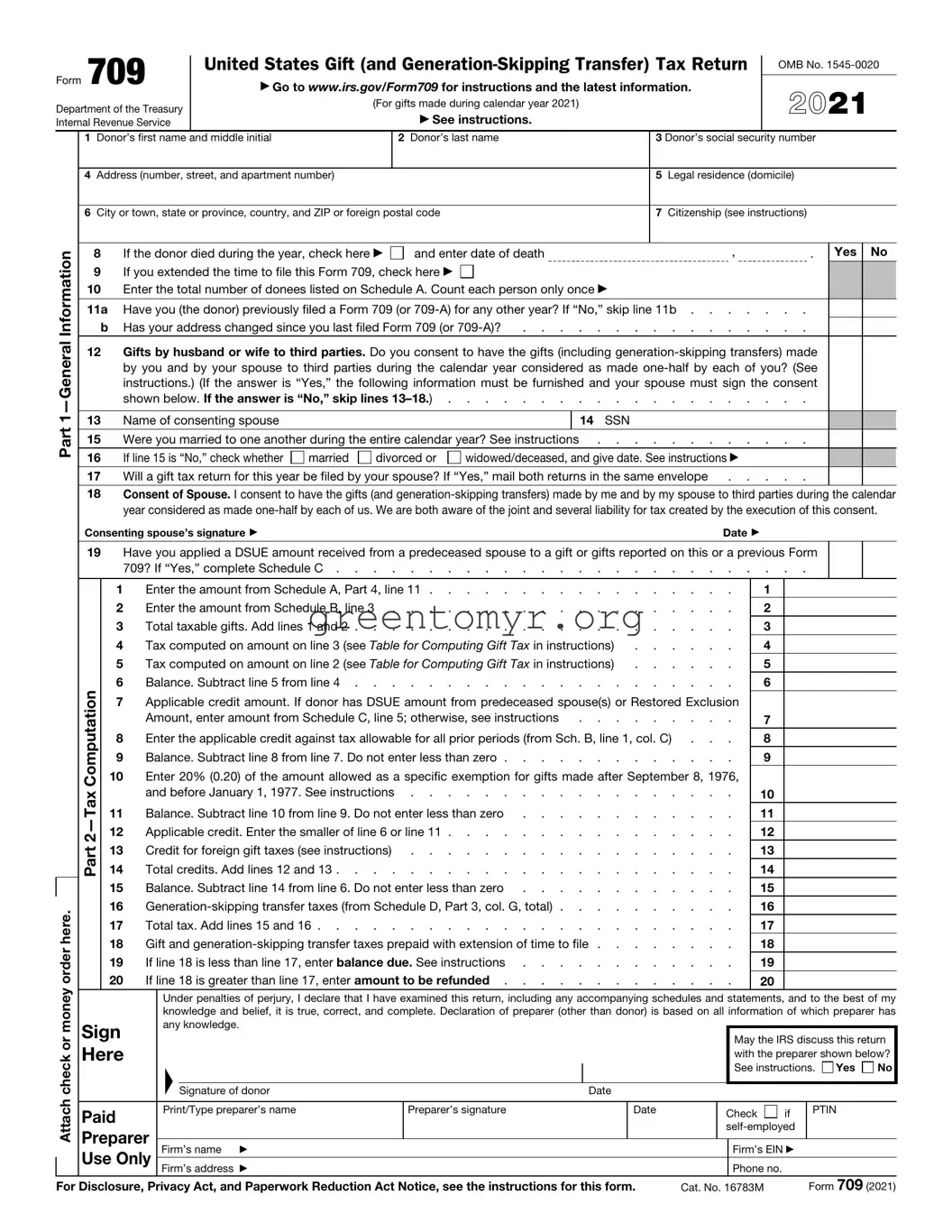

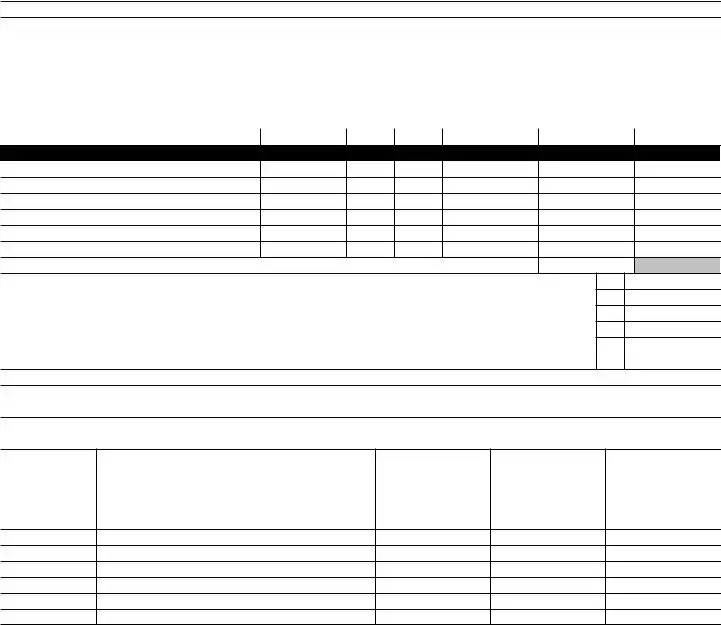

The IRS 709 form, commonly known as the United States Gift (and Generation-Skipping Transfer) Tax Return, plays a crucial role in the landscape of gift and estate tax regulations. Every year, countless individuals find themselves navigating the complexities of financial gifts, whether from family members or friends. The form primarily serves to report gifts that exceed the annual exclusion limit set by the IRS, allowing the organization to track large financial transfers that may impact an individual's estate tax responsibilities. It is not only essential for those making substantial gifts but also for donors who want to ensure compliance with tax laws. Certain aspects of the form include details about the value of gifts given, the identity of both the donor and the recipient, and the applicable exemptions and deductions. Filling out the IRS 709 accurately is key for anyone looking to avoid potential tax penalties in the future. Additionally, discussions about the generation-skipping transfer tax, which may come into play for gifts that skip a generation, highlight the form's importance in estate planning. As tax season approaches, understanding the ins and outs of the IRS 709 becomes an invaluable tool for taxpayers who wish to manage their finances responsibly.

Form 709

Department of the Treasury Internal Revenue Service

United States Gift (and

Go to www.irs.gov/Form709 for instructions and the latest information.

(For gifts made during calendar year 2019)

See instructions.

OMB No.

2019

Part

Attach check or money order here.

1 |

Donor’s first name and middle initial |

2 Donor’s last name |

3 Donor’s social security number |

|

|||

|

|

|

|

|

|

|

|

4 |

Address (number, street, and apartment number) |

|

5 |

Legal residence (domicile) |

|

|

|

|

|

|

|

|

|

||

6 |

City or town, state or province, country, and ZIP or foreign postal code |

7 |

Citizenship (see instructions) |

|

|

||

|

|

|

|

|

|

|

|

|

8 |

If the donor died during the year, check here |

and enter date of death |

|

, |

. |

Yes No |

|

9 |

If you extended the time to file this Form 709, check here |

|

|

|

|

|

10Enter the total number of donees listed on Schedule A. Count each person only once

11a |

Have you (the donor) previously filed a Form 709 (or |

|

b |

Has your address changed since you last filed Form 709 (or |

. . . . . . . . . . . . . . . . |

12Gifts by husband or wife to third parties. Do you consent to have the gifts (including

shown below. If the answer is “No,” skip lines

13 |

Name of consenting spouse |

|

|

|

14 SSN |

|

15 |

Were you married to one another during the entire calendar year? See instructions |

|||||

16 |

If line 15 is “No,” check whether |

married |

divorced or |

widowed/deceased, and give date. See instructions |

|

|

17 |

Will a gift tax return for this year be filed by your spouse? If “Yes,” mail both returns in the same envelope |

|||||

18Consent of Spouse. I consent to have the gifts (and

Consenting spouse’s signature |

Date |

19Have you applied a DSUE amount received from a predeceased spouse to a gift or gifts reported on this or a previous Form

709? If “Yes,” complete Schedule C . . . . . . . . . . . . . . . . . . . . . . . . . .

|

1 |

Enter the amount from Schedule A, Part 4, line 11 |

. . . |

|

1 |

|

|

|

|||||||

|

2 |

Enter the amount from Schedule B, line 3 |

. . . |

|

2 |

|

|

|

|||||||

|

3 |

Total taxable gifts. Add lines 1 and 2 |

. . . |

|

3 |

|

|

|

|||||||

|

4 |

Tax computed on amount on line 3 (see Table for Computing Gift Tax in instructions) . . . |

. . . |

|

4 |

|

|

|

|||||||

|

5 |

Tax computed on amount on line 2 (see Table for Computing Gift Tax in instructions) . . . |

. . . |

|

5 |

|

|

|

|||||||

Computation |

6 |

Balance. Subtract line 5 from line 4 |

. . . |

|

6 |

|

|

|

|||||||

7 |

Applicable credit amount. If donor has DSUE amount from predeceased spouse(s) or Restored Exclusion |

|

|

|

|

|

|||||||||

|

|

|

|

|

|

||||||||||

|

|

Amount, enter amount from Schedule C, line 5; otherwise, see instructions |

. . . |

|

7 |

|

|

|

|||||||

|

8 |

Enter the applicable credit against tax allowable for all prior periods (from Sch. B, line 1, col. C) |

. . . |

|

8 |

|

|

|

|||||||

|

9 |

Balance. Subtract line 8 from line 7. Do not enter less than zero |

. . . |

|

9 |

|

|

|

|||||||

|

10 |

Enter 20% (0.20) of the amount allowed as a specific exemption for gifts made after September 8, 1976, |

|

|

|

|

|

||||||||

|

and before January 1, 1977. See instructions |

. . . |

|

10 |

|

|

|

||||||||

11 |

Balance. Subtract line 10 from line 9. Do not enter less than zero |

. . . |

|

11 |

|

|

|

||||||||

|

|

|

|

|

|||||||||||

|

12 |

Applicable credit. Enter the smaller of line 6 or line 11 |

. . . |

|

12 |

|

|

|

|||||||

Part |

13 |

Credit for foreign gift taxes (see instructions) |

. . . |

|

13 |

|

|

|

|||||||

14 |

Total credits. Add lines 12 and 13 |

. . . |

|

14 |

|

|

|

||||||||

|

15 |

Balance. Subtract line 14 from line 6. Do not enter less than zero |

. . . |

|

15 |

|

|

|

|||||||

|

16 |

. . . |

|

16 |

|

|

|

||||||||

|

17 |

Total tax. Add lines 15 and 16 |

. . . |

|

17 |

|

|

|

|||||||

|

18 |

Gift and |

. . . |

|

18 |

|

|

|

|||||||

|

19 |

If line 18 is less than line 17, enter balance due. See instructions |

. . . |

|

19 |

|

|

|

|||||||

|

20 |

If line 18 is greater than line 17, enter amount to be refunded |

. . . |

|

20 |

|

|

|

|||||||

|

|

|

Under penalties of perjury, I declare that I have examined this return, including any accompanying schedules and statements, and to the best of my |

||||||||||||

|

|

|

knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than donor) is based on all information of which preparer has |

||||||||||||

Sign |

|

any knowledge. |

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

May the IRS discuss this return |

|||||||

Here |

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

with the preparer shown below? |

|||||||

|

|

|

F |

|

|

|

|

|

|

See instructions. Yes |

No |

||||

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

Signature of donor |

|

Date |

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Paid |

|

Print/Type preparer’s name |

Preparer’s signature |

|

Date |

|

Check |

|

if |

PTIN |

|

||||

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|||||||

Preparer |

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Firm’s name |

|

|

|

|

|

Firm’s EIN |

|

|

|||||||

Use Only |

|

|

|

|

|

|

|

||||||||

Firm’s address |

|

|

|

|

|

Phone no. |

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For Disclosure, Privacy Act, and Paperwork Reduction Act Notice, see the instructions for this form. |

Cat. No. 16783M |

Form 709 (2019) |

Form 709 (2019) |

|

Page 2 |

|

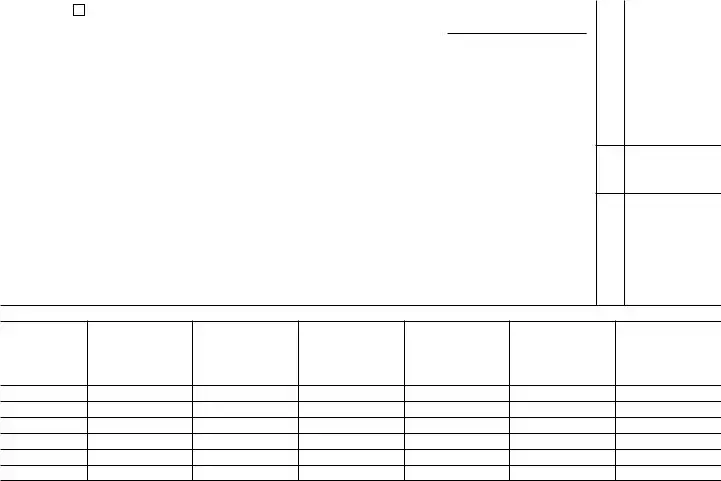

SCHEDULE A |

Computation of Taxable Gifts (Including transfers in trust) (see instructions) |

|

|

A |

Does the value of any item listed on Schedule A reflect any valuation discount? If “Yes,” attach explanation . . . . . . Yes |

No |

|

B |

Check here if you elect under section 529(c)(2)(B) to treat any transfers made this year to a qualified tuition program as made ratably over a |

||

|

|

||

Part

A |

B |

C |

D |

E |

F |

G |

H |

Item |

• Donee’s name and address |

|

Donor’s adjusted |

Date |

Value at |

For split gifts, |

Net transfer |

number |

• Relationship to donor (if any) |

|

basis of gift |

of gift |

date of gift |

enter 1/2 of |

(subtract col. G |

|

• Description of gift |

|

|

|

|

column F |

from col. F) |

|

• If the gift was of securities, give CUSIP no. |

|

|

|

|

|

|

|

• If closely held entity, give EIN |

|

|

|

|

|

|

1

Gifts made by

Total of Part 1. Add amounts from Part 1, column H . . . . . . . . . . . . . . . . . . . . . .

Part

A |

B |

C |

D |

E |

F |

G |

H |

Item |

• Donee’s name and address |

2632(b) |

Donor’s adjusted |

Date |

Value at |

For split gifts, |

Net transfer |

number |

• Relationship to donor (if any) |

election |

basis of gift |

of gift |

date of gift |

enter 1/2 of |

(subtract col. G |

|

• Description of gift |

out |

|

|

|

column F |

from col. F) |

|

• If the gift was of securities, give CUSIP no. |

|

|

|

|

|

|

|

• If closely held entity, give EIN |

|

|

|

|

|

|

1

Gifts made by

Total of Part 2. Add amounts from Part 2, column H . . . . . . . . . . . . . . . . . . . . . .

Part

A |

B |

C |

D |

E |

F |

G |

H |

Item |

• Donee’s name and address |

2632(c) |

Donor’s adjusted |

Date |

Value at |

For split gifts, |

Net transfer |

number |

• Relationship to donor (if any) |

election |

basis of gift |

of gift |

date of gift |

enter 1/2 of |

(subtract col. G |

|

• Description of gift |

|

|

|

|

column F |

from col. F) |

|

• If the gift was of securities, give CUSIP no. |

|

|

|

|

|

|

|

• If closely held entity, give EIN |

|

|

|

|

|

|

1

Gifts made by

Total of Part 3. Add amounts from Part 3, column H . . . . . . . . . . . . . . . . . . . . . .

(If more space is needed, attach additional statements.) |

Form 709 (2019) |

Form 709 (2019) |

Page 3 |

|

Part |

|

|

1 |

Total value of gifts of donor. Add totals from column H of Parts 1, 2, and 3 |

1 |

2 |

Total annual exclusions for gifts listed on line 1 (see instructions) |

2 |

3 |

Total included amount of gifts. Subtract line 2 from line 1 |

3 |

Deductions (see instructions) |

|

|

4Gifts of interests to spouse for which a marital deduction will be claimed, based on item

|

numbers |

of Schedule A |

|

4 |

|

|

5 |

Exclusions attributable to gifts on line 4 . . |

. . . . . . . . . . . . |

|

5 |

|

|

6 |

Marital deduction. Subtract line 5 from line 4 . |

. . . . . . . . . . . . |

|

6 |

|

|

7 |

Charitable deduction, based on item numbers |

less exclusions |

|

7 |

|

|

8 |

Total deductions. Add lines 6 and 7 . . . |

. . . . . . . . . . . . |

. . . . . . . . |

8 |

||

9 |

Subtract line 8 from line 3 |

. . . . . . . . . . . . |

. . . . . . . . |

9 |

||

10 |

10 |

|||||

11 |

Taxable gifts. Add lines 9 and 10. Enter here and on page 1, Part |

11 |

||||

Terminable Interest (QTIP) Marital Deduction. (See instructions for Schedule A, Part 4, line 4.)

If a trust (or other property) meets the requirements of qualified terminable interest property under section 2523(f), and: a. The trust (or other property) is listed on Schedule A; and

b. The value of the trust (or other property) is entered in whole or in part as a deduction on Schedule A, Part 4, line 4, then the donor shall be deemed to have made an election to have such trust (or other property) treated as qualified terminable interest property under section 2523(f).

If less than the entire value of the trust (or other property) that the donor has included in Parts 1 and 3 of Schedule A is entered as a deduction on line 4, the donor shall be considered to have made an election only as to a fraction of the trust (or other property). The numerator of this fraction is equal to the amount of the trust (or other property) deducted on Schedule A, Part 4, line 6. The denominator is equal to the total value of the trust (or other property) listed in Parts 1 and 3 of Schedule A.

If you make the QTIP election, the terminable interest property involved will be included in your spouse’s gross estate upon his or her death (section 2044). See instructions for line 4 of Schedule A. If your spouse disposes (by gift or otherwise) of all or part of the qualifying life income interest, he or she will be considered to have made a transfer of the entire property that is subject to the gift tax. See Transfer of Certain Life Estates Received From Spouse in the instructions.

12 Election Out of QTIP Treatment of Annuities

Check here if you elect under section 2523(f)(6) not to treat as qualified terminable interest property any joint and survivor annuities that are reported on Schedule A and would otherwise be treated as qualified terminable interest property under section 2523(f). See instructions. Enter the item numbers from Schedule A for the annuities for which you are making this election

Check here if you elect under section 2523(f)(6) not to treat as qualified terminable interest property any joint and survivor annuities that are reported on Schedule A and would otherwise be treated as qualified terminable interest property under section 2523(f). See instructions. Enter the item numbers from Schedule A for the annuities for which you are making this election

SCHEDULE B Gifts From Prior Periods

If you answered “Yes” on line 11a of page 1, Part 1, see the instructions for completing Schedule B. If you answered “No,” skip to the Tax Computation on page 1 (or Schedule C or D, if applicable). Complete Schedule A before beginning Schedule B. See instructions for recalculation of the column C amounts. Attach calculations.

A

Calendar year or calendar quarter (see instructions)

B

Internal Revenue office

where prior return was filed

C |

D |

Amount of applicable |

Amount of specific |

credit (unified credit) |

exemption for prior |

against gift tax |

periods ending before |

for periods after |

January 1, 1977 |

December 31, 1976 |

|

E

Amount of

taxable gifts

1 |

Totals for prior periods |

1

2 |

Amount, if any, by which total specific exemption, line 1, column D, is more than $30,000 |

. . . . . . . |

3Total amount of taxable gifts for prior periods. Add amount on line 1, column E, and amount, if any, on line 2. Enter here and on page 1, Part

2

3

(If more space is needed, attach additional statements.) |

Form 709 (2019) |

Form 709 (2019) |

Page 4 |

SCHEDULE C Deceased Spousal Unused Exclusion (DSUE) Amount and Restored Exclusion

Provide the following information to determine the DSUE amount and applicable credit received from prior spouses. Complete Schedule A before beginning Schedule C.

A |

B |

|

C |

D |

E |

F |

|

Name of deceased spouse |

Date of death |

Portability election |

If “Yes,” DSUE |

DSUE amount applied |

Date of gift(s) |

||

(dates of death after December 31, 2010, only) |

|

|

made? |

amount received |

by donor to lifetime |

(enter as mm/dd/yy |

|

|

|

|

|

|

from spouse |

gifts (list current |

for Part 1 and as |

|

|

Yes |

|

No |

|

and prior gifts) |

yyyy for Part 2) |

|

|

|

|

|

|

||

Part

Part

TOTAL (for all DSUE amounts applied from column E for Part 1 and Part 2) . . . . . . . . .

1 |

Donor’s basic exclusion amount (see instructions) |

2 |

Total from column E, Parts 1 and 2 |

3 |

Restored Exclusion Amount (see instructions) |

4 |

Add lines 1, 2, and 3 |

5Applicable credit on amount in line 4 (see Table for Computing Gift Tax in the instructions). Enter here and on line 7,

Part

1

2

3

4

5

SCHEDULE D Computation of

Note: Inter vivos direct skips that are completely excluded by the GST exemption must still be fully reported (including value and exemptions claimed) on Schedule D.

Part

A |

B |

C |

D |

E |

Item number |

Description |

Value |

Nontaxable |

Net transfer |

(from Schedule A, |

(only for ETIP transfers) |

(from Schedule A, |

portion of transfer |

(subtract col. D |

Part 2, col. A, then |

|

Part 2, col. H, |

|

from col. C) |

ETIP transfers, |

|

or close of ETIP |

|

|

if any) |

|

described in col. B) |

|

|

1

Gifts made by spouse (for gift splitting only)

(If more space is needed, attach additional statements.) |

Form 709 (2019) |

Form 709 (2019) |

|

|

Page 5 |

|

Part |

|

|||

Check here |

if you are making a section 2652(a)(3) (special QTIP) election. See instructions. |

|

||

Enter the item numbers from Schedule A of the gifts for which you are making this election |

|

|||

1 |

Maximum allowable exemption (see instructions) |

. . . . . . . . . . . . . . . . . . . |

1 |

|

2 |

Total exemption used for periods before filing this return |

2 |

||

3 |

Exemption available for this return. Subtract line 2 from line 1 |

3 |

||

4 |

Exemption claimed on this return from Part 3, column C, total below |

4 |

||

5Automatic allocation of exemption to transfers reported on Schedule A, Part 3. To opt out of the automatic

allocation rules, you must attach an “Election Out” statement. See instructions |

5 |

6Exemption allocated to transfers not shown on line 4 or line 5 above. You must attach a “Notice of Allocation.”

See instructions |

6 |

7 Add lines 4, 5, and 6 . . . . . . . . . . . . . . . . . . . . . . . . . . . .

7

8 |

Exemption available for future transfers. Subtract line 7 from line 3 |

8

Part

A |

B |

C |

D |

E |

F |

G |

Item number |

Net transfer |

GST exemption |

Divide col. C |

Inclusion ratio |

Applicable rate |

|

(from Schedule D, |

(from Schedule D, |

allocated |

by col. B |

(Subtract col. D |

(multiply col. E |

transfer tax |

Part 1) |

Part 1, col. E) |

|

|

from 1.000) |

by 40% (0.40)) |

(multiply col. B |

|

|

|

|

|

|

by col. F) |

1

Gifts made by spouse (for gift splitting only)

Total exemption claimed. Enter here and on Part 2, line 4, above. May not exceed Part 2, line 3, above . . .

Total

(If more space is needed, attach additional statements.) |

Form 709 (2019) |

| Fact Name | Details |

|---|---|

| Purpose | The IRS Form 709 is used to report gifts and to calculate any gift tax owed by the donor. |

| Filing Requirement | A taxpayer must file Form 709 if they give gifts above the annual exclusion limit, which is $17,000 for 2023. |

| Unified Credit | The form allows taxpayers to utilize the unified credit against the gift tax, which reduces the amount of tax owed on taxable gifts. |

| State-Specific Forms | Some states have their own gift tax forms that may be required in addition to Form 709, such as California's tax laws, which currently do not impose a state-level gift tax. |

| Deadline | Form 709 is due on April 15 of the year following the gift. However, an extension can be requested. |

After gathering the necessary information and documents, you are ready to begin filling out IRS Form 709, which is used to report gifts and certain transfers. Completing this form accurately is essential for compliance with federal tax regulations. Follow these steps to ensure everything is filled out correctly.

Once completed, you will need to file the form with the IRS by the due date, usually coinciding with tax day, and ensure you keep a copy for your records.

IRS Form 709 is used to report gifts made during the year that exceed the annual exclusion amount. The form is required for individuals who give gifts of money or property to others, including family members, friends, or charitable organizations. For 2023, the annual exclusion is $17,000 per recipient. If your gifts to an individual exceed this amount, you'll need to file Form 709 to report the gift to the IRS.

Filing Form 709 is necessary for individuals who have made taxable gifts or those who wish to allocate their lifetime gift tax exemption against gifts. This includes:

If you are required to file Form 709 and do not, you may face penalties. The IRS can impose a penalty of 5% of the tax due for each month the return is late, up to a maximum of 25%. Even if no tax is owed, failing to file can complicate your tax situation and may lead to further scrutiny from the IRS. It's important to meet filing deadlines to avoid unnecessary penalties.

IRS Form 709 is due on April 15 of the year following the calendar year in which the gifts were made. If April 15 falls on a weekend or holiday, the due date is the next business day. If you need additional time to file, you can request an extension using Form 4868. However, this extension only applies to filing your return, not to any taxes owed, which must still be paid by the original due date.

When filling out the IRS 709 form, some people make common mistakes that can lead to complications. One frequent error involves miscalculating gifts. The IRS requires a precise valuation of gifts made to others. If a person undervalues their gifts, they might unintentionally avoid reporting taxable transfers. However, the IRS could flag this and demand clarification. It’s essential to assess the fair market value honestly.

Another significant mistake is neglecting to report all applicable gifts. Many individuals assume that only large gifts need to be reported. However, the IRS requires reporting for any gifts exceeding the annual exclusion limit. Even small gifts can accumulate and trigger reporting requirements if the total exceeds the exclusion threshold. Being thorough is crucial to ensuring compliance.

In addition, many filers make the error of missing signatures and dates. This may seem trivial, but an unsigned form or a missing date can result in delays or rejections. It's vital to review the form carefully before submission. Making sure that everything is properly signed and dated can save a lot of time and trouble.

Finally, failing to keep accurate records is a mistake that can have long-lasting implications. Individuals should maintain documentation regarding each gift, including appraisals and records of any related transactions. These documents could prove critical if the IRS has questions in the future. Proper record-keeping safeguards against potential audits and discrepancies.

The IRS Form 709 is essential for reporting gift taxes and outlining certain gifts made by an individual. When preparing this form, you may need to gather several other documents for a complete picture of your financial obligations and benefits. Below is a list of common forms and documents that could accompany the IRS 709 Form.

Gathering these documents can help streamline the process and ensure compliance with tax laws. Making sure every detail is in order helps prevent issues down the line, giving peace of mind as you navigate your financial responsibilities.

The IRS 709 form, also known as the United States Gift (and Generation-Skipping Transfer) Tax Return, is used to report gifts and certain transfers to others. Here are eight documents that are similar to the IRS 709 form, detailing how they relate:

When it comes to filing the IRS Form 709, which is essential for reporting gifts, it’s important to get it right. Here’s a helpful list of what you should and shouldn't do to ensure your form is completed correctly.

When dealing with the IRS Form 709, there are key considerations that individuals should keep in mind.

By understanding these key points, taxpayers will be better equipped to navigate the requirements surrounding Form 709.