The IRS 8233 form plays a crucial role for non-resident aliens seeking to claim exemption from withholding on certain types of income. This form is primarily used by individuals who are receiving compensation for personal services performed in the United States, such as wages, salaries, or fees. By submitting Form 8233, eligible individuals can avoid excessive withholding on their earnings, ensuring they receive the full amount owed for their work. It is important to note that this form is typically utilized by foreign students, teachers, researchers, and other professionals who qualify under specific tax treaties between their home country and the U.S. Understanding the requirements for completing and submitting this form is essential, as inaccuracies or delays can lead to unnecessary tax complications. Additionally, the IRS mandates that certain conditions be met for the exemption to be granted, including proper documentation and adherence to deadlines. Overall, the IRS 8233 form serves as a vital tool for non-resident aliens, allowing them to navigate the complexities of U.S. tax obligations while maximizing their earnings.

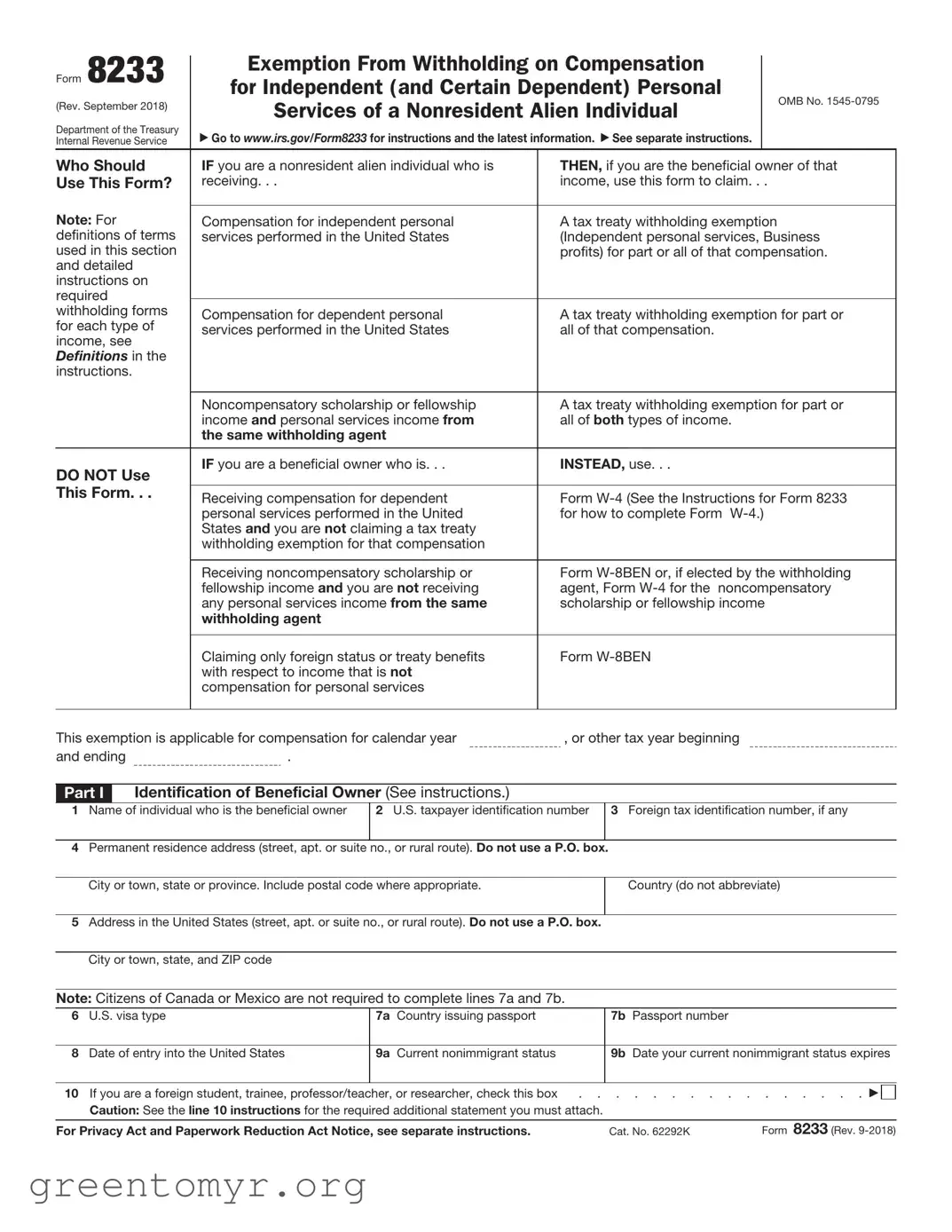

Form 8233

(Rev. September 2018)

Department of the Treasury Internal Revenue Service

Exemption From Withholding on Compensation for Independent (and Certain Dependent) Personal Services of a Nonresident Alien Individual

Go to www.irs.gov/Form8233 for instructions and the latest information. See separate instructions.

OMB No.

Who Should |

IF you are a nonresident alien individual who is |

THEN, if you are the beneficial owner of that |

Use This Form? |

receiving. . . |

income, use this form to claim. . . |

Note: For |

|

|

Compensation for independent personal |

A tax treaty withholding exemption |

|

definitions of terms |

services performed in the United States |

(Independent personal services, Business |

used in this section |

|

profits) for part or all of that compensation. |

and detailed |

|

|

instructions on |

|

|

required |

|

|

|

|

|

withholding forms |

Compensation for dependent personal |

A tax treaty withholding exemption for part or |

for each type of |

services performed in the United States |

all of that compensation. |

income, see |

|

|

Definitions in the |

|

|

instructions. |

|

|

|

|

|

|

Noncompensatory scholarship or fellowship |

A tax treaty withholding exemption for part or |

|

income and personal services income from |

all of both types of income. |

|

the same withholding agent |

|

|

|

|

DO NOT Use |

IF you are a beneficial owner who is. . . |

INSTEAD, use. . . |

|

|

|

This Form. . . |

Receiving compensation for dependent |

Form |

|

||

|

personal services performed in the United |

for how to complete Form |

|

States and you are not claiming a tax treaty |

|

|

withholding exemption for that compensation |

|

|

|

|

|

Receiving noncompensatory scholarship or |

Form |

|

fellowship income and you are not receiving |

agent, Form |

|

any personal services income from the same |

scholarship or fellowship income |

|

withholding agent |

|

|

|

|

|

Claiming only foreign status or treaty benefits |

Form |

|

with respect to income that is not |

|

|

compensation for personal services |

|

|

|

|

This exemption is applicable for compensation for calendar year |

, or other tax year beginning |

|

and ending |

. |

|

Part I Identification of Beneficial Owner (See instructions.)

1Name of individual who is the beneficial owner

2U.S. taxpayer identification number

3Foreign tax identification number, if any

4Permanent residence address (street, apt. or suite no., or rural route). Do not use a P.O. box.

City or town, state or province. Include postal code where appropriate.

Country (do not abbreviate)

5Address in the United States (street, apt. or suite no., or rural route). Do not use a P.O. box.

City or town, state, and ZIP code

Note: Citizens of Canada or Mexico are not required to complete lines 7a and 7b.

6U.S. visa type

7a Country issuing passport

7b Passport number

8Date of entry into the United States

9a Current nonimmigrant status

9b Date your current nonimmigrant status expires

10 If you are a foreign student, trainee, professor/teacher, or researcher, check this box |

. . . . . . . . . . . . . . . . |

|

Caution: See the line 10 instructions for the required additional statement you must attach. |

|

|

For Privacy Act and Paperwork Reduction Act Notice, see separate instructions. |

Cat. No. 62292K |

Form 8233 (Rev. |

Form 8233 (Rev. |

Page 2 |

|

Part II |

Claim for Tax Treaty Withholding Exemption |

|

11Compensation for independent (and certain dependent) personal services: a Description of personal services you are providing

b Total compensation you expect to be paid for these services in this calendar or tax year $

12If compensation is exempt from withholding based on a tax treaty benefit, provide: a Tax treaty on which you are basing exemption from withholding

b Treaty article on which you are basing exemption from withholding

c Total compensation listed on line 11b above that is exempt from tax under this treaty $ d Country of residence

Note: Do not complete lines 13a through 13d unless you also received compensation for personal services from the same withholding agent.

13Noncompensatory scholarship or fellowship income:

aAmount $

bTax treaty on which you are basing exemption from withholding

cTreaty article on which you are basing exemption from withholding

dTotal income listed on line 13a above that is exempt from tax under this treaty $

14Sufficient facts to justify the exemption from withholding claimed on line 12 and/or line 13 (see instructions)

Part III Certification

Under penalties of perjury, I declare that I have examined the information on this form and to the best of my knowledge and belief it is true, correct, and complete. I further certify under penalties of perjury that:

•I am the beneficial owner (or am authorized to sign for the beneficial owner) of all the income to which this form relates.

•The beneficial owner is not a U.S. person.

•The beneficial owner is a resident of the treaty country listed on line 12a and/or 13b above within the meaning of the income tax treaty

between the United States and that country, or was a resident of the treaty country listed on line 12a and/or 13b above at the time of, or immediately prior to, entry into the United States, as required by the treaty.

Furthermore, I authorize this form to be provided to any withholding agent that has control, receipt, or custody of the income of which I am the beneficial owner or any withholding agent that can disburse or make payments of the income of which I am the beneficial owner.

Sign Here |

▶ Signature of beneficial owner (or individual authorized to sign for beneficial owner) |

Date |

|

|

|

|

|

Part IV |

|

Withholding Agent Acceptance and Certification |

|

Name

Employer identification number

Address (number and street) (Include apt. or suite no. or P.O. box, if applicable.)

City, state, and ZIP code

Telephone number

Under penalties of perjury, I certify that I have examined this form and any accompanying statements, that I am satisfied that an exemption from withholding is warranted, and that I do not know or have reason to know that the nonresident alien individual is not entitled to the exemption or that the nonresident alien’s eligibility for the exemption cannot be readily determined.

Signature of withholding agent |

Date |

Form 8233 (Rev.

| Fact Name | Description |

|---|---|

| Purpose | The IRS 8233 form is used by non-resident aliens to claim exemption from withholding on compensation for independent personal services. |

| Eligibility | Only non-resident aliens who are providing services in the U.S. may use this form to avoid withholding taxes. |

| Submission | The completed form must be submitted to the payer before the payment is made to ensure proper tax treatment. |

| Governing Law | The IRS 8233 form is governed by U.S. federal tax laws, specifically the Internal Revenue Code. |

| Renewal | This form must be submitted each year or whenever there is a change in circumstances affecting the exemption. |

| Consequences of Non-Compliance | If the form is not submitted or is filled out incorrectly, the payer may be required to withhold taxes on the payments made. |

Completing the IRS 8233 form is an important step for non-resident aliens seeking to claim a tax exemption on income. After filling out the form, you will need to submit it to the appropriate withholding agent, who will process your request. Make sure all information is accurate to avoid delays.

IRS Form 8233 is a document used by nonresident aliens to claim exemption from withholding on compensation for independent personal services. This form is typically utilized by foreign individuals who are performing services in the United States, such as independent contractors or certain types of professionals.

Individuals who are nonresident aliens and are receiving compensation for independent personal services performed in the U.S. may need to file Form 8233. This includes:

Form 8233 should be submitted to the payer before the payment is made. It is important to file this form in a timely manner to ensure that the appropriate withholding exemption is applied. Ideally, submit the form at least a few weeks prior to the expected payment date.

Form 8233 requires various pieces of information, including:

If Form 8233 is not filed, the payer may be required to withhold taxes on your compensation at the standard rates. This could lead to a higher tax liability for you, as you may miss out on potential exemptions available through tax treaties.

Form 8233 is generally valid for the tax year in which it is filed. However, if there are changes in your circumstances or if you receive additional payments, you may need to submit a new form. Always ensure that the information provided is current and accurate.

Yes, Form 8233 can be used for multiple payments, but it must be submitted for each tax year. If you expect to receive payments in subsequent years, you will need to refile the form each year to maintain the exemption status.

IRS Form 8233 can be found on the official IRS website. It is available for download in PDF format. Additionally, instructions for completing the form are also provided on the IRS website to assist you in the filing process.

Filling out the IRS 8233 form can be a straightforward process, but many people make common mistakes that can lead to delays or issues with their tax filings. One frequent error is not providing accurate personal information. Ensure that your name, address, and taxpayer identification number are correct. Any discrepancies can cause significant problems down the line.

Another mistake is failing to check the correct box regarding your eligibility for tax treaty benefits. This section is crucial, as it determines whether you qualify for exemptions from withholding. Carefully review the tax treaty provisions that apply to your situation before making a selection.

Many individuals overlook the importance of signing and dating the form. An unsigned form is considered incomplete and will not be processed. Make sure to sign where indicated and include the date to avoid unnecessary complications.

Providing incorrect or incomplete information about your income is another common pitfall. It’s essential to accurately report the type and amount of income you expect to receive. This information helps the IRS determine your eligibility for tax treaty benefits.

Some people forget to attach the necessary documentation that supports their claims. This could include a copy of the tax treaty or any other relevant documents. Without this evidence, the IRS may deny your request for tax benefits.

Another mistake is not keeping a copy of the completed form for your records. Having a copy can be invaluable if any questions arise later. It’s always wise to maintain thorough records of all tax-related documents.

Lastly, many individuals do not seek assistance when needed. If you are unsure about any part of the form, consult a tax professional. Getting help can save you time and prevent costly errors.

The IRS 8233 form is used by non-resident aliens to claim exemption from withholding on compensation for independent personal services. Several other forms and documents may accompany the 8233 to ensure proper processing and compliance with tax regulations. Below is a list of commonly associated forms and documents.

Understanding these forms and documents is crucial for non-resident aliens seeking to navigate the U.S. tax system effectively. Properly completing and submitting these forms can help ensure compliance and minimize tax liabilities.

The IRS Form 8233 is primarily used by non-resident aliens to claim exemption from withholding on compensation for independent personal services. However, there are several other forms and documents that share similarities with Form 8233 in terms of purpose, audience, or function. Below is a list of nine such documents, each highlighting its relationship to Form 8233.

Each of these forms serves a specific purpose but shares a common thread with Form 8233 in terms of addressing the tax obligations and benefits for non-resident aliens in the United States.

When filling out the IRS 8233 form, it is important to follow certain guidelines to ensure accuracy and compliance. Here’s a list of things you should and shouldn’t do:

The IRS 8233 form is an important document for non-resident aliens who are claiming exemption from withholding on compensation for independent personal services. However, several misconceptions surround this form. Here are ten common misunderstandings:

Only students can use Form 8233. Many believe that only students or scholars can file this form. In reality, any non-resident alien who is receiving compensation for independent personal services can use it, provided they meet certain criteria.

Form 8233 guarantees exemption from all taxes. Some think that submitting this form automatically exempts them from all taxes. This is not true; it only exempts certain types of income from withholding, not from tax liability itself.

Form 8233 is only for employees. Many assume this form is only applicable to employees. However, it is specifically designed for independent contractors and self-employed individuals as well.

You can submit Form 8233 at any time. Some believe they can submit this form whenever they want. In fact, it must be submitted before the payment is made to ensure proper withholding.

All non-resident aliens qualify for the exemption. There is a misconception that all non-resident aliens can use Form 8233. However, eligibility depends on tax treaties between the U.S. and the individual's home country.

Filing Form 8233 means you won't owe taxes later. Many think that by filing this form, they will not owe taxes at the end of the year. However, they may still have tax obligations based on their total income.

Form 8233 can be filed without a tax identification number. Some believe they can submit the form without a Taxpayer Identification Number (TIN). A TIN is required for the form to be valid.

Once submitted, Form 8233 cannot be revoked. There is a belief that once the form is submitted, it cannot be changed or revoked. However, individuals can revoke their exemption at any time by notifying the payer.

Form 8233 is the same as W-8BEN. Many confuse Form 8233 with W-8BEN. While both are used by non-resident aliens, they serve different purposes and have different requirements.

Filing Form 8233 is a one-time process. Some think that once they file the form, they never need to do it again. In reality, the form must be filed for each tax year or for each new payment arrangement.

Understanding these misconceptions can help non-resident aliens navigate the complexities of tax withholding and ensure compliance with U.S. tax laws. Always consider seeking advice from a tax professional to clarify any uncertainties regarding the IRS 8233 form.

The IRS 8233 form is essential for non-resident aliens claiming exemption from withholding on compensation for independent personal services. Here are some key takeaways regarding this form:

Understanding these points can help ensure that the form is filled out correctly and that individuals can take advantage of tax treaty benefits where applicable.