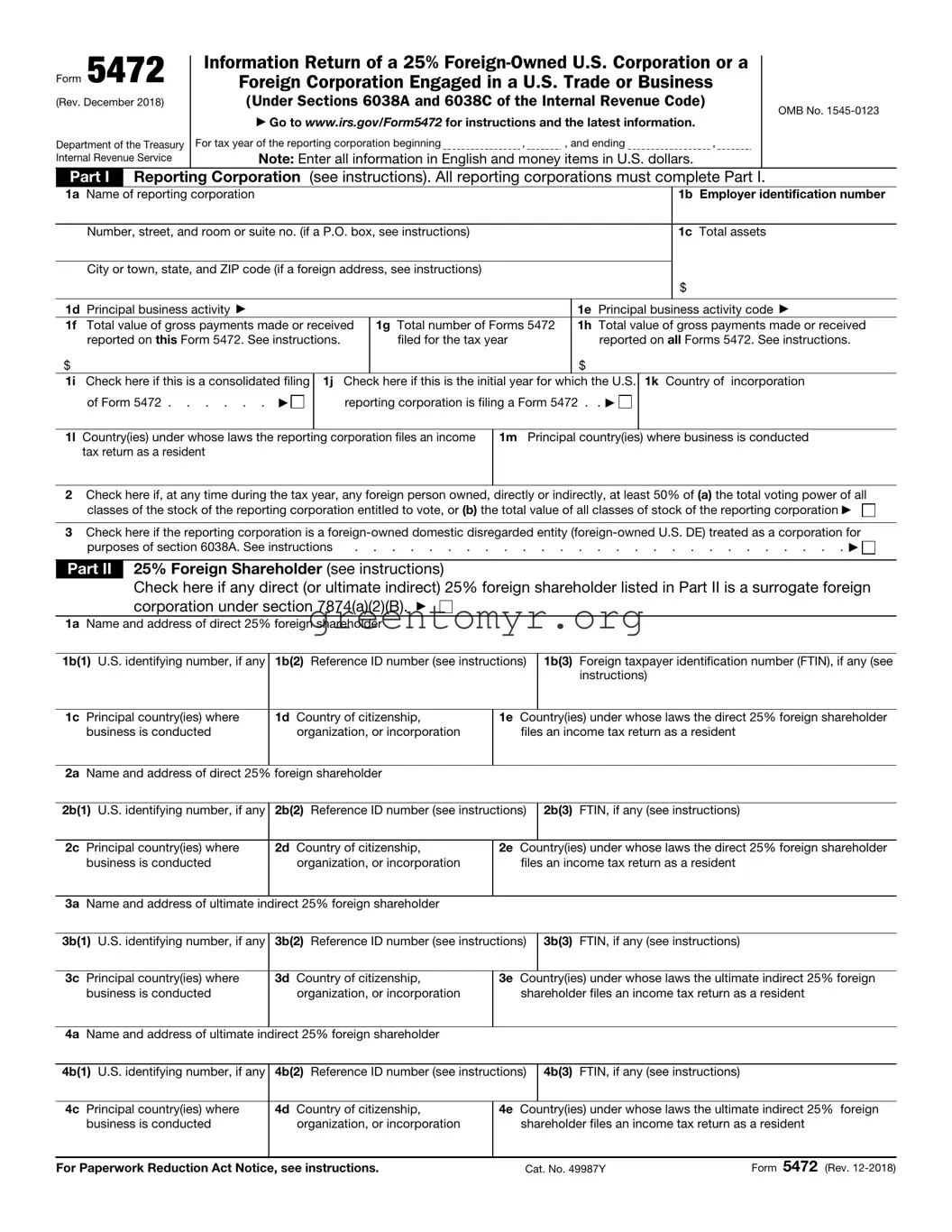

The IRS Form 5472 plays an essential role for foreign-owned corporations and U.S. businesses with foreign owners. Designed to facilitate reporting on transactions between these entities, the form is a crucial tool in promoting transparency and ensuring compliance with tax regulations. If you own a foreign corporation or are a U.S. resident with foreign ownership in your business, understanding this form is vital. You'll need to disclose various details, including the nature of the transactions, the amounts involved, and the relationship between the parties. Failing to file this form can result in significant penalties, including hefty fines and potential complications in your tax filings. Knowing the requirements and deadlines for Form 5472 not only helps avoid pitfalls but can also ensure your business remains in good standing with the IRS. With its intricate requirements and deadlines, navigating the complexities of this form can seem overwhelming, but being informed and prepared can make the process smoother.

Form 5472 |

Information Return of a 25% |

|

Foreign Corporation Engaged in a U.S. Trade or Business |

|

|

(Rev. December 2018) |

(Under Sections 6038A and 6038C of the Internal Revenue Code) |

OMB No. |

|

|

▶Go to www.irs.gov/Form5472 for instructions and the latest information.

Department of the Treasury |

For tax year of the reporting corporation beginning |

, |

, and ending |

, |

Internal Revenue Service |

Note: Enter all information in English and money items in U.S. dollars. |

|

||

Part I Reporting Corporation (see instructions). All reporting corporations must complete Part I.

1a Name of reporting corporation |

|

|

|

|

|

1b Employer identification number |

|

|

|

|

|

|

|

|

|

Number, street, and room or suite no. (if a P.O. box, see instructions) |

|

|

|

1c Total assets |

|||

|

|

|

|

|

|

|

|

City or town, state, and ZIP code (if a foreign address, see instructions) |

|

|

|

|

|||

|

|

|

|

|

|

|

$ |

|

|

|

|

|

|

|

|

1d Principal business activity ▶ |

|

|

|

1e Principal business activity code ▶ |

|||

1f Total value of gross payments made or received |

1g Total number of Forms 5472 |

1h Total value of gross payments made or received |

|||||

reported on this Form 5472. See instructions. |

|

filed for the tax year |

reported on all Forms 5472. See instructions. |

||||

$ |

|

|

|

|

$ |

|

|

1i Check here if this is a consolidated filing |

1j |

Check here if this is the initial year for which the U.S. |

1k Country of incorporation |

||||

of Form 5472 . . . . . . ▶ |

|

reporting corporation is filing a Form 5472 . . ▶ |

|

||||

|

|

|

|

||||

1l Country(ies) under whose laws the reporting corporation files an income |

1m Principal country(ies) where business is conducted |

||||||

tax return as a resident |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

2Check here if, at any time during the tax year, any foreign person owned, directly or indirectly, at least 50% of (a) the total voting power of all

classes of the stock of the reporting corporation entitled to vote, or (b) the total value of all classes of stock of the reporting corporation ▶

3Check here if the reporting corporation is a

purposes of section 6038A. See instructions |

. . . . . . . . . . . . . . . . . . . . . . . . . . . ▶ |

Part II 25% Foreign Shareholder (see instructions)

Check here if any direct (or ultimate indirect) 25% foreign shareholder listed in Part II is a surrogate foreign corporation under section 7874(a)(2)(B). ▶

1a Name and address of direct 25% foreign shareholder

1b(1) U.S. identifying number, if any |

1b(2) Reference ID number (see instructions) |

1b(3) Foreign taxpayer identification number (FTIN), if any (see |

||||

|

|

|

|

|

instructions) |

|

|

|

|

|

|

|

|

1c |

Principal country(ies) where |

1d Country of citizenship, |

1e |

Country(ies) under whose laws the direct 25% foreign shareholder |

||

|

business is conducted |

organization, or incorporation |

|

files an income tax return as a resident |

|

|

|

|

|

|

|

|

|

2a |

Name and address of direct 25% |

foreign shareholder |

|

|

|

|

|

|

|

|

|||

2b(1) U.S. identifying number, if any |

2b(2) Reference ID number (see instructions) |

2b(3) FTIN, if any (see instructions) |

|

|||

|

|

|

|

|

|

|

2c |

Principal country(ies) where |

2d Country of citizenship, |

2e |

Country(ies) under whose laws the direct 25% foreign shareholder |

||

|

business is conducted |

organization, or incorporation |

|

files an income tax return as a resident |

|

|

|

|

|

|

|

|

|

3a |

Name and address of ultimate indirect 25% foreign shareholder |

|

|

|

|

|

|

|

|

|

|||

3b(1) U.S. identifying number, if any |

3b(2) Reference ID number (see instructions) |

3b(3) FTIN, if any (see instructions) |

|

|||

|

|

|

|

|

|

|

3c |

Principal country(ies) where |

3d Country of citizenship, |

3e |

Country(ies) under whose laws the ultimate indirect 25% foreign |

||

|

business is conducted |

organization, or incorporation |

|

shareholder files an income tax return as a resident |

||

|

|

|

|

|

|

|

4a |

Name and address of ultimate indirect 25% foreign shareholder |

|

|

|

|

|

|

|

|

|

|||

4b(1) U.S. identifying number, if any |

4b(2) Reference ID number (see instructions) |

4b(3) FTIN, if any (see instructions) |

|

|||

|

|

|

|

|

|

|

4c |

Principal country(ies) where |

4d Country of citizenship, |

4e |

Country(ies) under whose laws the ultimate indirect 25% foreign |

||

|

business is conducted |

organization, or incorporation |

|

shareholder files an income tax return as a resident |

||

|

|

|

|

|

||

For Paperwork Reduction Act Notice, see instructions. |

|

Cat. No. 49987Y |

Form 5472 (Rev. |

|||

Form 5472 (Rev. |

Page 2 |

Part III Related Party (see instructions). All reporting corporations must complete this question and the rest of Part III. Check applicable box: Is the related party a  foreign person or

foreign person or  U.S. person?

U.S. person?

1a Name and address of related party

1b(1) U.S. identifying number, if any

1b(2) Reference ID number (see instructions)

1b(3) FTIN, if any (see instructions)

1c |

Principal business activity ▶ |

|

|

|

1d Principal business activity code ▶ |

|

1e |

Related to reporting corporation |

Related to 25% foreign shareholder |

25% foreign shareholder |

|||

1f |

Principal country(ies) where business is conducted |

1g Country(ies) under whose laws the related party files an income tax return as a |

||||

|

|

|

resident |

|

|

|

Part IV |

Monetary Transactions Between Reporting Corporations and Foreign Related Party (see instructions) |

|||||

|

|

Caution: Part IV must be completed if the “foreign person” box is checked in the heading for Part III. |

||||

|

|

If estimates are used, check here. ▶ |

|

|

|

|

|

|

|

|

|

||

1 |

Sales of stock in trade (inventory) |

1 |

|

|||

2 |

Sales of tangible property other than stock in trade |

2 |

|

|||

3 |

Platform contribution transaction payments received |

3 |

|

|||

4 |

4 |

|

||||

5a |

Rents received (for other than intangible property rights) |

5a |

|

|||

b |

Royalties received (for other than intangible property rights) |

5b |

|

|||

6 |

Sales, leases, licenses, etc., of intangible property rights (for example, patents, trademarks, secret formulas) . . |

6 |

|

|||

7 |

Consideration received for technical, managerial, engineering, construction, scientific, or like services . . . . |

7 |

|

|||

8 |

Commissions received |

8 |

|

|||

9 |

Amounts borrowed (see instructions) a Beginning balance |

|

b Ending balance or monthly average ▶ |

9b |

|

|

10 |

Interest received |

10 |

|

|||

11 |

Premiums received for insurance or reinsurance |

11 |

|

|||

12 |

Other amounts received (see instructions) |

12 |

|

|||

13 |

Total. Combine amounts on lines 1 through 12 |

13 |

|

|||

14 |

Purchases of stock in trade (inventory) |

14 |

|

|||

15 |

Purchases of tangible property other than stock in trade |

15 |

|

|||

16 |

Platform contribution transaction payments paid |

16 |

|

|||

17 |

17 |

|

||||

18a |

Rents paid (for other than intangible property rights) |

18a |

|

|||

b |

Royalties paid (for other than intangible property rights) |

18b |

|

|||

19 |

Purchases, leases, licenses, etc., of intangible property rights (for example, patents, trademarks, secret formulas) |

19 |

|

|||

20 |

Consideration paid for technical, managerial, engineering, construction, scientific, or like services |

20 |

|

|||

21 |

Commissions paid |

21 |

|

|||

22 |

Amounts loaned (see instructions) a Beginning balance |

|

b Ending balance or monthly average ▶ |

22b |

|

|

23 |

Interest paid |

23 |

|

|||

24 |

Premiums paid for insurance or reinsurance |

24 |

|

|||

25 |

Other amounts paid (see instructions) |

25 |

|

|||

26 |

Total. Combine amounts on lines 14 through 25 |

26 |

|

|||

Part V |

Reportable Transactions of a Reporting Corporation That is a |

|||||

|

|

Describe on an attached separate sheet any other transaction as defined by Regulations section |

||||

|

|

such as amounts paid or received in connection with the formation, dissolution, acquisition, and disposition |

||||

|

|

of the entity, including contributions to and distributions from the entity, and check here. ▶ |

||||

|

|

|||||

Part VI |

Nonmonetary and |

|||||

|

|

the Foreign Related Party (see instructions) |

|

|

|

|

|

|

Describe these transactions on an attached separate sheet and check here. ▶ |

|

|

||

Form 5472 (Rev.

Form 5472 (Rev. |

Page 3 |

|

Part VII |

Additional Information. |

All reporting corporations must complete Part VII. |

1 |

Does the reporting corporation import goods from a foreign related party? |

2a |

If “Yes,” is the basis or inventory cost of the goods valued at greater than the customs value of the imported goods? . |

bIf “Yes,” attach a statement explaining the reason or reasons for such difference.

Yes Yes

No No

cIf the answers to questions 1 and 2a are “Yes,” were the documents used to support this treatment of the imported

goods in existence and available in the United States at the time of filing Form 5472? . . . . . . . . . . .

3 During the tax year, was the foreign parent corporation a participant in any

4During the course of the tax year, did the foreign parent corporation become a participant in any

5a During the tax year, did the reporting corporation pay or accrue any interest or royalty, to the related party, for which the deduction is not allowed under section 267A? See instructions . . . . . . . . . . . . . . . . . .

Yes

Yes

Yes

Yes

No

No

No

No

b If “Yes,” enter the total amount of the disallowed deductions . |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

$ |

|

|

6a Does the reporting corporation claim a |

|

|

|||||||||||||||||

respect to amounts listed in Part IV? |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

. |

Yes |

No |

bIf “Yes,” enter the amount of gross income derived from sales, leases, exchanges, or other dispositions (but not licenses) of property to the foreign related party that the reporting corporation included in its computation of

deduction eligible income (FDDEI). See instructions . . . . . . . . . . . . . . . . . . . . $

cIf “Yes,” enter the amount of gross income derived from a license of property to the foreign related party that the

reporting corporation included in its computation of FDDEI. See instructions. . . . . . . . . . . . . $

dIf “Yes,” enter the amount of gross income derived from services provided to the foreign related party that the reporting

corporation included in its computation of FDDEI. See instructions . . . . . . . . . . . . . . . $

Part VIII Base Erosion Payments and Base Erosion Tax Benefits Under Section 59A (see instructions)

1 |

Amounts defined as base erosion payments under section 59A(d) |

. |

$ |

|

2 |

Amount of base erosion tax benefits under section 59A(c)(2) |

. |

$ |

|

3 |

Amount of total qualified derivative payments as described in section 59A(h) made by the reporting corporation . |

. |

$ |

|

4 |

Reserved for future use |

|

|

|

|

|

|

||

Form 5472 (Rev.

| Fact Name | Details |

|---|---|

| Purpose | The IRS Form 5472 is used to provide information regarding reportable transactions between a reporting corporation and a foreign related party. |

| Who Must File | Domestic corporations that are 25% foreign-owned must file this form if they engage in reportable transactions. |

| Filing Deadline | Form 5472 must be filed by the due date of the corporate tax return, including extensions. |

| Penalties for Non-Compliance | Failure to file Form 5472 can result in penalties of $25,000 per year, plus additional penalties for continued failure to file. |

| Form Location | The IRS Form 5472 can be downloaded from the official IRS website for free. |

| Additional Information Required | Along with the form, taxpayers must provide details such as the names and addresses of foreign related parties and the nature of their transactions. |

| Record Keeping | Certain records related to transactions must be maintained for five years from the date the return is filed. |

| Governing Laws | The IRS Form 5472 is governed by the Internal Revenue Code and associated IRS regulations. |

If you are required to file the IRS Form 5472, you will need to provide accurate information to ensure compliance with U.S. tax laws. Completing this form can seem daunting, but taking it step by step can make the process more manageable. Here’s how to fill it out correctly.

IRS Form 5472 is used to report information regarding transactions between a reporting corporation and related foreign entities. This form is mandatory for certain U.S. corporations and foreign corporations conducting business in the U.S.

Both U.S. corporations that are at least 25% foreign-owned and foreign corporations engaged in a trade or business in the United States must file Form 5472. It's also necessary if the corporation has reportable transactions with foreign related parties.

Reportable transactions include any exchange of money, goods, or services between the corporation and foreign related parties. This can involve sales, rentals, royalties, or any other types of payments that meet these conditions.

Form 5472 must be filed with the corporation's tax return. If the return is due on the 15th day of the fourth month after the end of the corporation's tax year, Form 5472 must be submitted by the same date. Extensions may apply if the tax return is extended.

Failing to file Form 5472 can result in significant penalties. Generally, the penalty is $25,000 for each form not filed completely and accurately. Additional penalties may apply for continuing failures.

Yes, Form 5472 can be filed electronically if it is included with the corporation’s income tax return. The corporation must have an approved e-filing option for the IRS to accept the form electronically.

To complete Form 5472, the following information is generally required:

Form 5472 can be downloaded from the IRS website. It is available in PDF format, and the accompanying instructions can also be found on the site to assist with completing the form.

No, there is no foreign version of Form 5472. The form must be completed in English and follow the instructions provided by the IRS for accurate reporting.

If assistance is needed, consider consulting a tax professional familiar with international business transactions and IRS regulations. They can provide guidance and ensure compliance with all requirements.

Filling out the IRS Form 5472 can be challenging, and mistakes can lead to significant penalties. One common error occurs when individuals fail to identify the reporting corporation correctly. It is crucial to use the exact legal name and Employer Identification Number (EIN) of the corporation to ensure accurate processing.

Another frequent mistake is neglecting to include all required information about foreign owners. If a foreign individual or entity owns at least 25% of the U.S. corporation, their details must be reported. Omitting this crucial information could trigger penalties.

Many people also misunderstand the reporting obligations. They may fail to recognize that Form 5472 must be filed if the reporting corporation engages in any transactions with a foreign related party, regardless of the amount. Failing to understand this could result in noncompliance.

Errors in reporting transaction amounts can lead to misinterpretation. Individuals may enter incorrect amounts or forget to convert foreign currency transactions into U.S. dollars. Accurate reporting is critical to avoid issues with the IRS.

Another mistake involves not providing sufficient detail on the types of transactions. The IRS requires clear descriptions of each transaction type, such as sales, loans, or asset transfers. Lack of specificity might raise questions during a review.

Ignoring or misunderstanding the deadline for filing Form 5472 can also result in penalties. The form must be submitted with the corporation’s income tax return, but it also can be filed separately if necessary. Missing the deadline can have serious consequences.

Some individuals incorrectly assume they can file Form 5472 in a subsequent year. This is inaccurate; the form must be submitted for each year that a reporting corporation conducts transactions with foreign related parties. Failure to do so for each tax year is a mistake.

Providing incomplete signatures or missing the required certifications can invalidate the form. The individuals responsible for preparing the return must review and ensure all certifications are complete. Omitting these steps can cause delays and additional scrutiny from the IRS.

Lastly, individuals often fail to retain adequate records and documentation relating to the transactions reported on Form 5472. Keeping organized and accurate records is essential for compliance and can help if the IRS requests additional information.

Addressing these mistakes during the preparation of Form 5472 can help individuals avoid penalties and ensure compliance with IRS regulations. Thorough review and adherence to guidelines can significantly improve the filing process.

The IRS Form 5472 is used by certain foreign-owned domestic corporations to report transactions with related parties. When filing this form, several other documents are typically necessary to provide comprehensive information to the IRS. Below is a list of forms and documents commonly associated with Form 5472.

Gathering these forms and documents in advance can facilitate a smoother filing process. Proper documentation ensures compliance and helps avoid potential issues with the IRS. Always consider consulting a tax professional if you have questions about your specific situation.

Filling out the IRS Form 5472 can seem overwhelming, but staying focused on key dos and don’ts can simplify the process. Here’s a helpful list:

Taking these steps can help ensure a smoother filing experience, so pay careful attention to details. It’s crucial to get it right the first time.

The IRS Form 5472 can be confusing for many taxpayers, especially those unfamiliar with international transactions or foreign entities. Here are four common misconceptions about this form:

No matter the misconceptions, understanding your obligations regarding IRS Form 5472 is key to maintaining compliance and avoiding penalties. When in doubt, consulting a tax professional can provide clarity and guidance.

Filling out the IRS 5472 form can seem daunting, but it is crucial for certain foreign-owned U.S. entities. Here are key takeaways to help you navigate the process.