Navigating the complexities of tax forms can be intimidating, especially when it comes to specific documents like the IRS Form 2439. This form plays a crucial role in the tax landscape for those who have invested in certain types of regulated investment companies or real estate investment trusts. When these entities make distributions that include undistributed long-term capital gains, investors receive Form 2439 to inform them of their tax obligations. The form details important information, including the amount of undistributed capital gains and any related tax liability that must be reported on the investor's personal tax return. For many, understanding the implications of this form can significantly impact their tax situation. Compliance with the reporting requirements ensures that taxpayers are not caught off guard when filing their returns. Grasping the nuances of Form 2439—and what it conveys about investment income—can help individuals make informed financial decisions and avoid potential pitfalls during tax season.

|

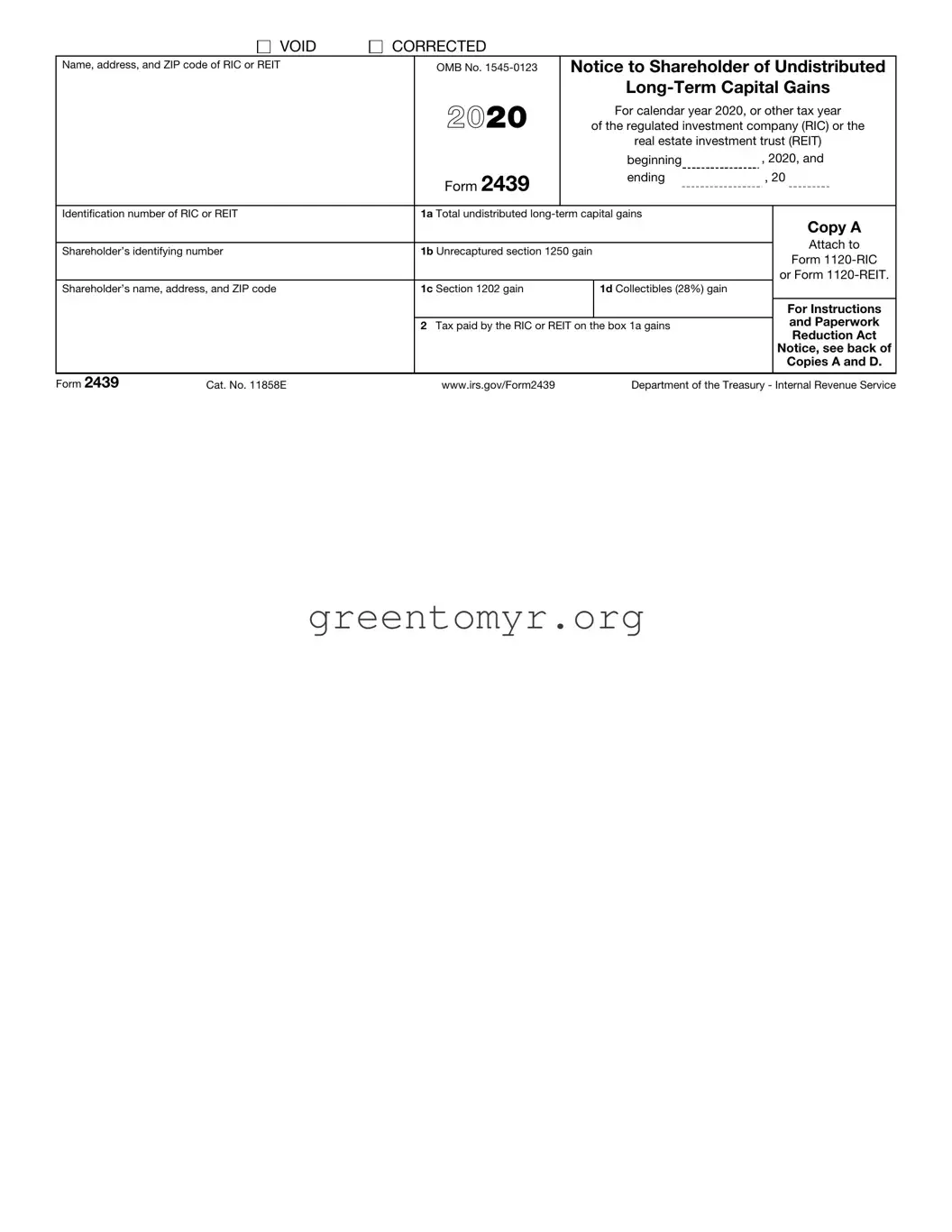

VOID |

CORRECTED |

|

|

|

|

|

Name, address, and ZIP code of RIC or REIT |

|

OMB No. |

Notice to Shareholder of Undistributed |

||||

|

|

|

|

|

|||

|

|

|

2020 |

|

For calendar year 2020, or other tax year |

||

|

|

|

of the regulated investment company (RIC) or the |

||||

|

|

|

|

|

real estate investment trust (REIT) |

||

|

|

|

|

|

beginning |

, 2020, and |

|

|

|

|

Form 2439 |

|

ending |

, 20 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Identification number of RIC or REIT |

|

1a Total undistributed |

|

Copy A |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Attach to |

Shareholder’s identifying number |

|

1b Unrecaptured section 1250 gain |

|

||||

|

|

Form |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

or Form |

Shareholder’s name, address, and ZIP code |

|

1c Section 1202 gain |

|

1d Collectibles (28%) gain |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For Instructions |

|

|

|

|

|

|

and Paperwork |

|

|

|

|

2 Tax paid by the RIC or REIT on the box 1a gains |

|

|||

|

|

|

|

|

|

|

Reduction Act |

|

|

|

|

|

|

|

Notice, see back of |

|

|

|

|

|

|

|

Copies A and D. |

|

|

|

|

|

|

|

|

Form 2439 |

Cat. No. 11858E |

|

www.irs.gov/Form2439 |

|

Department of the Treasury - Internal Revenue Service |

||

Instructions for the Regulated Investment Company (RIC) and the Real Estate Investment Trust (REIT)

Section references are to the Internal Revenue Code.

Reporting Information

1.Complete Copies A, B, C, and D for each shareholder for whom the regulated investment company (RIC) or real estate investment trust (REIT) paid tax on undistributed capital gains under section 852(b)(3)(D) or 857(b)(3)(C).

2.Attach Copy A of all Forms 2439 to Form

3.Furnish Copies B and C of Form 2439 to the shareholder by the 60th day after the end of the RIC’s or the REIT’s tax year.

4.Retain Copy D for the RIC’s or REIT’s records.

For a shareholder that is an individual retirement ▲! arrangement (IRA), send Copies B and C to the trustee or

custodian of the IRA. Do not send copies to the owner of CAUTION the IRA.

RIC’s or REIT’s name, address, and identification number. Enter the name, address (including ZIP code) and employer identification number (EIN) of the RIC or REIT as shown on Form 2438, Undistributed Capital Gains Tax Return.

Shareholder’s identifying number, name, and address. Enter the shareholder’s social security number (SSN), name, and address (including ZIP code). If the shareholder is not an individual, enter the EIN. If a shareholder is an IRA, enter the identification number of the IRA trust. Do not enter the SSN of the person for whom the IRA is maintained.

The RIC or REIT can truncate a shareholder’s identifying number on the Form 2439 the RIC or REIT sends to the shareholder. Truncation is not allowed on the Form 2439 the RIC or REIT files with the IRS. Also, the RIC or REIT cannot truncate its own identification number on any form.

To truncate, where allowed, replace the first 5 digits of the

Box 1a. Enter the amount of undistributed capital gains from line 11, Form 2438, allocable to the shareholder.

(Continued on the back of Copy D)

VOID |

CORRECTED |

|

|

|

|

|

Name, address, and ZIP code of RIC or REIT |

|

OMB No. |

Notice to Shareholder of Undistributed |

|||

|

|

|

|

|||

|

|

2020 |

|

For calendar year 2020, or other tax year |

||

|

|

of the regulated investment company (RIC) or the |

||||

|

|

|

|

real estate investment trust (REIT) |

||

|

|

|

|

beginning |

, 2020, and |

|

|

|

Form 2439 |

|

ending |

, 20 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Identification number of RIC or REIT |

|

1a Total undistributed |

|

Copy B |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

Attach to the |

Shareholder’s identifying number |

|

1b Unrecaptured section 1250 gain |

|

|||

|

|

shareholder’s |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

income tax return |

Shareholder’s name, address, and ZIP code |

|

1c Section 1202 gain |

|

1d Collectibles (28%) gain |

|

for the tax year |

|

|

|

|

|

|

that includes the |

|

|

|

|

|

|

last day of the |

|

|

2 Tax paid by the RIC or REIT on the box 1a gains |

|

|||

|

|

|

RIC’s or REIT’s |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

tax year. |

|

|

|

|

|

|

|

Form 2439 |

www.irs.gov/Form2439 |

|

Department of the Treasury - Internal Revenue Service |

|||

Instructions for the Shareholder

Section references are to the Internal Revenue Code.

Reporting Information

Shareholder’s identifying number. For your protection, Form 2439 may show only the last four digits of your identifying number (social security number (SSN), etc.). However, the RIC or REIT has reported your complete identifying number to the IRS.

Box 1a. This amount is your total undistributed

Report the total amount as a

Corporate shareholders report this amount in Part II of Form 8949. See Form 8949, Schedule D (Form 1120), and the related instructions for details.

If there is an amount in box 1b, 1c, or 1d, special instructions apply for entering those amounts on the appropriate Schedule D.

See Undistributed Capital Gains in the Schedule D (Form 1040) and Schedule D (Form 1041) instructions.

Box 1b. This amount is the unrecaptured section 1250 gain. Individual filers report this amount on line 11 of the Unrecaptured Section 1250 Gain Worksheet in the Schedule D (Form 1040) instructions. Estates and trusts use this amount to complete the Unrecaptured Section 1250 Gain Worksheet in the Schedule D (Form 1041) instructions.

Box 1c. This amount applies to the portion of the amount in box 1a attributable to a section 1202 gain (sale of qualified small business stock). Individual filers, see Exclusion of Gain on Qualified Small Business (QSB) Stock in the Schedule D (Form 1040) instructions. Estates and trusts, see Exclusion of Gain on Qualified Small Business (QSB) Stock (Section 1202) in the Schedule D (Form 1041) instructions.

Box 1d. This amount is the collectibles gain (28% rate gain) portion of the amount in box 1a. Individual filers enter this amount on line 4 of the 28% Rate Gain Worksheet in the Schedule D (Form 1040) instructions. Estates and trusts use this amount to complete the 28% Rate Gain Worksheet in the Schedule D (Form 1041) instructions.

Box 2. This amount is the tax paid by the RIC or REIT on the undistributed

(Continued on the back of Copy C)

VOID |

CORRECTED |

|

|

|

|

|

Name, address, and ZIP code of RIC or REIT |

|

OMB No. |

Notice to Shareholder of Undistributed |

|||

|

|

|

|

|||

|

2020 |

|

For calendar year 2020, or other tax year |

|||

|

of the regulated investment company (RIC) or the |

|||||

|

|

|

|

real estate investment trust (REIT) |

||

|

|

|

|

beginning |

, 2020, and |

|

|

|

Form 2439 |

|

ending |

, 20 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Identification number of RIC or REIT |

|

1a Total undistributed |

|

|

||

|

|

|

|

|

|

|

Shareholder’s identifying number |

|

1b Unrecaptured section 1250 gain |

|

|

||

|

|

|

|

|

|

Copy C |

Shareholder’s name, address, and ZIP code |

|

1c Section 1202 gain |

|

1d Collectibles (28%) gain |

|

For shareholder’s |

|

|

|

|

|

|

records. |

|

|

|

|

|

|

|

2Tax paid by the RIC or REIT on the box 1a gains

Form 2439 |

www.irs.gov/Form2439 |

Department of the Treasury - Internal Revenue Service |

Instructions for the Shareholder (Continued)

Individuals, nonresident aliens, and estates and trusts. See line 12a of Schedule 3 (Form 1040) or Schedule G, line 16a of Form 1041, and the related instructions.

Corporations (other than S corporations). See Schedule J, line 20a of Form 1120 or line 5f of Form

S corporations and partnerships. See the Specific Instructions for Schedules K and

Exempt organizations and certain trustees. See the Instructions for Form

1.Organizations exempt from tax under section 501(a) filing Form

2.Trustees for individual retirement arrangements (IRAs) described in section 408 (including accounts described in section 408(h)) filing a single composite Form

Nominees. If you are not the actual owner of the shares for which this form is issued, you must do the following.

1.Complete Copies A, B, C, and D of Form 2439 for each owner. The total undistributed

2.Enter your name as “Nominee” and your address in the block for the RIC’s or REIT’s name and address, and the RIC’s or REIT’s name and address in the same block.

3.Write “Nominee” in the upper right corner of the Copy B you received from the RIC or REIT and attach it to the Copy A you completed.

4.File the Copy B you received (with an attached Copy A) with the Internal Revenue Service Center where you file your income tax return.

5.Give the actual owner Copies B and C of the forms you complete.

6.Copy D is to be maintained by the RIC or REIT.

A nominee has 90 days after the close of the RIC’s or REIT’s tax year to complete items 1 through 5 above. However, a nominee acting as a custodian of a unit investment trust described in section 851(f)(1) has 70 days. A nominee who is a resident of a foreign country has 150 days.

VOID |

CORRECTED |

|

|

|

|

|

Name, address, and ZIP code of RIC or REIT |

|

OMB No. |

Notice to Shareholder of Undistributed |

|||

|

|

|

|

|||

|

|

2020 |

|

For calendar year 2020, or other tax year |

||

|

|

of the regulated investment company (RIC) or the |

||||

|

|

|

|

real estate investment trust (REIT) |

||

|

|

|

|

beginning |

, 2020, and |

|

|

|

Form 2439 |

|

ending |

, 20 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Identification number of RIC or REIT |

|

1a Total undistributed |

|

|

||

|

|

|

|

|

|

Copy D |

Shareholder’s identifying number |

|

1b Unrecaptured section 1250 gain |

|

|||

|

|

For records of the |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

regulated |

Shareholder’s name, address, and ZIP code |

|

1c Section 1202 gain |

|

1d Collectibles (28%) gain |

|

investment |

|

|

|

|

|

|

company or the |

|

|

|

|

|

|

real estate |

|

|

2 Tax paid by the RIC or REIT on the box 1a gains |

|

|||

|

|

|

investment trust. |

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form 2439 |

www.irs.gov/Form2439 |

|

Department of the Treasury - Internal Revenue Service |

|||

Instructions for the RIC and the REIT

(Continued)

Box 1b. Enter the shareholder’s allocable portion of the amount from box 1a that has been designated as unrecaptured section 1250 gain from the disposition of depreciable real property.

Box 1c. The section 1202 gain is the portion of box 1a that is attributable to the sale or exchange by the RIC of qualified small business stock issued after August 10, 1993, and held for more than 5 years. Enter the shareholder’s allocable portion of the amount from box 1a attributable to a section 1202 gain. In addition, attach a statement that reports separately for each designated section 1202 gain the following information: the amount of the section 1202 gain, the name of the corporation that issued the stock, the dates on which the RIC acquired and sold the stock, and the shareholder’s portion of the RIC’s adjusted basis and sales price of the stock.

Box 1d. Enter the shareholder’s allocable portion of the amount from box 1a attributable to collectibles gain (28% rate gain). Do not include any section 1202 gain in box 1d.

Box 2. Enter the tax paid on the amount in box 1a.

Future developments. For the latest information about developments related to Form 2439 and its instructions, such as legislation enacted after they were published, go to www.irs.gov/Form2439.

Paperwork Reduction Act Notice. We ask for the information on this form to carry out the Internal Revenue laws of the United States. You are required to give us the information. We need it to ensure that you are complying with these laws and to allow us to figure and collect the right amount of tax.

You are not required to provide the information requested on a form that is subject to the Paperwork Reduction Act unless the form displays a valid OMB control number. Books or records relating to a form or its instructions must be retained as long as their contents may become material in the administration of any Internal Revenue law. Generally, tax returns and return information are confidential, as required by section 6103.

The time needed to complete and file this form will vary depending on individual circumstances. The estimated burden for business taxpayers filing this form is approved under OMB control number

If you have comments concerning the accuracy of these time estimates or suggestions for making this form simpler, we would be happy to hear from you. You can send us comments from www.irs.gov/FormComments. Or you can write to the Internal Revenue Service, Tax Forms and Publications Division, 1111 Constitution Ave. NW,

| Fact Name | Description |

|---|---|

| Purpose | Form 2439 is used by shareholders of an S corporation to report an undistributed capital gains tax from the corporation. |

| Filing Requirement | If an S corporation has capital gains, shareholders must receive this form to accurately report their share of these gains. |

| Due Date | Shareholders must report the information on Form 2439 by the tax filing deadline, typically April 15 for individual taxpayers. |

| State-Specific Forms | Some states may require additional forms to report gains. For example, California requires Form 592-B for pass-through entities. |

| Box Information | The form contains various boxes. Notably, Box 1 reports the shareholder’s share of undistributed capital gains. |

| Tax Implications | The undistributed capital gains reported can increase a shareholder's tax liability, as they are subject to taxation even without distribution. |

| Penalties for Non-compliance | Failure to report the income reported on this form may result in penalties, including potential interest on unpaid taxes. |

Once you have collected your financial information, it's time to fill out the IRS Form 2439. This form is essential for reporting undistributed long-term capital gains from regulated investment companies. Careful attention to detail will help ensure that the form is completed accurately, avoiding any potential issues with the IRS.

After completing the form, you will need to submit it along with your tax return. Always keep a copy for your records, as it may be necessary for future reference or any inquiries from the IRS.

The IRS Form 2439 is a tax form used by shareholders of a Mutual Fund or a Regulated Investment Company (RIC). It primarily reports undistributed long-term capital gains that you may have received from these investments. This form is essential for properly calculating and reporting your tax liability related to these gains, ensuring you are aware of the amount that may need to be included on your tax return.

Only shareholders who have received this form need to take action. If you hold shares in a mutual fund or regulated investment company that reports undistributed gains to you, you will receive Form 2439. It’s important for taxpayers who have had dividends reinvested or received distributions that were not immediately taxed.

To report the information from Form 2439 on your tax return, follow these steps:

Always double-check your entries and consider seeking assistance from a tax professional if you’re unsure about the process.

Receiving Form 2439 indicates that you have undistributed capital gains, which can affect your tax liability. The amount listed in Box 1a is typically taxed as long-term capital gain, regardless of how long you have held the shares. This may lead to a higher tax bill, so it’s crucial to plan accordingly. Understanding these implications allows you to factor potential taxes into your investment decisions.

If you believe you should have received Form 2439 but did not, start by checking with your mutual fund or investment company. They can confirm whether there were any undistributed gains during the tax year. If they indicate that gains exist, request a copy of the form. It’s always better to ensure you have all necessary documents to avoid potential issues with tax reporting.

For more detailed information, you can visit the official IRS website. They provide comprehensive guidance, including instructions for completing Form 2439 and related forms. Additionally, you can consult tax professionals or resources like tax preparation software that often feature integrated instructions for dealing with various IRS forms.

Filling out the IRS Form 2439 can be a straightforward task, but mistakes are common and may lead to delays or issues with tax liabilities. One of the most frequent errors is failing to report the correct information regarding the amount of the undistributed capital gains. Taxpayers may underestimate or overlook this figure, leading to discrepancies that could complicate tax filings. It is essential to ensure that you accurately account for any undistributed amounts received from a regulated investment company or real estate investment trust.

Another common mistake involves incorrect personal information. People often forget to double-check their names, addresses, and Social Security numbers. A simple typo can create confusion and result in delays during processing. It is crucial to ensure that all personal details are accurate and consistent with the information already submitted to the IRS. This attention to detail can prevent unnecessary follow-ups and delays in your tax situation.

Some filers also neglect to attach the required documentation that supports the information provided on Form 2439. This could include the notice from the entity that sent out the capital gain distributions. If the IRS does not receive the appropriate supporting documentation, it may lead to queries that entail additional stress and workload. Always ensure that you include any necessary attachments when submitting your form.

Lastly, many individuals make the mistake of miscalculating their tax liability. Calculating the tax on undistributed capital gains can be tricky. Errors can easily occur, whether through arithmetic mistakes or misunderstanding tax rates. A thorough review of the calculation based on the current tax guidelines is essential. This diligence can save you from underpayment or overpayment penalties later on.

The IRS Form 2439 is used to report the income from the sale of certain partnerships or S corporations for shareholders. This form helps determine the tax obligations arising from these transactions. Below are five other forms and documents that are commonly used in conjunction with Form 2439, each serving its purpose in facilitating tax reporting and compliance.

Understanding these forms and documents will aid taxpayers in managing their obligations effectively and filing accurate returns. Proper documentation ensures compliance with IRS regulations while minimizing the risk of errors in tax reporting.

Form 1099-DIV: This form reports dividends and distributions to investors. Like Form 2439, it provides vital information regarding distributions from investments. When taxpayers receive dividends, they must report this income on their tax return, just as they would with the capital gains from distributions noted on Form 2439.

Form 1099-INT: This document is used to report interest income earned. Similar to Form 2439, it informs taxpayers of income they need to report to the IRS. Both forms highlight income that originates from investments, ensuring accurate tax reporting.

Form K-1: Issued by partnerships and S-corporations, this form details each partner's share of income, deductions, and credits. Just as Form 2439 summarizes capital gains from mutual fund distributions, Form K-1 offers a snapshot of a partner's tax obligations based on their share of the entity's income.

Form 8949: This form is utilized for reporting sales and other dispositions of capital assets. Both Form 2439 and Form 8949 play crucial roles in calculating capital gains and losses. While Form 2439 focuses on undistributed gains, Form 8949 provides a detailed account of individual transactions.

Form 1040 Schedule D: This schedule is a part of individual income tax returns, summarizing capital gains and losses. Like Form 2439, it helps taxpayers report and calculate their overall capital gains tax liability, ensuring compliance with IRS regulations.

When filling out the IRS Form 2439, it is important to approach the task with care. Here are some tips on what you should and shouldn’t do:

By following these guidelines, you can help ensure that your submission is processed smoothly and efficiently.

The IRS Form 2439 is often misunderstood, leading to confusion among taxpayers. Here are eight common misconceptions about this form, along with clarifications to help navigate the details more clearly.

By addressing these misconceptions, individuals and businesses can better understand how to handle the IRS Form 2439 and ensure they comply with tax regulations effectively.

The IRS Form 2439 is used by investors for reporting undistributed long-term capital gains from regulated investment companies (RICs) or real estate investment trusts (REITs). Here are some key takeaways regarding the form: