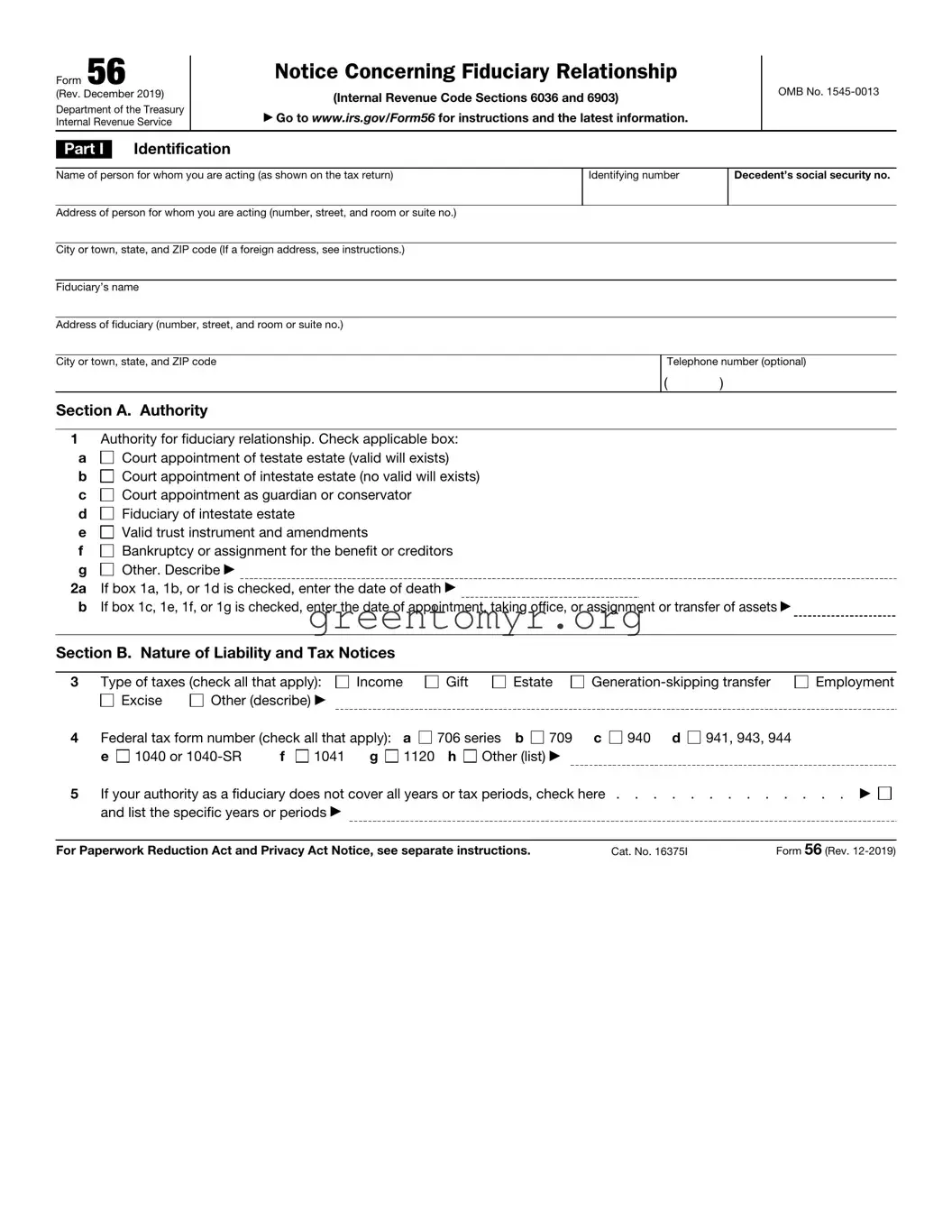

Form 56, also known as the Notice Concerning Fiduciary Relationship, plays a crucial role in managing the estate of a deceased individual or representing a trust. This form is essential for anyone acting as a fiduciary—this could include executors, administrators, or guardians—who need to establish their authority to act on behalf of another party. It requires detailed information such as the name of the individual for whom the fiduciary is acting, the fiduciary's details, and the reason for the fiduciary relationship. Additionally, the form seeks to clarify the nature of any tax liabilities that may exist, allowing the fiduciary to check appropriate boxes related to income, gift, and estate taxes. Those completing the form also must indicate the specific federal tax form numbers they anticipate filing. Importantly, the form has sections dedicated to the revocation or termination of prior notices and any potential substitution of fiduciaries, ensuring clarity and proper record-keeping. To ensure the accuracy of the provided information, the signature section requires the fiduciary to affirm the truthfulness of their statements under penalties of perjury. By understanding the significance of Form 56, fiduciaries can better navigate their responsibilities while ensuring compliance with IRS requirements.

Form 56 |

|

|

Notice Concerning Fiduciary Relationship |

|

|

|

|||

|

|

|

|

|

|||||

(Rev. December 2019) |

|

(Internal Revenue Code Sections 6036 and 6903) |

|

|

OMB No. |

||||

|

|

|

|

||||||

Department of the Treasury |

|

▶ Go to www.irs.gov/Form56 for instructions and the latest information. |

|

|

|

||||

Internal Revenue Service |

|

|

|

|

|||||

|

|

Identification |

|

|

|

|

|

|

|

Part I |

|

|

|

|

|

|

|||

|

|

|

|

|

|||||

Name of person for whom you are acting (as shown on the tax return) |

Identifying number |

|

Decedent’s social security no. |

||||||

|

|

|

|

|

|

||||

Address of person for whom you are acting (number, street, and room or suite no.) |

|

|

|

|

|

||||

|

|

|

|

|

|

||||

City or town, state, and ZIP code (If a foreign address, see instructions.) |

|

|

|

|

|

||||

|

|

|

|

|

|

|

|||

Fiduciary’s name |

|

|

|

|

|

|

|||

|

|

|

|

|

|

||||

Address of fiduciary (number, street, and room or suite no.) |

|

|

|

|

|

||||

|

|

|

|

||||||

City or town, state, and ZIP code |

|

|

Telephone number (optional) |

||||||

|

|

|

|

|

|

( |

) |

|

|

Section A. Authority

1Authority for fiduciary relationship. Check applicable box:

a Court appointment of testate estate (valid will exists)

Court appointment of testate estate (valid will exists)

b Court appointment of intestate estate (no valid will exists)

Court appointment of intestate estate (no valid will exists)

c Court appointment as guardian or conservator

Court appointment as guardian or conservator

d Fiduciary of intestate estate

Fiduciary of intestate estate

e Valid trust instrument and amendments

Valid trust instrument and amendments

f Bankruptcy or assignment for the benefit or creditors

Bankruptcy or assignment for the benefit or creditors

g Other. Describe ▶

Other. Describe ▶

2a If box 1a, 1b, or 1d is checked, enter the date of death ▶

bIf box 1c, 1e, 1f, or 1g is checked, enter the date of appointment, taking office, or assignment or transfer of assets ▶

Section B. Nature of Liability and Tax Notices

3 |

Type of taxes (check all that apply): |

Income |

|

Gift |

|

Estate |

||||||||

|

|

Excise |

Other (describe) ▶ |

|

|

|

|

|

|

|

|

|

||

4 |

Federal tax form number (check all that apply): |

a |

706 series |

b |

709 |

c |

940 d |

941, 943, 944 |

||||||

|

e |

1040 or |

f |

1041 |

g |

1120 |

h |

Other (list) ▶ |

|

|

|

|||

Employment

5If your authority as a fiduciary does not cover all years or tax periods, check here . . . . . . . . . . . . . ▶

and list the specific years or periods ▶

and list the specific years or periods ▶

For Paperwork Reduction Act and Privacy Act Notice, see separate instructions. |

Cat. No. 16375I |

Form 56 (Rev. |

Form 56 (Rev. |

Page 2 |

|

|

|

|

|

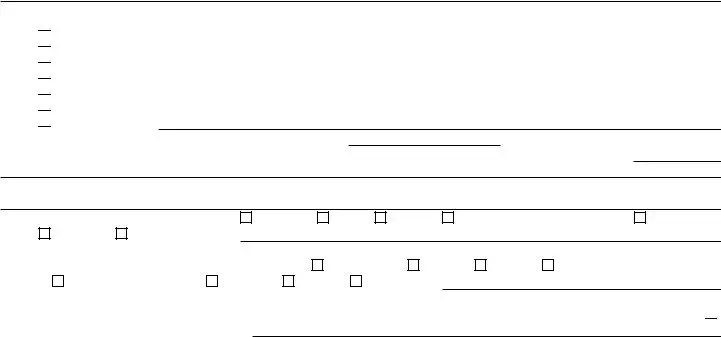

Revocation or Termination of Notice |

|

Part II |

|

|

Section

6Check this box if you are revoking or terminating all prior notices concerning fiduciary relationships on file with the Internal

Revenue Service for the same tax matters and years or periods covered by this notice concerning fiduciary relationship ▶

a b c

Reason for termination of fiduciary relationship. Check applicable box:

Court order revoking fiduciary authority

Court order revoking fiduciary authority

Certificate of dissolution or termination of a business entity Other. Describe ▶

Section

7a Check this box if you are revoking earlier notices concerning fiduciary relationships on file with the Internal Revenue Service for the same tax matters and years or periods covered by this notice concerning fiduciary relationship . . . . . . ▶

bSpecify to whom granted, date, and address, including ZIP code.

▶

Section

8Check this box if a new fiduciary or fiduciaries have been or will be substituted for the revoking or terminating fiduciary and

specify the name(s) and address(es), including ZIP code(s), of the new fiduciary(ies) . . . . . . . . . . . . ▶

▶

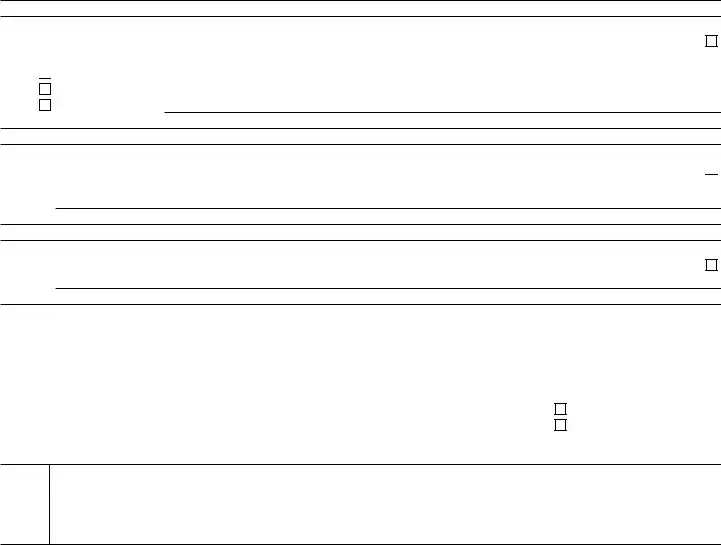

Part III |

Court and Administrative Proceedings |

|

|

|

|

|

|

|

|

|

|

||

Name of court (if other than a court proceeding, identify the type of proceeding and name of agency) |

Date proceeding initiated |

|||||

|

|

|

|

|

||

Address of court |

|

Docket number of proceeding |

||||

|

|

|

|

|

|

|

City or town, state, and ZIP code |

Date |

|

Time |

a.m. |

Place of other proceedings |

|

|

|

|

|

|

p.m. |

|

|

|

|

|

|

|

|

Part IV

Please

Sign

Here

Signature

Under penalties of perjury, I declare that I have examined this document, including any accompanying statements, and to the best of my knowledge and belief, it is true, correct, and complete.

▲ |

|

|

|

|

|

Fiduciary’s signature |

|

Title, if applicable |

|

Date |

Form 56 (Rev.

| Fact | Description |

|---|---|

| Purpose | Form 56 is used to notify the IRS of a fiduciary relationship, such as in cases related to estates or trusts. |

| Governing Law | This form is governed by the Internal Revenue Code sections 6036 and 6903. |

| Identification Information | The form requires basic information about the person for whom you are acting, including their name, address, and identifying numbers. |

| Authority | Filers must indicate the authority under which they are acting, such as through a court appointment or a valid trust instrument. |

| Type of Taxes | Form 56 allows you to specify the type of taxes related to the fiduciary relationship, including income, gift, and estate taxes. |

| Revocation Process | The form can also be used to revoke or terminate prior fiduciary notices with the IRS, either completely or partially. |

Filling out the IRS Form 56 is necessary when acting on behalf of someone in a fiduciary relationship. This form notifies the IRS of your authority for tax matters related to that individual. After collecting the necessary information, follow the steps outlined below to ensure accurate completion of the form.

IRS Form 56 is known as the Notice Concerning Fiduciary Relationship. It informs the IRS about the existence of a fiduciary relationship, which can involve estates, trusts, or guardianship situations. This form is necessary for anyone who is acting on behalf of another person, especially in tax matters.

Any fiduciary acting on behalf of a person or entity should file Form 56. This includes executors of estates, trustees of trusts, and guardians. It is important to notify the IRS as soon as you accept a fiduciary role.

The form requires several key pieces of information:

The authority may come from various sources, including:

Check the appropriate box on the form that matches your situation.

If you are substituting for an existing fiduciary, you need to check a specific box and provide the names and addresses of the new fiduciaries. This ensures that the IRS is updated on who is currently handling the responsibilities.

Yes, you can revoke a previous Form 56 by checking the appropriate box on the form. This process requires you to specify the reason for the termination of the fiduciary relationship and detail any court orders or certificates that apply.

You can report various types of taxes on Form 56, including:

Yes, the IRS has strict privacy measures in place. However, as with any submission of personal information, ensure that you provide accurate details and follow filing guidelines carefully.

For more guidance and up-to-date information, visit the IRS website at www.irs.gov/Form56 . This site includes instructions specific to this form and additional resources.

File Form 56 as soon as you accept your fiduciary role. Timely filing helps prevent any complications with tax issues regarding the individual or entity you represent. If your authority only covers specific years or periods, take care to note this on the form.

Filling out IRS Form 56 can be a daunting task, and many people make mistakes that can lead to delays or complications in their fiduciary responsibilities. One common error includes failing to provide accurate identification numbers. Every fiduciary must include the Social Security number of the person they are representing. Omitting or misinputting this information can cause significant issues with the IRS.

Another frequent mistake is neglecting to indicate the correct type of fiduciary authority. This form has several checkboxes under Section A, and it’s crucial to select the one that accurately reflects your situation. Selecting the wrong category could lead to misunderstandings or even legal consequences regarding your fiduciary duties.

Many individuals also forget to enter important dates. When checking certain boxes, the form will require the date of death or the date of appointment. Skip this vital step, and the IRS may not process the form properly, leading to potential delays in any necessary tax matters.

A common oversight is checking too few boxes under the type of taxes section. It’s essential to identify all forms of taxes applicable to the fiduciary relationship. If you neglect to do this, it could hinder the IRS's understanding of your obligations and responsibilities.

In Section B, failing to specify particular years or periods when the fiduciary authority does not cover all tax matters is another prevalent error. If your authority is limited, the IRS needs to know this to ensure compliance with your fiduciary duties. Missing this information can lead to confusion and complications.

Additionally, when completing the revocation or termination section, it is vital to accurately describe the reason for termination. If you check the box without providing a clear reason, the IRS may require further clarification, potentially delaying the processing of the form.

Many people also fail to confirm that they have revoked previous notices properly. When submitting a form for the termination of fiduciary relationships, it is necessary to indicate if all prior notices are being revoked. Without this clarification, the IRS might not appreciate the full scope of your fiduciary responsibilities, leading to legal issues.

Another mistake involves incomplete signatures. The form requires that the fiduciary's signature be included under the penalties of perjury. Omitting your signature or not dating the document can render the form invalid. Always check that you’ve signed and dated the form appropriately before submitting it.

Lastly, people sometimes neglect to double-check their forms for accuracy. Before submitting, take a moment to review all the information provided. An errant typographical error or miscommunication can lead to significant problems with the IRS, such as audits or penalties.

Being aware of these common mistakes can make a substantial difference in the smooth processing of IRS Form 56. By taking the time to understand the requirements and checking for errors, fiduciaries can ensure their submissions are complete and accurate.

The IRS Form 56, titled "Notice Concerning Fiduciary Relationship," is often used in conjunction with several other forms and documents that serve specific purposes related to tax matters, estate management, and fiduciary responsibilities. Here’s a brief overview of those commonly associated documents.

Understanding these forms and their purposes will enhance a fiduciary's ability to navigate the complexities of tax obligations and estate management. Each plays a crucial role in ensuring compliance with tax laws while honoring the wishes of the deceased.

Filling out the IRS Form 56 correctly is crucial for establishing a fiduciary relationship. To help you navigate this process, here are some essential dos and don'ts.

This is not true. While it's common for lawyers to assist in the process, anyone who is acting as a fiduciary, such as an executor or guardian, can file Form 56. Understanding the responsibilities involved can help ensure the form is completed accurately.

Many people think this form is solely for decedents, but that's not the entire picture. Form 56 is also used for other fiduciary relationships, including guardianships and trusts. If you manage another person's assets or affairs, you may need to use this form.

This misunderstanding can lead to complications. Submitting Form 56 does not automatically revoke prior appointments unless you specifically check the relevant box on the form. Clarifying your intentions on the form is essential to avoid miscommunication with the IRS.

Some individuals believe that once Form 56 is filed, it's set in stone. However, you can submit a new Form 56 to amend your previous submission. It’s vital to accurately reflect any changes in your fiduciary status or authority.

This is a common concern that can create undue stress. File Form 56 doesn't mean you owe taxes; it simply notifies the IRS about your fiduciary relationship. Your tax responsibilities depend on the specific situation and should be determined through other tax filings.

When preparing to fill out and use IRS Form 56, it's essential to keep these key points in mind:

Using Form 56 correctly ensures that fiduciary responsibilities are clear, and it establishes a pathway for handling tax obligations effectively.