The IRS 3800 form, also known as the General Business Credit form, plays a pivotal role for business owners and self-employed individuals seeking to leverage a range of tax credits. This form consolidates various business credits that a taxpayer can claim, allowing for a more streamlined approach to tax benefits. Claiming the credits on this form could lead to substantial reductions in tax liability, providing essential relief and support for businesses. It encompasses credits like the investment credit, the work opportunity credit, and many others that incentivize hiring, investment, and R&D activities. Understanding how to properly complete the IRS 3800 is crucial for maximizing potential tax savings. Moreover, failing to accurately claim these credits can lead to missed opportunities and financial loss. Organizing relevant documentation and thoroughly understanding eligibility requirements can significantly enhance one’s chances of successfully benefiting from these advantages.

Form 3800 |

General Business Credit |

|

OMB No. |

|

|

||

|

|

|

|

|

|

|

|

Department of the Treasury |

▶ Go to www.irs.gov/Form3800 for instructions and the latest information. |

2020 |

|

▶ You must attach all pages of Form 3800, pages 1, 2, and 3, to your tax return. |

|

Attachment |

|

Internal Revenue Service (99) |

|

Sequence No. 22 |

|

Name(s) shown on return |

|

Identifying |

number |

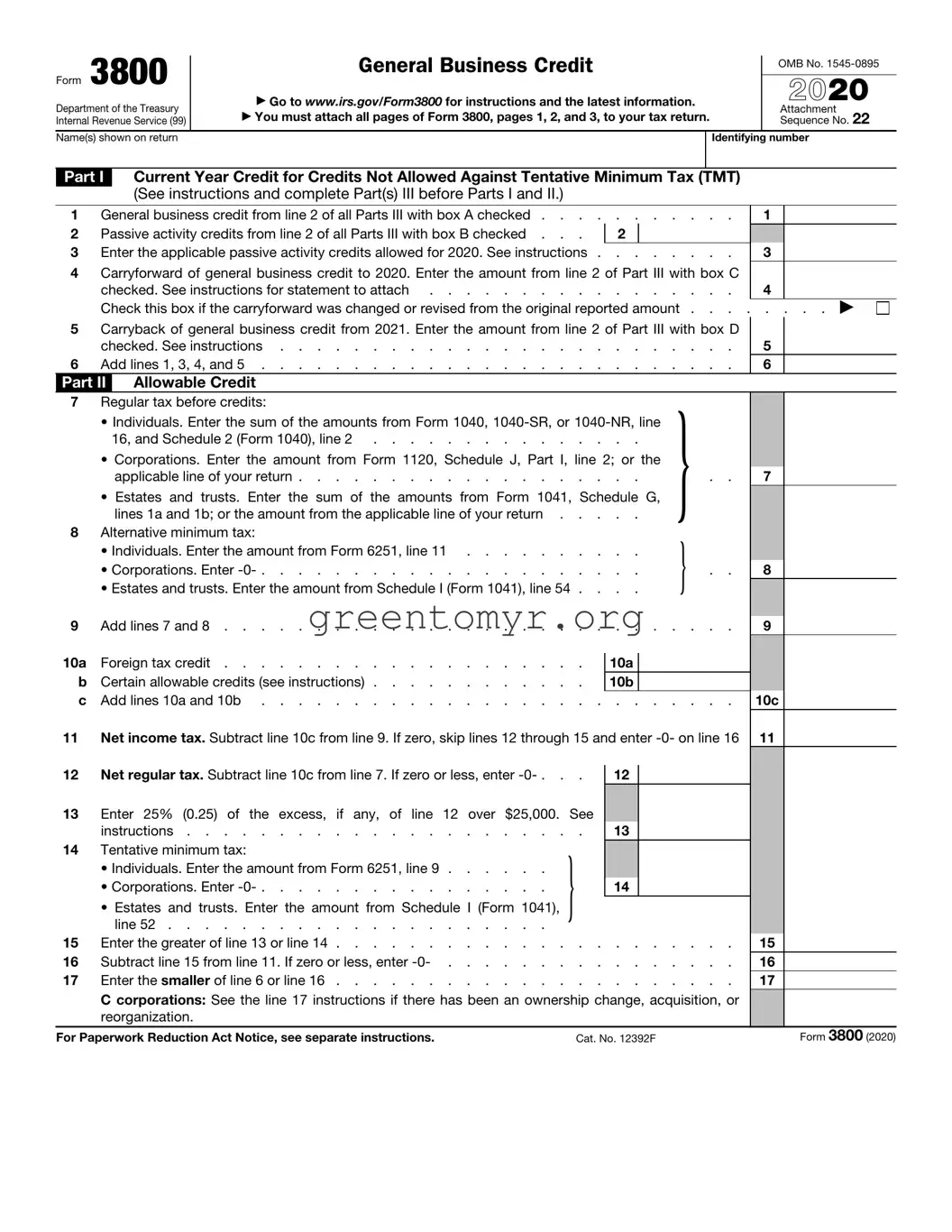

Part I Current Year Credit for Credits Not Allowed Against Tentative Minimum Tax (TMT)

(See instructions and complete Part(s) III before Parts I and II.)

1 |

General business credit from line 2 of all Parts III with box A checked . . . . |

. . . . . . . |

1 |

|

|

2 |

Passive activity credits from line 2 of all Parts III with box B checked . . . |

2 |

|

|

|

3 |

Enter the applicable passive activity credits allowed for 2020. See instructions . |

. . . . . . . |

3 |

|

|

4Carryforward of general business credit to 2020. Enter the amount from line 2 of Part III with box C

checked. See instructions for statement to attach |

|

4 |

Check this box if the carryforward was changed or revised from the original reported amount . . . |

. . . . . ▶ |

|

5Carryback of general business credit from 2021. Enter the amount from line 2 of Part III with box D

|

checked. See instructions |

. . . . |

. . . . |

5 |

|

||||

6 |

Add lines 1, 3, 4, and 5 |

. . . . |

. . . . |

6 |

|

||||

Part II |

Allowable Credit |

|

|

|

|

|

|

|

|

7 |

Regular tax before credits: |

|

|

|

} |

|

|

|

|

|

• Individuals. Enter the sum of the amounts from Form 1040, |

|

|

|

|||||

|

|

16, and Schedule 2 (Form 1040), line 2 |

|

|

|

||||

|

• Corporations. Enter the amount from Form 1120, Schedule J, Part I, line 2; or the |

|

|

|

|||||

|

|

applicable line of your return |

. . . |

|

. . |

7 |

|

||

|

• |

Estates and trusts. Enter the sum of the amounts from Form 1041, Schedule G, |

|

|

|

||||

8 |

lines 1a and 1b; or the amount from the applicable line of your return . . |

. . . |

|

|

|

|

|||

Alternative minimum tax: |

|

|

|

} |

|

|

|

||

|

• Individuals. Enter the amount from Form 6251, line 11 |

|

|

|

|||||

|

• Corporations. Enter |

. . . |

|

. . |

8 |

|

|||

|

• Estates and trusts. Enter the amount from Schedule I (Form 1041), line 54 . |

. . . |

|

|

|

|

|||

|

|

|

|

|

|

|

|

||

9 |

Add lines 7 and 8 |

. . . . |

. . . . |

9 |

|

||||

|

|

|

|

|

|

|

|

||

10a |

Foreign tax credit |

|

10a |

|

|

|

|

|

|

b |

Certain allowable credits (see instructions) |

|

10b |

|

|

|

|

|

|

c |

Add lines 10a and 10b |

. . . . |

. . . . |

10c |

|||||

11 |

Net income tax. Subtract line 10c from line 9. If zero, skip lines 12 through 15 and enter |

11 |

|

||||||

12 |

Net regular tax. Subtract line 10c from line 7. If zero or less, enter |

12 |

|

|

|

|

|

||

13Enter 25% (0.25) of the excess, if any, of line 12 over $25,000. See

|

instructions |

. |

13 |

|

|

|

|

14 |

Tentative minimum tax: |

} |

|

|

|

|

|

|

• Individuals. Enter the amount from Form 6251, line 9 |

|

|

|

|

|

|

|

• Corporations. Enter |

14 |

|

|

|

|

|

|

• Estates and trusts. Enter the amount from Schedule I (Form 1041), |

|

|

|

|

|

|

|

line 52 |

|

|

|

|

|

|

15 |

Enter the greater of line 13 or line 14 |

. . . . . . . . . |

|

15 |

|

||

16 |

Subtract line 15 from line 11. If zero or less, enter |

. . . . . . . . . |

|

16 |

|

||

17 |

Enter the smaller of line 6 or line 16 |

. . . . . . . . . |

|

17 |

|

||

|

C corporations: See the line 17 instructions if there has been an ownership change, acquisition, or |

|

|

||||

|

reorganization. |

|

|

|

|

|

|

For Paperwork Reduction Act Notice, see separate instructions. |

Cat. No. 12392F |

|

Form 3800 (2020) |

||||

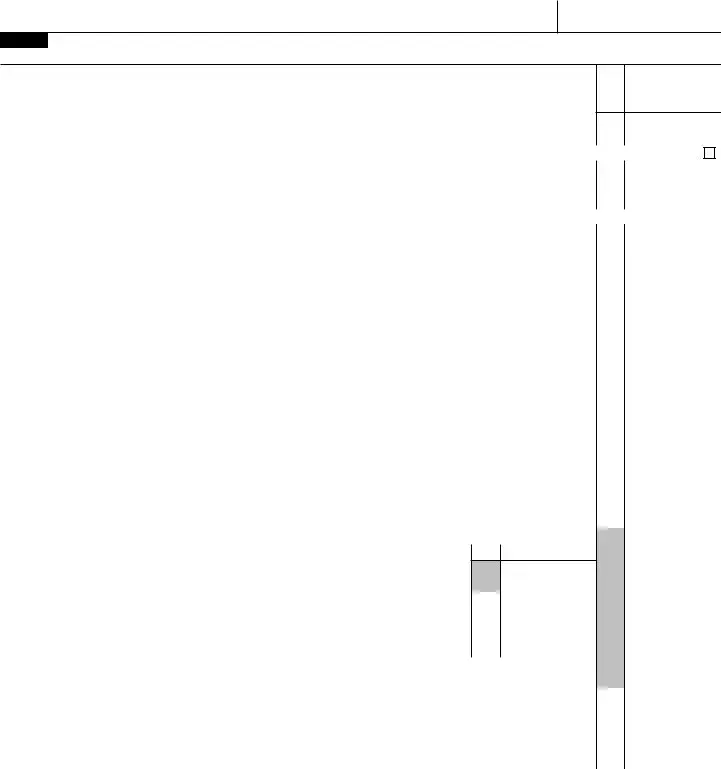

Form 3800 (2020) |

Page 2 |

Part II Allowable Credit (continued)

Note: If you are not required to report any amounts on line 22 or 24 below, skip lines 18 through 25 and enter

18 |

Multiply line 14 by 75% (0.75). See instructions |

. . . . . . . . |

18 |

|

||

19 |

Enter the greater of line 13 or line 18 |

. . . . . . . . |

19 |

|

||

20 |

Subtract line 19 from line 11. If zero or less, enter |

. . . . . . . . |

20 |

|

||

21 |

Subtract line 17 from line 20. If zero or less, enter |

. . . . . . . . |

21 |

|

||

22 |

Combine the amounts from line 3 of all Parts III with box A, C, or D checked . |

. . . . . . . . |

22 |

|

||

23 |

Passive activity credit from line 3 of all Parts III with box B checked . . . |

|

23 |

|

|

|

|

|

|

|

|||

24 |

Enter the applicable passive activity credit allowed for 2020. See instructions |

. . . . . . . . |

24 |

|

||

25 |

Add lines 22 and 24 |

. . . . . . . . |

25 |

|

||

26Empowerment zone and renewal community employment credit allowed. Enter the smaller of line 21

|

or line 25 |

. . . . . . . |

26 |

|

||

27 |

Subtract line 13 from line 11. If zero or less, enter |

. . . . . . . |

27 |

|

||

28 |

Add lines 17 and 26 |

. . . . . . . |

28 |

|

||

29 |

Subtract line 28 from line 27. If zero or less, enter |

. . . . . . . |

29 |

|

||

30 |

Enter the general business credit from line 5 of all Parts III with box A checked . |

. . . . . . . |

30 |

|

||

31 |

Reserved |

. . . . . . . |

31 |

|

||

|

||||||

32 |

Passive activity credits from line 5 of all Parts III with box B checked . . . |

|

32 |

|

|

|

|

|

|

|

|||

33 |

Enter the applicable passive activity credits allowed for 2020. See instructions . |

. . . . . . . |

33 |

|

||

34Carryforward of business credit to 2020. Enter the amount from line 5 of Part III with box C checked

and line 6 of Part III with box G checked. See instructions for statement to attach |

|

34 |

Check this box if the carryforward was changed or revised from the original reported amount . . . |

. . . . . ▶ |

|

35Carryback of business credit from 2021. Enter the amount from line 5 of Part III with box D checked.

|

See instructions |

. . |

35 |

|

|

36 |

Add lines 30, 33, 34, and 35 |

. . |

36 |

|

|

37 |

Enter the smaller of line 29 or line 36 |

. . |

37 |

|

|

38 |

Credit allowed for the current year. Add lines 28 and 37. |

|

|

|

|

|

Report the amount from line 38 (if smaller than the sum of Part I, line 6, and Part II, lines 25 and 36, |

|

|

||

|

see instructions) as indicated below or on the applicable line of your return. |

} |

|

|

|

|

• Individuals. Schedule 3 (Form 1040), line 6 |

|

|

|

|

|

• Corporations. Form 1120, Schedule J, Part I, line 5c |

. . |

|

|

|

|

• Estates and trusts. Form 1041, Schedule G, line 2b |

|

38 |

|

|

Form 3800 (2020)

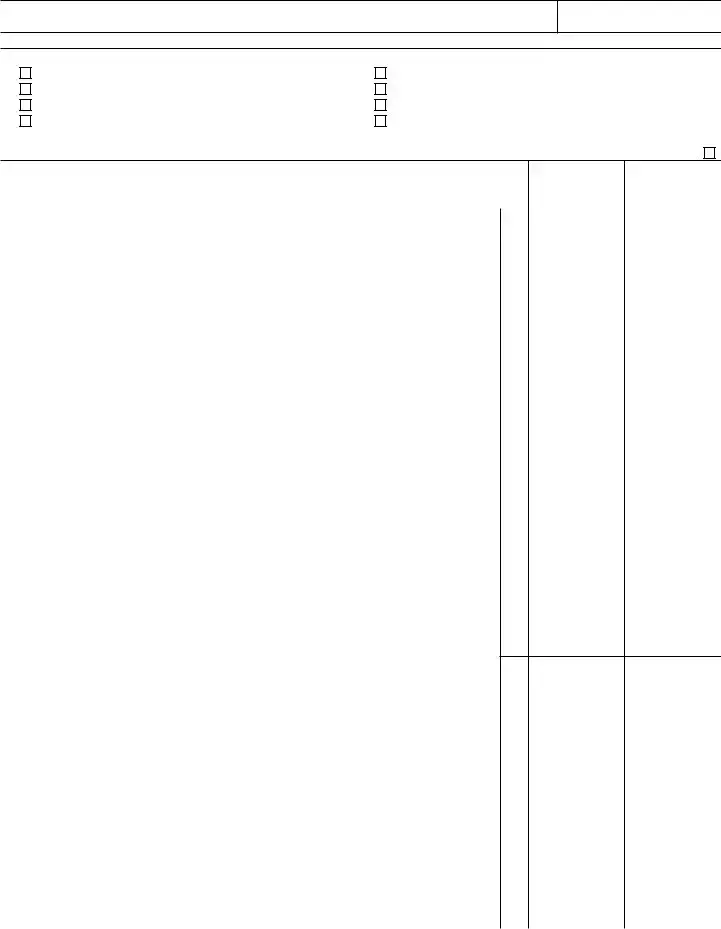

Form 3800 (2020) |

Page 3 |

Name(s) shown on return

Part III General Business Credits or Eligible Small Business Credits (see instructions)

Identifying number

Complete a separate Part III for each box checked below. See instructions.

A |

General Business Credit From a |

E |

|

Reserved |

|

||||

B |

General Business Credit From a Passive Activity |

F |

|

Reserved |

|

||||

C |

General Business Credit Carryforwards |

G |

|

Eligible Small Business Credit Carryforwards |

D |

General Business Credit Carrybacks |

H |

|

Reserved |

|

IIf you are filing more than one Part III with box A or B checked, complete and attach first an additional Part III combining amounts from

all Parts III with box A or B checked. Check here if this is the consolidated Part III . . . . . . . . . . . . . . . . ▶

|

(a) Description of credit |

|

(b) Enter EIN if |

(c) Enter the |

Note: On any line where the credit is from more than one source, a separate Part III is needed for each |

|

claiming the credit |

appropriate |

|

|

from a |

amount. |

||

|

||||

|

entity. |

|

||

1a |

Investment (Form 3468, Part II only) (attach Form 3468) |

1a |

|

|

b |

Reserved |

1b |

|

|

c |

Increasing research activities (Form 6765) |

1c |

|

|

d |

1d |

|

||

e |

Disabled access (Form 8826)* |

1e |

|

|

f |

Renewable electricity, refined coal, and Indian coal production (Form 8835) . . |

1f |

|

|

g |

Indian employment (Form 8845) |

1g |

|

|

h |

Orphan drug (Form 8820) |

1h |

|

|

i |

New markets (Form 8874) |

1i |

|

|

j |

Small employer pension plan startup costs and |

1j |

|

|

k |

1k |

|

||

l |

Biodiesel and renewable diesel fuels (attach Form 8864) |

1l |

|

|

m |

Low sulfur diesel fuel production (Form 8896) |

1m |

|

|

n |

Distilled spirits (Form 8906) |

1n |

|

|

o |

Nonconventional source fuel (carryforward only) |

1o |

|

|

p |

Energy efficient home (Form 8908) |

1p |

|

|

q |

Energy efficient appliance (carryforward only) |

1q |

|

|

r |

Alternative motor vehicle (Form 8910) |

1r |

|

|

s |

Alternative fuel vehicle refueling property (Form 8911) |

1s |

|

|

t |

Enhanced oil recovery credit (carryforward only) |

1t |

|

|

u |

Mine rescue team training (Form 8923) |

1u |

|

|

v |

Agricultural chemicals security (carryforward only) |

1v |

|

|

w |

Employer differential wage payments (Form 8932) |

1w |

|

|

x |

Carbon oxide sequestration (Form 8933) |

1x |

|

|

y |

Qualified |

1y |

|

|

z |

Qualified |

1z |

|

|

aa |

Employee retention (Form |

1aa |

|

|

bb |

General credits from an electing large partnership (carryforward only) . . . . |

1bb |

|

|

zzOther. Oil and gas production from marginal wells (Form 8904) and certain other

|

credits (see instructions) |

1zz |

||

2 |

Add lines 1a through 1zz and enter here and on the applicable line of Part I . . |

2 |

|

|

3 |

Enter the amount from Form 8844 here and on the applicable line of Part II . . |

3 |

|

|

4a |

Investment (Form 3468, Part III) (attach Form 3468) |

4a |

||

b |

Work opportunity (Form 5884) |

4b |

||

c |

Biofuel producer (Form 6478) |

4c |

||

d |

4d |

|||

e |

Renewable electricity, refined coal, and Indian coal production (Form 8835) . . |

4e |

||

f |

Employer social security and Medicare taxes paid on certain employee tips (Form 8846) |

4f |

||

g |

Qualified railroad track maintenance (Form 8900) |

4g |

||

h |

Small employer health insurance premiums (Form 8941) |

4h |

||

i |

Increasing research activities (Form 6765) |

4i |

||

j |

Employer credit for paid family and medical leave (Form 8994) |

4j |

||

z |

Other |

4z |

||

5 |

Add lines 4a through 4z and enter here and on the applicable line of Part II . . |

5 |

|

|

6 |

Add lines 2, 3, and 5 and enter here and on the applicable line of Part II . . . |

6 |

|

|

* See instructions for limitation on this credit. |

|

|

Form 3800 (2020) |

|

| Fact Name | Description |

|---|---|

| Purpose | The IRS Form 3800 is used to claim various tax credits, including the General Business Credit. |

| Eligibility | Taxpayers need to meet specific criteria to qualify for the credits claimed on this form. |

| Filing Requirement | Form 3800 must be attached to the taxpayer's income tax return, typically Form 1040. |

| State-Specific Forms | Many states have their own forms for business credits, based on state tax laws, such as California Revenue and Taxation Code Section 17052. |

| Yearly Updates | The credits and eligibility criteria can change annually, so it is important to review the latest IRS instructions. |

| Deadline | The form must be filed by the due date of the tax return, including extensions. |

After gathering all necessary documentation, you will fill out the IRS Form 3800. This form can seem daunting at first, but breaking it down into manageable steps makes the process smoother. Ensure you have your tax records and relevant information ready as you proceed.

Form IRS 3800, also known as the "General Business Credit," allows businesses to claim a variety of tax credits for certain activities, investments, and expenditures. This form consolidates multiple credits into a single credit which is applied against a business's tax liability. It plays a crucial role in reducing the overall tax burden for eligible businesses.

Any business entity that qualifies for one or more of the specific credits included in the form can use IRS 3800. This includes corporations, partnerships, and some sole proprietorships. Generally, businesses must meet certain criteria for eligibility concerning the activities or expenses incurred to qualify for the various credits.

Form 3800 includes several credits, such as:

Each of these credits has specific requirements that must be met to qualify.

To calculate the amount to enter on Form 3800, you need to determine the credit amounts you are eligible for. This involves filling out any additional forms associated with the specific credits you are claiming. After calculations, the total credit amount is reported on Form 3800, which is then applied to your tax return.

Form 3800 is generally due when you file your income tax return. If you are filing an extension, Form 3800 must be submitted along with your extended return. Ensure that you check the current tax year guidelines for exact due dates, as they may vary.

Yes, you can amend Form 3800 if you discover an error after submission. Use the appropriate procedures to file an amended return, and include the corrected Form 3800. Keep records of both the original and amended forms for your documentation.

If you do not file Form 3800, you will miss out on potential tax credits that could lower your tax liability. Additionally, failure to file may result in penalties or interest charges if you owe taxes. It's important to consider filing even if you are unsure of eligibility.

Yes, you can file Form 3800 electronically through the IRS e-file system, provided your tax software supports it. E-filing can streamline the process and help ensure that all forms are submitted accurately and on time.

For more information about Form 3800, visit the official IRS website. The IRS provides guidance, instructions, and resources to help you understand how to complete and file this form. Consulting with a tax professional is also a good option if you have specific questions or need assistance.

Filling out the IRS 3800 form can be a straightforward process, but many people make mistakes that can lead to complications. One common error is failing to check the eligibility requirements. Before completing the form, it’s essential to determine if you qualify for the specific credits being claimed. Many taxpayers overlook this step and may inadvertently seek benefits for which they do not qualify.

Another frequent mistake is inaccurate data entry. This can include misspelling names, entering wrong Social Security numbers, or miscalculating income or credits. Such errors can delay processing and potentially lead to a denial of benefits. It’s crucial to double-check all information for accuracy before submitting the form.

People often neglect to include all necessary supporting documentation. Failing to attach relevant documents can result in the IRS requesting additional information, causing delays and confusion. It’s best to gather all supporting documents prior to filling out the form to ensure that everything is submitted together.

Omitting certain tax credits available on the IRS 3800 form is another pitfall. Taxpayers sometimes overlook credits for which they may be eligible, such as the Credit for Increasing Research Activities or the Renewable Electricity Production Credit. Taking the time to understand all options can significantly impact potential refunds.

Some individuals also misinterpret the line items on the form. Each line has specific instructions that may be confusing. Reading instructions thoroughly can prevent errors in reporting and calculations, so taking a moment to clarify any confusion is well worth the effort.

People often fail to sign and date the form, which is essential for its validity. A signature signifies that the information provided is complete and accurate to the best of the taxpayer's knowledge. No signature can lead to rejection of the form.

Late submission poses a risk as well. Many individuals may think they can file the form any time within the tax season. However, missing deadlines might harm eligibility for certain credits. Set reminders for key dates to avoid last-minute submissions.

Misunderstanding the requirements for claiming carryforward credits is a mistake some taxpayers make. These credits may have specific rules governing how they can be applied across tax years, and failing to understand them can result in missed opportunities.

Finally, many people underestimate the importance of seeking help if needed. Tax laws can be complex, and consulting with a professional or using reliable tax software can simplify the process. Taking this step can save time and prevent mistakes that may affect a tax refund.

The IRS 3800 form, known as the "General Business Credit," allows businesses to claim various tax credits. Accompanying this form, several other documents may be required to provide essential information about the business's qualifications for these credits. Below is a list of common forms and documents often used alongside the IRS 3800.

Understanding and gathering these documents can streamline the process of claiming various tax credits. Each document serves a unique purpose and is vital in demonstrating eligibility for the credits on the IRS 3800 form, ensuring businesses maximize their tax benefits.

The IRS Form 3800, also known as the General Business Credit form, plays a significant role for businesses claiming various credits. Several documents serve a similar purpose, providing tools for tax credits and deductions essential for businesses. Here’s a list of eight documents that share similarities with Form 3800:

By understanding these forms, businesses can more effectively navigate the tax credit landscape and maximize their available benefits.

When filling out the IRS Form 3800, proper preparation is key to ensuring a smooth process. Here are six essential dos and don'ts to consider.

By following these guidelines, you can confidently navigate the complexities of the IRS Form 3800 and maximize your potential tax benefits.

The IRS Form 3800, also known as the General Business Credit, serves an important role in helping businesses take advantage of various tax credits. However, some common misconceptions can lead to confusion. Here are six misconceptions about Form 3800, along with clarifications:

By clearing up these misconceptions, business owners can make informed decisions regarding their potential tax benefits. Form 3800 can be an advantage, leading to significant savings when used correctly.

The IRS Form 3800 is a critical document for businesses seeking to claim various tax credits. Understanding how to fill it out correctly can significantly impact your tax liability. Here are some key takeaways regarding this form:

Being informed about these aspects can lead to more strategic tax planning and potential savings. Take the time to understand how to navigate Form 3800 effectively and maximize the benefits for your business.