The IRS 3520 form plays a crucial role for American taxpayers who have foreign trusts or have received foreign gifts. This form is not merely a routine tax document; it provides the IRS with important information regarding your financial interactions with non-U.S. entities. To ensure compliance, taxpayers must report certain transactions involving foreign trusts, as well as gifts that exceed specified thresholds. It is essential to understand that failing to file this form correctly or on time can lead to hefty penalties, which is why recognizing its importance cannot be overstated. The IRS uses the data collected through Form 3520 to assess potential tax obligations, ensuring transparency and accountability when it comes to cross-border financial activities. Navigating the intricacies of this form requires attention to detail, given that it asks for specific information about the trust, its beneficiaries, and any relevant transactions. Understanding the criteria for filing, the deadlines involved, and potential exemptions can help taxpayers meet their reporting requirements efficiently.

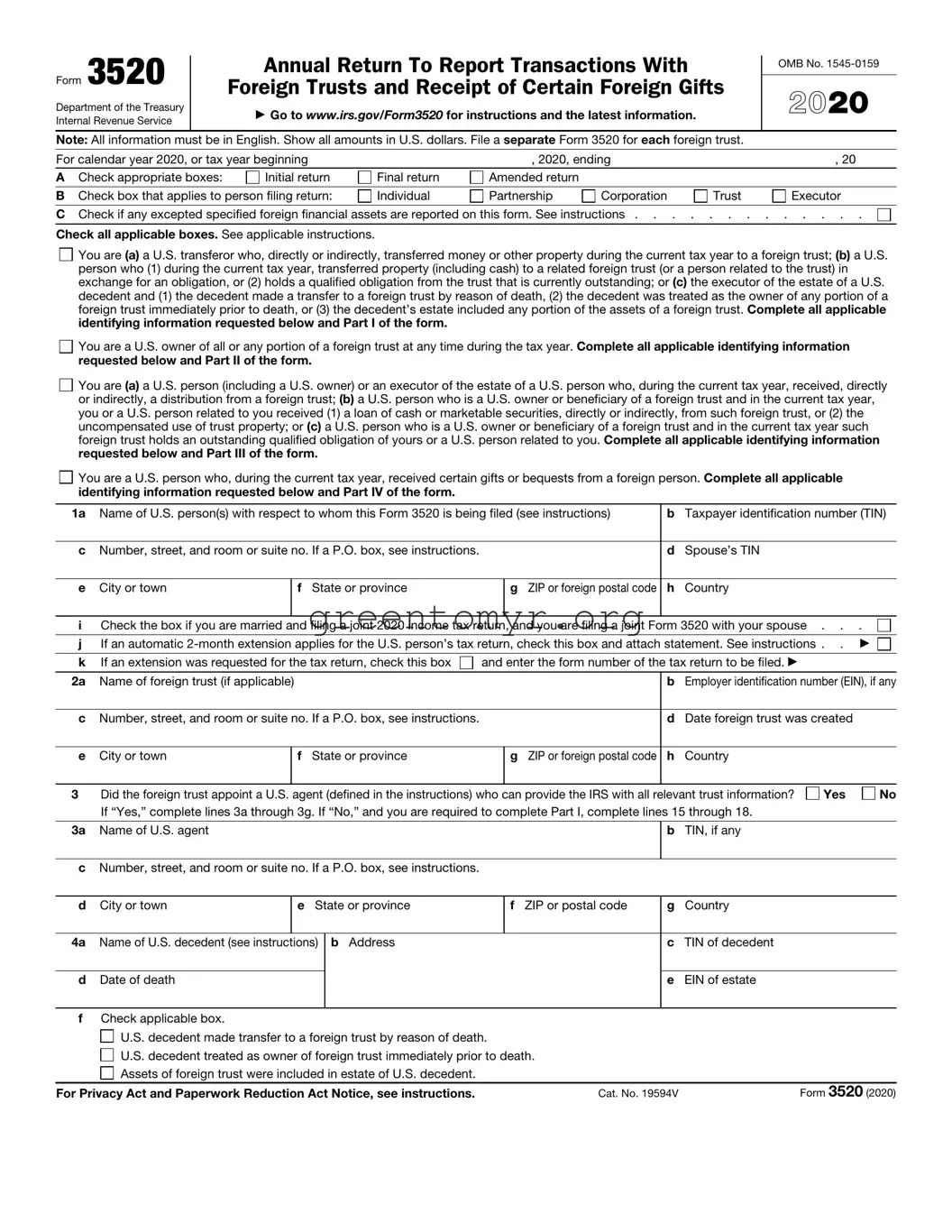

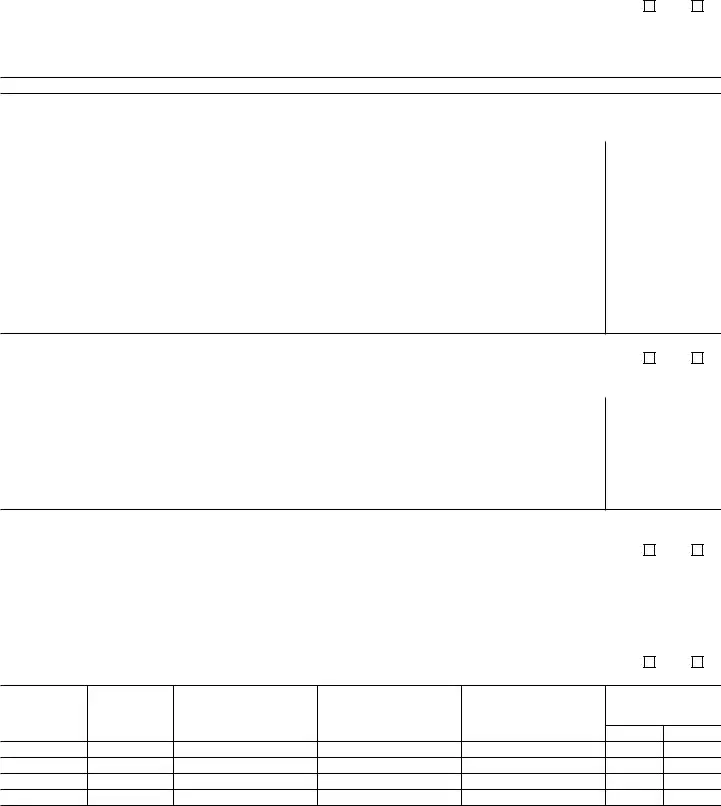

Form 3520

Department of the Treasury Internal Revenue Service

Annual Return To Report Transactions With

Foreign Trusts and Receipt of Certain Foreign Gifts

▶Go to www.irs.gov/Form3520 for instructions and the latest information.

OMB No.

2020

Note: All information must be in English. Show all amounts in U.S. dollars. File a separate Form 3520 for each foreign trust.

For calendar year 2020, or tax year beginning |

|

, 2020, ending |

|

, 20 |

|||

A |

Check appropriate boxes: |

Initial return |

Final return |

Amended return |

|

|

|

|

|

|

|

|

|

|

|

B |

Check box that applies to person filing return: |

Individual |

Partnership |

Corporation |

Trust |

Executor |

|

|

|

||||||

C |

Check if any excepted specified foreign financial assets are reported on this form. See instructions |

||||||

Check all applicable boxes. See applicable instructions.

You are (a) a U.S. transferor who, directly or indirectly, transferred money or other property during the current tax year to a foreign trust; (b) a U.S. person who (1) during the current tax year, transferred property (including cash) to a related foreign trust (or a person related to the trust) in exchange for an obligation, or (2) holds a qualified obligation from the trust that is currently outstanding; or (c) the executor of the estate of a U.S. decedent and (1) the decedent made a transfer to a foreign trust by reason of death, (2) the decedent was treated as the owner of any portion of a foreign trust immediately prior to death, or (3) the decedent’s estate included any portion of the assets of a foreign trust. Complete all applicable identifying information requested below and Part I of the form.

You are (a) a U.S. transferor who, directly or indirectly, transferred money or other property during the current tax year to a foreign trust; (b) a U.S. person who (1) during the current tax year, transferred property (including cash) to a related foreign trust (or a person related to the trust) in exchange for an obligation, or (2) holds a qualified obligation from the trust that is currently outstanding; or (c) the executor of the estate of a U.S. decedent and (1) the decedent made a transfer to a foreign trust by reason of death, (2) the decedent was treated as the owner of any portion of a foreign trust immediately prior to death, or (3) the decedent’s estate included any portion of the assets of a foreign trust. Complete all applicable identifying information requested below and Part I of the form.

You are a U.S. owner of all or any portion of a foreign trust at any time during the tax year. Complete all applicable identifying information requested below and Part II of the form.

You are a U.S. owner of all or any portion of a foreign trust at any time during the tax year. Complete all applicable identifying information requested below and Part II of the form.

You are (a) a U.S. person (including a U.S. owner) or an executor of the estate of a U.S. person who, during the current tax year, received, directly or indirectly, a distribution from a foreign trust; (b) a U.S. person who is a U.S. owner or beneficiary of a foreign trust and in the current tax year, you or a U.S. person related to you received (1) a loan of cash or marketable securities, directly or indirectly, from such foreign trust, or (2) the uncompensated use of trust property; or (c) a U.S. person who is a U.S. owner or beneficiary of a foreign trust and in the current tax year such foreign trust holds an outstanding qualified obligation of yours or a U.S. person related to you. Complete all applicable identifying information requested below and Part III of the form.

You are (a) a U.S. person (including a U.S. owner) or an executor of the estate of a U.S. person who, during the current tax year, received, directly or indirectly, a distribution from a foreign trust; (b) a U.S. person who is a U.S. owner or beneficiary of a foreign trust and in the current tax year, you or a U.S. person related to you received (1) a loan of cash or marketable securities, directly or indirectly, from such foreign trust, or (2) the uncompensated use of trust property; or (c) a U.S. person who is a U.S. owner or beneficiary of a foreign trust and in the current tax year such foreign trust holds an outstanding qualified obligation of yours or a U.S. person related to you. Complete all applicable identifying information requested below and Part III of the form.

You are a U.S. person who, during the current tax year, received certain gifts or bequests from a foreign person. Complete all applicable identifying information requested below and Part IV of the form.

You are a U.S. person who, during the current tax year, received certain gifts or bequests from a foreign person. Complete all applicable identifying information requested below and Part IV of the form.

1a |

Name of U.S. person(s) with respect to whom this Form 3520 is being filed (see instructions) |

b |

Taxpayer identification number (TIN) |

||||

|

|

|

|

|

|

|

|

c |

Number, street, and room or suite no. If a P.O. box, see instructions. |

|

|

d |

Spouse’s TIN |

||

|

|

|

|

|

|

|

|

e |

City or town |

|

f State or province |

|

g ZIP or foreign postal code |

h |

Country |

|

|

|

|

|

|||

i |

Check the box if you are married and filing a joint 2020 income tax return, and you are filing a joint Form 3520 with your spouse . . . |

||||||

|

|

||||||

j |

If an automatic |

||||||

|

|

|

|||||

k |

If an extension was requested for the tax return, check this box |

and enter the form number of the tax return to be filed. ▶ |

|||||

|

|

|

|

|

|

||

2a |

Name of foreign trust (if applicable) |

|

|

|

b Employer identification number (EIN), if any |

||

cNumber, street, and room or suite no. If a P.O. box, see instructions.

dDate foreign trust was created

eCity or town

fState or province

gZIP or foreign postal code

hCountry

3 |

Did the foreign trust appoint a U.S. agent (defined in the instructions) who can provide the IRS with all relevant trust information? |

Yes |

No |

|||||

|

If “Yes,” complete lines 3a through 3g. If “No,” and you are required to complete Part I, complete lines 15 through 18. |

|

|

|||||

|

|

|

|

|

|

|

|

|

3a |

Name of U.S. agent |

|

|

|

b |

TIN, if any |

|

|

|

|

|

|

|

|

|

|

|

c Number, street, and room or suite no. If a P.O. box, see instructions. |

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

d |

City or town |

e State or province |

f ZIP or postal code |

g |

Country |

|

|

|

|

|

|

|

|

|

|

|

|

4a |

Name of U.S. decedent (see instructions) |

b Address |

|

c |

TIN of decedent |

|

|

|

|

|

|

|

|

|

|

|

|

d |

Date of death |

|

|

|

e |

EIN of estate |

|

|

|

|

|

|

|

|

|

|

|

fCheck applicable box.

U.S. decedent made transfer to a foreign trust by reason of death. |

|

|

U.S. decedent treated as owner of foreign trust immediately prior to death. |

|

|

Assets of foreign trust were included in estate of U.S. decedent. |

|

|

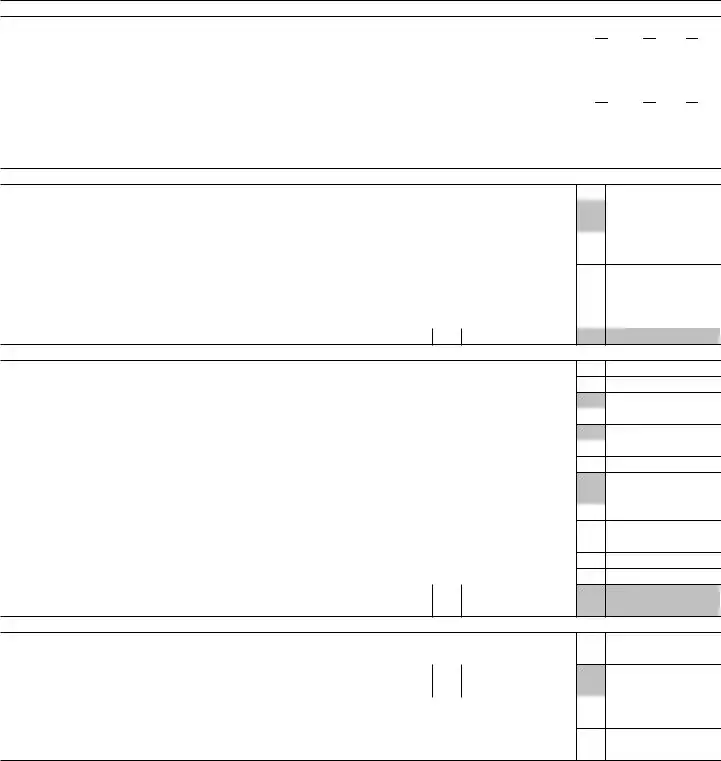

For Privacy Act and Paperwork Reduction Act Notice, see instructions. |

Cat. No. 19594V |

Form 3520 (2020) |

Form 3520 (2020) |

Page 2 |

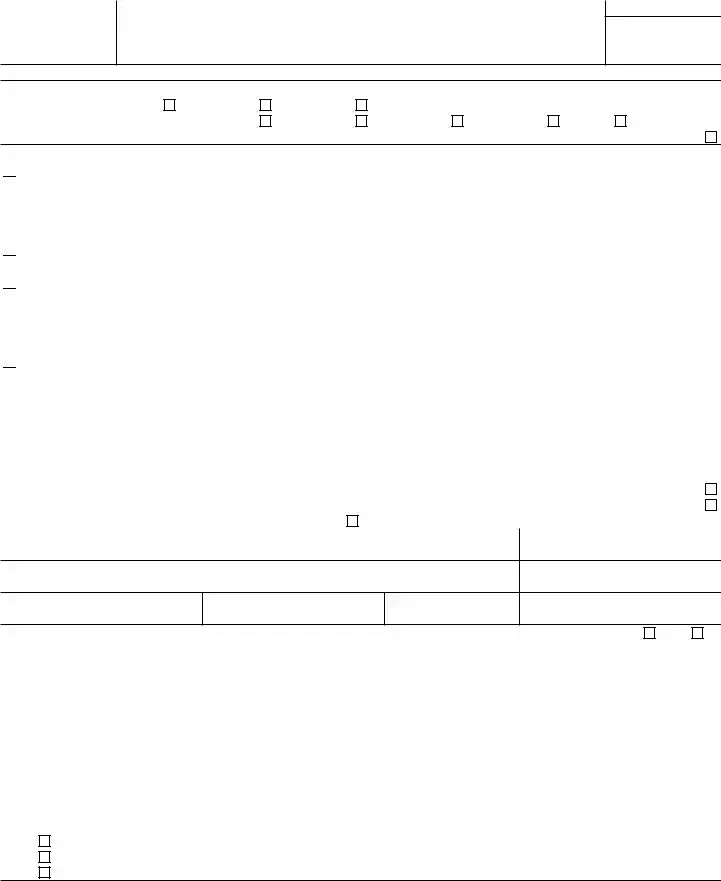

Part I Transfers by U.S. Persons to a Foreign Trust During the Current Tax Year (see instructions)

5a Name of trust creator

bAddress

cTIN, if any

6a Country code of country where trust was created

bCountry code of country whose law governs the trust

cDate trust was created

7a Will any person (other than the foreign trust) be treated as the owner of the transferred assets after the transfer? . . . . |

Yes |

No |

b(i)

Name of foreign

trust owner

(ii)

Address

(iii)

Country of residence

(iv)

TIN, if any

(v)

Relevant Code

section

8 |

Was the transfer a completed gift or bequest? If “Yes,” see instructions |

|

Yes |

|

No |

9a |

Now or at any time in the future, can any part of the income or corpus of the trust benefit any U.S. beneficiary? . . . . |

|

Yes |

|

No |

b |

If “No,” could the trust be revised or amended to benefit a U.S. beneficiary? |

|

Yes |

|

No |

10 |

Reserved for future use |

|

Yes |

|

No |

|

|

Schedule

11a During the current tax year, did you transfer property (including cash) to a related foreign trust in exchange for an obligation of the trust or an obligation of a person related to the trust? See instructions . . . . . . . . . . . . . .

If “Yes,” complete the rest of Schedule A, as applicable. If “No,” go to Schedule B.

bWere any of the obligations you received (with respect to a transfer described in line 11a above) qualified obligations? . .

If “Yes,” complete the rest of Schedule A and attach a copy of each loan document entered into with respect to each qualified obligation reported on line 11b. If these documents have been attached to a Form 3520 filed within the previous 3 years, attach only relevant updates.

If “No,” go to Schedule B.

Yes

Yes  No

No

Yes

Yes  No

No

(i)

Date of transfer giving rise to obligation

(ii)

Maximum term

(iii)

Yield to maturity

(iv)

FMV of obligation

12With respect to each qualified obligation you reported on line 11b, do you agree to extend the period of assessment of any income or transfer tax attributable to the transfer, and any consequential income tax changes for each year that the

obligation is outstanding, to a date 3 years after the maturity date of the obligation? |

Yes |

No |

Note: You have the right to refuse to extend the period of limitations or limit this extension to a mutually |

|

|

issue(s) or mutually |

|

|

each qualified obligation you reported on line 11b, then such obligation is not a qualified obligation and you cannot check |

|

|

“Yes” to the question on line 11b. |

|

|

Schedule

13During the current tax year, did you make any transfers (directly or indirectly) to the trust and receive less than FMV, or no

consideration at all, for the property transferred? |

. . . . . . . . . . . . . |

. . . . . . . . . |

Yes |

No |

||||||

If “Yes,” complete columns (a) through (i) below and the rest of Schedule B, as applicable. When completing columns (a) |

|

|

||||||||

through (i) with respect to each nonqualified obligation, enter |

|

|

|

|

||||||

If “No,” go to Schedule C. |

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

(a) |

(b) |

(c) |

(d) |

|

(e) |

(f) |

(g) |

(h) |

(i) |

|

Date of |

Description |

FMV of property |

U.S. adjusted |

Gain recognized |

Excess, if any, |

Description |

FMV of property |

Excess of |

|

|

transfer |

of property |

transferred |

basis of |

|

at time of |

of column (c) |

of property |

received |

column (c) over |

|

|

transferred |

|

property |

|

transfer, |

over the sum of |

received, |

|

column (h) |

|

|

|

|

transferred |

|

if any |

columns (d) and (e) |

if any |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Totals ▶ |

|

|

|

|

|

$ |

|

|

$ |

|

14You are required to attach a copy of each sale or loan document entered into in connection with a transfer reported on line 13. If these documents have been attached to a Form 3520 filed within the previous 3 years, attach only relevant updates.

|

|

|

|

Attached |

Year |

|

Are you attaching a copy of any of the following? |

Yes |

No |

Previously |

Attached |

a |

Sale document |

|

|

|

|

b |

Loan document |

|

|

|

|

c |

Subsequent variances to original sale or loan documents |

|

|

|

|

Form 3520 (2020)

Form 3520 (2020) |

Page 3 |

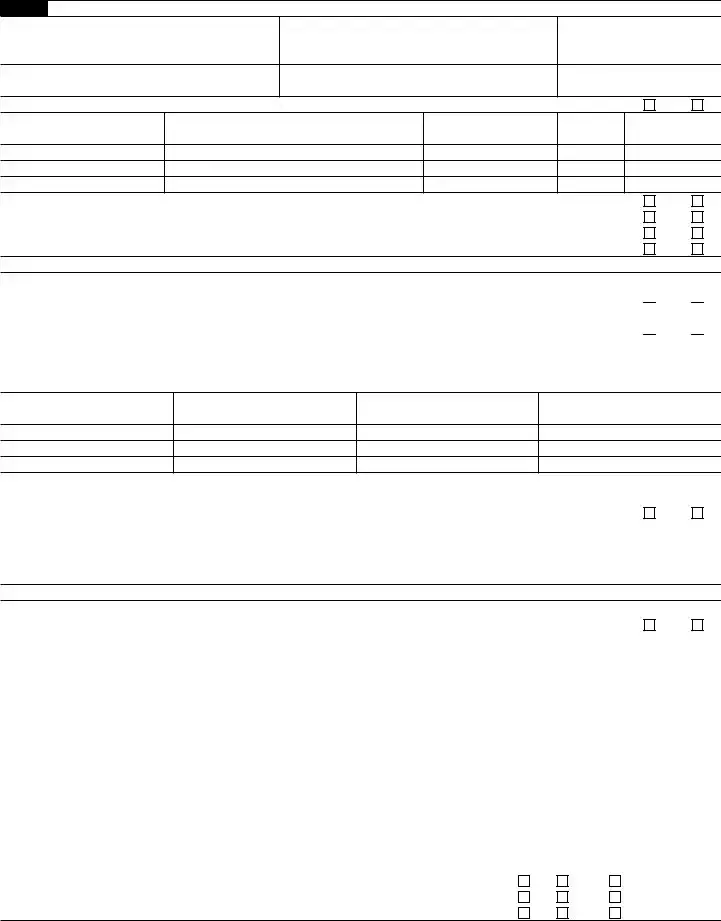

Part I Schedule

Note: Complete lines 15 through 18 only if you answered “No” to line 3, acknowledging that the foreign trust did not appoint a U.S. agent to provide the IRS with all relevant trust information.

15 |

(a) |

(b) |

|

(c) |

|

(d) |

|

|

Name of beneficiary |

Address of beneficiary |

|

U.S. beneficiary? |

TIN, if any |

||

|

|

|

|

|

|

|

|

|

|

|

|

Yes |

|

No |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

16 |

(a) |

(b) |

|

|

|

|

(c) |

|

Name of trustee |

Address of trustee |

|

|

|

|

TIN, if any |

|

|

|

|

|

|

||

|

|

|

|

|

|

||

|

|

|

|

|

|

||

|

|

|

|

|

|

||

|

|

|

|

|

|

||

17 |

(a) |

(b) |

(c) |

|

(d) |

||

|

Name of other person |

Address of other person with trust powers |

Description of powers |

|

TIN, if any |

||

|

with trust powers |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18If you checked “No” on line 3, you are required to attach a copy of all trust documents as indicated below. If these documents have been attached to a Form

|

|

|

|

Attached |

Year |

|

Are you attaching a copy of any of the following? |

Yes |

No |

Previously |

Attached |

a |

Summary of all written and oral agreements and understandings relating to the trust . . . . |

|

|

|

|

b |

Trust instrument |

|

|

|

|

c |

Memoranda or letters of wishes |

|

|

|

|

d |

Subsequent variances to original trust documents |

|

|

|

|

e |

Trust financial statements |

|

|

|

|

f |

Organizational chart and other trust documents |

|

|

|

|

Schedule

19Did you, at any time during your tax year, hold an outstanding obligation of a related foreign trust (or a person related to the

trust) that you reported as a qualified obligation in the current tax year? |

Yes |

No |

If “Yes,” complete columns (a) through (f) below for each obligation. |

|

|

(a)

Date of original

obligation

(b)

Tax year qualified

obligation first reported

(c)

Amount of principal

payments made during

your tax year

(d)

Amount of interest

payments made during

your tax year

(e)

Balance of the outstanding

obligation at the end

of the tax year

(f)

Does the obligation

still meet the criteria for a qualified obligation?

Yes |

No |

Form 3520 (2020)

Form 3520 (2020) |

|

|

|

|

|

|

Page 4 |

|||

Part II |

U.S. Owner of a Foreign Trust (see instructions) |

|

|

|

|

|

||||

20 |

|

(a) |

|

|

(b) |

(c) |

(d) |

|

(e) |

|

|

|

Name of foreign |

|

Address |

Country of tax residence |

TIN, if any |

|

Relevant Code |

||

|

|

trust owner |

|

|

section |

|

||||

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|||

21a |

Country code of country where foreign trust was created |

|

b Country code of country whose law governs the trust |

c Date foreign trust was created |

||||||

|

|

|

|

|

|

|||||

22 |

Did the foreign trust file Form |

. . . . . |

Yes |

No |

||||||

|

If “Yes,” attach the Foreign Grantor Trust Owner Statement you received from the foreign trust. |

|

|

|

|

|||||

|

If “No,” to the best of your ability, complete and attach a substitute Form |

|

|

|

|

|||||

|

See instructions for information on penalties for failing to complete and attach a substitute Form |

|

|

|

|

|||||

23Enter the gross value of the portion of the foreign trust that you are treated as owning at the end of your tax year . ▶ $

Part III Distributions to a U.S. Person From a Foreign Trust During the Current Tax Year (see instructions)

Note: If you received an amount from a portion of a foreign trust of which you are treated as the owner, only complete lines 24 and 27.

24Enter cash amounts or FMV of property received, directly or indirectly, during your current tax year, from the foreign trust (exclude loans and uncompensated use of trust property included on line 25).

(a) |

(b) |

(c) |

(d) |

(e) |

(f) |

Date of distribution |

Description of property received |

FMV of property received |

Description of property |

FMV of property |

Excess of column (c) |

|

|

(determined on date |

transferred, if any |

transferred |

over column (e) |

|

|

of distribution) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ▶ $ |

25During your current tax year, did you (or a person related to you) receive a loan or uncompensated use of trust property from a

related foreign trust (including an extension of credit upon the purchase of property from the trust)? |

Yes |

No |

If “Yes,” complete columns (a) through (g) below for each such loan or use of trust property. |

|

|

Note: See instructions for additional information, including how to complete columns (a) through (g) for use of trust property.

(a) |

(b) |

(c) |

(d) |

|

(e) |

(f) |

(g) |

|

Is the obligation a |

Amount treated as |

|||||||

FMV of loan proceeds |

Date of original |

Maximum term of |

Interest rate |

qualified obligation? |

FMV of qualified |

distribution from the trust |

||

or property |

transaction |

repayment of |

of obligation |

|

|

|

obligation |

(subtract column (f) |

|

|

obligation |

|

Yes |

|

No |

|

from column (a)) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . ▶ $ |

26With respect to each obligation you reported as a qualified obligation on line 25, do you agree to extend the period of assessment of any income or transfer tax attributable to the transaction, and any consequential income tax changes for each

year that the obligation is outstanding, to a date 3 years after the maturity date of the obligation? . . . |

. |

. |

. |

. . . |

Yes |

No |

|

Note: You have the right to refuse to extend the period of limitations or limit this extension to a mutually |

|

|

|||||

or mutually |

|

|

|||||

that you reported as a qualified obligation on line 25, then such obligation is not a qualified obligation and you cannot check |

|

|

|||||

“Yes” in column (e) of line 25. |

|

|

|

|

|

|

|

27 Total distributions received during your current tax year. Add line 24, column (f), and line 25, column (g) . |

. |

. |

. |

▶ $ |

|

|

|

|

|

|

|

|

|

|

|

28Did the trust, at any time during the current tax year, hold an outstanding obligation of yours (or a person related to you) that

you reported as a qualified obligation? |

Yes |

No |

If “Yes,” complete columns (a) through (f) below for each obligation. |

|

|

(a) |

(b) |

(c) |

(d) |

Date of original |

Tax year qualified |

Amount of principal payments |

Amount of interest payments |

loan transaction |

obligation first |

made during your tax year |

made during your tax year |

|

reported |

|

|

(e)

Balance of the outstanding

obligation at the end

of the tax year

(f)

Does the loan still

meet the criteria of a qualified obligation?

Yes |

No |

Form 3520 (2020)

Form 3520 (2020) |

Page 5 |

Part III Distributions to a U.S. Person From a Foreign Trust During the Current Tax Year (continued)

29Did you receive a Foreign Grantor Trust Beneficiary Statement from the foreign trust with respect to a distribution? If “Yes,” attach the statement and do not complete the remainder of Part III with respect to that distribution.

If “No,” complete Schedule A with respect to that distribution. Also, complete Schedule C if you enter an amount greater than zero on line 37.

30Did you receive a Foreign Nongrantor Trust Beneficiary Statement from the foreign trust with respect to a distribution?

If “Yes,” attach the statement and complete either Schedule A or Schedule B below. See instructions. Also, complete Schedule C if you enter an amount greater than zero on line 37 or line 41a.

If “No,” complete Schedule A with respect to that distribution. Also, complete Schedule C if you enter an amount greater than zero on line 37.

Yes

Yes

Yes

Yes

No

No  N/A

N/A

No

No  N/A

N/A

Schedule

31 |

Enter amount from line 27 |

. . . . . . . . . |

|

31 |

|

32 |

Number of years the trust has been a foreign trust (see instructions) . . . ▶ |

32 |

|

|

|

33Enter total distributions received from the foreign trust during the 3 preceding tax years (or during the number

|

of years the trust has been a foreign trust, if fewer than 3 years) |

33 |

34 |

Multiply line 33 by 1.25 |

34 |

35Average distribution. Divide line 34 by 3.0 (or the number of years the trust has been a foreign trust, if fewer

|

than 3 years) and enter the result |

35 |

|

36 |

Amount treated as ordinary income earned in the current year. Enter the smaller of line 31 or line 35 . . . |

36 |

|

37 |

Amount treated as accumulation distribution. Subtract line 36 from line 31. If zero, do not complete the rest of Part III |

37 |

|

38 |

Applicable number of years of trust. Divide line 32 by 2.0 and enter the result here ▶ |

38 |

|

Schedule

39 |

Enter amount from line 27 |

|||

40a |

Amount treated as ordinary income in the current tax year |

|||

b |

Qualified dividends |

. . . . . . . . . . . ▶ |

40b |

|

41a |

Amount treated as accumulation distribution. If zero, do not complete Schedule C, Part III |

|||

b |

Amount of line 41a that is tax exempt . |

. . . . . . . . . . . ▶ |

41b |

|

42a |

Amount treated as net |

|||

b |

Amount treated as net |

|||

c |

28% rate gain |

. . . . . . . . . . . ▶ |

42c |

|

d |

Unrecaptured section 1250 gain . . |

. . . . . . . . . . . ▶ |

42d |

|

43 |

Amount treated as distribution from trust corpus |

|||

44Enter any other distributed amount received from the foreign trust not included on lines 40a, 41a, 42a, 42b,

|

and 43. (Attach explanation.) |

45 |

Amount of foreign trust’s aggregate undistributed net income |

46 |

Amount of foreign trust’s weighted undistributed net income |

47Applicable number of years of trust. Divide line 46 by line 45 and enter the result

here . . . . . . . . . . . . . . . . . . . . . . ▶ |

47 |

Schedule

39

40a

41a

42a

42b

43

44

45

46

48 |

Enter accumulation distribution from line 37 or line 41a, as applicable |

48 |

49 |

Enter tax on total accumulation distribution from line 28 of Form 4970. (Attach Form |

49 |

50Enter applicable number of years of foreign trust from line 38 or line 47, as

|

applicable (round to nearest half year) . . . . . . . . . . . . ▶ |

50 |

|

|

51 |

Combined interest rate imposed on the total accumulation distribution (see instructions) |

|

51 |

|

52 |

Interest charge. Multiply the amount on line 49 by the combined interest rate on line 51 |

52 |

||

53Tax attributable to accumulation distributions. Add lines 49 and 52. Enter here and as “additional tax” on your

income tax return |

53 |

Form 3520 (2020)

Form 3520 (2020) |

Page 6 |

Part IV U.S. Recipients of Gifts or Bequests Received During the Current Tax Year From Foreign Persons (see instructions)

54During your current tax year, did you receive more than $100,000 that you treated as gifts or bequests from a nonresident

alien (including a distribution received from a domestic trust treated as owned by a foreign person) or a foreign estate? See |

Yes |

No |

|||||||||||||

instructions for special rules regarding related donors |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. . . |

|||||

If “Yes,” complete columns (a) through (c) with respect to each such gift or bequest in excess of $5,000. If more space is |

|

|

|||||||||||||

needed, attach a statement. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(a) |

|

(b) |

|

|

|

|

|

|

|

|

|

|

|

(c) |

|

Date of gift or bequest |

|

Description of property received |

|

|

|

|

|

|

|

|

|

|

FMV of property received |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

. |

. |

. |

. |

. |

. |

. |

. |

. |

▶ |

$ |

|

|

||

55During your current tax year, did you receive more than $16,649 that you treated as gifts from a foreign corporation or a foreign partnership (including a distribution received from a domestic trust treated as owned by a foreign person)? See

|

|

instructions regarding related donors |

. . . . . |

. . . |

Yes |

No |

||||||||||||

|

|

If “Yes,” complete columns (a) through (g) with respect to each such gift. If more space is needed, attach a statement. |

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(a) |

|

(b) |

|

|

|

|

(c) |

|

|

|

|

(d) |

|

|||

|

Date of gift |

|

Name of foreign donor |

|

|

|

|

Address of foreign donor |

|

|

|

|

TIN, if any |

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(e) |

|

|

|

|

|

|

(f) |

|

|

|

|

(g) |

|

||

Check the box that applies to the foreign donor |

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

Description of property received |

|

|

|

FMV of property received |

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

Corporation |

|

Partnership |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

56 |

|

Do you have any reason to believe that the foreign donor, in making any gift or bequest described in lines 54 and 55, was |

|

|

||||||||||||||

|

|

acting as a nominee or intermediary for any other person? If “Yes,” see instructions . . . . |

. . . . . |

. . . |

Yes |

No |

||||||||||||

|

|

Under penalties of perjury, I declare that I have examined this return, including any accompanying reports, schedules, or statements, and to the best of my |

|

|||||||||||||||

Sign |

|

knowledge and belief, it is true, correct, and complete. |

|

|

|

|

|

|

|

|

|

|

||||||

Here |

▲ |

|

|

|

|

|

|

|

▲ |

|

|

|

|

▲ |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

Signature |

|

|

|

|

|

Title |

|

|

Date |

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Paid |

|

|

Print/Type preparer’s name |

Preparer’s signature |

|

|

|

Date |

|

Check |

if |

PTIN |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Preparer |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Firm’s name |

▶ |

|

|

|

|

|

|

|

Firm’s EIN ▶ |

|

|

|

||||||

Use Only |

|

|

|

|

|

|

|

|

|

|

||||||||

Firm’s address ▶ |

|

|

|

|

|

|

|

Phone no. |

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Form 3520 (2020) |

|

| Fact Name | Description |

|---|---|

| Purpose | The IRS Form 3520 is used to report certain transactions with foreign trusts and receipts of certain foreign gifts. |

| Who Needs to File | U.S. persons, including citizens and residents, must file this form if they receive gifts over a certain amount from foreign individuals or if they have foreign trust transactions. |

| Filing Deadline | The form is due on the 15th day of the 4th month after the end of the taxpayer's tax year. Extensions may apply. |

| Penalties for Non-Compliance | If you fail to file, fines can be substantial, reaching up to 35% of the amount involved. |

| Foreign Gift Limits | For 2023, you must report gifts over $100,000 from foreign individuals or over $16,649 if it’s from foreign estates or corporations. |

| Governing Law | This form is governed primarily by the Internal Revenue Code, particularly sections 6048 and 6039F. |

Once you gather all necessary documents, you will be ready to complete the IRS Form 3520. This form requires specific information regarding foreign trusts and transactions with foreign corporations. Take your time while filling it out to ensure accuracy.

The IRS Form 3520 is used to report certain transactions with foreign trusts and the receipt of foreign gifts. This form helps the IRS track overseas financial activities to ensure compliance with U.S. tax laws.

You need to file Form 3520 if you are a U.S. person and you:

Form 3520 is due on the 15th day of the 4th month following the end of the tax year. For most people, this means it is usually due by April 15. If you file for an extension for your federal tax return, it will also apply to Form 3520.

If you fail to file Form 3520 when required, you may face significant penalties. The IRS may impose a penalty of up to 35% of the amount received from foreign trusts or gifts not reported. Other penalties may also apply depending on your specific situation.

The form requires detailed information, including:

As of now, the IRS does not allow electronic filing of Form 3520. You must print it out, complete it, and mail it to the appropriate address based on your location.

Form 3520 must be completed using the official IRS form format. Follow the instructions provided with the form carefully to ensure all required information is included and accurately reported.

If you receive a notice from the IRS regarding Form 3520, it is important to read it carefully. The notice may ask for additional information or confirm that you have not filed the form. Respond in a timely manner and consult with a tax professional if needed.

You may find information and resources on the official IRS website. Additionally, consulting a tax professional or an attorney who specializes in international tax issues can provide you with personalized assistance.

Filling out the IRS Form 3520 can be a daunting task, and mistakes often occur. One common error is failing to file the form altogether. Individuals may overlook the requirement if they are not fully aware of their obligations regarding foreign trusts or gifts. Thus, it is important to understand when the form is necessary to avoid penalties.

Another mistake frequently made is misreporting specific amounts. When individuals fail to accurately report the value of gifts or distributions, they risk facing significant monetary fines. It is essential to carefully calculate any amounts being reported on the form to ensure accuracy.

Many also neglect to include all necessary documentation. The IRS requires that certain additional forms and information accompany the 3520. Without the proper attachments, the form is incomplete, which can trigger further inquiries from the IRS.

Some filers incorrectly assume that they can submit their form without an accompanying explanation for any discrepancies. Clear explanations regarding foreign trusts or gifts help establish context and may mitigate potential issues. Supporting documentation may also fortify one’s case during any audits.

Using the wrong form version is another prevalent error. People sometimes mistakenly refer to older versions of the form, leading to potential compliance problems. It is crucial to ensure that the most current version of the form is used at the time of submission.

In addition, individuals may be unaware of deadlines for filing. Delays can lead to late fees, so understanding all relevant timelines is vital. Planning ahead and knowing when the form is due can help avoid unnecessary stress.

A frequent oversight involves not signing the form correctly. A form that is not signed, or is signed incorrectly, is considered invalid. This seemingly small detail can delay processing and create additional complications.

Lastly, inadequate record-keeping often proves detrimental. Many individuals fail to maintain appropriate records related to foreign gifts or trusts that might be necessary for their future filings. Keeping thorough documentation can be invaluable in providing evidence if questions arise later.

The IRS Form 3520 serves as an essential document for U.S. taxpayers reporting certain transactions with foreign trusts and receipt of foreign gifts. Due to the complexity of international financial regulations, several other forms and documents are frequently used in conjunction with Form 3520. These documents help ensure compliance with tax obligations and provide comprehensive reporting of foreign financial interests.

These forms and documents collectively support U.S. taxpayers in fulfilling their reporting obligations regarding foreign trusts and assets. Being aware of and compliant with each requirement is critical for mitigating potential penalties and ensuring accurate tax reporting.

The IRS Form 3520 relates to the reporting of certain transactions with foreign trusts and the receipt of foreign gifts. Here are five documents that share similarities with Form 3520:

When filling out the IRS 3520 form, it’s essential to follow certain practices to ensure that the submission is accurate and complete. Here are ten things you should and shouldn't do:

The IRS Form 3520, known as the Annual Return to Report Transactions with Foreign Trusts and Receipt of Certain Foreign Gifts, is often misunderstood. Here are some common misconceptions about this form:

This is incorrect. Both U.S. citizens and resident aliens must file Form 3520 if they engage in certain transactions with foreign trusts or receive foreign gifts above specific thresholds.

Filing is not optional. Even if no tax is owed, failure to file may result in significant penalties. It's essential to adhere to reporting requirements to avoid such consequences.

This is a common misunderstanding. Form 3520-A is specifically for foreign trusts, while Form 3520 is for U.S. persons. Each serves different purposes and has distinct filing requirements.

This is misleading. Form 3520 has its own filing deadline, which may differ from that of the standard income tax return. It's crucial to be aware of the specific due dates for compliance.

When dealing with the IRS 3520 form, there are several important points to keep in mind. This form is used to report certain transactions with foreign trusts and the receipt of certain foreign gifts. It's essential to fill it out correctly to avoid penalties. Here are some key takeaways: