Understanding tax credits can be a rewarding endeavor, especially when it comes to maximizing your family’s benefits. One critical tool in this process is the IRS Form 8862, which plays a pivotal role for taxpayers who have previously faced a denial of the Earned Income Credit, the Child Tax Credit, or the Additional Child Tax Credit due to a failed compliance with certain eligibility requirements. Successfully completing Form 8862 is essential for those wishing to reclaim these important tax credits after having their prior claims denied. This form not only asks for personal information and tax filing history but also requires a demonstration that the issues leading to the previous denial have been resolved. Whether it’s proving residency, dependency, or qualifying income, failure to provide adequate information may jeopardize your ability to claim these credits once more. Delving into the intricacies of this form can provide guidance and clarity, ensuring that you navigate the application process smoothly and confidently.

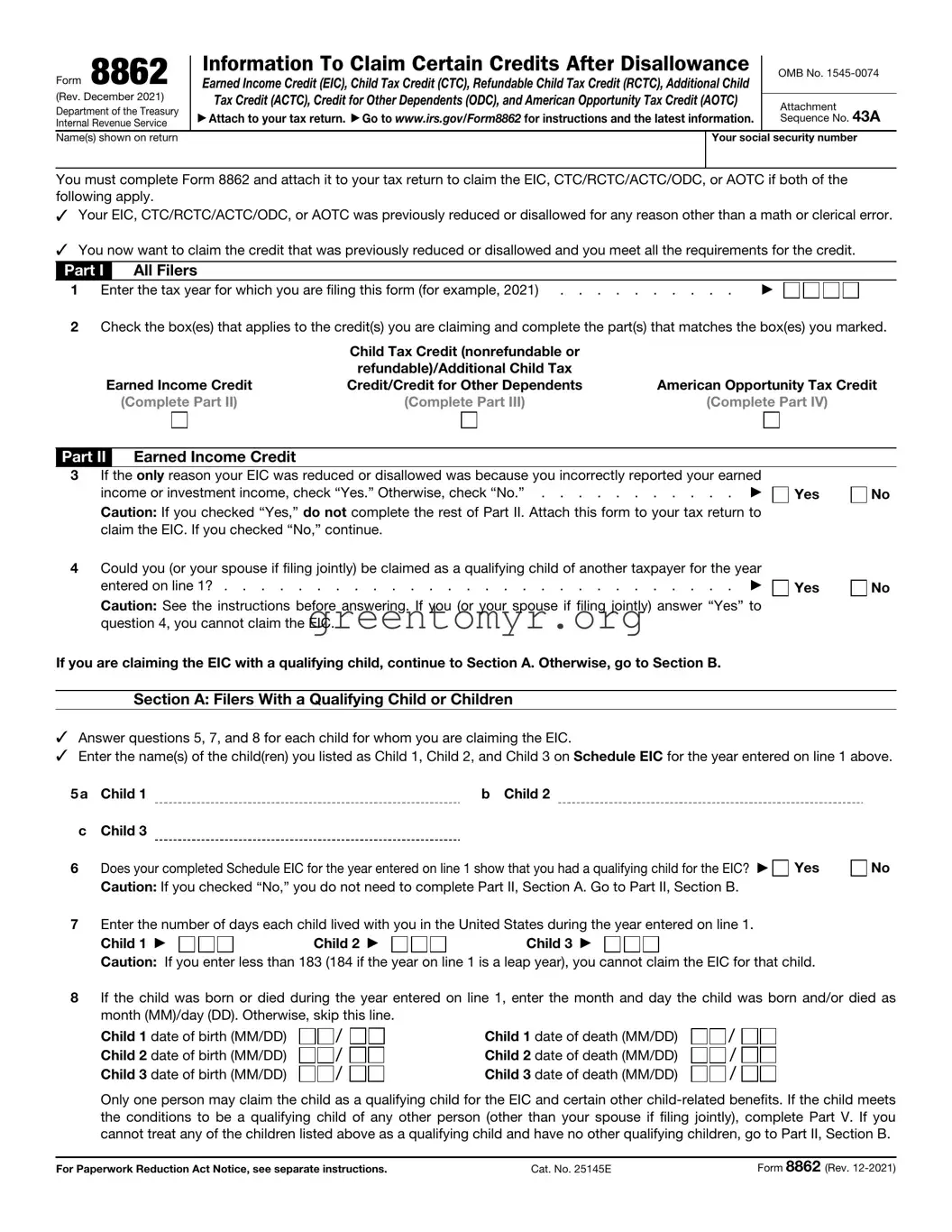

Form 8862 |

Information To Claim Certain Credits After Disallowance |

OMB No. |

||

Earned Income Credit (EIC), American Opportunity Tax Credit (AOTC), Child Tax Credit (CTC), |

|

|||

(Rev. November 2018) |

Additional Child Tax Credit (ACTC), and Credit for Other Dependents (ODC) |

|

||

Attachment |

||||

Department of the Treasury |

|

|

||

Attach to your tax return. Go to www.irs.gov/Form8862 for instructions and the latest information. |

Sequence No. 43A |

|||

Internal Revenue Service |

||||

|

|

|

||

Name(s) shown on return |

|

Your social security number |

||

|

|

|

|

|

You must complete Form 8862 and attach it to your tax return to claim the EIC, CTC/ACTC/ODC, or AOTC if both of the following apply.

Your EIC, CTC/ACTC/ODC, or AOTC was previously reduced or disallowed for any reason other than a math or clerical error.

You now want to claim the credit that was previously reduced or disallowed and you meet all the requirements for the credit.

Part I |

All Filers |

|

1 |

Enter the tax year for which you are filing this form (for example, 2018) |

|

2Check the box(es) that applies to the credit(s) you are claiming and complete the part(s) that matches the box(es) you marked.

|

Child Tax Credit/Additional Child Tax |

|

Earned Income Credit |

Credit/Credit for Other Dependents |

American Opportunity Tax Credit |

(Complete Part II) |

(Complete Part III) |

(Complete Part IV) |

Part II Earned Income Credit

3If the only reason your EIC was reduced or disallowed was because you incorrectly reported your earned

income or investment income, check “Yes.” Otherwise, check “No.” |

Yes |

Caution: If you checked “Yes,” do not complete the rest of Part II. Attach this form to your tax return to |

|

claim the EIC. If you checked “No,” continue. |

|

No

4Could you (or your spouse if filing jointly) be claimed as a qualifying child of another taxpayer for the year entered on line 1? . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Caution: See the instructions before answering. If you (or your spouse if filing jointly) answer “Yes” to question 4, you cannot claim the EIC.

If you are claiming the EIC with a qualifying child, continue to Section A. Otherwise, go to Section B.

Yes

No

Section A: Filers With a Qualifying Child or Children

Answer questions 5, 7, and 8 for each child for whom you are claiming the EIC.

Enter the name(s) of the child(ren) you listed as Child 1, Child 2, and Child 3 on Schedule EIC for the year entered on line 1 above.

5a |

Child 1 |

b Child 2 |

|

c |

Child 3 |

|

|

6 |

Does your completed Schedule EIC for the year entered on line 1 show that you had a qualifying child for the EIC? |

Yes |

|

|

Caution: If you checked “No,” you do not need to complete Part II, Section A. Go to Part II, Section B. |

|

|

7Enter the number of days each child lived with you in the United States during the year entered on line 1.

Child 1 |

Child 2 |

Child 3 |

Caution: If you enter less than 183 (184 if the year on line 1 is a leap year), you cannot claim the EIC for that child.

No

8If the child was born or died during the year entered on line 1, enter the month and day the child was born and/or died as month (MM)/day (DD). Otherwise, skip this line.

Child 1 date of birth (MM/DD) |

/ |

Child 1 date of death (MM/DD) |

/ |

Child 2 date of birth (MM/DD) |

/ |

Child 2 date of death (MM/DD) |

/ |

Child 3 date of birth (MM/DD) |

/ |

Child 3 date of death (MM/DD) |

/ |

Only one person may claim the child as a qualifying child for the EIC and certain other

For Paperwork Reduction Act Notice, see separate instructions. |

Cat. No. 25145E |

Form 8862 (Rev. |

Form 8862 (Rev.

Section B: Filers Without a Qualifying Child or Children

9a Enter the number of days during the year entered on line 1 that your main home was in the United States . . .

bIf married filing jointly, enter the number of days during the year entered on line 1 that your spouse’s main home was

|

in the United States |

|

|

Caution: Members of the military stationed outside the United States during the year entered on line 1, see the instructions |

|

|

before answering. If you enter less than 183 (184 if the year on line 1 is a leap year) on either line 9a or 9b (if filing jointly), you |

|

|

cannot claim the EIC. |

|

10a |

Enter your age at the end of the year on line 1 |

|

b |

Enter your spouse’s age at the end of the year on line 1 |

|

|

Caution: If your spouse died during the year entered on line 1 or you are preparing a return for someone who died during the |

|

|

year entered on line 1, see the instructions before answering. If neither you (nor your spouse if filing jointly) were at least age 25 |

|

|

but under age 65 at the end of the year on line 1, you cannot claim the EIC. |

|

11a Can you be claimed as a dependent on another taxpayer’s return? . . . . . . . . . . . .

bCan your spouse (if filing jointly) be claimed as a dependent on another taxpayer’s return? . . . .

Caution: If either you (or your spouse if filing jointly) answer “Yes” to question 11, you cannot claim the EIC.

Yes Yes

No No

Part III Child Tax Credit/Additional Child Tax Credit/Credit for Other Dependents

12Enter the name(s) of each child for whom you are claiming the child tax credit/additional child tax credit (CTC/ACTC). If you are claiming the CTC/ACTC for more than four qualifying children, attach a statement also answering questions 12 and

a |

Child 1 |

b |

Child 2 |

c |

Child 3 |

d |

Child 4 |

13Enter the name(s) of each person for whom you are claiming the credit for other dependents (ODC). If you are claiming the credit for more than four dependents, attach a statement answering questions 13, 16, and 17 for those dependents.

a |

Other dependent 1 |

b |

Other dependent 2 |

c |

Other dependent 3 |

d |

Other dependent 4 |

14For each child listed in response to question 12, did the child live with you for more than half of the year or meet an exception described in the instructions?

Child 1

Yes

No |

Child 2 |

Yes

No |

Child 3 |

Yes

No |

Child 4 |

Yes

No

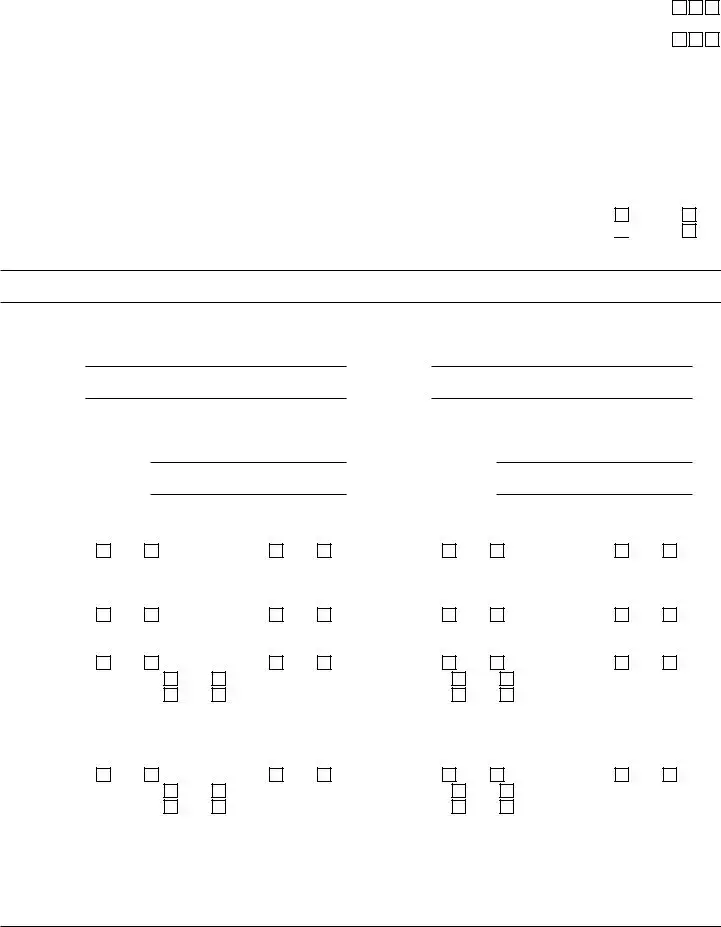

15For each child listed in response to question 12, did the child meet the requirements to be a qualifying child for the CTC/ACTC?

Child 1

Yes

No |

Child 2 |

Yes

No |

Child 3 |

Yes

No |

Child 4 |

Yes

No

16For each person claimed as a qualifying child or other dependent for the CTC/ACTC/ODC, is that person your dependent?

Child 1

Yes

No |

Child 2 |

Yes

No |

Child 3 |

Yes

No |

Child 4 |

Yes

No

Other dependent 1

Yes

No |

Other dependent 2 |

Yes

No

Other dependent 3

Yes

No |

Other dependent 4 |

Yes

No

17For each person claimed as a qualifying child or other dependent for the CTC/ACTC/ODC, is that person a citizen, national, or resident of the United States? See Pub. 519 for more information on when a person is a resident of the United States or is treated as a resident of the United States.

Child 1 |

Yes |

Other dependent 1 Other dependent 3

No

Yes

Yes

Child 2

No

No

Yes

No |

Child 3 |

Other dependent 2 Other dependent 4

Yes

Yes

Yes

No |

Child 4 |

No |

|

No |

|

Yes

No

Caution: If the answer is “No” for questions 14, 15, 16, or 17, you cannot claim the CTC/ACTC/ODC for that child or other dependent.

Only one person can claim the child as a qualifying child for the CTC/ACTC/ODC. If the child meets the conditions to be a qualifying child of any other person (other than your spouse if filing jointly), complete Part V. If you cannot treat any of the children listed above as a qualifying child and have no other qualifying children, you cannot claim the CTC/ACTC or the ODC based on having a qualifying child. If you are a noncustodial parent who is entitled to treat the child as a qualifying child, you do not need to complete Part V.

Form 8862 (Rev.

Form 8862 (Rev. |

Page 3 |

|

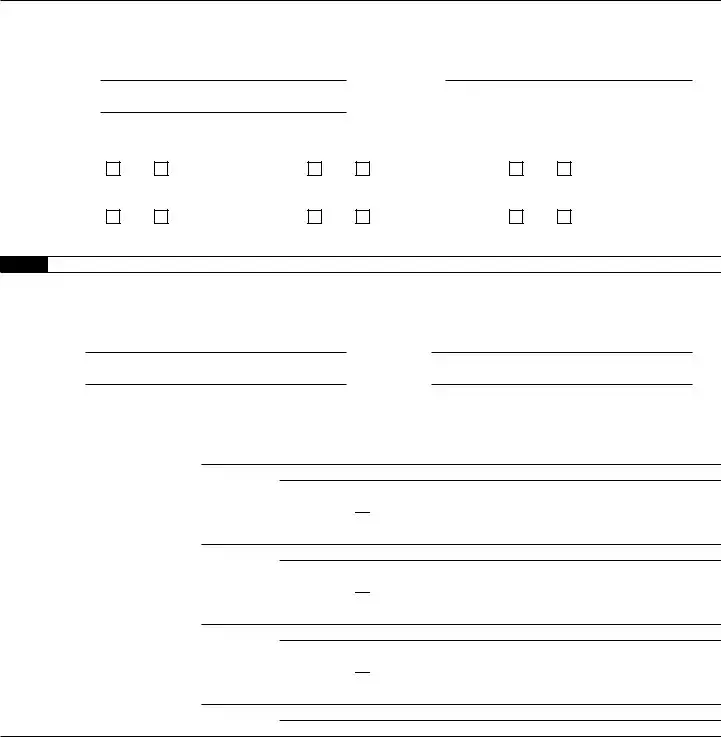

Part IV |

American Opportunity Tax Credit |

|

Answer the following questions for each student for whom you are claiming the AOTC. If you have more than three students, attach a statement also answering questions 18 and 19 for those students.

Enter the name(s) of the student(s) as listed on Form 8863.

18a Student 1 |

b Student 2 |

cStudent 3

19a Did the student meet the requirements to be an eligible student for purposes of the AOTC for the year entered on line 1? See Pub. 970 for more information.

Student 1

Yes

No |

Student 2 |

Yes

No |

Student 3 |

Yes

No

bHas the Hope Scholarship Credit or AOTC been claimed for the student for any 4 tax years before the year entered on line 1?

Student 1

Yes

No |

Student 2 |

Yes

No |

Student 3 |

Yes

No

Caution: If you answered “No” to question 19a or “Yes” to question 19b, you cannot claim the credit for that student.

Part V Qualifying Child of More Than One Person

Answer the following questions for each child who meets the conditions to be a qualifying child of any other person (other than your spouse if filing jointly). If you have more than four qualifying children, attach a statement also answering questions

20a |

Child 1 |

b |

Child 2 |

c |

Child 3 |

d |

Child 4 |

21Enter the address where you and the child lived together during the year entered on line 1. If you lived with the child at more than one address during the year, attach a list of the addresses where you lived.

Child 1 Number and street

City or town, state, and ZIP code

Child 2 If same as shown for Child 1, check this box

Number and street

City or town, state, and ZIP code

Child 3 If same as shown for Child 1, check this box

Number and street

City or town, state, and ZIP code

Child 4 If same as shown for Child 1, check this box

Number and street

City or town, state, and ZIP code

Otherwise, enter below.

Otherwise, enter below.

Otherwise, enter below.

Form 8862 (Rev.

Form 8862 (Rev. |

Page 4 |

|

Part V |

Qualifying Child of More Than One Person (continued) |

|

22Did any other person (except your spouse, if filing jointly, and your dependents claimed on your return)

live with Child 1, Child 2, Child 3, or Child 4 for more than half the year? |

Yes |

If “Yes,” enter the relationship of each person to the child on the appropriate line below. |

|

No

Other person living with Child 1: Name

Relationship to Child 1

Other person living with Child 2: If same as shown for Child 1, check this box

Name

Relationship to Child 2

Other person living with Child 3: If same as shown for Child 1, check this box

Name

Relationship to Child 3

Other person living with Child 4: If same as shown for Child 1, check this box

Name

Relationship to Child 4

Otherwise, enter below.

Otherwise, enter below.

Otherwise, enter below.

To determine which person can treat the child as a qualifying child for the EIC and CTC/ACTC, see Qualifying Child of More Than One Person in Pub. 501.

Note: The IRS may ask you to provide additional information to verify your eligibility to claim each credit.

Form 8862 (Rev.

| Fact Name | Description |

|---|---|

| Purpose | The IRS 8862 form is used by individuals to claim the Earned Income Tax Credit (EITC) after the credit was previously denied or revoked. |

| Eligibility | Taxpayers must complete this form and provide certain information to demonstrate eligibility for the EITC in subsequent tax years. |

| Submission | The form must be submitted with the tax return for the year the taxpayer is claiming the credit. |

| Compliance | Filing this form is a requirement based on IRS guidelines to ensure compliance if the taxpayer has previously been disallowed the credit. |

Completing the IRS Form 8862 requires careful attention to detail. This form is used by taxpayers who need to reclaim a tax benefit or establish eligibility for certain tax credits. Follow these steps to ensure accurate completion.

Once the form is completed, be sure to attach it to your tax return when submitting. Keep a copy for your records. Processing may take some time, so patience is necessary as you await a response from the IRS.

IRS Form 8862, titled "Information to Claim Certain Tax Benefits After Disallowance," is an important document for individuals who have previously had their claim for certain tax credits disallowed. Specifically, this form is required after a denial of the Earned Income Tax Credit (EITC) or the Child and Dependent Care Credit. By filing Form 8862, taxpayers can provide information that demonstrates their eligibility to claim these credits once again.

You should file Form 8862 if you have previously claimed the EITC or Child and Dependent Care Credit and your request for these credits was disallowed by the IRS. If you want to claim these credits in a future tax return, you’ll need to include Form 8862 to inform the IRS that you believe you meet the qualifications. It is essential to file this form with your tax return for the year you wish to claim the credits after the disallowance.

Form 8862 requires several pieces of information that help the IRS determine your eligibility. Here are key sections of the form:

It’s vital to review the instructions carefully before completing the form to ensure all required information is accurately provided.

If you do not file Form 8862 after your claim has been disallowed, your efforts to claim the EITC or Child and Dependent Care Credit may be rejected by the IRS. The credits cannot be claimed until the form is filed and your eligibility has been established. This means you could miss out on potential tax benefits that may provide significant financial assistance.

You can obtain IRS Form 8862 directly from the IRS website. The form is available for download in PDF format, which you can print and complete. Additionally, the accompanying instructions provide valuable insights on how to fill out the form accurately. If you prefer physical copies, many local libraries and post offices have tax forms available during the filing season. Tax software programs often include Form 8862 as part of their offerings as well.

Completing the IRS Form 8862 can be a complex process. Many individuals encounter common pitfalls that can delay their tax returns or lead to rejection of claims. By being aware of these mistakes, taxpayers can improve the accuracy of their submissions.

One frequent error is failing to provide the required identifying information, such as Social Security numbers. Each person listed on the form must have a valid Social Security number. Missing or incorrect numbers can result in processing delays.

Another common mistake involves incorrectly reporting dependency status. Taxpayers must clearly indicate who qualifies as a dependent. Misinterpretation of the dependency rules can lead to significant issues, particularly when claiming credits like the Earned Income Tax Credit.

Inaccurate information about the previous year’s tax return can also pose problems. Form 8862 asks if an individual has ever had a claim denied for certain tax benefits. Providing incorrect details may not only slow down processing but could also flag the return for further review by the IRS.

Some filers forget to sign and date their form. An unsigned application may be sent back by the IRS, causing delays. Always ensure that there is a proper signature and date before submission.

Additionally, people often overlook the importance of answering all questions thoroughly and accurately. Form 8862 includes sections that require specific details about previous income and tax filings. Incomplete responses can lead to automatic denial.

Another mistake is miscalculating income levels. Eligibility for certain tax credits depends on income thresholds, which can differ significantly from year to year. Taxpayers must ensure they are using the correct figures to avoid potential disqualification.

Failure to attach the necessary documentation is a frequent oversight. Taxpayers should always verify that they have included supporting documents, such as tax returns from previous years or proof of residency. Without this paperwork, claims may be denied.

Often, individuals do not review the entire form for clarity and detail. Taking the extra time to double-check responses can help in recognizing potential discrepancies or errors before submission.

Lastly, procrastination can lead to filling out the form hurriedly, which increases the likelihood of mistakes. It’s vital to set aside sufficient time to complete the form carefully. Proper planning ensures a more accurate and timely submission, minimizing potential issues with the IRS.

The IRS 8862 form is an important document for taxpayers who have experienced issues claiming tax credits. However, it's often accompanied by other forms and documents that help support your claim. Here are some of the commonly used forms and documents that you may need alongside the IRS 8862 form.

Having these forms ready can ensure a smoother process when you file your taxes. Proper documentation shows your eligibility and can help resolve any issues related to your tax credits.

When filling out the IRS Form 8862, it's important to follow guidelines to ensure accuracy and compliance. Here are ten actions you should take and avoid:

By following these guidelines, you can avoid common pitfalls and ensure that your submission is handled efficiently.

The IRS Form 8862 is often surrounded by misconceptions that can lead to confusion among taxpayers. Here are nine common misconceptions about this form, along with explanations to clarify each point:

This form is actually used by taxpayers who have previously claimed the Child Tax Credit or Additional Child Tax Credit and were denied. It helps reinstate eligibility for these credits after a denial.

You only need to file this form after a prior disallowance if you wish to claim the same tax credits again. If your circumstances haven't changed, you might not need to submit it every year.

While Form 8862 is necessary to establish your eligibility, it does not automatically secure the credits. You must still meet all other criteria set by the IRS.

If you fail to submit Form 8862 on time, you risk losing the ability to claim the tax credits for that year. Timeliness is critical to ensure your claim is processed.

In reality, Form 8862 is designed to be user-friendly. Many taxpayers can complete it on their own without needing to hire a professional.

While the form can be filed electronically, it may require additional steps for verification if you previously had your credits disallowed.

Submitting this form can delay your refund, especially if the IRS needs more time to review your eligibility for credits.

This is not true; tax preparers are still required to perform due diligence in determining eligibility for credits, even when Form 8862 is involved.

You can still change how you claim your children and your filing status if circumstances change. However, you may need to submit adjusted documentation in line with your new claims.

Understanding these misconceptions can help you navigate the filing process more effectively and ensure you claim the credits you're eligible for.

When navigating the IRS Form 8862, understanding its purpose and how to fill it out is essential. Here are five key takeaways: