The IRS 720 form plays a critical role in the tax landscape, particularly for those engaged in specific activities subject to federal excise taxes. Understanding this form is essential for businesses and professionals alike, as it is primarily used to report and pay these taxes, which can encompass a range of items such as fuel, air transportation, and certain environmental taxes. Each quarter, taxpayers must carefully compile the necessary data to ensure accurate reporting and timely submission. Completing the IRS 720 involves more than just filling out a few sections; it requires a solid grasp of the applicable excise tax rates and categories, as well as the nuances of calculating liabilities appropriately. The form is structured to facilitate both quarterly payments and annual reconciliations, allowing taxpayers to manage their obligations effectively throughout the year. Thus, navigating the intricacies of the IRS 720 form can seem daunting, but with the right approach and understanding, it becomes a manageable task that ensures compliance with federal regulations.

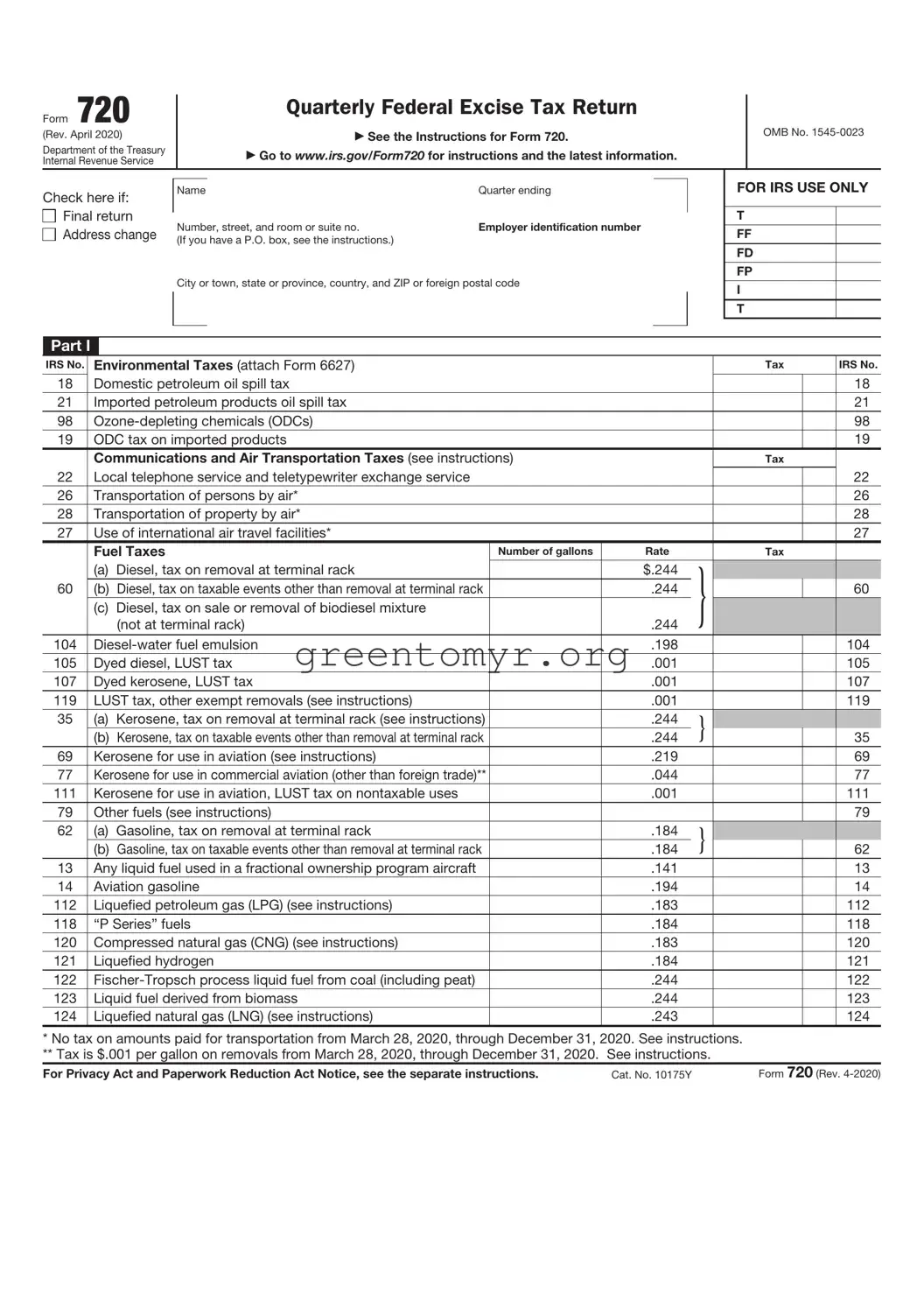

Form 720

(Rev. April 2020)

Department of the Treasury

Internal Revenue Service

Quarterly Federal Excise Tax Return

See the Instructions for Form 720.

Go to www.irs.gov/Form720 for instructions and the latest information.

OMB No.

Check here if:

Final return

Final return

Address change

Name |

Quarter ending |

Number, street, and room or suite no. |

Employer identification number |

(If you have a P.O. box, see the instructions.) |

|

City or town, state or province, country, and ZIP or foreign postal code

FOR IRS USE ONLY

T

FF

FD

FP

I

T

Part I

IRS No. |

Environmental Taxes (attach Form 6627) |

|

|

|

Tax |

|

IRS No. |

|

18 |

|

Domestic petroleum oil spill tax |

|

|

|

|

|

18 |

21 |

|

Imported petroleum products oil spill tax |

|

|

|

|

|

21 |

98 |

|

|

|

|

|

|

98 |

|

19 |

|

ODC tax on imported products |

|

|

|

|

|

19 |

|

|

Communications and Air Transportation Taxes (see instructions) |

|

|

Tax |

|

|

|

22 |

|

Local telephone service and teletypewriter exchange service |

|

|

|

|

|

22 |

26 |

|

Transportation of persons by air* |

|

|

|

|

|

26 |

28 |

|

Transportation of property by air* |

|

|

|

|

|

28 |

27 |

|

Use of international air travel facilities* |

|

|

|

|

|

27 |

|

|

Fuel Taxes |

Number of gallons |

Rate |

|

Tax |

|

|

|

|

(a) Diesel, tax on removal at terminal rack |

|

$.244 |

} |

|

|

|

60 |

|

(b) Diesel, tax on taxable events other than removal at terminal rack |

|

.244 |

|

|

60 |

|

|

|

(c) Diesel, tax on sale or removal of biodiesel mixture |

|

|

|

|

|

|

|

|

(not at terminal rack) |

|

.244 |

|

|

|

|

104 |

|

|

.198 |

|

|

|

104 |

|

105 |

|

Dyed diesel, LUST tax |

|

.001 |

|

|

|

105 |

107 |

|

Dyed kerosene, LUST tax |

|

.001 |

|

|

|

107 |

119 |

|

LUST tax, other exempt removals (see instructions) |

|

.001 |

|

|

|

119 |

35 |

|

(a) Kerosene, tax on removal at terminal rack (see instructions) |

|

.244 |

} |

|

|

|

|

|

(b) Kerosene, tax on taxable events other than removal at terminal rack |

|

.244 |

|

|

35 |

|

69 |

|

Kerosene for use in aviation (see instructions) |

|

.219 |

|

|

|

69 |

77 |

|

Kerosene for use in commercial aviation (other than foreign trade)** |

|

.044 |

|

|

|

77 |

111 |

|

Kerosene for use in aviation, LUST tax on nontaxable uses |

|

.001 |

|

|

|

111 |

79 |

|

Other fuels (see instructions) |

|

|

|

|

|

79 |

62 |

|

(a) Gasoline, tax on removal at terminal rack |

|

.184 |

} |

|

|

|

|

|

(b) Gasoline, tax on taxable events other than removal at terminal rack |

|

.184 |

|

|

62 |

|

13 |

|

Any liquid fuel used in a fractional ownership program aircraft |

|

.141 |

|

|

|

13 |

14 |

|

Aviation gasoline |

|

.194 |

|

|

|

14 |

112 |

|

Liquefied petroleum gas (LPG) (see instructions) |

|

.183 |

|

|

|

112 |

118 |

|

“P Series” fuels |

|

.184 |

|

|

|

118 |

120 |

|

Compressed natural gas (CNG) (see instructions) |

|

.183 |

|

|

|

120 |

121 |

|

Liquefied hydrogen |

|

.184 |

|

|

|

121 |

122 |

|

|

.244 |

|

|

|

122 |

|

123 |

|

Liquid fuel derived from biomass |

|

.244 |

|

|

|

123 |

124 |

|

Liquefied natural gas (LNG) (see instructions) |

|

.243 |

|

|

|

124 |

* No tax on amounts paid for transportation from March 28, 2020, through December 31, 2020. See instructions. ** Tax is $.001 per gallon on removals from March 28, 2020, through December 31, 2020. See instructions.

For Privacy Act and Paperwork Reduction Act Notice, see the separate instructions. |

Cat. No. 10175Y |

Form 720 (Rev. |

Form 720 (Rev. |

|

|

|

|

|

|

|

|

|

|

|

|

|

Page 2 |

||

IRS No. |

|

|

|

|

|

|

|

|

|

Rate |

|

|

Tax |

IRS No. |

||

|

Retail |

|

|

|

|

|

|

|

||||||||

33 |

12% of sales price |

|

|

|

33 |

|||||||||||

|

Ship Passenger Tax |

|

|

|

Number of persons |

|

Rate |

|

|

Tax |

|

|||||

29 |

Transportation by water |

|

|

|

|

|

|

$3 per person |

|

|

|

29 |

||||

|

Other Excise Tax |

|

|

|

Amount of obligations |

|

Rate |

|

|

Tax |

|

|||||

31 |

Obligations not in registered form |

|

|

|

|

|

|

$.01 |

|

|

|

|

|

31 |

||

|

Foreign Insurance |

Premiums paid |

|

Rate |

|

|

Tax |

IRS No. |

||||||||

|

|

Casualty insurance and indemnity bonds |

|

|

|

|

|

|

$.04 |

|

} |

|

|

|

|

|

30 |

|

Life insurance, sickness and accident policies, and annuity |

|

|

|

|

|

|

|

|

|

|

||||

|

|

contracts |

|

|

|

|

|

|

.01 |

|

|

|

|

30 |

||

|

|

Reinsurance |

|

|

|

|

|

|

.01 |

|

|

|

|

|

||

|

Manufacturers Taxes |

Number of tons |

Sales price |

|

|

|

|

|

|

|

|

|||||

36 |

|

|

|

|

|

|

$1.10 per ton |

|

|

|

|

36 |

||||

37 |

|

|

|

|

|

|

4.4% of sales price |

|

|

|

37 |

|||||

|

|

|

|

|

|

|

|

|

|

|

||||||

38 |

|

|

|

|

|

|

|

$.55 per ton |

|

|

|

|

38 |

|||

39 |

|

|

|

|

|

|

4.4% of sales price |

|

|

|

39 |

|||||

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

Number of tires |

|

Tax |

IRS No. |

||||

108 |

Taxable tires other than bias ply or super single tires |

|

|

|

|

|

|

|

|

|

|

|

|

108 |

||

109 |

Taxable bias ply or super single tires (other than super single tires designed for steering) |

|

|

|

|

|

|

|

109 |

|||||||

113 |

Taxable tires, super single tires designed for steering |

|

|

|

|

|

|

|

|

|

|

|

|

113 |

||

40 |

Gas guzzler tax. Attach Form 6197. Check if |

. . . . . |

|

|

|

|

|

40 |

||||||||

97 |

Vaccines (see instructions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

97 |

|

|

|

|

|

|

|

Sales price |

|

|

|

|

|

|

|

|

||

|

Reserved for future use |

|

|

|

|

|

|

2.3% of sales price |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

||||||

1 |

Total. Add all amounts in Part I. Complete Schedule A unless |

|

|

|

|

$ |

|

|

|

|||||||

Part II |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(a) Avg. number |

(b) Rate for |

|

(c) Fee (see |

|

|

|

|

||||||||

IRS No. |

instructions) |

|

of lives covered |

avg. |

|

|

|

|

|

|||||||

|

(see inst.) |

covered life |

|

instructions) |

|

Tax |

IRS No. |

|||||||||

|

Specified health insurance policies |

|

|

|

|

|

|

|

|

|

|

} |

|

|

|

|

|

(a) With a policy year ending before October 1, 2019 |

|

|

|

$2.45 |

|

|

|

|

|

|

|

||||

|

(b) With a policy year ending on or after October 1, |

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

2019, and before October 1, 2020 |

|

|

|

|

$2.54 |

|

|

|

|

|

|

|

|||

133 |

Applicable |

|

|

|

|

|

|

|

|

|

|

|

|

133 |

||

|

(c) With a plan year ending before October 1, 2019 |

|

|

|

$2.45 |

|

|

|

|

|

|

|

||||

|

(d) With a plan year ending on or after October 1, |

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

2019, and before October 1, 2020 |

|

|

|

|

$2.54 |

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

Rate |

|

|

Tax |

|

||

41 |

Sport fishing equipment (other than fishing rods and fishing poles) |

|

|

10% of sales price |

|

|

|

41 |

||||||||

110 |

Fishing rods and fishing poles (limits apply, see instructions) |

|

|

|

10% of sales price |

|

|

|

110 |

|||||||

42 |

Electric outboard motors |

|

|

|

|

|

|

3% of sales price |

|

|

|

42 |

||||

114 |

Fishing tackle boxes |

|

|

|

|

|

|

3% of sales price |

|

|

|

114 |

||||

44 |

Bows, quivers, broadheads, and points |

|

|

|

|

|

|

11% of sales price |

|

|

|

44 |

||||

106 |

Arrow shafts |

|

|

|

|

|

|

$.52 per shaft |

|

|

|

106 |

||||

140 |

Indoor tanning services |

|

|

|

|

|

|

10% of amount paid |

|

|

|

140 |

||||

|

|

|

|

|

|

Number of gallons |

|

Rate |

|

|

Tax |

|

||||

64 |

Inland waterways fuel use tax |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

$.29 |

|

|

|

|

|

64 |

||||

125 |

LUST tax on inland waterways fuel use (see instructions) |

|

|

|

.001 |

|

|

|

|

|

125 |

|||||

51 |

Section 40 fuels (see instructions) |

|

|

|

|

|

|

|

|

|

|

|

|

|

51 |

|

117 |

Biodiesel sold as but not used as fuel |

|

|

|

|

|

|

|

|

|

|

|

|

|

117 |

|

20 |

Floor Stocks |

|

|

|

|

|

|

|

20 |

|||||||

2 |

Total. Add all amounts in Part II |

|

|

|

|

|

|

|

|

|

|

$ |

|

|

|

|

Form 720 (Rev.

Form 720 (Rev. |

Page 3 |

|

Part III |

|

|

3 |

Total tax. Add Part I, line 1, and Part II, line 2 |

|

|||||||

4 |

Claims (see instructions; complete Schedule C) |

. . . . . . . |

|

4 |

|

|

|||

5 |

Deposits made for the quarter . . . . |

|

5 |

|

|

|

|

|

|

|

Check here if you used the safe harbor rule to make your deposits. |

|

|

|

|

||||

6 |

Overpayment from previous quarters . . |

6 |

|

|

|

|

|

|

|

7Enter the amount from Form

|

on line 6, if any |

|

7 |

|

|

|

|

8 |

Add lines 5 and 6 |

. . . . . . . . . |

8 |

|

|

||

9 |

Add lines 4 and 8 |

|

|||||

10Balance Due. If line 3 is greater than line 9, enter the difference. Pay the full amount with the return (see instructions)

11Overpayment. If line 9 is greater than line 3, enter the difference. Check if you want the

overpayment: |

Applied to your next return, or |

Refunded to you. |

3

9

10

11

Third Party Designee

Sign

Here

Paid

Preparer

Use Only

Do you want to allow another person to discuss this return with the IRS (see instructions)? |

Yes. Complete the following. |

No |

|||||

Designee name |

Phone no. |

Personal identification number (PIN) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

F |

|

|

|

|

F |

|

|

|

|

|

Signature |

|

Date |

|

Title |

|

|

||||

|

|

|

|

|

|

|||||

|

Type or print name below signature. |

|

|

|

Telephone number |

|

|

|||

Print/Type preparer’s name |

Preparer’s signature |

Date |

|

|

Check |

if |

PTIN |

|||

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

Firm’s name |

|

|

|

|

|

Firm’s EIN |

|

|

||

Firm’s address |

|

|

|

|

|

Phone no. |

|

|

||

Form 720 (Rev.

Form 720 (Rev. |

Page 4 |

Schedule A Excise Tax Liability (see instructions)

Note: You must complete Schedule A if you have a liability for any tax in Part I of Form 720. Don’t complete Schedule A for Part II taxes or for a

1Regular method taxes

(a) Record of Net |

|

|

Period |

|

|||

Tax Liability |

|

|

|

|

|||

First month |

A |

|

|

B |

|

|

|

Second month |

C |

|

|

D |

|

|

|

Third month |

E |

|

|

F |

|

|

|

Special rule for September |

* |

. . . . . . . . . |

|

G |

|

|

|

(b)Net liability for regular method taxes. Add the amounts for each semimonthly period.

2Alternative method taxes (IRS Nos. 22, 26, 28, and 27)

(a) Record of Taxes |

|

|

Period |

|

|||

Considered as |

|

|

|

|

|||

Collected |

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

First month |

M |

|

|

N |

|

|

|

Second month |

O |

|

|

P |

|

|

|

Third month |

Q |

|

|

R |

|

|

|

Special rule for September |

* |

. . . . . . . . . |

|

S |

|

|

|

(b)Alternative method taxes. Add the amounts for each semimonthly period.

* Complete only as instructed (see instructions).

Schedule T

Fuel |

Number of gallons |

Diesel fuel, gallons received in a |

|

on Form 720, IRS No. 60(a) |

|

Diesel fuel, gallons delivered in a |

|

|

|

Kerosene, gallons received in a |

|

on Form 720, IRS No. 35(a), 69, 77, or 111 |

|

Kerosene, gallons delivered in a |

|

|

|

Gasoline, gallons received in a |

|

on Form 720, IRS No. 62(a) |

|

Gasoline, gallons delivered in a |

|

|

|

Aviation gasoline, gallons received in a |

|

on Form 720, IRS No. 14 |

|

Aviation gasoline, gallons delivered in a |

|

|

|

|

Form 720 (Rev. |

Form 720 (Rev. |

|

Page 5 |

Schedule C |

Claims |

Month your income tax year ends |

•Complete Schedule C for claims only if you are reporting liability in Part I or II of Form 720.

•See instructions for kerosene used in commercial aviation from March 28, 2020, through December 31, 2020.

•Attach a statement explaining each claim as required. Include your name and EIN on the statement (see instructions).

Caution: Claimant has the name and address of the person(s) who sold the fuel to the claimant, the dates of purchase, and if exported, the required proof of export. For claims on lines 1a and 2b (type of use 13 and 14), 3c, 4b, and 5, claimant hasn’t waived the right to make the claim.

1 |

Nontaxable Use of Gasoline |

Note: CRN is credit reference number. |

Period of claim |

|

|

|

||

|

|

|

Type of use |

Rate |

Gallons |

Amount of claim |

CRN |

|

a Gasoline (see Caution above line 1) |

|

$.183 |

|

$ |

|

362 |

||

|

|

|

|

|

|

|

|

|

b Exported (see Caution above line 1) |

|

.184 |

|

|

|

411 |

||

2 |

Nontaxable Use of Aviation Gasoline |

Period of claim |

|

|

|

|||

|

|

|

Type of use |

Rate |

Gallons |

Amount of claim |

CRN |

|

a Used in commercial aviation (other than foreign trade) |

|

$.15 |

|

$ |

|

354 |

||

|

|

|

|

|

|

|

|

|

b Other nontaxable use (see Caution above line 1) |

|

.193 |

|

|

|

324 |

||

|

|

|

|

|

|

|

|

|

c Exported (see Caution above line 1) |

|

.194 |

|

|

|

412 |

||

|

|

|

|

|

|

|

|

|

d LUST tax on aviation fuels used in foreign trade |

|

.001 |

|

|

|

433 |

||

3 |

Nontaxable Use of Undyed Diesel Fuel |

Period of claim |

|

|

|

|||

Claimant certifies that the diesel fuel did not contain visible evidence of dye.

Exception. If any of the diesel fuel included in this claim did contain visible evidence of dye, attach a detailed explanation and check here . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

|

|

Type of use |

Rate |

Gallons |

|

Amount of claim |

CRN |

|

a |

Nontaxable use |

|

$.243 |

|

$ |

|

|

360 |

b |

Use in trains |

|

.243 |

|

|

|

|

353 |

c Use in certain intercity and local buses (see Caution above line 1) |

|

.17 |

|

|

|

|

350 |

|

|

|

|

|

|

|

|

|

|

d Use on a farm for farming purposes |

|

.243 |

|

|

|

|

360 |

|

|

|

|

|

|

|

|

|

|

e Exported (see Caution above line 1) |

|

.244 |

|

|

|

|

413 |

|

4Nontaxable Use of Undyed Kerosene (Other Than Kerosene Used in Aviation) Period of claim

Claimant certifies that the kerosene did not contain visible evidence of dye.

Exception. If any of the kerosene included in this claim did contain visible evidence of dye, attach a detailed explanation and check here . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

|

Caution: Claims cannot be made on line 4 for kerosene sales from a blocked pump. |

Type of use |

Rate |

Gallons |

Amount of claim |

CRN |

|

a |

Nontaxable use |

|

$.243 |

|

$ |

|

346 |

b |

Use in certain intercity and local buses (see Caution above line 1) |

|

.17 |

|

|

|

347 |

c |

Use on a farm for farming purposes |

|

.243 |

|

|

|

346 |

d |

Exported (see Caution above line 1) |

|

.244 |

|

|

|

414 |

e |

Nontaxable use taxed at $.044 |

|

.043 |

|

|

|

377 |

f |

Nontaxable use taxed at $.219 |

|

.218 |

|

|

|

369 |

5 Kerosene Used in Aviation (see Caution above line 1) |

Period of claim |

|

|

|

|||

|

|

Type of use |

Rate |

Gallons |

Amount of claim |

CRN |

|

a |

Kerosene used in commercial aviation (other than foreign |

|

|

|

|

|

|

|

trade) taxed at $.244 |

|

$.200 |

|

$ |

|

417 |

b |

Kerosene used in commercial aviation (other than foreign |

|

|

|

|

|

|

|

trade) taxed at $.219 |

|

.175 |

|

|

|

355 |

c |

Nontaxable use (other than use by state or local |

|

|

|

|

|

|

|

government) taxed at $.244 |

|

.243 |

|

|

|

346 |

d |

Nontaxable use (other than use by state or local |

|

|

|

|

|

|

|

government) taxed at $.219 |

|

.218 |

|

|

|

369 |

e |

LUST tax on aviation fuels used in foreign trade |

|

.001 |

|

|

|

433 |

Form 720 (Rev.

Form 720 (Rev. |

Page 6 |

6Nontaxable Use of Alternative Fuel

Caution: There is a reduced credit rate for use in certain intercity and local buses (type of use 5) (see instructions).

|

|

Type of use |

Rate |

Gallons, or gasoline |

Amount of claim |

CRN |

|

|

|

or diesel gallon |

|||||

|

|

|

|

equivalents |

|

|

|

a |

Liquefied petroleum gas (LPG) (see instructions) |

|

$.183 |

|

$ |

|

419 |

b |

“P Series” fuels |

|

.183 |

|

|

|

420 |

c |

Compressed natural gas (CNG) (see instructions) |

|

.183 |

|

|

|

421 |

d |

Liquefied hydrogen |

|

.183 |

|

|

|

422 |

e |

|

.243 |

|

|

|

423 |

|

f |

Liquid fuel derived from biomass |

|

.243 |

|

|

|

424 |

g |

Liquefied natural gas (LNG) (see instructions) |

|

.243 |

|

|

|

425 |

h |

Liquefied gas derived from biomass |

|

.183 |

|

|

|

435 |

7 Sales by Registered Ultimate Vendors of Undyed Diesel Fuel |

|

Period of claim |

|

|

|

||

|

|

|

Registration number |

|

|

|

|

Claimant certifies that it sold the diesel fuel at a

|

|

Rate |

Gallons |

|

Amount of claim |

CRN |

|

a Use by a state or local government |

$.243 |

|

$ |

|

|

360 |

|

|

|

|

|

|

|

|

|

b Use in certain intercity and local buses |

.17 |

|

|

|

|

350 |

|

8 Sales by Registered Ultimate Vendors of Undyed Kerosene |

|

Period of claim |

|

|

|

|

|

|

(Other Than Kerosene For Use in Aviation) |

Registration number |

|

|

|

|

|

Claimant certifies that it sold the kerosene at a

explanation and check here . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

|

|

Rate |

Gallons |

Amount of claim |

CRN |

|

a Use by a state or local government |

$.243 |

|

$ |

|

346 |

|

|

|

|

|

|

|

|

b Sales from a blocked pump |

.243 |

|

|

|

||

|

|

|

|

|||

|

|

|

|

|

|

|

c Use in certain intercity and local buses |

.17 |

|

|

|

347 |

|

9 Sales by Registered Ultimate Vendors of Kerosene For Use in Aviation |

Registration number |

|

|

|

||

•See Caution above line 1.

•Claimant sold the kerosene for use in aviation at a

|

|

Type of use |

Rate |

Gallons |

Amount of claim |

CRN |

|

a |

Use in commercial aviation (other than foreign trade) taxed at $.219 |

|

$.175 |

|

$ |

|

355 |

b |

Use in commercial aviation (other than foreign trade) taxed at $.244 |

|

.200 |

|

|

|

417 |

c |

Nonexempt use in noncommercial aviation |

|

.025 |

|

|

|

418 |

d |

Other nontaxable uses taxed at $.244 |

|

.243 |

|

|

|

346 |

e |

Other nontaxable uses taxed at $.219 |

|

.218 |

|

|

|

369 |

f |

LUST tax on aviation fuels used in foreign trade |

|

.001 |

|

|

|

433 |

10 Sales by Registered Ultimate Vendors of Gasoline |

Registration number |

|

|

|

|||

Claimant sold the gasoline at a

|

|

Rate |

Gallons |

Amount of claim |

CRN |

|

a Use by a nonprofit educational organization |

$.183 |

|

$ |

|

362 |

|

|

|

|

|

|

|

|

b Use by a state or local government |

.183 |

|

|

|

||

|

|

|

|

|||

Form 720 (Rev.

Form 720 (Rev. |

|

|

|

|

|

|

|

Page 7 |

|

11 Sales by Registered Ultimate Vendors of Aviation Gasoline |

Registration number |

|

|

|

|

||||

|

Claimant sold the aviation gasoline at a |

||||||||

|

of tax to the buyer, or has obtained written consent of the buyer to take the claim; and obtained an unexpired certificate from the buyer |

||||||||

|

and has no reason to believe any information in the certificate is false. See the instructions for additional information to be submitted. |

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

Rate |

|

Gallons |

|

Amount of claim |

|

CRN |

|

a Use by a nonprofit educational organization |

$.193 |

|

|

$ |

|

|

|

324 |

|

|

|

|

|

|

|

|

|

|

|

b Use by a state or local government |

.193 |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|||

12 |

Biodiesel or Renewable Diesel Mixture Credit Period of claim |

|

|

Registration number |

|

||||

|

Biodiesel mixtures. Claimant produced a mixture by mixing biodiesel with diesel fuel. The biodiesel used to produce the |

||||||||

|

mixture met ASTM D6751 and met EPA’s registration requirements for fuels and fuel additives. The mixture was sold by the |

||||||||

|

claimant to any person for use as a fuel or was used as a fuel by the claimant. Claimant has attached the Certificate for |

|

|||||||

|

Biodiesel and, if applicable, the Statement of Biodiesel Reseller. Renewable diesel mixtures. Claimant produced a mixture by |

||||||||

|

mixing renewable diesel with liquid fuel (other than renewable diesel). The renewable diesel used to produce the renewable |

||||||||

|

diesel mixture was derived from biomass, met EPA’s registration requirements for fuels and fuel additives, and met ASTM |

||||||||

|

D975, D396, or other equivalent standard approved by the IRS. The mixture was sold by the claimant to any person for use as |

||||||||

|

a fuel or was used as a fuel by the claimant. Claimant has attached the Certificate for Biodiesel and, if applicable, Statement of |

||||||||

|

Biodiesel Reseller, both of which have been edited as discussed in the instructions for line 12. See the instructions for line 12 |

||||||||

|

for information about renewable diesel used in aviation. |

|

|

|

|

|

|

|

|

|

|

Rate |

Gal. of biodiesel or |

|

Amount of claim |

|

CRN |

||

|

|

|

renewable diesel |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

a Biodiesel (other than |

$1.00 |

|

|

$ |

|

|

|

388 |

|

b |

1.00 |

|

|

|

|

|

|

390 |

|

c |

Renewable diesel mixtures |

1.00 |

|

|

|

|

|

|

307 |

13 Alternative Fuel Credit and Alternative Fuel Mixture Credit |

|

Registration number |

|

||||||

For the alternative fuel mixture credit, claimant produced a mixture by mixing taxable fuel with alternative fuel. Claimant certifies that it (a) produced the alternative fuel, or (b) has in its possession the name, address, and EIN of the person(s) that sold the alternative fuel to the claimant; the date of purchase; and an invoice or other documentation identifying the amount of the alternative fuel. The claimant also certifies that it made no other claim for the amount of the alternative fuel, or has repaid the amount to the government. The alternative fuel mixture was sold by the claimant to any person for use as a fuel or was used as a fuel by the claimant.

|

|

|

Gallons, or |

|

|

|

|

|

|

Rate |

gasoline or diesel |

Amount of claim |

CRN |

||

|

|

|

gallon equivalents |

|

|

|

|

|

|

|

(see instructions) |

|

|

|

|

a |

Liquefied petroleum gas (LPG)* |

$.50 |

|

|

$ |

|

426 |

b |

“P Series” fuels |

.50 |

|

|

|

|

427 |

c |

Compressed natural gas (CNG)* |

.50 |

|

|

|

|

428 |

d |

Liquefied hydrogen |

.50 |

|

|

|

|

429 |

e |

.50 |

|

|

|

|

430 |

|

f |

Liquid fuel derived from biomass |

.50 |

|

|

|

|

431 |

g |

Liquefied natural gas (LNG)* |

.50 |

|

|

|

|

432 |

h |

Liquefied gas derived from biomass* |

.50 |

|

|

|

|

436 |

i |

Compressed gas derived from biomass* |

.50 |

|

|

|

|

437 |

|

* You can’t claim the alternative fuel mixture credit for this fuel. |

|

|

|

|

|

|

|

|

|

|

|

|||

14 |

Other claims. See the instructions. For lines 14b and 14c, see the Caution above line 1 on page 5. |

Amount of claim |

CRN |

||||

a |

Section 4051(d) tire credit (tax on vehicle reported on IRS No. 33) |

|

|

|

$ |

|

366 |

b |

Exported dyed diesel fuel and exported gasoline blendstocks taxed at $.001 |

|

|

|

|

415 |

|

c |

Exported dyed kerosene |

|

|

|

|

|

416 |

d |

|

|

|

|

|

|

|

e |

Registered credit card issuers |

|

|

|

|

|

|

|

|

|

Number of tires |

Amount of claim |

CRN |

||

f |

Taxable tires other than bias ply or super single tires |

|

|

|

$ |

|

396 |

g |

Taxable tires, bias ply or super single tires (other than super single tires designed for steering) |

|

|

|

|

304 |

|

h |

Taxable tires, super single tires designed for steering |

|

|

|

|

|

305 |

i |

|

|

|

|

|

|

|

j |

|

|

|

|

|

|

|

k |

|

|

|

|

|

|

|

15 |

Total claims. Add amounts on lines 1 through 14. Enter the result here and on Form 720, Part III, line 4. |

15 |

|

|

|

||

Form 720 (Rev.

Form

Purpose of Form

Complete Form

If you have your return prepared by a third party and a payment is required, provide this payment voucher to the return preparer.

Don’t file Form

Specific Instructions

Box 1. If you don’t have an EIN, you may apply for one online by visiting www.irs.gov/EIN. You may also apply for an EIN by faxing or mailing Form

Box 2. Enter the amount paid from line 10 of Form 720.

Box 3. Darken the circle identifying the quarter for which the payment is made. Darken only one circle.

Box 4. Enter your name and address as shown on Form 720.

•Enclose your check or money order made payable to “United States Treasury.” Be sure to enter your

EIN (SSN for

•Detach the completed voucher and send it with your payment and Form 720. See Where To File in the Instructions for Form 720.

Form

Detach here and mail with your payment and Form 720.

Form

Department of the Treasury

Internal Revenue Service

1Enter your employer identification

number (EIN). See instructions.

|

Payment Voucher |

OMB No. |

|

|

|

|

|

|

Don’t staple or attach this voucher to your payment. |

2020 |

|

|

||

|

|

|

2 |

Dollars |

Cents |

Enter the amount of your payment.

Make your check or money order payable to “United States Treasury.”

3Tax Period

1st |

3rd |

Quarter |

Quarter |

2nd |

4th |

Quarter |

Quarter |

4Enter your business name (individual name if sole proprietor).

Enter your address.

City or town, state or province, country, and ZIP or foreign postal code

| Fact Name | Description |

|---|---|

| Form Purpose | The IRS Form 720 is used to report and pay certain federal excise taxes. |

| Filing Frequency | This form is typically filed quarterly, but some taxes require more frequent filings. |

| Eligibility | Businesses that report liabilities for excise taxes must file this form. |

| Types of Taxes | Excise taxes on gasoline, air transportation, and environmental taxes are reported using this form. |

| Due Dates | Form 720 is due on the last day of the month following the end of each quarter. |

| Extensions | Taxpayers can apply for an extension to file, but any owed tax must still be paid on time. |

| Electronic Filing | Form 720 can be filed electronically through the IRS e-file program. |

| State-Specific Forms | Some states have specific excise tax forms governed by state laws, which may differ from the IRS process. |

| Record Keeping | It’s crucial to maintain records related to excise taxes, as the IRS may request documentation. |

| Penalties | Failure to file Form 720 on time can result in penalties and interest on unpaid taxes. |

After obtaining the IRS 720 form, it's essential to ensure that you fill it out accurately to meet your tax obligations. Follow these steps carefully to complete the form and avoid any mistakes that might delay processing your return.

IRS Form 720, also known as the Quarterly Federal Excise Tax Return, is used by businesses to report and pay specific excise taxes. These taxes are often related to activities like the sale of certain goods, transportation services, or environmental taxes. Filing this form ensures compliance with federal tax requirements.

Businesses that are liable for excise taxes need to file Form 720. This includes sellers of specific products, businesses offering taxable services, and those involved in activities like wagering or using fuel for non-taxable purposes. If your business falls into these categories, you’ll likely need to file.

The due date for Form 720 is quarterly. It must be filed on or before the last day of the month following the end of each quarter. For example:

You can file Form 720 electronically, which is often the easiest method. Alternatively, you can mail a paper copy to the IRS. Ensure that you provide accurate information and attach any necessary schedules. Most businesses find that e-filing simplifies the process and allows for faster processing.

If you fail to file Form 720 on time, you may face penalties and interest charges on unpaid taxes. The penalty for late filing can be significant, so it’s crucial to get your form submitted on schedule. Additionally, failure to pay any taxes owed by the deadline can result in further complications.

Yes, you can amend Form 720 if you discover an error after you’ve already filed. Use Form 720-X, which is specifically designed for making corrections to your previously submitted Form 720. Ensure you follow the instructions closely when filing an amendment.

Form 720 covers various excise taxes, including but not limited to:

Each tax may have different reporting requirements, so be sure to check the instructions or consult with a tax professional.

You can find IRS Form 720 on the official IRS website. The form is available for download in PDF format. Additionally, the website provides detailed instructions on how to complete and submit it.

No, there is no fee for filing Form 720 itself. However, if you owe excise taxes, you'll need to pay them along with your filing. Be prepared to submit payment electronically or by check, depending on your filing method.

Filing the IRS Form 720 can be a straightforward process, yet many individuals make common mistakes that lead to complications. First and foremost, failing to identify the applicable tax period can cause confusion. Taxpayers must specify whether they are reporting for a quarterly or annual period. If this information is incorrect, it may result in penalties or delays in processing.

Another frequent oversight involves incomplete information. Many filers neglect to provide all required details about their business activity or industry classification. This lack of thoroughness can hinder the IRS's ability to properly review the submission. Ensuring that all sections of the form are filled out accurately and completely is essential.

The third mistake involves incorrect calculations. Taxpayers might miscalculate their tax liabilities or misinterpret the tax rate applicable to their activities. This can lead to either overpayment or underpayment, both of which carry potential consequences. It is vital to double-check all calculations and consult IRS guidelines to confirm accuracy.

Furthermore, another error people often commit is neglecting to sign and date the form. Without a signature, the form is considered incomplete. The IRS does not process unsigned forms, which can cause delays and necessitate re-filing.

Not keeping a copy of the submitted form represents a fifth pitfall. Documentation is crucial for future reference or in case the IRS requests additional information or clarification. Retaining a copy of the completed form provides a safeguard against possible disputes.

Lastly, failing to file on time can result in penalties or interest on overdue payments. Many individuals underestimate the importance of adhering to deadlines, which can lead to unnecessary financial burdens. Setting reminders or using electronic filing options can help ensure timely submissions.

The IRS Form 720, known as the Quarterly Federal Excise Tax Return, is a critical document for reporting and paying federal excise taxes. When completing this form, individuals and businesses may also need to reference or submit additional forms and documents related to these taxes. Below is a list of other forms and documents that are often used in conjunction with the IRS Form 720.

Using the correct forms in conjunction with IRS Form 720 is essential for compliance with federal tax obligations. Each form serves a specific purpose and helps ensure that taxpayers report their taxes accurately and completely.

When filling out the IRS Form 720, it's essential to keep several key points in mind. Here are six things you should and shouldn't do to ensure your submission is accurate and complete.

Misconceptions about the IRS 720 form can lead to confusion among taxpayers. Understanding these misconceptions can help clarify the purpose and requirements of the form. Here are six common misunderstandings:

Understanding these misconceptions helps ensure compliance with IRS regulations and simplifies the filing process.

When dealing with the IRS 720 form, understanding its purpose and proper completion is essential. Here are some important takeaways to keep in mind: