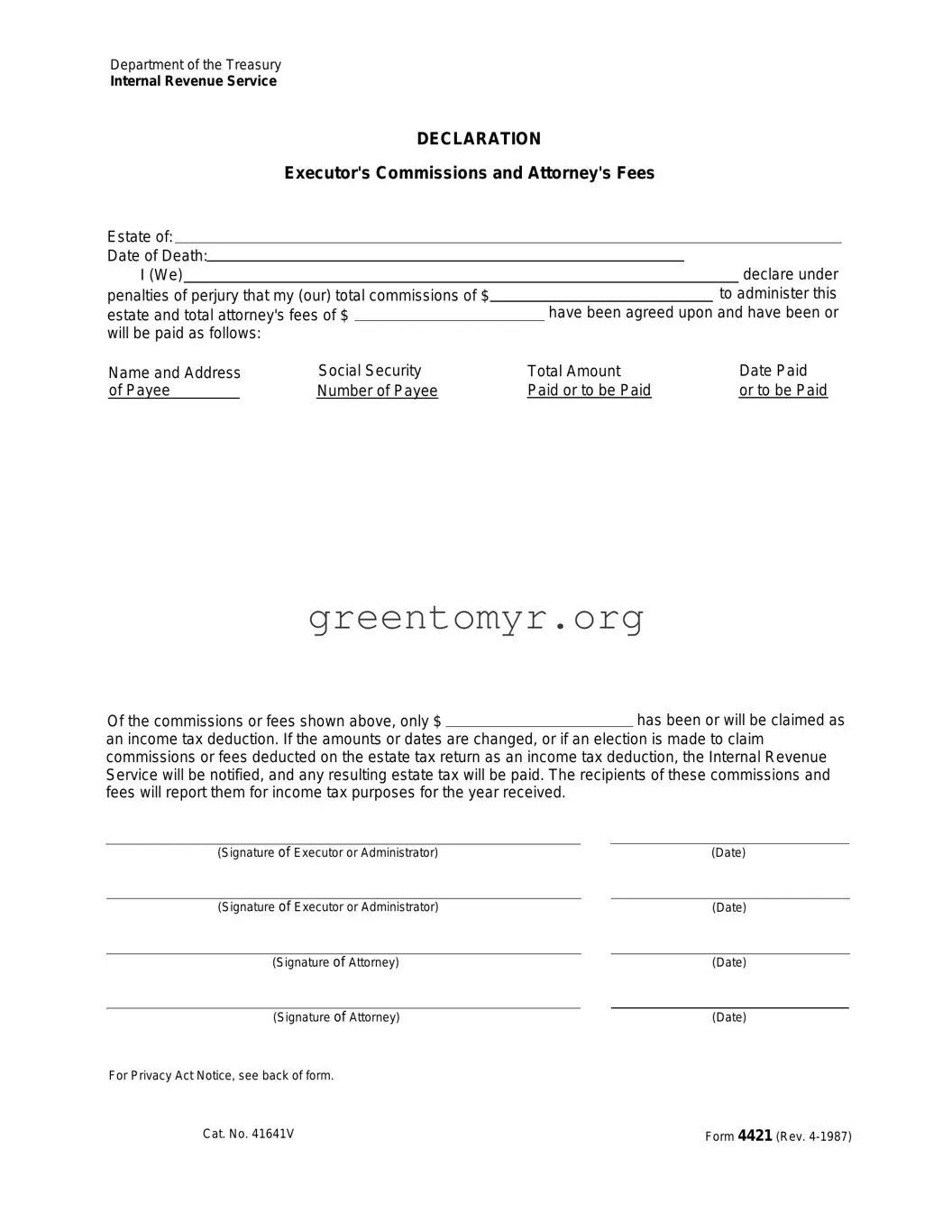

The IRS Form 4421 is a crucial document for individuals involved in administering an estate, particularly when it comes to declaring executor’s commissions and attorney's fees. When someone passes away, settling their estate involves various financial responsibilities, and this form serves as a declaration of the agreed-upon fees for the services rendered. Executors and administrators must fill out relevant details, like the total amounts of commissions and fees, along with the name and address of the payees. Additionally, the form requires clarity regarding any amounts claimed as income tax deductions. Understanding the implications of this form is essential, especially since it mandates that recipients will need to report these payments as income for tax purposes in the year they are received. Furthermore, the form highlights the necessity of notifying the IRS about any changes to the amounts or the decisions regarding deductions, ensuring compliance with estate tax obligations. Filling out this form correctly not only helps ensure a smooth estate administration process but also mitigates the risk of complications with the IRS.

Department of the Treasury

Internal Revenue Service

DECLARATION

Executor's Commissions and Attorney's Fees

Estate of:

Date of Death: |

|

|

|

|

|

|

|

declare under |

|||

|

I (We) |

|

|

|

|

|

|

|

|||

penalties of perjury that my (our) total commissions of $ |

|

|

|

to administer this |

|||||||

estate and total attorney's fees of $ |

|

|

have been agreed upon and have been or |

||||||||

will be paid as follows: |

|

|

|

|

|

|

|

||||

Name and Address |

Social Security |

Total Amount |

|

|

Date Paid |

||||||

|

of Payee |

|

Number of Payee |

Paid or to be Paid |

|

|

or to be Paid |

||||

Of the commissions or fees shown above, only $has been or will be claimed as an income tax deduction. If the amounts or dates are changed, or if an election is made to claim commissions or fees deducted on the estate tax return as an income tax deduction, the Internal Revenue Service will be notified, and any resulting estate tax will be paid. The recipients of these commissions and fees will report them for income tax purposes for the year received.

(Signature of Executor or Administrator) |

|

(Date) |

|

|

|

|

|

(Signature of Executor or Administrator) |

|

(Date) |

|

|

|

|

|

(Signature of Attorney) |

|

(Date) |

|

|

|

|

|

(Signature of Attorney) |

|

(Date) |

|

For Privacy Act Notice, see back of form.

Cat. No. 41641V |

Form 4421 (Rev. |

Privacy Act Notice

Under the Privacy Act of 1974, we must tell you:

Our legal right to ask for the information and whether the law says you must give it.

Our legal right to ask for the information and whether the law says you must give it.

What major purposes we have in asking for it, and how it will be used.

What major purposes we have in asking for it, and how it will be used.

What could happen if we do not receive it.

What could happen if we do not receive it.

The law covers: Tax returns and any papers

filed with them. Any questions we need to ask

filed with them. Any questions we need to ask

you so we can:

you so we can:

Complete, correct, or process your return. Figure your tax.

Collect tax, interest, or penalties.

Our legal right to ask for information is Internal Revenue Code sections 6001, 601 1, and 6012(a), and their regulations. They say that you must file a return or statement with us for any tax you are liable for. Code section 6109 and its regulations say that you must show your social security number on what you file. This is so we know who you are, and can process your return and papers.

You must fill in all parts of the tax form that apply to you. But you do not have to check boxes for the Presidential Election Campaign Fund.

We ask for tax return information to carry out the In- ternal Revenue

We may give the information to the Department of Justice and to other Federal agencies, as provided by law. We may also give it to cities, States, the District of Columbia, and U.S. commonwealths or possessions to carry out their tax laws. And we may give it to foreign governments because of tax treaties they have with the United States.

If you do not file a return, do not provide the infor- mation we ask for, or provide fraudulent information, the law provides that you may be charged penalties and, in certain cases, you may be subject to criminal prosecution. We may also have to disallow the exemp- tions, exclusions, credits, deductions, or adjustments shown on the tax return. This could make the tax higher or delay any refund. Interest may also be charged.

Please keep this notice with your records. It may help you if we ask you for other information.

If you have questions about the rules for filing and giving information, please call or visit any Internal Revenue Service office.

This is the only notice we must give you to explain the Privacy Act. However, we may give you other notices if we have to examine your return or collect any tax, interest, or penalties.

| Fact Name | Description |

|---|---|

| Purpose | The IRS Form 4421 serves as a declaration for executor's commissions and attorney's fees related to an estate's administration. |

| Signatures Required | Both the executor or administrator and the attorney must sign the form, affirming the details provided are accurate. |

| Income Tax Deductions | Only the specified portion of the commissions or fees can be claimed as an income tax deduction by the estate. |

| Reporting Obligations | Recipients of commissions and fees must report the amounts received for income tax purposes in the year they are paid. |

| Changes Notification | If any amounts or payment dates change, or if deductions are elected on the estate tax return, the IRS must be notified. |

| Legal Authority | The form's requirements fall under Internal Revenue Code sections 6001, 6011, and 6012(a), which govern the filing and reporting obligations. |

Filling out the IRS Form 4421 is a straightforward process when you know what information is required. The form plays a crucial role in reporting executor commissions and attorney fees related to an estate. Here are specific steps that will guide you through the process of completing this form accurately.

Once you complete these steps, ensure to keep a copy for your records before submitting the form to the IRS. If you have any questions or need assistance while filling out the form, consider reaching out to a tax professional who can provide personalized guidance.

IRS Form 4421 is a declaration used for reporting executor commissions and attorney's fees related to the administration of an estate. It provides details about the amounts paid and specifies how much will be claimed as an income tax deduction.

The executor or administrator of an estate must file Form 4421. This form is necessary for reporting the fees they receive and any attorney's fees associated with estate administration.

Form 4421 requires the following information:

Executors must state the total commissions and attorney's fees. They should then indicate how much of those amounts will be claimed as an income tax deduction. If any changes occur in these amounts or the payment dates, the IRS needs to be notified.

If there are changes to the reported amounts or if an adjustment affects the income tax deduction, the executor must inform the IRS. This notification is crucial as it may impact the estate tax owed.

Yes, recipients of the commissions and fees must report these amounts for income tax purposes in the year they receive them, as stated on Form 4421.

The Privacy Act Notice explains how the IRS collects and uses the information on the form. It includes details about legal rights, purposes for requesting information, and the consequences of not providing necessary information.

For additional questions or detailed guidance, individuals can contact their local IRS office or visit the IRS website. Assistance is available for understanding the rules regarding filing and providing information.

Filling out the IRS Form 4421 can be straightforward, yet many people make common mistakes that can cause delays or issues. One significant error occurs when individuals fail to accurately report the total commissions and attorney’s fees. It is crucial to ensure that the amounts listed match the actual agreements made regarding the estate. Discrepancies can lead to complications or audits.

Another common oversight is neglecting to provide complete details about the payees. Each payee's name, address, and Social Security number should be listed correctly. Incomplete or incorrect information can result in difficulties for the recipients when they report the commissions and fees on their tax returns.

Furthermore, people often forget to sign and date the form appropriately. Signatures from both the executor and the attorney are essential. This validates the declaration under penalties of perjury. Without these signatures, the form may be considered invalid or incomplete by the IRS.

Some individuals fail to indicate how much of the commissions or fees will be claimed as an income tax deduction. This section is important, as it informs the IRS about the tax implications for the estate. Overlooking this may create confusion regarding the estate's tax liabilities.

An additional pitfall includes not notifying the IRS about any changes in amounts or dates after submission. If there are modifications to the agreement, it is necessary to inform the IRS. This ensures that the correct estate tax is calculated and paid, preventing future issues.

Many mistakenly assume they do not need to keep a copy of the form for their records. Retaining a copy is vital for tracking and managing the estate’s finances and answering any follow-up inquiries from the IRS.

In terms of deadlines, failing to submit the form on time is a frequent problem. Missing a deadline can lead to penalties or delays in processing. It is essential to be aware of the submission timeline to avoid unnecessary complications.

Some filers also disregard the implications of not providing the Social Security numbers as required. This information is crucial for the IRS to process returns accurately, and its absence can cause significant issues.

Finally, individuals sometimes misjudge the need for consulting with a tax professional. While Form 4421 might seem simple, complexities in estate administration can arise. Seeking guidance from a qualified expert can help navigate potential pitfalls and ensure accurate completion.

When handling estate matters, various forms and documents play a crucial role alongside the IRS Form 4421. Each document serves a specific purpose in the estate administration process. Below is a list of key forms that are commonly used in conjunction with the IRS Form 4421, providing a brief explanation of each.

Understanding these forms and their purposes can significantly ease the estate administration process. Each document plays its part in ensuring compliance with legal tax obligations and proper management of the deceased's affairs. Estate matters can be complex and emotional; thus, it is beneficial to approach this process with care and thoroughness.

When filling out the IRS Form 4421, it's essential to keep certain best practices in mind. Here’s a helpful list of dos and don’ts to guide you through the process.

The IRS Form 4421 is vital for managing executor's commissions and attorney's fees during estate administration. However, several misconceptions surround the form. Below is a list clarifying nine of these misunderstandings.

Understanding these misconceptions can enhance compliance and ensure a smoother estate administration process. For those involved, it’s crucial to have accurate information to navigate the complexities associated with IRS Form 4421.

Filling out and using the IRS Form 4421 is an important step in the administration of an estate. Here are some key takeaways to keep in mind:

Following these takeaways can help ensure a smooth process when handling the estate's financial obligations and tax responsibilities.