The IRS 4137 form plays a critical role in tax reporting for individuals who have received tips or other compensation through services. This form is primarily used by taxpayers to report tips received while working in certain industries, such as hospitality and food service. Understanding how to accurately fill out the 4137 is essential, as it ensures that all income is properly accounted for, which is important for tax compliance. Furthermore, the form addresses various issues, including calculating the total amount of tips received and determining the applicable Social Security and Medicare taxes. By providing a clear and organized way to declare this income, the IRS 4137 helps taxpayers fulfill their obligations while ensuring that they do not fall short of reporting all forms of earnings. This article will delve into the intricacies of the form, guiding readers through its purpose and requirements, and shedding light on its importance in the larger context of federal tax responsibilities.

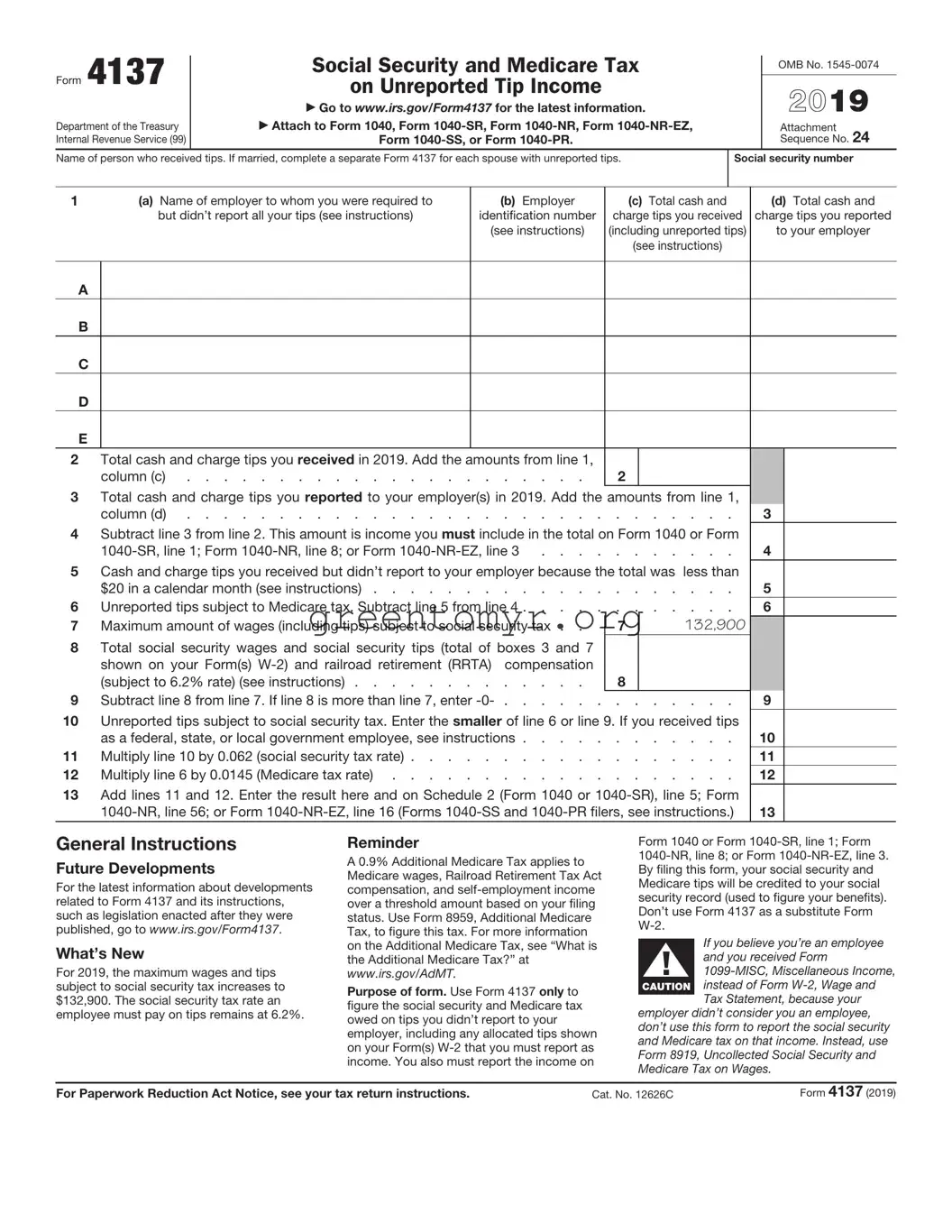

Form 4137 |

Social Security and Medicare Tax |

|

|

|

OMB No. |

|||

|

|

|

|

|

|

|||

on Unreported Tip Income |

|

|

|

|

|

|||

|

|

|

|

2019 |

||||

|

|

Go to www.irs.gov/Form4137 for the latest information. |

|

|

|

|||

Department of the Treasury |

Attach to Form 1040, Form |

|

Attachment |

|||||

Internal Revenue Service (99) |

Form |

|

|

|

|

Sequence No. 24 |

||

Name of person who received tips. If married, complete a separate Form 4137 for each spouse with unreported tips. |

|

Social security number |

||||||

|

|

|

|

|

|

|

|

|

1 |

(a) Name of employer to whom you were required to |

(b) Employer |

(c) |

Total cash and |

|

(d) Total cash and |

||

|

but didn’t report all your tips (see instructions) |

identification number |

charge tips you received |

charge tips you reported |

||||

|

|

|

(see instructions) |

(including unreported tips) |

|

to your employer |

||

|

|

|

|

(see instructions) |

|

|

||

|

|

|

|

|

|

|

|

|

|

A |

|

|

|

|

|

|

|

|

B |

|

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

|

D |

|

|

|

|

|

|

|

E

2Total cash and charge tips you received in 2019. Add the amounts from line 1,

column (c) |

2 |

3Total cash and charge tips you reported to your employer(s) in 2019. Add the amounts from line 1,

column (d) |

3 |

4Subtract line 3 from line 2. This amount is income you must include in the total on Form 1040 or Form

4 |

5Cash and charge tips you received but didn’t report to your employer because the total was less than

|

$20 in a calendar month (see instructions) |

. . . . . |

5 |

|

6 |

Unreported tips subject to Medicare tax. Subtract line 5 from line 4 |

. . . . . |

6 |

|

7 |

Maximum amount of wages (including tips) subject to social security tax . . |

7 |

132,900 |

|

8Total social security wages and social security tips (total of boxes 3 and 7

shown on your Form(s) |

compensation |

|

|

(subject to 6.2% rate) (see instructions) |

. . . . . |

8 |

|

9 Subtract line 8 from line 7. If line 8 is more than line 7, enter |

. . . . . . |

. . . . . . . |

9 |

10Unreported tips subject to social security tax. Enter the smaller of line 6 or line 9. If you received tips

|

as a federal, state, or local government employee, see instructions |

10 |

|

11 |

Multiply line 10 by 0.062 |

(social security tax rate) |

11 |

12 |

Multiply line 6 by 0.0145 |

(Medicare tax rate) |

12 |

13Add lines 11 and 12. Enter the result here and on Schedule 2 (Form 1040 or

13 |

General Instructions

Future Developments

For the latest information about developments related to Form 4137 and its instructions, such as legislation enacted after they were published, go to www.irs.gov/Form4137.

What’s New

For 2019, the maximum wages and tips subject to social security tax increases to $132,900. The social security tax rate an employee must pay on tips remains at 6.2%.

Reminder

A 0.9% Additional Medicare Tax applies to Medicare wages, Railroad Retirement Tax Act compensation, and

Purpose of form. Use Form 4137 only to figure the social security and Medicare tax owed on tips you didn’t report to your employer, including any allocated tips shown on your Form(s)

Form 1040 or Form

If you believe you’re an employee F! and you received Form

Tax Statement, because your employer didn’t consider you an employee, don’t use this form to report the social security and Medicare tax on that income. Instead, use Form 8919, Uncollected Social Security and Medicare Tax on Wages.

For Paperwork Reduction Act Notice, see your tax return instructions. |

Cat. No. 12626C |

Form 4137 (2019) |

Form 4137 (2019) |

Page 2 |

Who must file. You must file Form 4137 if you received cash and charge tips of $20 or more in a calendar month and didn’t report all of those tips to your employer. You also must file Form 4137 if your Form(s)

Allocated tips. You must report all your tips from 2019, including both cash tips and noncash tips, as income on Form 1040 or Form

Tips you must report to your employer. If you receive $20 or more in cash tips, you must report 100% of those tips to your employer through a written report. Cash tips include tips paid by cash, check, debit card, and credit card. The written report should include tips your employer paid to you for charge customers, tips you received directly from customers, and tips you received from other employees under any

Employees subject to the Railroad Retirement Tax Act. Don’t use Form 4137 to report tips received for work covered by the Railroad Retirement Tax Act. To get railroad retirement credit, you must report these tips to your employer.

Payment of tax. Tips you reported to your employer are subject to social security and Medicare tax (or railroad retirement tax), Additional Medicare Tax, and income tax withholding. Your employer collects these taxes from wages (excluding tips) or other funds of yours available to cover them. If your wages weren’t enough to cover these taxes, you may have given your employer the additional amounts needed. Your Form

will include the tips you reported to your employer and the taxes withheld. If there wasn’t enough money to cover the social security and Medicare tax (or railroad retirement tax), your Form

Penalty for not reporting tips. If you didn’t report tips to your employer as required, you may be charged a penalty equal to 50% of the social security, Medicare, and Additional Medicare Taxes due on those tips. You can avoid this penalty if you can show (in a statement attached to your return) that your failure to report tips to your employer was due to reasonable cause and not due to willful neglect.

Additional information. See Pub. 531, Reporting Tip Income. See Rev. Rul.

Specific Instructions

Line 1. Complete a separate line for each employer. If you had more than five employers in 2019, attach a statement that contains all of the information (and in a similar format) as required on Form 4137, line 1, or complete and attach line 1 of additional Form(s) 4137. Complete lines 2 through 13 on only one Form 4137. The line 2 and line 3 amounts on that Form 4137 should be the combined totals of all your Forms 4137 and attached statements. Include your name, social security number, and calendar year (2019) on the top of any attachment.

Column (a). Enter your employer’s name exactly as shown on your Form

Column (b). For each employer’s name you entered in column (a), enter the employer identification number (EIN) or the words “Applied For” exactly as shown on your Form

Columns (c) and (d). Include all cash and charge tips you received. All of the following tips must be included.

•Total tips you reported to your employer on time. Tips you reported, as required, by the 10th day of the month following the month you received them are considered income in the month you reported them. For example, tips you received in December 2018 that you reported to your employer after December 31, 2018, but by January 10, 2019, are considered income in 2019 and should be included on your 2019 Form

•Tips you received in December 2019 that you reported to your employer after December 31, 2019, but by January 10, 2020, are considered income in 2020. Don’t include these tips on line 1 for 2019. Instead, report these tips on line 1, column (d), on your 2020 Form 4137.

•Tips you didn’t report to your employer on time. Report these tips in column (d).

•Tips you didn’t report at all (include any allocated tips (see Allocated tips, earlier) shown in box 8 on your Form(s)

•Tips you received that you weren’t required to report to your employer because they totaled less than $20 during the month. Report these tips in column (c).

Line 5. Enter only the tips you weren’t required to report to your employer because the total received was less than $20 in a calendar month. These tips aren’t subject to social security and Medicare tax.

Line 6. Enter this amount on Form 8959, line 2, if you’re required to file that form.

Line 8. For railroad retirement (RRTA) compensation, don’t include an amount greater than $132,900, which is the amount subject to the 6.2% rate for 2019.

Line 10. If line 6 includes tips you received for work you did as a federal, state, or local government employee and your pay was subject only to the 1.45% Medicare tax, subtract the amount of those tips from the line 6 amount only for the purpose of comparing lines 6 and 9. Don’t reduce the actual entry on line 6. Enter “1.45% tips” and the amount you subtracted on the dotted line next to line 10.

Line 11. Multiply the amount on line 10 by 0.062 (the social security rate for 2019).

Line 13. Form

| Fact Name | Description |

|---|---|

| Purpose of Form | The IRS 4137 form is used to report tips received by employees in the food and beverage industry, as well as other service sectors, and to calculate additional taxes due on those tips. |

| Who Needs to File | Employees who receive tips that are not reported to their employer must file this form to ensure accurate tax reporting and compliance. |

| Deadline for Submission | The form must be submitted along with your annual income tax return, typically by April 15 of the following year. |

| Calculating Tip Income | Workers must report the total amount of tips received, including those not reported to their employer, to determine tax liability. |

| Tax Implications | Filing this form may result in additional taxes owed, as unreported tips are subject to Social Security and Medicare taxes. |

| State Regulations | While the IRS 4137 form is federal, some states may have additional forms or laws requiring specific tip reporting. For example, California's labor law mandates accurate reporting of tip income for wage calculations. |

Next, you will proceed to fill out Form 4137, which is necessary to report tips that were not reported to your employer. Gathering your information ahead of time will help streamline the process and ensure accuracy.

The IRS 4137 form is used to report tips that employees receive, particularly in industries such as hospitality, food service, and entertainment. This form helps ensure that the income from tips is accurately reported to the Internal Revenue Service (IRS), allowing employees to fulfill their tax obligations correctly. It is essential for employees who receive tips directly from customers or through indirect methods, such as shared tips among staff.

Employees who receive tips must file Form 4137 if they do not report their tips to their employer or if the tips are not included in their salary. This is particularly important for workers in occupations where tipping is common. If you earn tips but are unsure whether you need to file, consulting a tax professional can provide clarification.

Filling out the IRS 4137 form involves several steps:

The deadline for filing Form 4137 aligns with the regular deadline for submitting your income tax return, which is typically April 15th of each year. However, if you need extra time, you can request an extension. Remember, if you owe taxes, paying by the original deadline helps you avoid penalties and interest.

If you fail to file Form 4137 when required, you could face several consequences. The IRS may impose penalties for late filing or underreporting your income. Additionally, you risk an audit, which can lead to further scrutiny of your finances and potentially result in higher taxes due. Filing accurately and on time is crucial for keeping your financial matters in good standing.

Yes, if you discover that there are errors on Form 4137 after you’ve submitted it, you can amend your form. Use Form 1040-X, the Amended U.S. Individual Income Tax Return, to make corrections related to your tip income. Be sure to act promptly to avoid any penalties, and include a brief explanation of the changes you are making.

You can obtain the IRS 4137 form directly from the IRS website. It is available as a downloadable PDF that you can fill out electronically or print and complete by hand. Additionally, tax software programs often include Form 4137 as part of their filing options, making it easier for you to incorporate it into your overall tax return.

The IRS Form 4137 is a critical document for reporting unreported tips received by employees in certain service industries. Filling it out accurately is essential to avoid complications with tax obligations. However, several common mistakes can lead to inaccuracies, which may result in penalties or increased scrutiny from the IRS.

One of the first mistakes occurs in the misunderstanding of what constitutes reportable tips. Employees may fail to include all tips, believing only cash payments require reporting. However, any unreported tips—whether cash, credit, or other forms—need to be included on this form. Neglecting to do this can lead to underreporting of income.

Secondly, failing to keep meticulous records of tips received throughout the year remains a prevalent issue. Without accurate records, individuals might estimate their tips, which could lead to mismatches between what is reported and what the IRS expects. Consistent documentation is vital for ensuring conformity with actual earnings.

In addition, people often miscalculate their total tips. If calculations are off, it can lead to incorrect tax liabilities. Double-checking the math and confirming totals against personal records assists in providing accurate information to the IRS. Precision is crucial, as errors may draw unwanted attention from federal agents.

Another mistake is premature submission of the form. Individuals might fill out the form without considering other related tax documents, potentially causing inconsistencies. All tax forms should be completed with a complete understanding of each and how they interact with one another.

Some individuals also neglect to report tips received during work-related services performed outside of their primary employer. Employees may assume tips given in a side-job context do not require reporting. In truth, all earnings from tips received should be disclosed on the IRS Form 4137.

Omitting the signature or date on the form is another common issue that can delay processing or lead to rejection. It is essential to sign and date the form to validate that the information provided is accurate and complete.

Finally, individuals sometimes fail to keep copies of their submitted forms. In the event of an audit or inquiry, having a copy of what was filed can significantly ease the response process. Keeping organized records, including the submitted form, is advisable for all taxpayers.

The IRS Form 4137 is used to report tips received by a taxpayer working in the hospitality or service industry that are not reported by an employer. Typically, several other forms and documents complement this form, helping taxpayers accurately report their income and fulfill their tax obligations. Below are some key forms and documents that are often utilized alongside the IRS 4137 form.

Collectively, these forms and documents help ensure that taxpayers properly report their income and meet their tax responsibilities. Using them accurately plays a crucial role in the tax filing process, especially for those relying on tips as part of their earnings.

Form 1040: This is the standard individual income tax return form. Like Form 4137, it reports income, but Form 4237 specifically focuses on tip income and unreported income.

Form 941: This form is used for reporting employment taxes. Similar to Form 4137, it addresses earnings that employees receive but is designed for employers to report wages and taxes.

Schedule C (Form 1040): A taxpayer uses Schedule C to report income or loss from a business, offering a similar function of declaring income as seen with tips reported on Form 4137.

Form W-2: This document is provided by employers to report an employee's annual wages and taxes withheld. It provides a similar context as the IRS 4137 when dealing with earned income.

Form 1099: This form reports various types of income other than wages, salaries, and tips, echoing Form 4137's purpose of reporting non-salaried income.

Form 8889: Used for Health Savings Accounts (HSAs), it reports contributions and distributions, paralleling how Form 4137 addresses specific types of income and deductions.

Schedule SE (Form 1040): This form is used to calculate self-employment tax. It shares a similar focus on income types and how they can affect tax liabilities.

Form 1098-T: This form is for reporting tuition payments and education credits. Both forms capture specific areas of income and credits, albeit in different tax contexts.

When completing the IRS Form 4137, there are specific practices to follow and avoid. This form is used to report unreported tips for employees in the food and beverage industry. Adhering to the correct procedures ensures accuracy and compliance with tax regulations.

The IRS 4137 form is often misunderstood. Here are four common misconceptions about it, along with clarifications.

This form is used to report tips received and is applicable to both employees and self-employed individuals who earn tips. It applies to anyone who receives tips and needs to report them for tax purposes.

Even if the total amount of tips is low, any tips received must still be reported. There is no minimum threshold for reporting; all tips are considered taxable income.

While the form helps calculate Social Security and Medicare taxes, tips reported on the 4137 also contribute to your overall taxable income. This means they will affect both your federal income tax and other potential deductions.

If you report tips through your employer, you may still need to file the 4137 form to accurately document your tip income, especially if you have received tips that were not reported to your employer.

Using the IRS 4137 form correctly is crucial for reporting unreported tips or allocated tips. Here are some key takeaways to keep in mind: