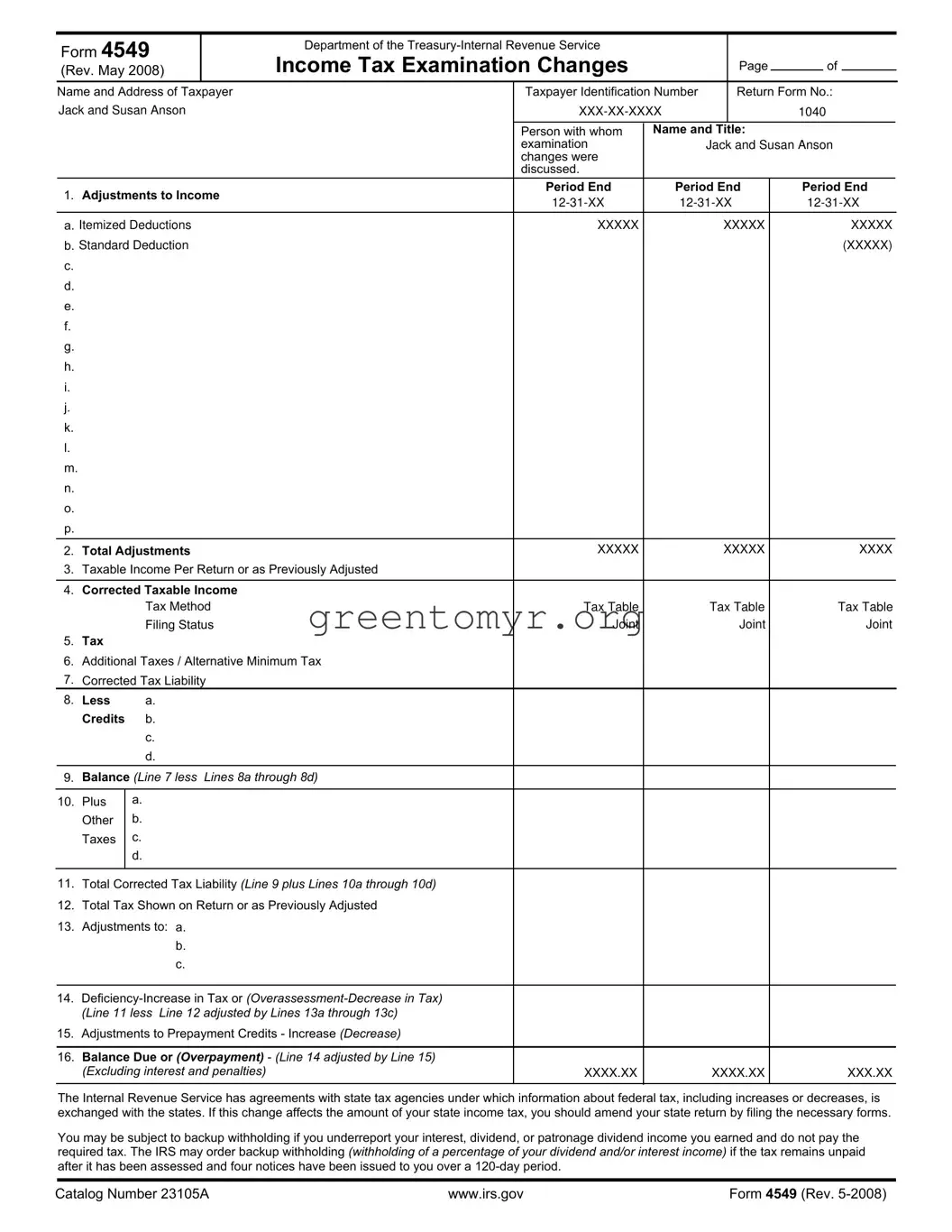

The IRS Form 4549 is an essential tool for taxpayers undergoing an income tax examination. This form facilitates the communication of adjustments made during the review process and serves as a summary of changes to a taxpayer's return. Notably, it outlines any alterations to income, deductions, and ultimately, the calculated tax liability. The document presents the corrected taxable income alongside additional taxes and credits, giving a comprehensive overview of one’s financial obligations. Furthermore, it includes sections for detailing penalties and interest that may accrue due to underpayment or errors found in prior submissions. Taxpayers are informed about any possible implications these adjustments may have on their state tax returns, emphasizing the interconnectedness of federal and state tax systems. By signing this form, individuals consent to the findings and the corresponding adjustments, streamlining the process of tax assessment and collection. Understanding the details within Form 4549 can empower taxpayers to navigate the outcomes of their tax examinations with clarity and preparedness.

Form 4549 |

|

Department of the |

|

|

|

|

|

|

|

|

||

|

Income Tax Examination Changes |

|

|

|

Page |

|

of |

|

|

|||

(Rev. May 2008) |

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

||||

Name and Address of Taxpayer |

|

Taxpayer Identification Number |

|

Return Form No.: |

||||||||

Jack and Susan Anson |

|

|

|

|

1040 |

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

Person with whom |

Name and Title: |

|

|

|

|

|||

|

|

|

|

examination |

|

|

Jack and Susan Anson |

|||||

|

|

|

|

changes were |

|

|

|

|

|

|

|

|

|

|

|

|

discussed. |

|

|

|

|

|

|

|

|

1. |

Adjustments to Income |

|

Period End |

|

Period End |

Period End |

||||||

|

|

|||||||||||

|

|

|

|

|

||||||||

a. Itemized Deductions |

|

XXXXX |

|

|

XXXXX |

|

|

XXXXX |

||||

b. Standard Deduction |

|

|

|

|

|

|

|

|

(XXXXX) |

|||

c. |

|

|

|

|

|

|

|

|

|

|

|

|

d. |

|

|

|

|

|

|

|

|

|

|

|

|

e. |

|

|

|

|

|

|

|

|

|

|

|

|

f. |

|

|

|

|

|

|

|

|

|

|

|

|

g. |

|

|

|

|

|

|

|

|

|

|

|

|

h. |

|

|

|

|

|

|

|

|

|

|

|

|

i. |

|

|

|

|

|

|

|

|

|

|

|

|

j. |

|

|

|

|

|

|

|

|

|

|

|

|

k. |

|

|

|

|

|

|

|

|

|

|

|

|

l. |

|

|

|

|

|

|

|

|

|

|

|

|

m. |

|

|

|

|

|

|

|

|

|

|

|

|

n. |

|

|

|

|

|

|

|

|

|

|

|

|

o. |

|

|

|

|

|

|

|

|

|

|

|

|

p. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

2. |

Total Adjustments |

|

XXXXX |

|

|

XXXXX |

|

|

XXXX |

|||

3.Taxable Income Per Return or as Previously Adjusted

4.Corrected Taxable Income

Tax Method |

Tax Table |

Tax Table |

Tax Table |

Filing Status |

Joint |

Joint |

Joint |

5.Tax

6.Additional Taxes / Alternative Minimum Tax

7.Corrected Tax Liability

8.Less a. Credits b. c. d.

9.Balance (Line 7 less Lines 8a through 8d)

10.Plus a. Other b. Taxes c. d.

11.Total Corrected Tax Liability (Line 9 plus Lines 10a through 10d)

12.Total Tax Shown on Return or as Previously Adjusted

13.Adjustments to: a.

b.

c.

14.

15.Adjustments to Prepayment Credits - Increase (Decrease)

16.Balance Due or (Overpayment) - (Line 14 adjusted by Line 15)

(Excluding interest and penalties) |

XXXX.XX |

XXXX.XX |

XXX.XX |

The Internal Revenue Service has agreements with state tax agencies under which information about federal tax, including increases or decreases, is exchanged with the states. If this change affects the amount of your state income tax, you should amend your state return by filing the necessary forms.

You may be subject to backup withholding if you underreport your interest, dividend, or patronage dividend income you earned and do not pay the required tax. The IRS may order backup withholding (withholding of a percentage of your dividend and/or interest income) if the tax remains unpaid after it has been assessed and four notices have been issued to you over a

Catalog Number 23105A |

www.irs.gov |

Form 4549 (Rev. |

Form 4549 |

|

|

Department of the |

|

|

|

|

|

|

|

|

|

Income Tax Examination Changes |

|

|

Page |

|

of |

|

|

|

||

(Rev. May 2008) |

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

||

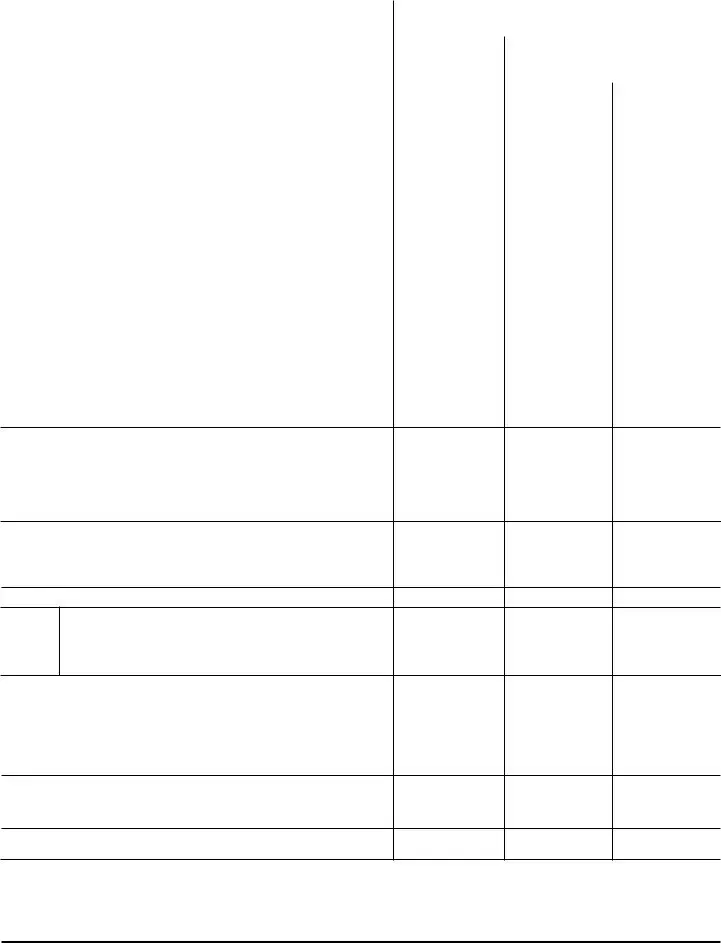

Name of Taxpayer |

|

Taxpayer Identification Number |

|

Return Form No.: |

|

||||||

Jack and Susan Anson |

|

|

|

|

1040 |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Period End |

Period End |

Period End |

|

|||||

17. Penalties/ Code Sections |

|

|

|||||||||

a. Accuracy Related Penalty - IRC 6662 |

XXX.XX |

|

XXX.XX |

|

|

XX.XX |

|

||||

b. |

|

|

|

|

|

|

|

|

|

|

|

c. |

|

|

|

|

|

|

|

|

|

|

|

d. |

|

|

|

|

|

|

|

|

|

|

|

e. |

|

|

|

|

|

|

|

|

|

|

|

f. |

|

|

|

|

|

|

|

|

|

|

|

g. |

|

|

|

|

|

|

|

|

|

|

|

h. |

|

|

|

|

|

|

|

|

|

|

|

i. |

|

|

|

|

|

|

|

|

|

|

|

j. |

|

|

|

|

|

|

|

|

|

|

|

k. |

|

|

|

|

|

|

|

|

|

|

|

l. |

|

|

|

|

|

|

|

|

|

|

|

m. |

|

|

|

|

|

|

|

|

|

|

|

n. |

|

|

|

|

|

|

|

|

|

|

|

18.Total Penalties

Underpayment attributable to negligence: (19811987) A tax addition of 50 percent of the interest due on the underpayment will accrue until it is paid or assessed.

Underpayment attributable to fraud: (19811987)

A tax addition of 50 percent of the interest due on the underpayment will accrue until it is paid or assessed.

Underpayment attributable to Tax Motivated Transactions (TMT). The interest will accrue and be assessed at 120% of the under payment rate in accordance with IRC §6621(c)

19.Summary of Taxes, Penalties and Interest:

a. |

Balance due or (Overpayment) Taxes - (Line 16, Page 1) |

XXXX.XX |

XXXX.XX |

XXX.XX |

|

b. |

Penalties (Line 18) - computed to |

|

XXX.XX |

XXX.XX |

XX.XX |

c. |

Interest (IRC § 6601) - computed to |

|

XXX.XX |

XXX.XX |

XX.XX |

d. |

TMT Interest - computed to |

(on TMT underpayment) |

|

|

|

e. |

Amount due or (refund) (sum of Lines a, b, c and d) |

XXXX.XX |

XXXX.XX |

XXXX.XX |

|

Other Information:

Examiner's Signature:

Employee ID:

XXXXXXX

Office:

SBSE- Exam

Date:

Consent to Assessment and Collection- I do not wish to exercise my appeal rights with the Internal Revenue Service or to contest in the United States Tax Court the findings in this report. Therefore, I give my consent to the immediate assessment and collection of any increase in tax and penalties, and accept any decrease in tax and penalties shown above, plus additional interest as provided by law. It is understood that this report is subject to acceptance by the Area Director, Area Manager, Specialty Tax Program Chief, or Director of Field Operations.

PLEASE NOTE: If a joint return was filed. BOTH taxpayers must sign

Signature of Taxpayer |

Date: |

Signature of Taxpayer |

|

|

|

Date:

By:

Title:

Date:

Catalog Number 23105A |

www.irs.gov |

Form 4549 (Rev. |

| Fact Title | Details |

|---|---|

| Purpose of Form | The IRS 4549 form is used for documenting adjustments to income tax following an examination. It reflects changes made by the IRS during an audit. |

| Adjustment Summary | Form 4549 provides a summary of all adjustments made to taxable income, including itemized deductions and credits. |

| Joint Filers | If a joint tax return is filed, both taxpayers must sign the form to consent to the findings and adjustments. |

| Consent to Assessment | By signing the form, taxpayers agree to the immediate assessment of any increased tax and consent to the collection of any liabilities. |

| Penalties Information | The form includes sections detailing any applicable penalties for underpayment, which may arise from negligence or fraud. |

| State Reporting | Taxpayers are advised to amend their state returns if federal tax changes affect their state income tax, as states may receive information from the IRS. |

Completing IRS Form 4549 is essential when there are changes to your income tax examination. This form outlines adjustments that may impact your tax liability. After filling out the form, you will need to submit it to the IRS for their records and to fulfill any obligations regarding tax assessments or corrections.

Form 4549 is a document issued by the Internal Revenue Service (IRS) that outlines changes to a taxpayer's income tax return following an examination. It details any adjustments made to income, deductions, and ultimately the tax liability. This form is generated if the IRS finds discrepancies during an audit or examination of a tax return.

You might receive Form 4549 if the IRS conducts a review of your tax return and discovers issues that necessitate changes. These adjustments could arise from underreported income, disallowed deductions, or calculation errors. The IRS uses this form to communicate its findings and inform you about the revisions to your tax liability.

Responding to Form 4549 involves a few steps. First, review the changes carefully to understand how they affect your tax situation. If you agree with the findings, you can sign the consent section to accept the adjustments. If you disagree, you have the right to appeal the decision. It's advisable to consult a tax professional for guidance on how to proceed.

If Form 4549 indicates that you owe additional taxes, it is essential to address this as soon as possible. The form will outline the balance due, and you will need to pay this amount to avoid further penalties or interest. Payment options are available on the IRS website, or you can set up a payment plan if necessary.

Yes, the IRS has agreements with state tax agencies that allow them to share information about federal tax changes. If the adjustments made on Form 4549 affect your state taxes, you may need to amend your state tax return as well to ensure everything is accurate and up-to-date.

Ignoring Form 4549 can lead to increasing penalties and interest on any unpaid taxes. The IRS may take further action, including enforced collection measures. Addressing the form promptly is critical to avoid potential financial repercussions.

For more information, visit the official IRS website. There, you will find resources and guides related to Form 4549, as well as contact information if you need to speak directly with a representative. It’s crucial to stay informed and take any necessary actions regarding your tax situation.

Filling out IRS Form 4549 can seem overwhelming, especially if it's your first time. Many people stumble over key details that can impact their tax situation significantly. One common mistake is failing to include all necessary income adjustments. The form requires adjustments to various types of income, but sometimes taxpayers overlook specific deductions or income types, which can lead to inaccuracies in reported figures.

Another frequent error is neglecting to check for accuracy in personal information. This includes names, addresses, and Social Security numbers. A simple typo can cause significant delays in processing and may even lead to correspondence from the IRS, which can be quite stressful. Double-checking all entries before submission can help avoid these problems.

Many individuals also mistakenly ignore to update their filing status. The filing status can affect tax rates and eligibility for various deductions and credits. If there has been a change in marital status or household income situation, it’s crucial to reflect that on the form to ensure that computations are based on accurate assumptions.

People sometimes overlook the importance of acknowledging prior adjustments. If there were previous adjustments made to a prior year’s return, these should be taken into account in the current form. Failing to reference past changes can lead to inconsistencies and may even raise red flags for IRS examiners.

It’s also common for taxpayers to miscalculate the income tax liability due. Form 4549 requires significant calculations, and small arithmetic errors can lead to incorrect balances. Seeking assistance from a tax professional or using reliable software can minimize these risks.

Many individuals forget to address penalties and interest correctly. There are specific boxes on the form to report penalties associated with negligence or fraud. Misunderstanding these could lead to unexpected financial consequences, so attention to detail in this section is crucial.

Lastly, a significant mistake arises when taxpayers don’t consider the implications on state tax returns. Changes to federal tax filings can impact state tax obligations. Thus, it’s important to be proactive about updating state returns accordingly to avoid possible complications down the line.

The IRS 4549 form is a notice of examination changes regarding your income tax. When you receive this form, there are several other documents you may encounter or need to reference. Each one plays a specific role in the tax adjustment process. Understanding these documents can make it easier to navigate your situation.

Being aware of these forms can help make the exam process less daunting. Each document serves a purpose, aiding you in resolving any discrepancies while ensuring compliance with tax laws. Stay organized and proactive in managing your tax affairs.

When filling out the IRS Form 4549, careful attention can make a significant difference in how the process unfolds. Here are some recommended practices, as well as common pitfalls to avoid.

Understanding IRS Form 4549 is essential for anyone facing an audit or correction to their tax returns. Unfortunately, there are several misconceptions surrounding this form that can create confusion. Here are five common misunderstandings clear explained.

Understanding how to fill out and use the IRS Form 4549 is important for taxpayers involved in tax examinations. Here are some key takeaways to keep in mind:

Taking these points into account will help you navigate any tax changes or assessments more smoothly.