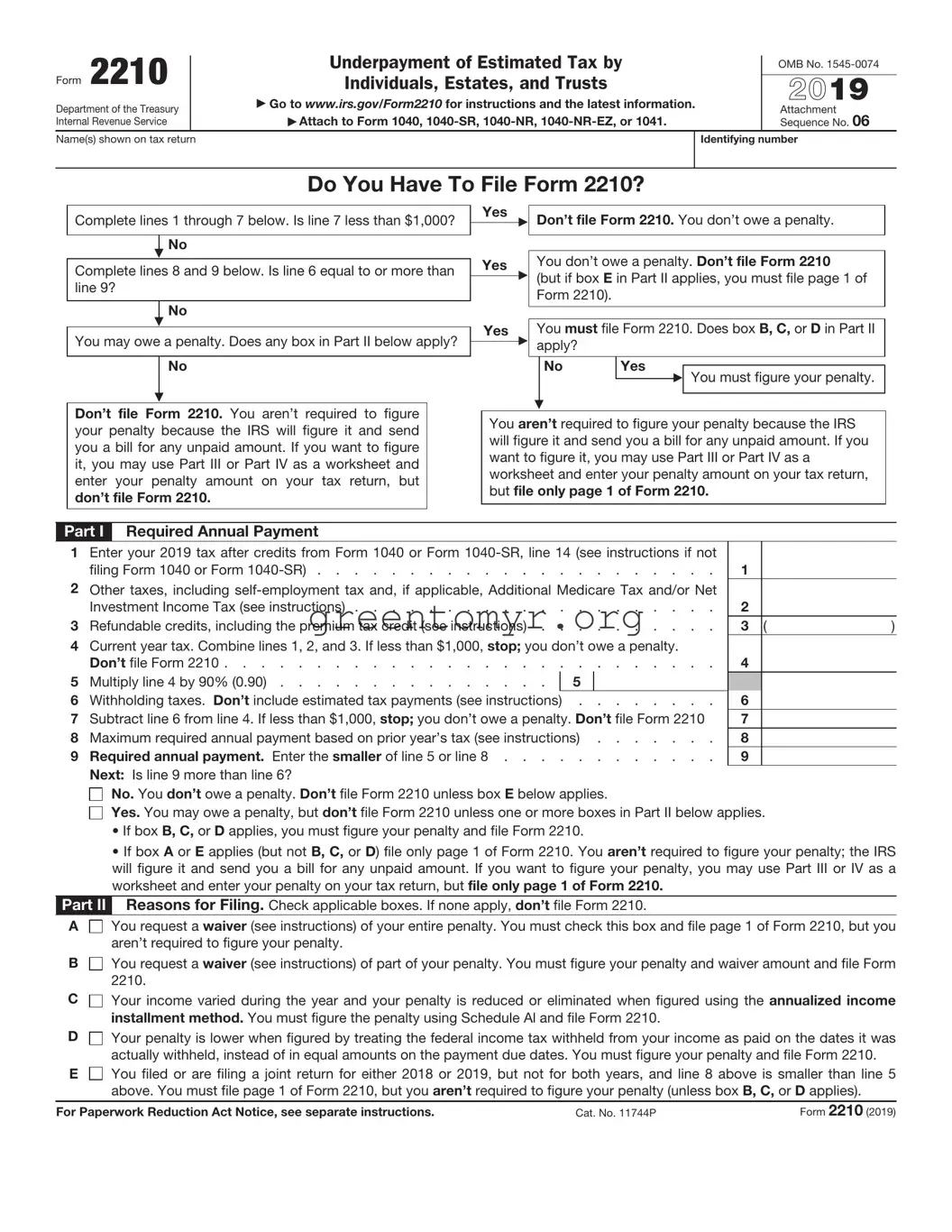

Do You Have To File Form 2210?

Complete lines 1 through 7 below. Is line 7 less than $1,000?

No

Complete lines 8 and 9 below. Is line 6 equal to or more than line 9?

No

You may owe a penalty. Does any box in Part II below apply?

No

Don’t file Form 2210. You aren’t required to figure your penalty because the IRS will figure it and send you a bill for any unpaid amount. If you want to figure it, you may use Part III or Part IV as a worksheet and enter your penalty amount on your tax return, but don’t file Form 2210.

Yes |

Don’t file Form 2210. You don’t owe a penalty. |

|

|

Yes |

|

You don’t owe a penalty. Don’t file Form 2210 |

|||||

|

|

|||||||

|

|

|

|

(but if box E in Part II applies, you must file page 1 of |

||||

|

|

|

|

|||||

|

|

|

|

Form 2210). |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Yes |

|

You must file Form 2210. Does box B, C, or D in Part II |

|||||

|

||||||||

|

|

|

|

apply? |

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

No |

Yes |

|

|

|

|

|

|

|

You must figure your penalty. |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

You aren’t required to figure your penalty because the IRS will figure it and send you a bill for any unpaid amount. If you want to figure it, you may use Part III or Part IV as a worksheet and enter your penalty amount on your tax return, but file only page 1 of Form 2210.

Part I Required Annual Payment

1Enter your 2019 tax after credits from Form 1040 or Form

filing Form 1040 or Form |

1 |

2Other taxes, including

Investment Income Tax (see instructions) |

2 |

|

|

3 Refundable credits, including the premium tax credit (see instructions) |

3 |

( |

) |

4Current year tax. Combine lines 1, 2, and 3. If less than $1,000, stop; you don’t owe a penalty.

|

Don’t file Form 2210 |

4 |

|

||

5 |

Multiply line 4 by 90% (0.90) |

5 |

|

|

|

6 |

Withholding taxes. Don’t include estimated tax payments (see instructions) |

6 |

|

||

7 |

Subtract line 6 from line 4. If less than $1,000, stop; you don’t owe a penalty. Don’t file Form 2210 |

7 |

|

||

8 |

Maximum required annual payment based on prior year’s tax (see instructions) |

8 |

|

||

9 |

Required annual payment. Enter the smaller of line 5 or line 8 |

9 |

|

||

|

Next: Is line 9 more than line 6? |

|

|

|

|

|

No. You don’t owe a penalty. Don’t file Form 2210 unless box E below applies. |

|

|

||

|

Yes. You may owe a penalty, but don’t file Form 2210 unless one or more boxes in Part II below applies. |

||||

•If box B, C, or D applies, you must figure your penalty and file Form 2210.

•If box A or E applies (but not B, C, or D) file only page 1 of Form 2210. You aren’t required to figure your penalty; the IRS will figure it and send you a bill for any unpaid amount. If you want to figure your penalty, you may use Part III or IV as a worksheet and enter your penalty on your tax return, but file only page 1 of Form 2210.

Part II Reasons for Filing. Check applicable boxes. If none apply, don’t file Form 2210.

A

You request a waiver (see instructions) of your entire penalty. You must check this box and file page 1 of Form 2210, but you aren’t required to figure your penalty.

You request a waiver (see instructions) of your entire penalty. You must check this box and file page 1 of Form 2210, but you aren’t required to figure your penalty.

B

You request a waiver (see instructions) of part of your penalty. You must figure your penalty and waiver amount and file Form 2210.

You request a waiver (see instructions) of part of your penalty. You must figure your penalty and waiver amount and file Form 2210.

C

Your income varied during the year and your penalty is reduced or eliminated when figured using the annualized income installment method. You must figure the penalty using Schedule Al and file Form 2210.

Your income varied during the year and your penalty is reduced or eliminated when figured using the annualized income installment method. You must figure the penalty using Schedule Al and file Form 2210.

D

Your penalty is lower when figured by treating the federal income tax withheld from your income as paid on the dates it was actually withheld, instead of in equal amounts on the payment due dates. You must figure your penalty and file Form 2210.

Your penalty is lower when figured by treating the federal income tax withheld from your income as paid on the dates it was actually withheld, instead of in equal amounts on the payment due dates. You must figure your penalty and file Form 2210.

E

You filed or are filing a joint return for either 2018 or 2019, but not for both years, and line 8 above is smaller than line 5 above. You must file page 1 of Form 2210, but you aren’t required to figure your penalty (unless box B, C, or D applies).

You filed or are filing a joint return for either 2018 or 2019, but not for both years, and line 8 above is smaller than line 5 above. You must file page 1 of Form 2210, but you aren’t required to figure your penalty (unless box B, C, or D applies).

For Paperwork Reduction Act Notice, see separate instructions. |

Cat. No. 11744P |

Form 2210 (2019) |

Form 2210 (2019) |

Page 2 |

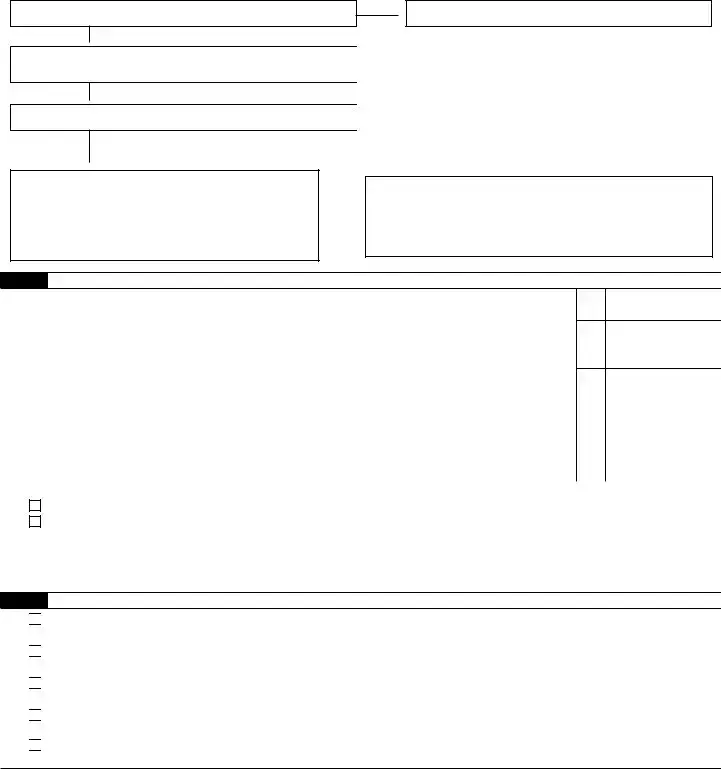

Part III Short Method

You can use the short method if:

• You made no estimated tax payments (or your only payments were withheld federal income tax), or

•You paid the same amount of estimated tax on each of the four payment due dates.

You must use the regular method (Part IV) instead of the short method if:

• You made any estimated tax payments late,

•You checked box C or D in Part II, or

•You are filing Form

Note: If any payment was made earlier than the due date, you can use the short method, but using it may cause you to pay a larger penalty than the regular method. If the payment was only a few days early, the difference is likely to be small.

10 |

Enter the amount from Form 2210, line 9 |

||

11 |

Enter the amount, if any, from Form 2210, line 6 |

11 |

|

12 |

Enter the total amount, if any, of estimated tax payments you made . . . |

12 |

|

13 |

Add lines 11 and 12 |

||

14Total underpayment for year. Subtract line 13 from line 10. If zero or less, stop; you don’t owe a

penalty. Don’t file Form 2210 unless you checked box E in Part II . . . . . . . . . . .

15 Multiply line 14 by 0.03398 . . . . . . . . . . . . . . . . . . . . . . . . .

16• If the amount on line 14 was paid on or after 4/15/20, enter

•If the amount on line 14 was paid before 4/15/20, make the following computation to find the amount to enter on line 16.

Amount on |

|

Number of days paid |

|

line 14 |

× |

before 4/15/20 |

× 0.00014 |

17Penalty. Subtract line 16 from line 15. Enter the result here and on Form 1040 or Form

Don’t file Form 2210 unless you checked a box in Part II . . . . . . . . . . . . .

10

13

14

15

16

17

Form 2210 (2019)

Form 2210 (2019) |

|

|

|

|

Page 3 |

||

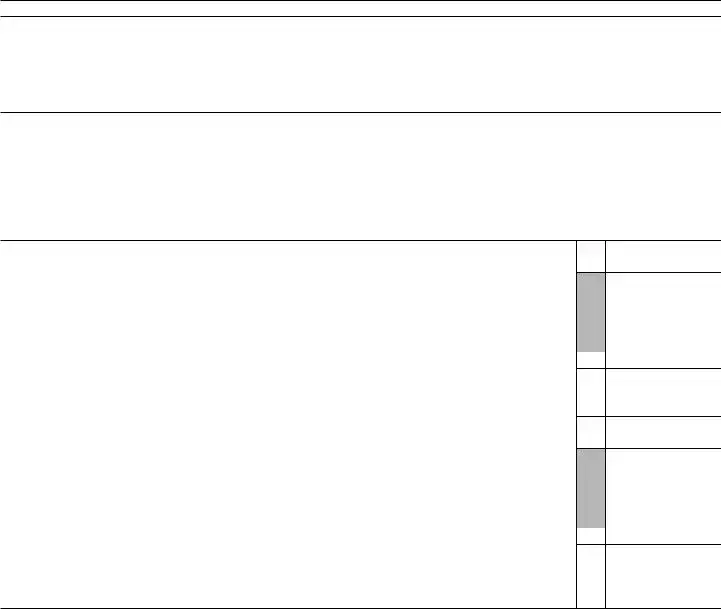

Part IV |

Regular Method (See the instructions if you are filing Form |

|

|||||

Section |

|

|

Payment Due Dates |

|

|||

|

(a) |

(b) |

(c) |

(d) |

|||

|

|

|

|

4/15/19 |

6/15/19 |

9/15/19 |

1/15/20 |

18 Required installments. If box C in Part II applies, |

|

|

|

|

|

||

enter the amounts from Schedule AI, line 27. |

|

|

|

|

|

||

Otherwise, enter 25% (0.25) of line 9, Form 2210, in |

|

|

|

|

|

||

each column |

|

18 |

|

|

|

|

|

19 Estimated tax paid and tax withheld (see the |

|

|

|

|

|

||

instructions). For column (a) only, also enter the |

|

|

|

|

|

||

amount from line 19 on line 23. If line 19 is equal to |

|

|

|

|

|

||

or more than line 18 for all payment periods, stop |

|

|

|

|

|

||

here; you don’t owe a penalty. Don’t file Form |

|

|

|

|

|

||

2210 unless you checked a box in Part II . . . |

19 |

|

|

|

|

||

Complete lines 20 through 26 of one column before going to line 20 of the next column.

20Enter the amount, if any, from line 26 in the previous

column |

. |

. . . |

. . . |

. |

. |

. |

20 |

|

|

21 Add lines 19 and 20 . |

. |

. . . |

. . . |

. |

. |

. |

21 |

|

|

22Add the amounts on lines 24 and 25 in the previous

column . . . . . . . . . . . . . . . 22

23Subtract line 22 from line 21. If zero or less, enter

19 . . . . . . . . . . . . . . . . . 23

24If line 23 is zero, subtract line 21 from line 22.

Otherwise, enter

25 |

Underpayment. If line 18 |

is equal to or more than |

|

|

|

line 23, subtract line 23 from line 18. Then go to line |

|

|

|

|

20 of the next column. Otherwise, go to line 26 . |

25 |

|

|

26 |

Overpayment. If line 23 |

is more than line 18, |

|

|

|

subtract line 18 from line 23. Then go to line 20 of |

|

|

|

|

the next column . . . |

. . . . . . . . . |

26 |

|

Section

27Penalty. Enter the total penalty from line 14 of the Worksheet for Form 2210, Part IV, Section

27

Form 2210 (2019)

Form 2210 (2019) |

Page 4 |

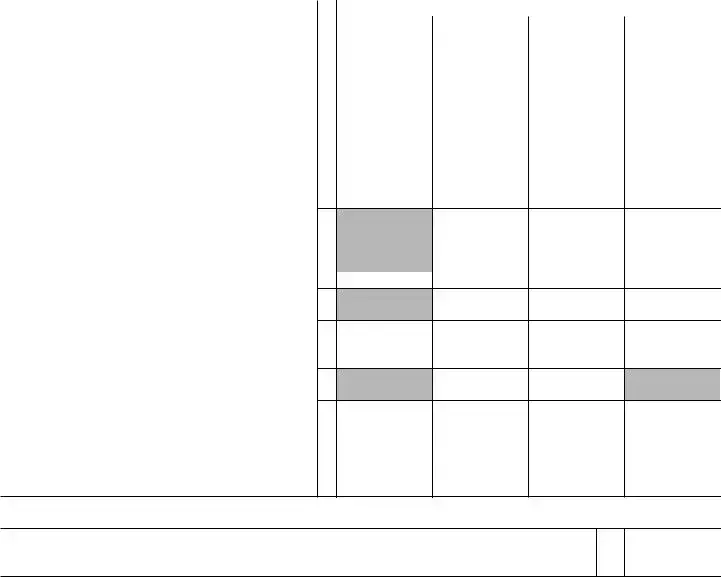

Schedule

Estates and trusts, don’t use the period ending dates shown to the right. Instead, use the following: 2/28/19, 4/30/19, 7/31/19, and 11/30/19.

(a)

(b)

(c)(d)

Part I Annualized Income Installments

1Enter your adjusted gross income for each period (see instructions). (Estates and trusts, enter your taxable

|

income without your exemption for each period.) . . |

1 |

|

|

|

|

2 |

Annualization amounts. (Estates and trusts, see instructions.) |

2 |

4 |

2.4 |

1.5 |

1 |

3 |

Annualized income. Multiply line 1 by line 2 . . . |

3 |

|

|

|

|

4 |

If you itemize, enter itemized deductions for the period |

|

|

|

|

|

|

shown in each column. All others enter |

|

|

|

|

|

|

line 7. Exception: Estates and trusts, skip to line 9 . |

4 |

|

|

|

|

5 |

Annualization amounts |

5 |

4 |

2.4 |

1.5 |

1 |

6 |

Multiply line 4 by line 5 |

6 |

|

|

|

|

7 |

In each column, enter the full amount of your standard |

|

|

|

|

|

|

deduction from Form 1040 or Form |

|

|

|

|

|

|

|

|

|

|

|

|

|

students and business apprentices, see instructions.) . . |

7 |

|

|

|

|

8 |

Enter the larger of line 6 or line 7 |

8 |

|

|

|

|

9 |

Deduction for qualified business income. Estates and trusts: |

|

|

|

|

|

|

Subtract this amount from the amount on line 3, skip |

|

|

|

|

|

|

line 10, and enter the result on line 11 |

9 |

|

|

|

|

10 |

Add lines 8 and 9 |

10 |

|

|

|

|

11 |

Subtract line 10 from line 3 |

11 |

|

|

|

|

12 |

Form 1040, |

|

|

|

|

|

|

12 |

|

|

|

|

|

13 |

Subtract line 12 from line 11. If zero or less, enter |

13 |

|

|

|

|

14 |

Figure your tax on the amount on line 13 (see instructions) |

14 |

|

|

|

|

15 |

15 |

|

|

|

|

|

16 |

Enter other taxes for each payment period including, |

|

|

|

|

|

|

if applicable, Additional Medicare Tax and/or Net |

|

|

|

|

|

|

Investment Income Tax (see instructions) . . . . |

16 |

|

|

|

|

17 |

Total tax. Add lines 14, 15, and 16 |

17 |

|

|

|

|

18 |

For each period, enter the same type of credits as allowed |

|

|

|

|

|

|

on Form 2210, Part I, lines 1 and 3 (see instructions) . . |

18 |

|

|

|

|

19 |

Subtract line 18 from line 17. If zero or less, enter |

19 |

|

|

|

|

20 |

Applicable percentage |

20 |

22.5% |

45% |

67.5% |

90% |

21 |

Multiply line 19 by line 20 |

21 |

|

|

|

|

|

Complete lines |

|

|

|

|

|

|

going to line 22 of the next column. |

|

|

|

|

|

22 |

Enter the total of the amounts in all previous columns of line 27 |

22 |

|

|

|

|

23 |

Subtract line 22 from line 21. If zero or less, enter |

23 |

|

|

|

|

24 |

Enter 25% (0.25) of line 9 on page 1 of Form 2210 in each column |

24 |

|

|

|

|

25 |

Subtract line 27 of the previous column from line 26 of that column 25 |

|

|

|

|

|

26 |

Add lines 24 and 25 |

26 |

|

|

|

|

27Enter the smaller of line 23 or line 26 here and on

|

Form 2210, Part IV, line 18 |

27 |

|

|

|

|

|

Part II |

Annualized |

|

|||||

28 |

Net earnings from |

28 |

|

|

|

|

|

29 |

Prorated social security tax limit |

29 |

$33,225 |

$55,375 |

$88,600 |

$132,900 |

|

30 |

Enter actual wages for the period subject to social security tax |

|

|

|

|

|

|

|

or the 6.2% portion of the 7.65% railroad retirement (tier 1) tax. |

|

|

|

|

|

|

|

Exception: If you filed Form 4137 or Form 8919, see instructions |

30 |

|

|

|

|

|

31 |

Subtract line 30 from line 29. If zero or less, enter |

31 |

|

|

|

|

|

32 |

Annualization amounts |

32 |

0.496 |

0.2976 |

0.186 |

0.124 |

|

33 |

Multiply line 32 by the smaller of line 28 or line 31 . |

33 |

|

|

|

|

|

34 |

Annualization amounts |

34 |

0.116 |

0.0696 |

0.0435 |

0.029 |

|

35 |

Multiply line 28 by line 34 |

35 |

|

|

|

|

|

36 |

Add lines 33 and 35. Enter here and on line 15 above |

36 |

|

|

|

|

|

Form 2210 (2019)

| Fact Name | Details |

|---|---|

| Purpose | The IRS Form 2210 is used to determine if you owe a penalty for underpayment of estimated tax. |

| Eligibility | Taxpayers who expect to owe tax of $1,000 or more when filing their return must use this form. |

| Filing Deadline | Form 2210 is generally filed alongside your annual tax return, due on April 15 unless an extension is granted. |

| State-Specific Forms | Many states have their own equivalent forms for estimated tax penalties, governed by state tax laws. |

Completing IRS Form 2210 can streamline the process of reporting any penalty for underpayment of estimated tax. Whether you are self-employed or simply managing your tax obligations, it’s important to ensure you fill out this form correctly to avoid potential penalties.

Once all required sections of the form are filled out accurately, review your calculations and information carefully. Submit the completed form along with your tax return or as instructed by the IRS. Keeping a copy for your records is also advisable.

The IRS Form 2210 is used to determine whether a taxpayer has to pay an underpayment penalty on their federal income taxes. This form helps individuals calculate if they paid enough taxes throughout the year either through withholding or estimated tax payments. If not, the form may be necessary to identify if a penalty applies and how much it might be.

Typically, you must file Form 2210 if you owe a penalty for not paying enough tax throughout the year. This situation can arise if you did not have enough tax withheld from your wages or if you did not make sufficient estimated tax payments. Generally, if your total tax due is at least $1,000 and your withholding and refundable credits are less than 90% of your current year tax or 100% of your last year's tax, you will likely need to file this form.

To determine if you owe a penalty, complete the IRS Form 2210. The form includes a section where you report your total tax liability and payments made throughout the year. If the calculations show that your payments were significantly less than your total tax due, a penalty may apply. It's important to ensure all calculations are accurate to avoid unnecessary penalties. You can also find penalty details in the instructions provided with the form.

There are several exceptions where you may not be subject to a penalty, including:

Always review your specific situation or consult a tax professional to see if you qualify for any exceptions.

Yes, increasing your withholding or making estimated payments can help avoid the underpayment penalty in the future. By ensuring that enough tax is paid during the year, you can meet the payment requirements set by the IRS. Adjusting your withholdings can be done through your employer by submitting a new W-4 form. This proactive approach is especially beneficial if you anticipate a higher income or tax liability in the coming year.

Form 2210 can be filed along with your income tax return. If you're required to file the form, it should accompany your 1040 when you mail it to the IRS or electronically, depending on your filing method. Ensure you complete all sections of the form and provide any necessary attachments. You can find the form on the IRS website, along with detailed instructions on how to fill it out.

If you need assistance with completing Form 2210, there are several resources available. You can access the IRS website, which provides guidelines and instructions. Additionally, you may choose to consult a tax professional who can offer personalized advice based on your unique tax situation. Many community organizations also offer tax assistance services, especially during tax season, which can be invaluable for those who prefer hands-on help.

Filling out the IRS Form 2210 can be a daunting task. Many individuals make common mistakes that can lead to complications or even penalties. Understanding these pitfalls can help ensure your form is completed accurately.

One frequent error is failing to check the box that indicates which method of calculating underpayment penalties applies. This simple step may seem minor, but it significantly affects how the IRS assesses your tax obligations.

Another mistake is not accurately reporting estimated tax payments made throughout the year. Ensure that you include all relevant payments, as missing any could lead to an inaccurate calculation of the penalty.

Many filers miscalculate their tax owed. This can happen when individuals rely on rough estimates instead of using the actual amounts reported on their tax return. That's why double-checking the figures helps avoid unwelcome surprises later.

It's also common for individuals to forget to consider the total tax liability. This figure needs to be compared against the total payments made to determine if there was indeed an underpayment.

Another mistake is omitting the required supporting documents. While the form itself is crucial, attaching necessary documentation or schedules enhances clarity and backs up the figures reported.

Additionally, some people do not account for special circumstances that might exempt them from penalties. If you had circumstances that affected your ability to pay, such as a serious illness or natural disaster, be sure to indicate this on the form.

Filing the form late is another regrettable error. It’s essential to submit IRS Form 2210 by the deadline to avoid further penalties. Ensure you know the due dates associated with your tax filings.

Lastly, not retaining copies of your completed form can lead to future headaches. Always keep a copy for your records in case questions arise later or you need to reference it in the future.

By being aware of these common mistakes, you can complete IRS Form 2210 more confidently and accurately. Take your time, double-check your work, and remember that clarity and precision are your best allies in the process.

The IRS Form 2210 is essential for taxpayers who need to calculate their underpayment of estimated taxes. However, there are several other forms and documents that are often used alongside it to ensure compliance with tax obligations. Below is a list of related forms that may be relevant as you navigate your tax responsibilities.

Understanding these documents can facilitate a smoother filing process and help avoid potential penalties. Staying informed and organized is crucial in managing your tax obligations effectively.

Filling out the IRS Form 2210 can seem daunting, but understanding what to do and what to avoid can simplify the process. Here’s a helpful list of dos and don’ts to guide you through completing this form.

Following these guidelines can make the process smoother and reduce the risk of mistakes when filling out the IRS Form 2210. Proper preparation ensures a more accurate and efficient filing experience.

There are several misconceptions surrounding the IRS Form 2210 that individuals should be aware of. Understanding these can help taxpayers navigate their obligations more effectively.

This form is commonly associated with penalties for underpayment of taxes. However, it is also used to calculate whether taxpayers may qualify for a waiver of that penalty. Thus, it can serve both to assess penalties and to request relief.

Many taxpayers believe that they need to submit Form 2210 annually. In reality, it is only necessary to file the form if there is a reason to do so, such as if you owe a penalty for underpayment. If you have paid enough taxes throughout the year, you may not need to file it.

Some individuals think that submitting Form 2210 automatically absolves them of any penalties for underpaying taxes. While the form allows for the calculation of penalties and potential waivers, final decisions are made by the IRS based on the details of each case.

The annualized income method is a specific calculation available on Form 2210. However, not everyone will qualify or need to use this method. Taxpayers with steady incomes may find the regular method more straightforward and suitable for their situation.

While it may seem daunting, Form 2210 is designed to clarify tax liabilities and penalties. In many cases, utilizing the form can lead to a better understanding of tax obligations and potentially lower penalties. Assistance is available for those who may find the form challenging.

Understanding the IRS Form 2210 can make a significant difference in managing your taxes, especially if you're facing an underpayment penalty. Here are some important points to keep in mind when filling out and using this form:

By following these key points, you can navigate the complexities of Form 2210 with confidence and avoid unnecessary penalties. Proper preparation and understanding of your tax obligations can go a long way in ensuring a smooth tax season.