The IRS 940 form plays a crucial role in the realm of payroll taxes, specifically focusing on the Federal Unemployment Tax Act (FUTA). Employers are required to file this annual form to report their contributions to unemployment insurance. Understanding the nuances of the 940 form is essential for businesses, as it helps ensure compliance with federal regulations and avoids potential penalties. The form captures important information such as the total wages subject to FUTA, the amount of tax owed, and any adjustments from prior years. Additionally, it provides a clear picture of an employer's obligation to support the unemployment system, which is vital for workers who find themselves without a job. Filing the IRS 940 accurately and on time can significantly impact a business's financial standing and its relationship with the IRS. As the deadline approaches, it’s important for employers to gather necessary data and understand the implications of their contributions to unemployment taxes.

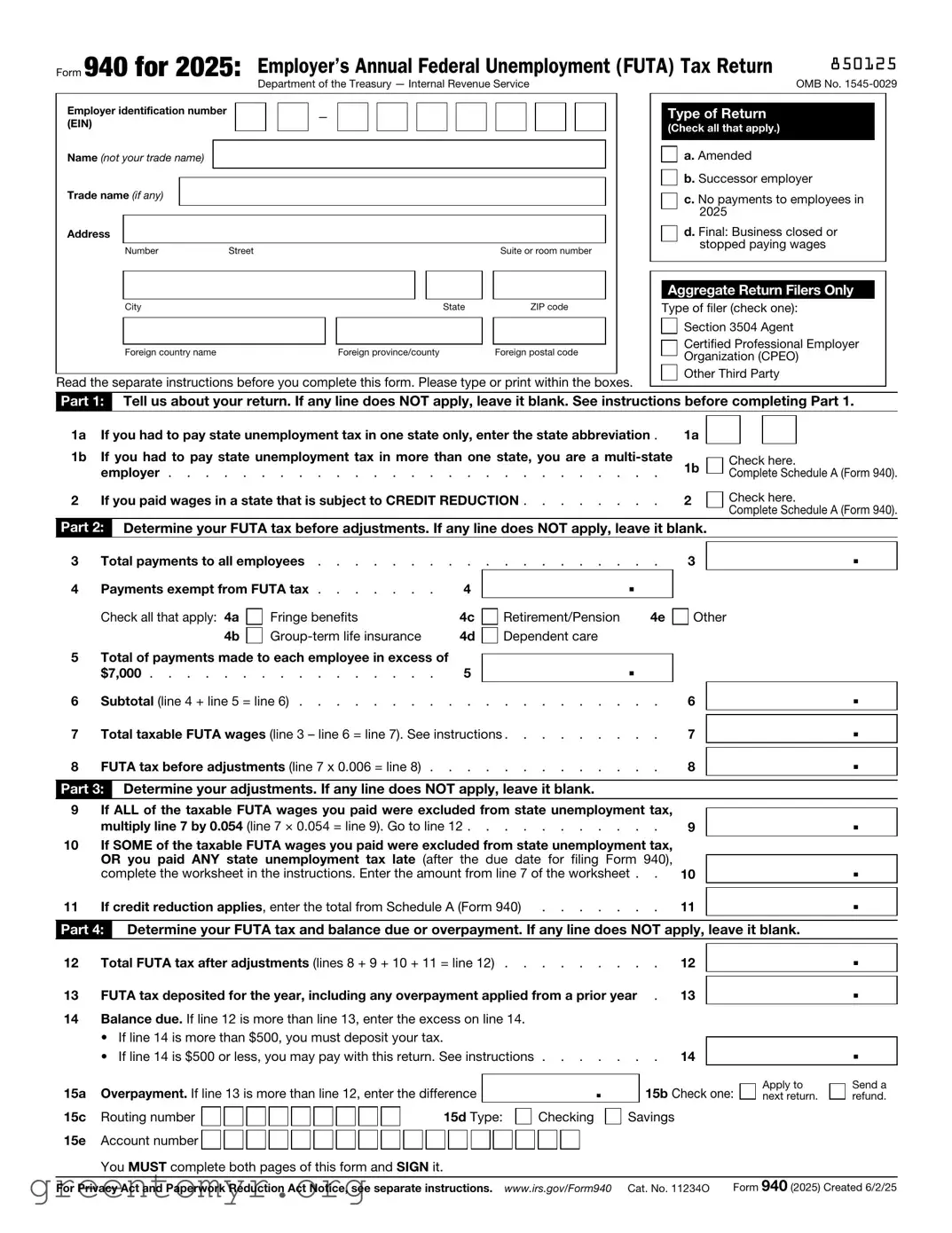

Form 940 for 2025: Employer’s Annual Federal Unemployment (FUTA) Tax Return |

850125 |

|

|

Department of the Treasury — Internal Revenue Service |

OMB No. |

Employer identification number |

|

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

(EIN) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name (not your trade name) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Trade name (if any) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Number |

Street |

|

|

|

|

|

Suite or room number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

|

|

State |

|

ZIP code |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

Foreign country name |

|

|

Foreign province/county |

|

Foreign postal code |

||

Read the separate instructions before you complete this form. Please type or print within the boxes.

Type of Return (Check all that apply.)

a. Amended

b. Successor employer

c. No payments to employees in 2025

d. Final: Business closed or stopped paying wages

Aggregate Return Filers Only

Type of filer (check one): Section 3504 Agent

Certified Professional Employer Organization (CPEO)

Other Third Party

Part 1: Tell us about your return. If any line does NOT apply, leave it blank. See instructions before completing Part 1.

1a |

If you had to pay state unemployment tax in one state only, enter the state abbreviation . |

1b |

If you had to pay state unemployment tax in more than one state, you are a |

|

employer |

2 |

If you paid wages in a state that is subject to CREDIT REDUCTION |

1a

1b

2

Check here.

Complete Schedule A (Form 940).

Check here.

Complete Schedule A (Form 940).

Part 2: Determine your FUTA tax before adjustments. If any line does NOT apply, leave it blank.

3 |

Total payments to all employees |

||

4 |

Payments exempt from FUTA tax |

4 |

|

|

Check all that apply: 4a |

Fringe benefits |

4c |

|

4b |

4d |

|

5 Total of payments made to each employee in excess of

$7,000 . . . . . . . . . . . . . . . . 5

6 Subtotal (line 4 + line 5 = line 6) . . . . . . . . . .

. . . . . . . . .. .

Retirement/Pension 4e Dependent care

.

. . . . . . . . . .

3

Other

6

.

.

7 Total taxable FUTA wages (line 3 – line 6 = line 7). See instructions . . . . . . . . .

8 FUTA tax before adjustments (line 7 x 0.006 = line 8) . . . . . . . . . . . . .

7

8

.

.

Part 3: Determine your adjustments. If any line does NOT apply, leave it blank.

9 |

If ALL of the taxable FUTA wages you paid were excluded from state unemployment tax, |

|

|

|

. |

||

|

multiply line 7 by 0.054 (line 7 × 0.054 = line 9). Go to line 12 |

9 |

|

10 |

If SOME of the taxable FUTA wages you paid were excluded from state unemployment tax, |

|

|

|

OR you paid ANY state unemployment tax late (after the due date for filing Form 940), |

|

|

|

|

. |

|

|

complete the worksheet in the instructions. Enter the amount from line 7 of the worksheet . . |

10 |

|

|

|

|

|

11 |

If credit reduction applies, enter the total from Schedule A (Form 940) |

11 |

. |

|

|

|

|

Part 4: Determine your FUTA tax and balance due or overpayment. If any line does NOT apply, leave it blank.

12 |

Total FUTA tax after adjustments (lines 8 + 9 + 10 + 11 = line 12) |

12 |

. |

|

|

|

|

13 |

FUTA tax deposited for the year, including any overpayment applied from a prior year . |

13 |

. |

14Balance due. If line 12 is more than line 13, enter the excess on line 14.

|

• If line 14 is more than $500, you must deposit your tax. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

14 |

|

|

. |

||||||||||||||||||||||

|

• If line 14 is $500 or less, you may pay with this return. See instructions . . . . |

. . . |

|

|

||||||||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15a |

Overpayment. If line 13 is more than line 12, enter the difference |

|

|

|

. |

|

15b |

Check one: |

Apply to |

Send a |

||||||||||||||||||||||||||||||||

|

|

next return. |

refund. |

|||||||||||||||||||||||||||||||||||||||

15c |

Routing number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15d Type: |

|

|

|

Checking |

Savings |

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

15e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

Account number |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

You MUST complete both pages of this form and SIGN it. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

For Privacy Act and Paperwork Reduction Act Notice, see separate instructions. www.irs.gov/Form940 Cat. No. 11234O |

Form 940 (2025) Created 6/2/25 |

850212

Name (not your trade name) |

Employer identification number (EIN) |

|

– |

Part 5: Report your FUTA tax liability by quarter only if line 12 is more than $500. If not, go to Part 6.

16Report the amount of your FUTA tax liability for each quarter; do NOT enter the amount you deposited. If you had no liability for

a quarter, leave the line blank.

16a 1st quarter (January 1 – March 31) . . . . . . . . . 16a.

|

|

|

|

|

16b |

2nd quarter (April 1 – June 30) |

16b |

. |

|

|

|

|

|

|

16c |

3rd quarter (July 1 – September 30) |

16c |

. |

|

|

|

|

|

|

16d |

4th quarter (October 1 – December 31) |

16d |

. |

|

|

|

|

|

|

17 Total tax liability for the year (lines 16a + 16b + 16c + 16d = line 17) |

17 |

. |

Total must equal line 12. |

|

Part 6: May we speak with your

Do you want to allow an employee, a paid tax preparer, or another person to discuss this return with the IRS? See the instructions for details.

Yes. Designee’s name and phone number

Select a

No.

Part 7: Sign here. You MUST complete both pages of this form and SIGN it.

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete, and that no part of any payment made to a state unemployment fund claimed as a credit was, or is to be, deducted from the payments made to employees. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

Sign your name here

Date

/ /

Print your name here

Print your title here

Best daytime phone

Paid Preparer Use Only

Preparer’s name

Preparer’s signature

Firm’s name (or yours if

Address

City

State

Check if you are

PTIN

Date |

/ |

/ |

EIN

Phone

ZIP code

Page 2 |

Form 940 (2025) |

Form

Purpose of Form

Complete Form

Making Payments With Form 940

To avoid a penalty, make your payment with your 2025 Form 940 only if your FUTA tax for the fourth quarter (plus any undeposited amounts from earlier quarters) is $500 or less. If your total FUTA tax after adjustments (Form 940, line 12) is more than $500, you must make deposits by electronic funds transfer (EFT). An EFT can be made using the Electronic Federal Tax Payment System (EFTPS), IRS Direct Pay, or your IRS business tax account. Don’t use Form

Use Form

that should’ve been deposited, you may be subject to a penalty. See Deposit Penalties in section 11 of Pub. 15.

Specific Instructions

Box

entry space.

Box

Box

•Enclose your check or money order made payable to “United States Treasury.” Be sure to enter your EIN, “Form 940,” and “2025” on your check or money order. Don’t send cash. Don’t staple Form

•Detach Form

Note: You must also complete the entity information above Part 1 on Form 940.

Detach Here and Mail With Your Payment and Form 940.

Form

Department of the Treasury

Internal Revenue Service

1Enter your employer identification number (EIN).

–

Payment Voucher

Don’t staple or attach this voucher to your payment.

2Enter the amount of your payment.

Make your check or money order payable to “United States Treasury.”

OMB No.

2025

Dollars |

Cents |

|

|

3Enter your business name (individual name if sole proprietor). Enter your address.

Enter your city, state, and ZIP code; or your city, foreign country name, foreign province/county, and foreign postal code.

| Fact Name | Details |

|---|---|

| Purpose | The IRS Form 940 is used to report annual Federal Unemployment Tax Act (FUTA) taxes. |

| Filing Deadline | The form is typically due by January 31 of the following year, though it may be extended to February 10 if the employer deposits all FUTA taxes on time. |

| Eligibility | Employers who pay $1,500 or more in wages in any calendar quarter or have one or more employees for at least 20 weeks in a calendar year must file this form. |

| State-Specific Forms | Each state has its own unemployment tax forms governed by state laws, such as the California Unemployment Insurance Code. |

| Penalties | Failure to file Form 940 or pay the taxes owed can result in penalties and interest charges. |

Filling out the IRS 940 form is an important step for employers to report their annual federal unemployment tax. After completing the form, you will need to submit it to the IRS, along with any necessary payments. Follow these steps to ensure accurate completion.

The IRS 940 form is an annual report used by employers to report their Federal Unemployment Tax Act (FUTA) liability. This form is essential for employers who pay wages to employees and is filed with the Internal Revenue Service (IRS). It helps the IRS determine how much unemployment tax an employer owes for the year.

Employers who meet certain criteria must file Form 940. Generally, if you paid $1,500 or more in wages in any calendar quarter during the year or had one or more employees for at least 20 weeks, you are required to file. Additionally, if you are a household employer or a farm employer, you may also need to file.

Form 940 is due by January 31 of the following year. If you are making timely payments of your FUTA taxes, you may have until February 10 to file. It’s important to keep track of these deadlines to avoid penalties and interest.

You can file Form 940 either electronically or by mail. If you choose to file electronically, you can use IRS e-file or authorized e-file providers. If you prefer to file by mail, send the completed form to the address specified in the instructions. Make sure to keep a copy for your records.

Form 940 requires various pieces of information, including:

Ensure that all information is accurate to avoid issues with the IRS.

Failing to file Form 940 can lead to significant penalties. The IRS may impose fines for late filings or for not filing at all. Additionally, not filing can affect your ability to claim FUTA tax credits, which could result in higher tax liabilities.

Yes, if you need to correct any errors on a previously filed Form 940, you can do so by filing Form 940-X, the Amended Employer's Annual Federal Unemployment (FUTA) Tax Return. This form allows you to make necessary adjustments to your original filing.

The FUTA tax rate is currently set at 6.0% on the first $7,000 of each employee’s wages. However, if you pay your state unemployment taxes on time, you may be eligible for a credit of up to 5.4%, effectively reducing the FUTA rate to 0.6%.

You can download Form 940 from the IRS website. The form is available in PDF format, and you can also access the accompanying instructions, which provide detailed guidance on how to complete the form correctly.

If you have additional questions about Form 940, consider consulting a tax professional or visiting the IRS website for more information. The IRS offers resources and guidance that can help clarify any uncertainties regarding your filing obligations.

Filling out the IRS Form 940 can be a daunting task. Many people make mistakes that can lead to delays or even penalties. One common error is incorrect reporting of wages. It's crucial to ensure that the wages reported match the amounts on your payroll records. Discrepancies can trigger audits or additional scrutiny from the IRS.

Another frequent mistake involves miscalculating the Federal Unemployment Tax Act (FUTA) tax. The tax rate can change, and it's essential to apply the correct rate for the tax year in question. Failing to do so can result in underpayment, leading to penalties. Always double-check the current rate before submitting your form.

Many individuals also overlook the importance of signing the form. An unsigned form is considered incomplete and will not be processed. Make it a priority to review your form thoroughly before submission. This simple step can save you time and frustration.

Additionally, some people forget to include any adjustments for prior year credits. If you had any adjustments or credits from previous years, these must be accurately reflected in the current form. Neglecting this can lead to inaccurate tax calculations.

Another mistake is failing to file on time. The deadline for submitting Form 940 is typically January 31 of the following year. Late submissions can incur penalties and interest. Mark your calendar and set reminders to avoid this issue.

Lastly, not keeping copies of submitted forms is a mistake many make. Always retain a copy of your completed Form 940 and any supporting documentation. This practice will help you if questions arise in the future and provide peace of mind.

The IRS 940 form is essential for employers who need to report their annual Federal Unemployment Tax Act (FUTA) liability. However, several other forms and documents are often used in conjunction with the 940 to ensure compliance with federal tax regulations. Below is a list of these important documents.

Understanding these forms and their purposes is vital for maintaining compliance and ensuring that your business meets all tax obligations. Stay organized and proactive to avoid any potential issues with tax reporting and payments.

When filling out the IRS 940 form, which is used to report annual Federal Unemployment Tax Act (FUTA) taxes, it’s important to follow certain guidelines to ensure accuracy and compliance. Here are five things you should and shouldn't do.

By following these guidelines, you can help ensure that your filing process goes smoothly and that you remain compliant with IRS regulations.

The IRS 940 form is an important document for employers, but many misconceptions surround it. Here are ten common misunderstandings about this form:

Understanding these misconceptions can help employers navigate their tax responsibilities more effectively and avoid potential penalties.

Filling out and using the IRS 940 form is an important task for employers. This form is used to report and pay federal unemployment taxes. Here are some key takeaways to keep in mind:

Staying informed about these key points will help ensure compliance and streamline the filing process for the IRS 940 form.