The IRS 8889 form is an essential document for individuals who have a Health Savings Account (HSA). This form serves multiple purposes, allowing you to report contributions to your HSA, track the distributions made throughout the year, and ensure compliance with tax regulations pertaining to health care expenses. With the growing importance of health care costs in personal finance, understanding how to accurately complete Form 8889 is crucial for optimizing tax benefits. Whether you're making contributions to your HSA, withdrawing funds for qualified medical expenses, or considering the impact of traditional or high-deductible health plans, this form captures your IRS obligations for the year. Furthermore, as tax laws evolve, it's vital to stay informed about any changes that might affect your HSA contributions and distributions. By getting familiar with the intricacies of Form 8889, you position yourself to take full advantage of the tax advantages tied to health savings accounts, making it easier to navigate the financial landscape of your healthcare needs.

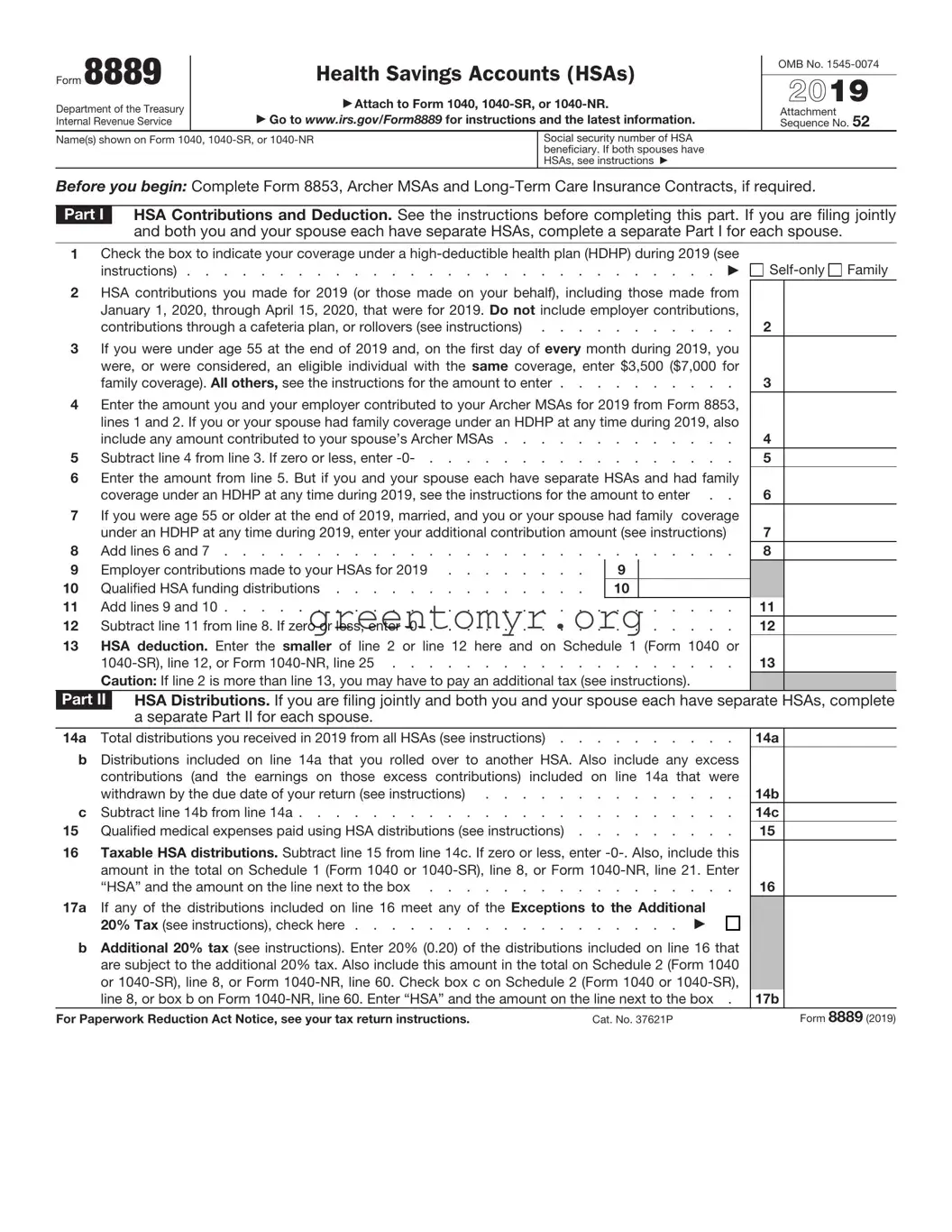

Form 8889

Department of the Treasury Internal Revenue Service

Health Savings Accounts (HSAs)

Attach to Form 1040,

Go to www.irs.gov/Form8889 for instructions and the latest information.

OMB No.

2019

Attachment Sequence No. 52

Name(s) shown on Form 1040,

Social security number of HSA beneficiary. If both spouses have HSAs, see instructions

Before you begin: Complete Form 8853, Archer MSAs and

Part I HSA Contributions and Deduction. See the instructions before completing this part. If you are filing jointly and both you and your spouse each have separate HSAs, complete a separate Part I for each spouse.

1Check the box to indicate your coverage under a

instructions) . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

2HSA contributions you made for 2019 (or those made on your behalf), including those made from January 1, 2020, through April 15, 2020, that were for 2019. Do not include employer contributions,

contributions through a cafeteria plan, or rollovers (see instructions) . . . . . . . . . . .

3If you were under age 55 at the end of 2019 and, on the first day of every month during 2019, you were, or were considered, an eligible individual with the same coverage, enter $3,500 ($7,000 for

family coverage). All others, see the instructions for the amount to enter . . . . . . . . . .

4Enter the amount you and your employer contributed to your Archer MSAs for 2019 from Form 8853, lines 1 and 2. If you or your spouse had family coverage under an HDHP at any time during 2019, also

include any amount contributed to your spouse’s Archer MSAs . . . . . . . . . . . . .

5 Subtract line 4 from line 3. If zero or less, enter

6Enter the amount from line 5. But if you and your spouse each have separate HSAs and had family

coverage under an HDHP at any time during 2019, see the instructions for the amount to enter . .

7If you were age 55 or older at the end of 2019, married, and you or your spouse had family coverage under an HDHP at any time during 2019, enter your additional contribution amount (see instructions)

8 |

Add lines 6 |

and |

7 |

||

9 |

Employer contributions made to your HSAs for 2019 |

9 |

|

||

10 |

Qualified HSA funding distributions |

10 |

|

||

11 |

Add lines 9 |

and |

10 |

||

12 |

Subtract line 11 from line 8. If zero or less, enter |

||||

13HSA deduction. Enter the smaller of line 2 or line 12 here and on Schedule 1 (Form 1040 or

Caution: If line 2 is more than line 13, you may have to pay an additional tax (see instructions).

Family

Family

2

3

4

5

6

7

8

11

12

13

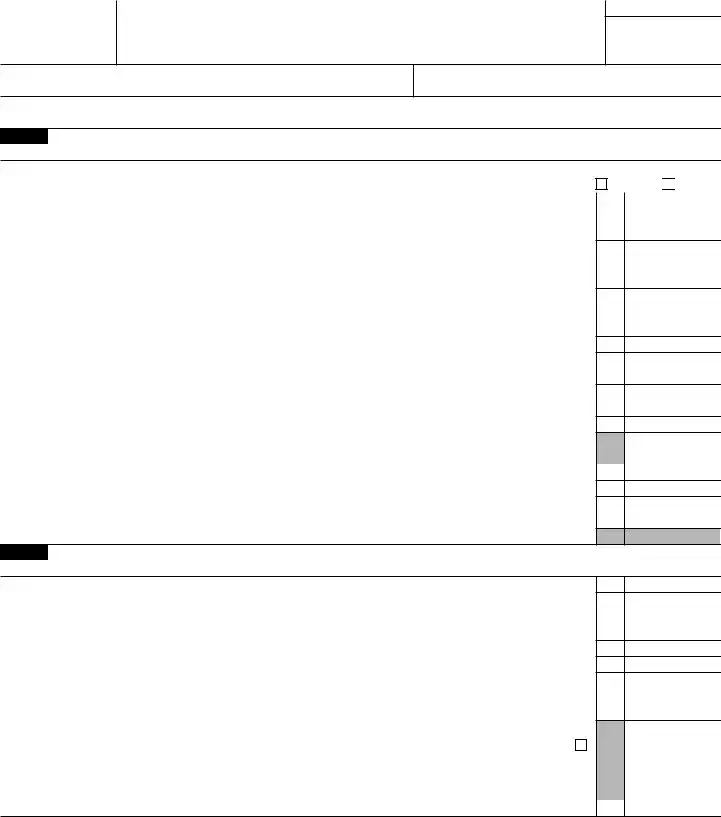

Part II HSA Distributions. If you are filing jointly and both you and your spouse each have separate HSAs, complete a separate Part II for each spouse.

14a Total distributions you received in 2019 from all HSAs (see instructions) . . . . . . . . . .

bDistributions included on line 14a that you rolled over to another HSA. Also include any excess contributions (and the earnings on those excess contributions) included on line 14a that were

|

withdrawn by the due date of your return (see instructions) |

c |

Subtract line 14b from line 14a |

15 |

Qualified medical expenses paid using HSA distributions (see instructions) |

16Taxable HSA distributions. Subtract line 15 from line 14c. If zero or less, enter

amount in the total on Schedule 1 (Form 1040 or

17a If any of the distributions included on line 16 meet any of the Exceptions to the Additional 20% Tax (see instructions), check here . . . . . . . . . . . . . . . . . .

bAdditional 20% tax (see instructions). Enter 20% (0.20) of the distributions included on line 16 that are subject to the additional 20% tax. Also include this amount in the total on Schedule 2 (Form 1040

or

14a

14b

14c

15

16

17b

For Paperwork Reduction Act Notice, see your tax return instructions. |

Cat. No. 37621P |

Form 8889 (2019) |

Form 8889 (2019) |

Page 2 |

Part III Income and Additional Tax for Failure To Maintain HDHP Coverage. See the instructions before completing this part. If you are filing jointly and both you and your spouse each have separate HSAs, complete a separate Part III for each spouse.

18

19 Qualified HSA funding distribution . . . . . . . . . . . . . . . . . . . . . . .

20Total income. Add lines 18 and 19. Include this amount on Schedule 1 (Form 1040 or

8, or Form

21Additional tax. Multiply line 20 by 10% (0.10). Include this amount in the total on Schedule 2 (Form 1040 or

18

19

20

21

Form 8889 (2019)

| Fact Name | Description |

|---|---|

| Purpose of IRS 8889 | The IRS 8889 form is used to report Health Savings Account (HSA) contributions and distributions. It helps taxpayers who have HSAs to demonstrate compliance with tax laws related to these accounts. |

| Eligibility Requirements | To use Form 8889, an individual must be enrolled in a high-deductible health plan (HDHP) and cannot have other health coverage that disqualifies them from contributing to an HSA. |

| Filing Deadline | Taxpayers must submit Form 8889 along with their annual tax return, typically due on April 15th. This means it is essential to keep accurate records of HSA contributions throughout the year. |

| Impact of Contributions | Contributions made to an HSA can be deducted from taxable income, potentially lowering the overall tax liability. This tax advantage makes HSAs an attractive option for individuals with qualified health plans. |

After obtaining the IRS Form 8889, it is essential to fill it out carefully to ensure proper reporting. This form deals with Health Savings Accounts (HSAs) and requires accurate information about contributions and distributions. Follow these steps closely to complete the form correctly.

Now that the form is completed, ensure it is submitted by the tax deadline. Keep a copy for your records and be prepared for any follow-up questions from the IRS regarding your reported HSA activity.

IRS Form 8889 is specifically designed for individuals who have established a Health Savings Account (HSA). This form allows you to report your HSA contributions, distributions, and any applicable deductions for the tax year. Completing this form correctly ensures compliance with IRS regulations regarding HSAs, an essential step to avoid potential penalties.

Individuals who have an HSA during the tax year are required to file Form 8889. If you have contributed to an HSA, received distributions from it, or both, you must include this form when filing your federal income tax return. Additionally, it is essential for those who are eligible for the HSA deduction, whether or not they have made contributions during the year.

Reporting HSA contributions on Form 8889 requires you to fill out Section I of the form. You will need to include contributions made by you, your employer, and any other eligible sources. It’s vital to keep track of your contributions as there are limits set by the IRS based on your age and health plan coverage, which can affect your tax deductions.

Distributions from an HSA must be reported in Section II of Form 8889. These distributions can be tax-free if used for qualified medical expenses. It's important to maintain accurate records of your distributions to ensure compliance with IRS rules. If the funds are used for non-qualified expenses, however, they may be subject to income tax and an additional penalty.

Withdrawing money from an HSA comes with specific tax implications. If the funds are used for qualifying medical expenses, the withdrawal is tax-free. Conversely, if the funds are withdrawn for non-qualifying expenses before the age of 65, penalties can apply. After age 65, distributions are subject to income tax but not penalties, which offers some tax relief for those who may not incur medical expenses.

Yes, contributions made to an HSA can be tax-deductible, potentially reducing your taxable income. When you complete Form 8889, you can claim these deductions in Section I. It is important to note that both personal contributions and those made by your employer qualify for this deduction. However, contributions above the IRS limits could disallow some of these deductions.

Failing to file Form 8889 when required can lead to penalties and complications with your tax return. The IRS may impose additional taxes on HSA distributions made for non-qualified expenses. Moreover, neglecting to report your HSA contributions may later result in a denied deduction, leading to higher taxable income.

To find more resources regarding IRS Form 8889, you can visit the official IRS website, where comprehensive details about HSAs and their tax advantages are available. Consulting a tax professional can also provide personalized assistance, ensuring that you meet everyone’s requirements and maximize your tax benefits correctly. Additionally, IRS Publication 969 offers in-depth explanations related to HSAs and Form 8889.

The IRS Form 8889 is crucial for anyone with a Health Savings Account (HSA). Many individuals appreciate the tax advantages associated with HSAs, but errors on this form can lead to complications. One common mistake is failing to properly report the contributions made to the HSA. Individuals may forget to include their own contributions or those made by their employer, leading to discrepancies.

Another frequent error involves incorrect calculations. Some taxpayers mistakenly calculate the contribution limits. This can occur particularly when individuals have family coverage versus individual coverage. Understanding the appropriate contribution limits is essential, as exceeding them may result in penalties.

Many people also overlook the importance of checking the date of their contributions. It is essential to note whether the contributions were made within the applicable tax year. Misplacing this detail can lead to confusion about which tax year the contributions should apply to, impacting tax liabilities.

People should also be cautious about not claiming qualified medical expenses. The IRS has specific guidelines on which expenses qualify for tax deduction. Failing to identify or document these expenses correctly can undermine the potential benefits of the HSA.

Moreover, some filers incorrectly report distributions from their HSAs. It is crucial to differentiate between qualified and non-qualified distributions. When distributions are misreported, it could lead to unnecessary taxation and penalties, creating a perplexing situation for taxpayers.

People often forget to sign the form. This might seem minor but lacks validation. Without a signature, the IRS could treat the form as incomplete, potentially delaying processing and approval.

Another mistake involves using outdated forms. Taxpayers may not realize that the IRS often updates its forms and instructions. Utilizing an outdated version can lead to misinterpretation of eligibility and criteria.

Additionally, individuals sometimes ignore the importance of keeping thorough records. Proper documentation of contributions, distributions, and expenses is vital. Without adequate records, one might struggle to substantiate claims during an audit.

Finally, some filers misinterpret the IRS instructions provided for the form. The guidance can be complex, and failure to follow the instructions closely may cause errors. Taking the time to read and understand each section can save headaches down the line.

The IRS Form 8889 is an important document that deals with Health Savings Accounts (HSAs). It helps individuals report contributions, distributions, and deductions related to their HSAs. However, it’s not the only form needed when managing HSAs. Several other documents often accompany this form, providing essential information for both taxpayers and the IRS.

In summary, understanding and gathering the correct forms and documents is essential when preparing to file taxes related to Health Savings Accounts. Keeping these documents organized not only helps in filing but also ensures compliance with IRS regulations. Make sure to review all relevant forms to avoid any complications during the tax process.

The IRS Form 8889 is specifically used for reporting Health Savings Account (HSA) contributions and distributions. Various other forms serve related purposes in the context of health expenses and account management. Here is a list of nine documents that are similar in function or intent to Form 8889:

These documents vary in their specific purpose but share common themes of reporting financial information related to health and other expenses. Each plays a role in helping taxpayers navigate their financial responsibilities effectively.

When filling out the IRS 8889 form, it's important to follow certain guidelines. Here’s a helpful list of things you should and shouldn't do.

The IRS Form 8889 is an essential document for individuals who have Health Savings Accounts (HSAs). However, there are several misconceptions surrounding this form that can lead to confusion. Below is a list of five common misconceptions.

This is incorrect. Anyone with an HSA, regardless of their employment status, may need to file this form to report contributions and distributions.

This is misleading. Form 8889 must be filed each tax year during which you make contributions to or take distributions from your HSA.

This is false. Any contributions made by your employer into your HSA must be reported on Form 8889, regardless of whether they are pre-tax or post-tax.

This is incorrect. While reporting on the form indicates that distributions were for qualified medical expenses, it’s crucial to keep adequate documentation for your records in case of an audit.

This is a misconception. While HSA funds used for qualified medical expenses are tax-free, failure to comply with the IRS guidelines can lead to taxes imposed on distributions that do not meet the qualifications.

Understanding these misconceptions is vital for anyone involved with Health Savings Accounts. Correctly filing Form 8889 can help avoid penalties and ensure compliance with tax laws.

The IRS 8889 form is a crucial document for individuals with Health Savings Accounts (HSAs). Understanding how to fill it out correctly can help maximize your tax benefits. Here are five key takeaways to keep in mind:

By keeping these essential points in mind, you can better navigate the process of completing the IRS 8889 form and ensure that you're making the most of your Health Savings Account.