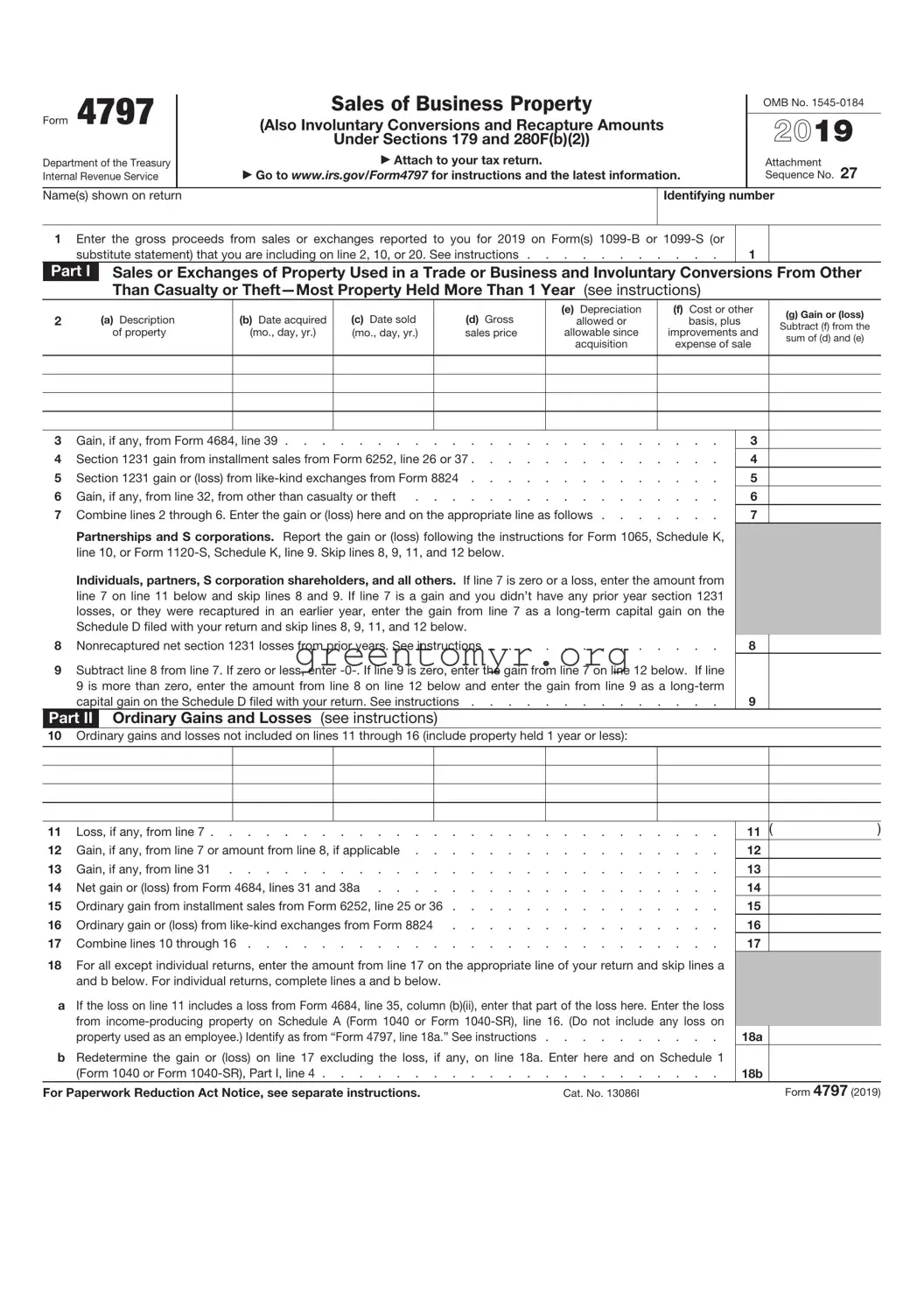

Navigating the world of taxes can be a complex undertaking, particularly when it comes to the sale of business property or certain types of assets. The IRS Form 4797 plays a crucial role in this process, helping taxpayers report the sale or exchange of property used in a trade or business. Whether you’re disposing of real estate or selling equipment, Form 4797 is essential for accurately documenting gains or losses associated with these transactions. It categorizes the types of assets involved, providing clarity on how these sales impact your overall tax liability. Taxpayers must understand the significance of both Section 1231 and Section 1245 property, as these classifications influence how gains are taxed, potentially leading to ordinary income rates or capital gains treatment. Additionally, the form requires careful calculations, especially regarding depreciation recapture, which can significantly affect the tax outcome. Familiarity with Form 4797 ensures that taxpayers are equipped to handle the intricacies of asset sales, allowing them to fulfill their reporting obligations while optimizing their tax situation.

Form 4797 |

|

Sales of Business Property |

|

OMB No. |

|

|

|

||||

|

|

|

|

||

|

|

|

|

|

|

|

(Also Involuntary Conversions and Recapture Amounts |

|

2019 |

||

|

|

Under Sections 179 and 280F(b)(2)) |

|

||

Department of the Treasury |

|

Attach to your tax return. |

|

Attachment |

|

Internal Revenue Service |

|

Go to www.irs.gov/Form4797 for instructions and the latest information. |

|

Sequence No. 27 |

|

|

|

|

|

|

|

Name(s) shown on return |

|

|

Identifying number |

||

|

|

|

|

|

|

1Enter the gross proceeds from sales or exchanges reported to you for 2019 on Form(s)

1

Part I |

Sales or Exchanges of Property Used in a Trade or Business and Involuntary Conversions From Other |

|||||||

|

Than Casualty or |

|

||||||

2 |

(a) Description |

(b) Date acquired |

(c) Date sold |

(d) Gross |

(e) Depreciation |

(f) Cost or other |

(g) Gain or (loss) |

|

allowed or |

basis, plus |

|||||||

Subtract (f) from the |

||||||||

|

of property |

(mo., day, yr.) |

(mo., day, yr.) |

sales price |

allowable since |

improvements and |

||

|

sum of (d) and (e) |

|||||||

|

|

|

|

|

acquisition |

expense of sale |

||

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

Gain, if any, from Form 4684, line 39 |

3 |

4 |

Section 1231 gain from installment sales from Form 6252, line 26 or 37 |

4 |

5 |

Section 1231 gain or (loss) from |

5 |

6 |

Gain, if any, from line 32, from other than casualty or theft |

6 |

7 |

Combine lines 2 through 6. Enter the gain or (loss) here and on the appropriate line as follows |

7 |

|

Partnerships and S corporations. Report the gain or (loss) following the instructions for Form 1065, Schedule K, |

|

|

line 10, or Form |

|

Individuals, partners, S corporation shareholders, and all others. If line 7 is zero or a loss, enter the amount from line 7 on line 11 below and skip lines 8 and 9. If line 7 is a gain and you didn’t have any prior year section 1231 losses, or they were recaptured in an earlier year, enter the gain from line 7 as a

8 Nonrecaptured net section 1231 losses from prior years. See instructions |

8 |

9Subtract line 8 from line 7. If zero or less, enter

capital gain on the Schedule D filed with your return. See instructions |

9 |

Part II Ordinary Gains and Losses (see instructions)

10Ordinary gains and losses not included on lines 11 through 16 (include property held 1 year or less):

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

11 |

Loss, if any, from line 7 |

11 |

( |

) |

|||||

12 |

Gain, if any, from line 7 or amount from line 8, if applicable |

12 |

|

|

|||||

13 |

Gain, if any, from line 31 |

13 |

|

|

|||||

14 |

Net gain or (loss) from Form 4684, lines 31 and 38a |

14 |

|

|

|||||

15 |

Ordinary gain from installment sales from Form 6252, line 25 or 36 |

15 |

|

|

|||||

16 |

Ordinary gain or (loss) from |

16 |

|

|

|||||

17 |

Combine lines 10 through 16 |

17 |

|

|

|||||

18For all except individual returns, enter the amount from line 17 on the appropriate line of your return and skip lines a and b below. For individual returns, complete lines a and b below.

aIf the loss on line 11 includes a loss from Form 4684, line 35, column (b)(ii), enter that part of the loss here. Enter the loss from

property used as an employee.) Identify as from “Form 4797, line 18a.” See instructions |

18a |

bRedetermine the gain or (loss) on line 17 excluding the loss, if any, on line 18a. Enter here and on Schedule 1

(Form 1040 or Form |

18b |

|

For Paperwork Reduction Act Notice, see separate instructions. |

Cat. No. 13086I |

Form 4797 (2019) |

Form 4797 (2019) |

|

|

|

Page 2 |

|||

Part III |

Gain From Disposition of Property Under Sections 1245, 1250, 1252, 1254, and 1255 |

|

|||||

|

|

(see instructions) |

|

|

|

|

|

19 |

(a) |

Description of section 1245, 1250, 1252, 1254, or 1255 property: |

|

(b) Date acquired |

(c) Date sold |

||

|

(mo., day, yr.) |

(mo., day, yr.) |

|||||

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

A |

|

|

|

|

|

|

|

B |

|

|

|

|

|

|

|

C |

|

|

|

|

|

|

|

D |

|

|

|

|

|

|

|

|

These columns relate to the properties on lines 19A through 19D. |

Property A |

Property B |

Property C |

Property D |

||

|

|

|

|

|

|||

20 |

Gross sales price (Note: See line 1 before completing.) . |

|

20 |

|

|

|

|

21 |

Cost or other basis plus expense of sale |

|

21 |

|

|

|

|

22 |

Depreciation (or depletion) allowed or allowable . . . |

|

22 |

|

|

|

|

23 |

Adjusted basis. Subtract line 22 from line 21. . . . |

|

23 |

|

|

|

|

24 |

Total gain. Subtract line 23 from line 20 |

24 |

|

|

|

||

25 |

If section 1245 property: |

|

|

|

|

||

a |

Depreciation allowed or allowable from line 22 . . . |

|

25a |

|

|

|

|

b |

Enter the smaller of line 24 or 25a |

25b |

|

|

|

||

26If section 1250 property: If straight line depreciation was used, enter

a Additional depreciation after 1975. See instructions . |

26a |

bApplicable percentage multiplied by the smaller of line

24 or line 26a. See instructions |

26b |

cSubtract line 26a from line 24. If residential rental property

|

or line 24 isn’t more than line 26a, skip lines 26d and 26e |

26c |

d |

Additional depreciation after 1969 and before 1976. . |

26d |

e |

Enter the smaller of line 26c or 26d |

26e |

f |

Section 291 amount (corporations only) |

26f |

g |

Add lines 26b, 26e, and 26f |

26g |

27If section 1252 property: Skip this section if you didn’t dispose of farmland or if this form is being completed for a partnership.

a |

Soil, water, and land clearing expenses |

27a |

b Line 27a multiplied by applicable percentage. See instructions |

27b |

|

c |

Enter the smaller of line 24 or 27b |

27c |

28 If section 1254 property: |

|

|

a Intangible drilling and development costs, expenditures |

|

|

|

for development of mines and other natural deposits, |

|

|

mining exploration costs, and depletion. See instructions |

28a |

b |

Enter the smaller of line 24 or 28a |

28b |

29 If section 1255 property: |

|

|

a Applicable percentage of payments excluded from |

|

|

|

income under section 126. See instructions . . . . |

29a |

b |

Enter the smaller of line 24 or 29a. See instructions . |

29b |

Summary of Part III Gains. Complete property columns A through D through line 29b before going to line 30.

30 |

Total gains for all properties. Add property columns A through D, line 24 |

31 |

Add property columns A through D, lines 25b, 26g, 27c, 28b, and 29b. Enter here and on line 13 |

32Subtract line 31 from line 30. Enter the portion from casualty or theft on Form 4684, line 33. Enter the portion from other than casualty or theft on Form 4797, line 6 . . . . . . . . . . . . . . . . . . . .

30

31

32

Part IV Recapture Amounts Under Sections 179 and 280F(b)(2) When Business Use Drops to 50% or Less

(see instructions)

|

|

|

(a) Section |

(b) Section |

|

|

|

179 |

280F(b)(2) |

33 |

|

|

|

|

Section 179 expense deduction or depreciation allowable in prior years |

33 |

|

|

|

34 |

Recomputed depreciation. See instructions |

34 |

|

|

35 |

Recapture amount. Subtract line 34 from line 33. See the instructions for where to report . . |

35 |

|

|

Form 4797 (2019)

| Fact Name | Description |

|---|---|

| Purpose | The IRS Form 4797 is primarily used to report the sale or exchange of business property. |

| Who Must File | Taxpayers who sell or exchange business property, including assets held for more than one year, are required to file this form. |

| Capital Gains and Losses | The form helps determine capital gains or losses on the sale of property, which can affect tax liabilities. |

| Filing Deadline | Form 4797 must be filed with your income tax return, typically by April 15, unless an extension is filed. |

| State-Specific Information | Some states may have their own forms for reporting similar transactions; consult your state's tax agency for details. |

| Record Keeping | It is crucial to maintain records of all transactions reported on Form 4797 as the IRS may request supporting documentation. |

| Electronic Filing | Taxpayers can typically e-file Form 4797 as part of their income tax return using various tax software options. |

Filling out the IRS Form 4797 requires attention to detail, as this form is crucial for reporting the sale of business property. After completing it, you will proceed to transfer relevant data to your tax return. Follow the steps below carefully to ensure accurate reporting.

Following these steps will help ensure accurate reporting. Pay attention to details throughout the process to avoid complications with the IRS.

IRS Form 4797 is used to report the sale or exchange of business property. This includes various types of assets, such as real estate, equipment, and other depreciable property. The form helps taxpayers calculate any gains or losses resulting from these transactions, which will ultimately affect their overall tax liability.

Taxpayers who sell or exchange business property need to file Form 4797. This applies to individuals, partnerships, corporations, and other entities that dispose of property used in a trade or business. If you have sold or exchanged fixed assets such as machinery, vehicles, or real estate for more than their adjusted basis, this form is necessary.

Filling out Form 4797 involves several steps:

Carefully review the instructions available on the IRS website, as they provide detailed guidance for each section of the form.

Failing to file Form 4797 when required can lead to serious consequences. The IRS may impose penalties for late filing or for not filing at all. Additionally, if you do not report gains or losses accurately, you may face additional taxes, interest on underpayments, or even audit risks. It is imperative to ensure that all necessary forms are filed correctly and on time to avoid these issues.

You can obtain IRS Form 4797 directly from the IRS website. The form is available for download in PDF format. You can also find instructions on how to complete the form. For those who prefer paper forms, you may request a physical copy by contacting the IRS. Always ensure you are using the correct version of the form for the tax year in question.

When individuals or businesses need to report the sale of property used in a trade or business, they often turn to IRS Form 4797. However, several common mistakes can lead to issues down the line. Understanding these mistakes can help ensure a smoother filing process.

One frequent error is failing to categorize the property correctly. Form 4797 is used for different types of property transactions, including the sale of business assets and capital gains. Misclassifying the property can lead to incorrect calculations and penalties. It's crucial to determine if the property is subject to Section 1231 treatment or falls under different categories.

Another common mistake is incomplete or inaccurate calculations. Whether it’s determining the adjusted basis of the property or calculating depreciation, errors can significantly affect the final tax liability. Double-checking these figures ensures the report aligns with financial records and the IRS guidelines.

Some people overlook reporting all necessary sales details. When completing Form 4797, ensuring every sale is accounted for is essential. Missing out on multiple sales can raise flags during an audit, leading to possible financial or legal repercussions.

Neglecting to include depreciation recapture is another mistake that can have serious consequences. When claiming deductions for depreciation, it’s vital to understand that recapturing that depreciation upon sale alters the tax implications. Failure to report this accurately can lead to substantial underpayment of taxes.

Additionally, not filing by the deadline can be a significant oversight. Timely submission is critical to avoid penalties. People sometimes miscalculate when the sale occurred or confuse deadlines, leading to unnecessary fees or interest accrual.

Lastly, not seeking professional advice can be a costly mistake. Tax laws can be complex. Consulting with a tax professional ensures that individuals understand the requirements of Form 4797 and helps in correctly reporting transactions. This can save both time and money in the long run.

The IRS Form 4797, titled "Sales of Business Property," is used to report the sale or exchange of business property and may require some accompanying documents or forms for complete submission. Here is a list of other forms and documents commonly related to Form 4797, along with brief explanations of each.

Understanding which documents are needed along with the IRS Form 4797 is crucial for ensuring accurate reporting and compliance with tax regulations. Ensuring that all accompanying forms are completed correctly will aid in a smoother tax filing experience and help avoid potential audits or inquiries from the IRS.

When filling out the IRS Form 4797, there are important guidelines to follow for accurate submission. Below are essential dos and don’ts to keep in mind.

By following these guidelines, you can help ensure that your IRS Form 4797 is completed accurately, potentially avoiding delays or issues with your tax return.

When it comes to tax forms, the IRS 4797 is often surrounded by a number of misconceptions. This form is used to report the sale of business property, and understanding it can help taxpayers navigate their tax obligations effectively. Here are some of the common misconceptions related to the IRS 4797 form:

Understanding these misconceptions will help taxpayers feel more confident when dealing with IRS Form 4797. Taking the time to learn about its requirements ensures accurate reporting and compliance, ultimately leading to a smoother tax experience.

When filling out and using the IRS Form 4797, which is essential for reporting the sale of business property, there are several key takeaways to keep in mind: