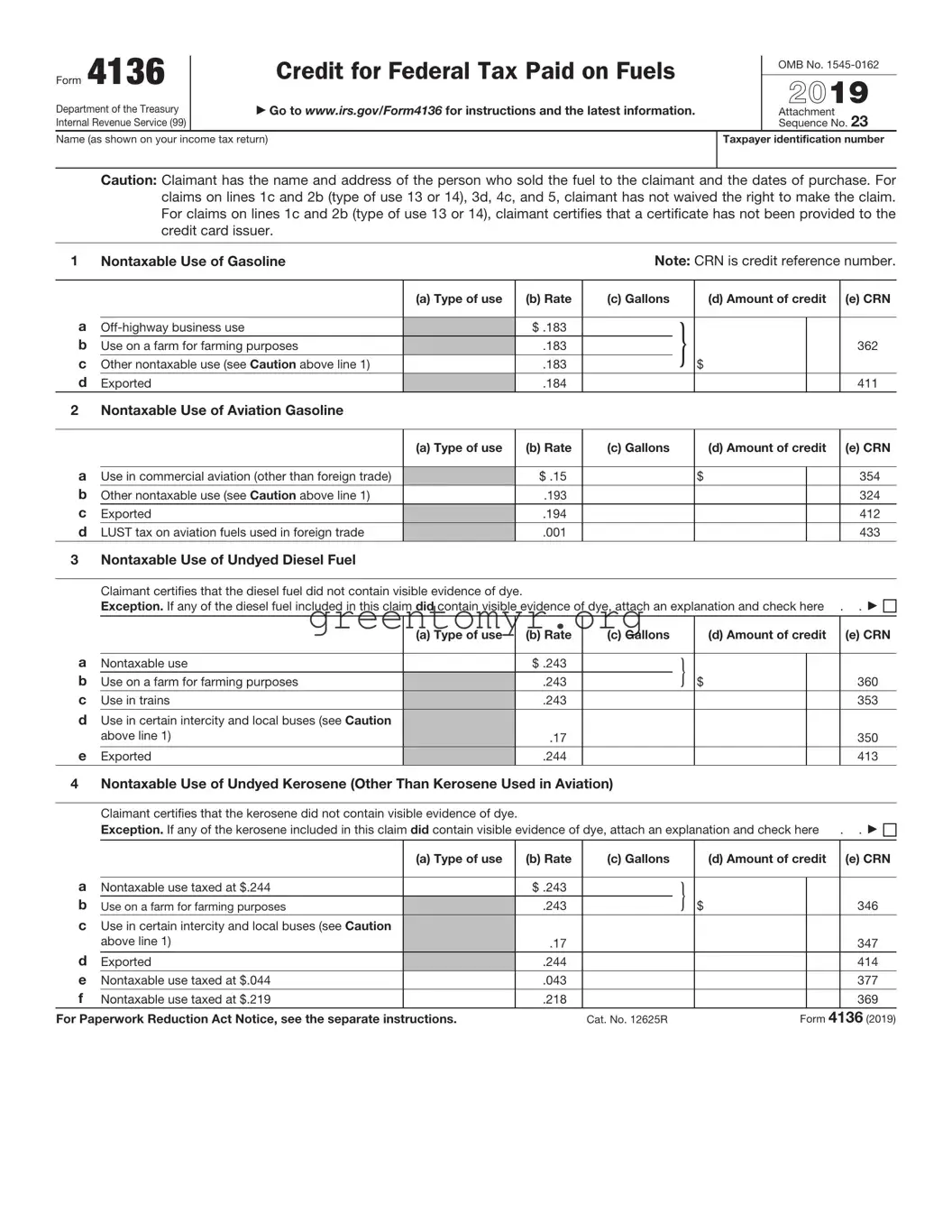

The IRS Form 4136, also known as the Credit for Federal Tax Paid on Fuels, serves an important function for taxpayers who purchase certain types of fuels. This form enables eligible individuals and businesses to claim a tax credit for federal excise taxes paid on fuel used for specific purposes, such as farming, fishing, or for other certain off-highway uses. By detailing the types of fuel and the corresponding tax amounts paid, users can seek reimbursement to help alleviate some of the financial burden associated with fuel costs. The form also outlines specific criteria for eligibility, ensuring that only those who meet designated guidelines can benefit from this tax relief. Understanding how to accurately complete Form 4136, including providing necessary data and documentation, is essential in navigating the claims process effectively. Additionally, keeping track of applicable deadlines and filing requirements is crucial to avoid any potential penalties or missing out on financial benefits. Thus, Form 4136 plays a critical role in helping taxpayers maximize their potential tax refunds related to fuel expenses.

Form 4136 |

|

Credit for Federal Tax Paid on Fuels |

|

OMB No. |

|

|

|

||

|

|

2019 |

||

Department of the Treasury |

|

Go to www.irs.gov/Form4136 for instructions and the latest information. |

|

|

|

|

Attachment |

||

Internal Revenue Service (99) |

|

|

|

Sequence No. 23 |

Name (as shown on your income tax return) |

|

Taxpayer identification number |

||

|

|

|

|

|

Caution: Claimant has the name and address of the person who sold the fuel to the claimant and the dates of purchase. For claims on lines 1c and 2b (type of use 13 or 14), 3d, 4c, and 5, claimant has not waived the right to make the claim. For claims on lines 1c and 2b (type of use 13 or 14), claimant certifies that a certificate has not been provided to the credit card issuer.

1 Nontaxable Use of Gasoline |

|

Note: CRN is credit reference number. |

||||||

|

|

|

|

|

|

|

|

|

|

|

(a) Type of use |

(b) Rate |

(c) Gallons |

(d) Amount of credit |

(e) CRN |

||

a |

|

|

|

|

|

|

|

|

|

$ .183 |

|

} |

|

|

|

||

b |

Use on a farm for farming purposes |

|

.183 |

|

|

|

362 |

|

c |

Other nontaxable use (see Caution above line 1) |

|

.183 |

|

$ |

|

|

|

d |

Exported |

|

.184 |

|

|

|

|

411 |

2Nontaxable Use of Aviation Gasoline

|

|

(a) Type of use |

(b) Rate |

(c) Gallons |

|

(d) Amount of credit |

(e) CRN |

|

a |

|

|

|

|

|

|

|

|

Use in commercial aviation (other than foreign trade) |

|

$ .15 |

|

$ |

|

|

354 |

|

b |

Other nontaxable use (see Caution above line 1) |

|

.193 |

|

|

|

|

324 |

c |

Exported |

|

.194 |

|

|

|

|

412 |

d |

LUST tax on aviation fuels used in foreign trade |

|

.001 |

|

|

|

|

433 |

3Nontaxable Use of Undyed Diesel Fuel

Claimant certifies that the diesel fuel did not contain visible evidence of dye.

|

Exception. If any of the diesel fuel included in this claim did contain visible evidence of dye, attach an explanation and check here . . |

|||||||

|

|

(a) Type of use |

(b) Rate |

(c) Gallons |

(d) Amount of credit |

(e) CRN |

||

a |

|

|

|

|

|

|

|

|

Nontaxable use |

|

$ .243 |

|

} |

|

|

|

|

b |

Use on a farm for farming purposes |

|

.243 |

|

$ |

|

360 |

|

c |

Use in trains |

|

.243 |

|

|

|

|

353 |

d Use in certain intercity and local buses (see Caution |

|

|

|

|

|

|

|

|

|

above line 1) |

|

.17 |

|

|

|

|

350 |

e |

Exported |

|

.244 |

|

|

|

|

413 |

4Nontaxable Use of Undyed Kerosene (Other Than Kerosene Used in Aviation)

Claimant certifies that the kerosene did not contain visible evidence of dye.

|

Exception. If any of the kerosene included in this claim did contain visible evidence of dye, attach an explanation and check here |

. . |

|||||||

|

|

(a) Type of use |

(b) Rate |

(c) Gallons |

|

(d) Amount of credit |

(e) CRN |

||

a |

|

|

|

|

|

|

|

|

|

Nontaxable use taxed at $.244 |

|

$ .243 |

|

} |

|

|

|

|

|

b |

Use on a farm for farming purposes |

|

.243 |

|

$ |

|

|

346 |

|

c |

Use in certain intercity and local buses (see Caution |

|

|

|

|

|

|

|

|

|

above line 1) |

|

.17 |

|

|

|

|

|

347 |

d |

Exported |

|

.244 |

|

|

|

|

|

414 |

e |

Nontaxable use taxed at $.044 |

|

.043 |

|

|

|

|

|

377 |

f |

Nontaxable use taxed at $.219 |

|

.218 |

|

|

|

|

|

369 |

For Paperwork Reduction Act Notice, see the separate instructions. |

|

Cat. No. 12625R |

Form 4136 (2019) |

||||||

Form 4136 (2019) |

Page 2 |

5Kerosene Used in Aviation (see Caution above line 1)

|

|

|

(a) Type of use |

(b) Rate |

(c) Gallons |

(d) Amount of credit |

(e) CRN |

|

|

|

|

|

|

|

|

|

|

|

a Kerosene used in commercial aviation (other than |

|

|

|

|

|

|

|

|

|

foreign trade) taxed at $.244 |

|

$ .200 |

|

$ |

|

417 |

|

b Kerosene used in commercial aviation (other than |

|

|

|

|

|

|

|

|

|

foreign trade) taxed at $.219 |

|

.175 |

|

|

|

355 |

|

c Nontaxable use (other than use by state or local |

|

|

|

|

|

|

|

|

|

government) taxed at $.244 |

|

.243 |

|

|

|

346 |

|

d Nontaxable use (other than use by state or local |

|

|

|

|

|

|

|

|

|

government) taxed at $.219 |

|

.218 |

|

|

|

369 |

|

e |

LUST tax on aviation fuels used in foreign trade |

|

.001 |

|

|

|

433 |

6 |

|

Sales by Registered Ultimate Vendors of Undyed Diesel Fuel |

|

Registration No. |

|

|

|

|

Claimant certifies that it sold the diesel fuel at a

Exception. If any of the diesel fuel included in this claim did contain visible evidence of dye, attach an explanation and check here . .

|

|

(b) Rate |

(c) Gallons |

|

(d) Amount of credit |

(e) CRN |

|

|

|

|

|

|

|

|

|

a |

Use by a state or local government |

$ .243 |

|

$ |

|

|

360 |

b |

Use in certain intercity and local buses |

.17 |

|

|

|

|

350 |

7 Sales by Registered Ultimate Vendors of Undyed Kerosene

(Other Than Kerosene For Use in Aviation)

Registration No.

Claimant certifies that it sold the kerosene at a

|

Exception. If any of the kerosene included in this claim did contain visible evidence of dye, attach an explanation and check here . . |

||||||

|

|

(b) Rate |

(c) Gallons |

(d) Amount of credit |

(e) CRN |

||

a |

|

|

|

|

|

|

|

Use by a state or local government |

$ .243 |

|

} |

|

|

|

|

b |

Sales from a blocked pump |

.243 |

|

$ |

|

346 |

|

c |

Use in certain intercity and local buses |

.17 |

|

|

|

|

347 |

8 |

Sales by Registered Ultimate Vendors of Kerosene For Use in Aviation |

Registration No. |

|

|

|

||

Claimant sold the kerosene for use in aviation at a

|

|

(a) Type of use |

(b) Rate |

(c) Gallons |

(d) Amount of credit |

(e) CRN |

|

a |

|

|

|

|

|

|

|

Use in commercial aviation (other than foreign trade) |

|

|

|

|

|

|

|

|

taxed at $.219 |

|

$ .175 |

|

$ |

|

355 |

b |

Use in commercial aviation (other than foreign trade) |

|

|

|

|

|

|

|

taxed at $.244 |

|

.200 |

|

|

|

417 |

c |

Nonexempt use in noncommercial aviation |

|

.025 |

|

|

|

418 |

d |

Other nontaxable uses taxed at $.244 |

|

.243 |

|

|

|

346 |

e |

Other nontaxable uses taxed at $.219 |

|

.218 |

|

|

|

369 |

f |

LUST tax on aviation fuels used in foreign trade |

|

.001 |

|

|

|

433 |

Form 4136 (2019)

Form 4136 (2019) |

Page 3 |

9 Reserved for future use |

Registration No. |

aReserved for future use b Reserved for future use

(b) Rate |

(c) Gallons |

(d) Amount of credit |

(e) CRN |

|

|

of alcohol |

|

|

|

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

10 Biodiesel or Renewable Diesel Mixture Credit |

Registration No. |

Biodiesel mixtures. Claimant produced a mixture by mixing biodiesel with diesel fuel. The biodiesel used to produce the mixture met ASTM D6751 and met EPA’s registration requirements for fuels and fuel additives. The mixture was sold by the claimant to any person for use as a fuel or was used as a fuel by the claimant. Claimant has attached the Certificate for Biodiesel and, if applicable, the Statement of Biodiesel Reseller. Renewable diesel mixtures. Claimant produced a mixture by mixing renewable diesel with liquid fuel (other than renewable diesel). The renewable diesel used to produce the renewable diesel mixture was derived from biomass, met EPA’s registration requirements for fuels and fuel additives, and met ASTM D975, D396, or other equivalent standard approved by the IRS. The mixture was sold by the claimant to any person for use as a fuel or was used as a fuel by the claimant. Claimant has attached the Certificate for Biodiesel and, if applicable, Statement of Biodiesel Reseller, both of which have been edited as discussed in the instructions for line 10. See the instructions for line 10 for information about renewable diesel used in aviation.

|

|

(b) Rate |

(c) Gallons |

(d) Amount of credit |

(e) CRN |

|

|

|

|

of biodiesel or |

|

|

|

|

|

|

renewable diesel |

|

|

|

|

|

|

|

|

|

|

a |

Biodiesel (other than |

$1.00 |

|

$ |

|

388 |

b |

1.00 |

|

|

|

390 |

|

c |

Renewable diesel mixtures |

1.00 |

|

|

|

307 |

11Nontaxable Use of Alternative Fuel

Caution: There is a reduced credit rate for use in certain intercity and local buses (type of use 5). See instructions.

|

|

(a) Type of use |

(b) Rate |

(c) Gallons, |

|

(d) Amount |

(e) CRN |

|

|

|

|

|

or gasoline |

|

of credit |

|

|

|

|

|

|

or diesel gallon |

|

|

|

|

|

|

|

|

equivalents |

|

|

|

|

a |

|

|

|

|

|

|

|

|

Liquefied petroleum gas (LPG) (see instructions) |

|

$ .183 |

|

$ |

|

|

419 |

|

b |

“P Series” fuels |

|

.183 |

|

|

|

|

420 |

c |

Compressed natural gas (CNG) (see instructions) |

|

.183 |

|

|

|

|

421 |

d |

Liquefied hydrogen |

|

.183 |

|

|

|

|

422 |

e |

|

|

|

|

|

|

|

|

|

(including peat) |

|

.243 |

|

|

|

|

423 |

f |

Liquid fuel derived from biomass |

|

.243 |

|

|

|

|

424 |

g |

Liquefied natural gas (LNG) (see instructions) |

|

.243 |

|

|

|

|

425 |

h |

Liquefied gas derived from biomass |

|

.183 |

|

|

|

|

435 |

12 |

Alternative Fuel Credit |

|

Registration No. |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

(b) Rate |

(c) Gallons, or |

|

(d) Amount of credit |

(e) CRN |

|

|

|

|

|

gasoline or diesel |

|

|

|

|

|

|

|

|

gallon equivalents |

|

|

|

|

a |

|

|

|

|

|

|

|

|

Liquefied petroleum gas (LPG) (see instructions) |

$ .50 |

|

$ |

|

|

426 |

||

b |

“P Series” fuels |

.50 |

|

|

|

|

427 |

|

c |

Compressed natural gas (CNG) (see instructions) |

.50 |

|

|

|

|

428 |

|

d |

Liquefied hydrogen |

.50 |

|

|

|

|

429 |

|

e |

.50 |

|

|

|

|

430 |

||

f |

Liquid fuel derived from biomass |

.50 |

|

|

|

|

431 |

|

g |

Liquefied natural gas (LNG) (see instructions) |

.50 |

|

|

|

|

432 |

|

h |

Liquefied gas derived from biomass |

.50 |

|

|

|

|

436 |

|

i |

Compressed gas derived from biomass |

.50 |

|

|

|

|

437 |

|

Form 4136 (2019)

Form 4136 (2019) |

|

|

|

|

Page 4 |

||

13 |

|

Registered Credit Card Issuers |

|

Registration No. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(b) Rate |

(c) Gallons |

(d) Amount of credit |

(e) CRN |

|

|

|

|

|

|

|

|

|

|

a |

Diesel fuel sold for the exclusive use of a state or local government |

$ .243 |

|

$ |

|

360 |

|

b |

Kerosene sold for the exclusive use of a state or local government |

.243 |

|

|

|

346 |

|

c Kerosene for use in aviation sold for the exclusive use of a state or local |

|

|

|

|

|

|

|

|

government taxed at $.219 |

.218 |

|

|

|

369 |

14Nontaxable Use of a

Caution: There is a reduced credit rate for use in certain intercity and local buses (type of use 5). See instructions.

|

|

(a) Type of use |

(b) Rate |

(c) Gallons |

(d) Amount of credit |

(e) CRN |

|

a |

|

|

|

|

|

|

|

Nontaxable use |

|

$ .197 |

|

$ |

|

309 |

|

b |

Exported |

|

.198 |

|

|

|

306 |

15 |

|

Registration No. |

|

|

|

||

Blender credit

(b) Rate |

(c) Gallons |

|

(d) Amount of credit |

(e) CRN |

|

$ .046 |

|

$ |

|

310 |

|

|

|

|

|||

16 |

Exported Dyed Fuels and Exported Gasoline Blendstocks |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(b) Rate |

(c) Gallons |

|

(d) Amount of credit |

(e) CRN |

||

|

|

|

|

|

|

|

|

|

a Exported dyed diesel fuel and exported gasoline blendstocks taxed |

|

|

|

|

|

|

|

|

|

at $.001 |

$ .001 |

|

|

|

$ |

|

415 |

b |

Exported dyed kerosene |

.001 |

|

|

|

|

|

416 |

17 |

Total income tax credit claimed. Add lines 1 through 16, column (d). Enter here and on |

|

|

|

|

|

||

|

Schedule 3 (Form 1040 or |

|

|

|

|

|

||

|

line 23c; Form 1041, Schedule G, line 16b; or the proper line of other returns . . |

. . |

|

17 |

$ |

|

|

|

Form 4136 (2019)

| Fact Name | Details |

|---|---|

| Purpose | The IRS Form 4136 is used to claim a credit for the federal excise tax on fuel used in certain types of vehicles. |

| Who Can File | Eligible claimants include businesses and individuals who use fuel in qualifying activities. |

| Filing Frequency | Typically, the form is filed annually or with the income tax return. |

| Eligible Fuel Types | This form applies to gasoline, diesel, kerosene, and other types of fuel specified by the IRS. |

| Credit Amount | The credit amount per gallon varies based on the type of fuel and current tax laws. |

| Related IRS Forms | Form 4136 is often filed alongside forms like 1040 and 1065, depending on the taxpayer's situation. |

| Record Keeping | Taxpayers must keep detailed records of their fuel purchases to substantiate claims made on the form. |

| Governing Law | The IRS governs the use of Form 4136 under the Internal Revenue Code (IRC) Section 6427. |

| Submission Method | Taxpayers can file Form 4136 electronically, by mail, or with their income tax submission. |

| Importance of Accuracy | Accurate completion is crucial; errors can lead to delayed refunds or penalties. |

When you're ready to complete IRS Form 4136, gather any relevant tax documents so you can easily find the information needed. The steps below guide you through filling out the form accurately.

With these steps complete, you'll be on your way to finalizing the form. Always remember to double-check for any errors or omissions before sending it off. This attention to detail can streamline your filing process and ensure a smoother experience.

IRS Form 4136 is used to claim the credit for federal tax paid on fuel for certain vehicles. This includes gasoline or diesel used in commercial transportation, boats, and airplanes. Typically, businesses and individuals who use fuel for non-highway purposes are eligible to file this form.

Eligibility to file Form 4136 generally includes:

To file Form 4136, follow these steps:

You will need to provide detailed information about:

If an error occurs when completing Form 4136, you should correct it as soon as possible. Depending on the nature of the mistake:

For more information regarding Form 4136, you can visit the IRS website. It provides comprehensive guidance, including instructions and FAQs. Additionally, tax professionals can offer personalized assistance if needed.

The IRS 4136 form is used to claim a credit for certain fuels. When completing this form, it is important to avoid common mistakes that can lead to delays or denials. One mistake is failing to include the correct identification number. The taxpayer’s identification number must be provided accurately to ensure proper processing of the claim. Omitting or misentering this information can result in significant complications.

Another frequent error involves incorrect calculations of the fuel credit. It is essential to keep track of the amount of fuel used and the appropriate rates for the credit. Miscalculating these figures can lead to an overstated or understated claim. Ensuring all calculations are double-checked can help prevent this issue.

People sometimes neglect to sign and date the form. A missing signature can render the form invalid and cause delays in claim processing. It is important to check that the form is fully completed before submission, including all necessary signatures.

Submitting the form late is also a common mistake. There are specific deadlines for filing the IRS 4136, and missing these deadlines can result in disqualification for the credit. Individuals should be aware of these dates and plan to submit the form in a timely manner.

Additionally, failing to keep proper records can lead to problems if the IRS requires supporting documents. Documentation should include receipts, logs, or any other proof of fuel use. Maintaining thorough records is crucial for validating the claims made on the form.

Some individuals overlook the importance of understanding eligibility requirements. Not all fuels qualify for the credit, and it is vital to confirm that the fuel used meets the necessary criteria before submitting the form. Lack of understanding may lead to unnecessary complications.

Finally, individuals may submit the form without reviewing the instructions provided by the IRS. Each section of the form has specific guidelines that must be followed. Ignoring these instructions could result in an incomplete or inaccurate submission.

The IRS Form 4136, titled "Credit for Federal Tax Paid on Fuels," is essential for anyone who has paid federal excise tax on fuel and is seeking a credit or refund. To effectively navigate the process related to this form, various other documents may be required. Below is a list of forms and documents often used alongside the IRS 4136 form.

Each of these forms and documents serves a unique purpose, often helping individuals and businesses substantiate their claims and ensuring proper tax reporting. By understanding their roles, taxpayers can prepare better and streamline their interactions with the IRS.

The IRS Form 4136 is used for the credit for federal tax on fuels. This form allows taxpayers, particularly those in businesses that use fuel, to claim a refund for fuel taxes that they may have overpaid. Several other forms serve similar purposes in tax reporting and refund claims. Here are four documents with comparable functions:

Each of these documents plays a role in tax compliance and refund mechanisms, albeit in different contexts. When dealing with fuel-related tax credits or reporting, it’s essential to understand the purpose of each form and how they interrelate within the larger tax system.

When filling out the IRS 4136 form, it is important to adhere to best practices to ensure accuracy and compliance. Below is a list of things to do and not to do during this process.

The IRS Form 4136 is used for claiming a credit for gasoline and special fuels used in certain non-highway vehicles and for other specific purposes. Several misconceptions exist regarding this form. Here are ten common misunderstandings:

In reality, individuals can also use this form if they meet eligibility requirements, such as using gasoline or special fuel for qualified non-highway use.

This form can be submitted by mail as well. While electronic filing may offer convenience, paper submissions are permissible.

The form applies to both gasoline and special fuels, which include diesel and kerosene, among others, when used in eligible vehicles.

Claiming a credit does not ensure a refund, as the IRS reviews submissions and may reject claims based on accuracy and proper documentation.

The credit amount can change annually and is based on the current tax laws and regulations in force during the year of filing.

While agricultural use qualifies, non-highway vehicles for various purposes, including certain construction equipment, may also be eligible for the credit.

Only fuel used in qualified non-highway vehicles counts toward the credit. It does not apply to vehicles intended for public highways.

Only specific purchases of gasoline and special fuels used in eligible circumstances will qualify for the credit, so documentation is crucial.

Completing the form is not mandatory each year; it only needs to be filed when claiming an eligible credit during that tax year.

There are limits on the amounts that can be claimed based on type of fuel, vehicle use, and other regulations that must be observed.

Understanding these misconceptions enhances compliance and ensures accurate claims when using IRS Form 4136 for tax credits.

When it comes to using the IRS Form 4136, which is primarily utilized for claiming a credit for federal tax paid on fuels, there are important aspects to keep in mind. Below are some key takeaways that can help ensure a smoother experience with this form: