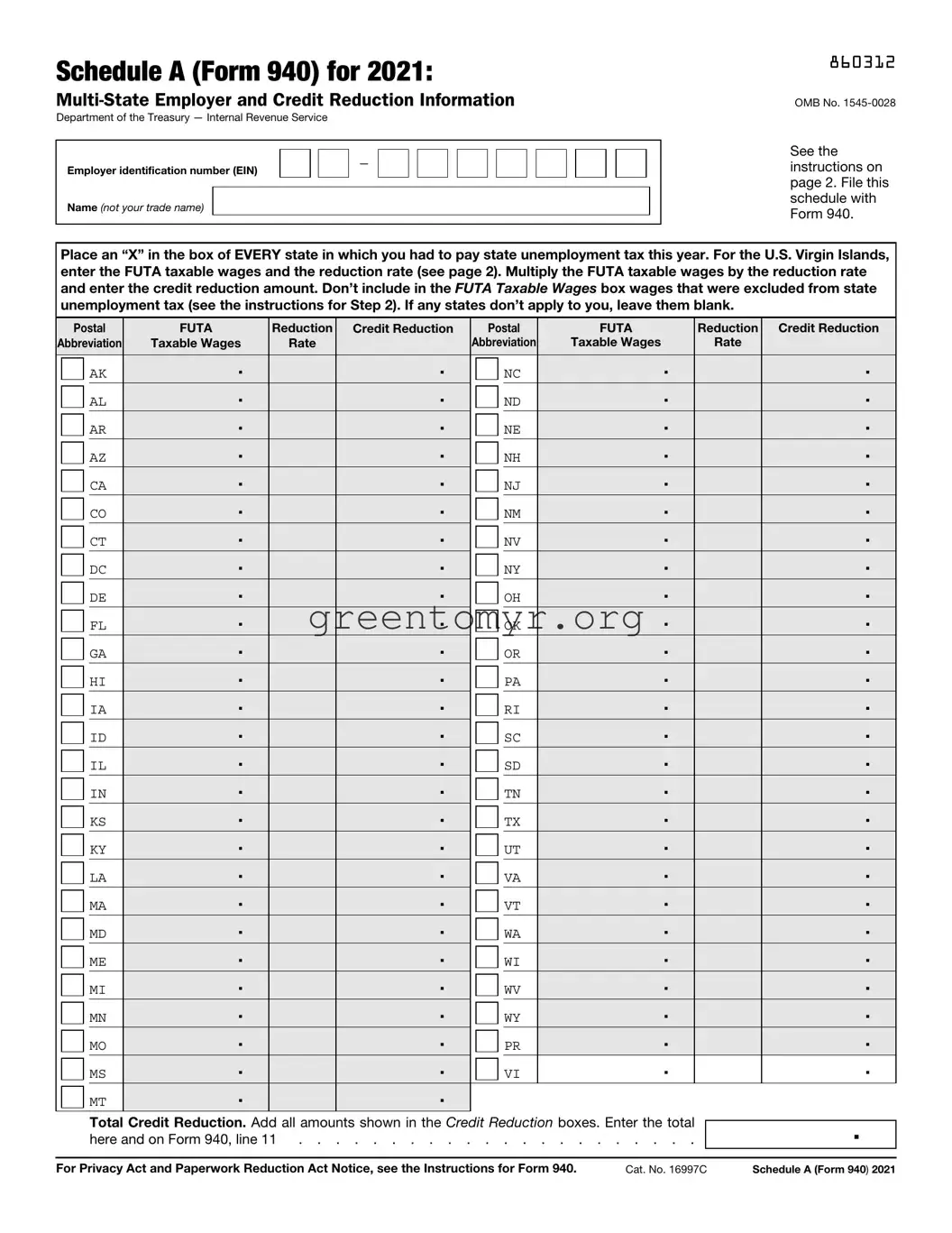

The IRS 940 Schedule A form serves as a crucial component for multi-state employers, offering a structured format to provide essential information regarding federal unemployment tax contributions and any credit reductions applicable under state unemployment tax laws. This form tracks the states in which an employer has paid unemployment taxes, requiring employers to mark each relevant jurisdiction with an “X.” One key aspect is the need to disclose taxable wages subject to state unemployment tax, particularly in states designated as credit reduction locations, such as the U.S. Virgin Islands for certain tax years. Employers should take particular care to differentiate between FUTA taxable wages and those excluded from state taxes. This precision is critical in calculating potential credits that may impact their overall federal tax liability. Additionally, Schedule A necessitates an accurate calculation of any credit reductions, which can occur when FUTA taxable wages intersect with state unemployment taxes. The form includes comprehensive instructions for completion, illustrating how to add credits across multiple states and ensuring that employers are in compliance with federal requirements. Ultimately, properly filling out Schedule A not only aids in maintaining accurate records but also in optimizing tax liabilities.

Schedule A (Form 940) for 2021:

Department of the Treasury — Internal Revenue Service

Employer identification number (EIN) |

|

|

|

— |

|

|

|

|

Name (not your trade name)

860312

OMB No.

See the instructions on page 2. File this schedule with Form 940.

Place an “X” in the box of EVERY state in which you had to pay state unemployment tax this year. For the U.S. Virgin Islands, enter the FUTA taxable wages and the reduction rate (see page 2). Multiply the FUTA taxable wages by the reduction rate and enter the credit reduction amount. Don’t include in the FUTA Taxable Wages box wages that were excluded from state unemployment tax (see the instructions for Step 2). If any states don’t apply to you, leave them blank.

|

Postal |

FUTA |

Reduction |

Credit Reduction |

|

Postal |

FUTA |

Reduction |

Credit Reduction |

||||||

Abbreviation |

Taxable Wages |

Rate |

|

|

Abbreviation |

Taxable Wages |

Rate |

|

|||||||

|

|

|

AK |

|

. |

|

|

. |

|

|

|

NC |

. |

|

. |

|

|

|

|

|

|

|

|||||||||

|

|

|

AL |

|

. |

|

|

. |

|

|

|

ND |

. |

|

. |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

AR |

|

. |

|

|

. |

|

|

|

NE |

. |

|

. |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

AZ |

|

. |

|

|

. |

|

|

|

NH |

. |

|

. |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

CA |

|

. |

|

|

. |

|

|

|

NJ |

. |

|

. |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

CO |

|

. |

|

|

. |

|

|

|

NM |

. |

|

. |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

CT |

|

. |

|

|

. |

|

|

|

NV |

. |

|

. |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

DC |

|

. |

|

|

. |

|

|

|

NY |

. |

|

. |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

DE |

|

. |

|

|

. |

|

|

|

OH |

. |

|

. |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

FL |

|

. |

|

|

. |

|

|

|

OK |

. |

|

. |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

GA |

|

. |

|

|

. |

|

|

|

OR |

. |

|

. |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

HI |

|

. |

|

|

. |

|

|

|

PA |

. |

|

. |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

IA |

|

. |

|

|

. |

|

|

|

RI |

. |

|

. |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

ID |

|

. |

|

|

. |

|

|

|

SC |

. |

|

. |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

IL |

|

. |

|

|

. |

|

|

|

SD |

. |

|

. |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

IN |

|

. |

|

|

. |

|

|

|

TN |

. |

|

. |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

KS |

|

. |

|

|

. |

|

|

|

TX |

. |

|

. |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

KY |

|

. |

|

|

. |

|

|

|

UT |

. |

|

. |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

LA |

|

. |

|

|

. |

|

|

|

VA |

. |

|

. |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

MA |

|

. |

|

|

. |

|

|

|

VT |

. |

|

. |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

MD |

|

. |

|

|

. |

|

|

|

WA |

. |

|

. |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

ME |

|

. |

|

|

. |

|

|

|

WI |

. |

|

. |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

MI |

|

. |

|

|

. |

|

|

|

WV |

. |

|

. |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

MN |

|

. |

|

|

. |

|

|

|

WY |

. |

|

. |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

MO |

|

. |

|

|

. |

|

|

|

PR |

. |

|

. |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

MS |

|

. |

|

|

. |

|

|

|

VI |

. |

|

. |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

MT |

|

. |

|

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Credit Reduction. Add all amounts shown in the Credit Reduction boxes. Enter the total here and on Form 940, line 11 . . . . . . . . . . . . . . . . . . . . . .

.

For Privacy Act and Paperwork Reduction Act Notice, see the Instructions for Form 940. |

Cat. No. 16997C |

Schedule A (Form 940) 2021 |

Instructions for Schedule A (Form 940) for 2021: |

860412 |

|

|

|

|

|

|

Specific Instructions: Completing Schedule A |

|

Step 1. Place an “X” in the box of every state (including the District of Columbia, Puerto Rico, and the U.S. Virgin Islands) in which you had to pay state unemployment taxes this year, even if the state’s credit reduction rate is zero.

Note: Make sure that you have applied for a state reporting number for your business. If you don’t have an unemployment account in a state in which you paid wages, contact the state unemployment agency to receive one. For a list of state unemployment agencies, visit the U.S. Department of Labor’s website at https://oui.doleta.gov/unemploy/agencies.asp.

The table below provides the

|

Postal |

|

Postal |

State |

Abbreviation |

State |

Abbreviation |

|

|

|

|

Alabama |

AL |

Montana |

MT |

Alaska |

AK |

Nebraska |

NE |

Arizona |

AZ |

Nevada |

NV |

Arkansas |

AR |

New Hampshire |

NH |

California |

CA |

New Jersey |

NJ |

Colorado |

CO |

New Mexico |

NM |

Connecticut |

CT |

New York |

NY |

Delaware |

DE |

North Carolina |

NC |

District of Columbia |

DC |

North Dakota |

ND |

Florida |

FL |

Ohio |

OH |

Georgia |

GA |

Oklahoma |

OK |

Hawaii |

HI |

Oregon |

OR |

Idaho |

ID |

Pennsylvania |

PA |

Illinois |

IL |

Rhode Island |

RI |

Indiana |

IN |

South Carolina |

SC |

Iowa |

IA |

South Dakota |

SD |

Kansas |

KS |

Tennessee |

TN |

Kentucky |

KY |

Texas |

TX |

Louisiana |

LA |

Utah |

UT |

Maine |

ME |

Vermont |

VT |

Maryland |

MD |

Virginia |

VA |

Massachusetts |

MA |

Washington |

WA |

Michigan |

MI |

West Virginia |

WV |

Minnesota |

MN |

Wisconsin |

WI |

Mississippi |

MS |

Wyoming |

WY |

Missouri |

MO |

Puerto Rico |

PR |

|

|

U.S. Virgin Islands |

VI |

Credit reduction state. For 2021, the U.S. Virgin Islands (USVI) is the only credit reduction state. The credit reduction rate is 0.033 (3.3%).

Step 2. You’re subject to credit reduction if you paid FUTA taxable wages that were also subject to state unemployment taxes in the USVI.

In the FUTA Taxable Wages box, enter the total FUTA taxable wages that you paid in the USVI. (The FUTA wage base for all states is $7,000.) However, don’t include in the FUTA Taxable Wages box wages that were excluded from state unemployment tax. For example, if you paid $5,000 in FUTA taxable wages in the USVI but $1,000 of those wages were excluded from state unemployment tax, report $4,000 in the FUTA Taxable Wages box.

Note: Don’t enter your state unemployment wages in the FUTA Taxable Wages box.

Enter the reduction rate and then multiply the total FUTA taxable wages by the reduction rate.

Enter your total in the Credit Reduction box at the end of the line.

Step 3. Total credit reduction

To calculate the total credit reduction, add up all of the Credit Reduction boxes and enter the amount in the Total Credit Reduction box.

Then enter the total credit reduction on Form 940, line 11.

Example 1

You paid $20,000 in wages to each of three employees in State A. State A is subject to credit reduction at a rate of 0.033 (3.3%). Because you paid wages in a state that is subject to credit reduction, you must complete Schedule A and file it with Form 940.

Total payments to all employees in State A . . . . . . $60,000

Payments exempt from FUTA tax

(see the Instructions for Form 940) . . . . . . . . . . $0

Total payments made to each employee in

excess of $7,000 (3 x ($20,000 - $7,000)) . . . . . . . $39,000

Total FUTA taxable wages you paid in State A entered in

the FUTA Taxable Wages box ($60,000 - $0 - $39,000) . . . $21,000 Credit reduction rate for State A . . . . . . . . . . 0.033 Total credit reduction for State A ($21,000 x 0.033) . . . . $693.00

|

Don’t include in the FUTA Taxable Wages box wages |

▲ |

|

! |

in excess of the $7,000 wage base for each employee |

subject to state unemployment insurance in the credit |

|

CAUTION |

reduction state. The credit reduction applies only |

|

to FUTA taxable wages that were also subject to state unemployment tax.

In this case, you would write $693.00 in the Total Credit Reduction box and then enter that amount on Form 940, line 11.

Example 2

You paid $48,000 ($4,000 a month) in wages to Mary Smith and no payments were exempt from FUTA tax. Mary worked in State B (not subject to credit reduction) in January and then transferred to State C (subject to credit reduction) on February

1.Because you paid wages in more than one state, you must complete Schedule A and file it with Form 940.

The total payments in State B that aren’t exempt from FUTA tax are $4,000. Since this payment to Mary doesn’t exceed the $7,000 FUTA wage base, the total FUTA taxable wages paid in State B are $4,000.

The total payments in State C that aren’t exempt from FUTA tax are $44,000. However, $4,000 of FUTA taxable wages was paid in State B with respect to Mary. Therefore, the total FUTA taxable wages with respect to Mary in State C are $3,000 ($7,000 (FUTA wage base) - $4,000 (total FUTA taxable wages paid in State B)). Enter $3,000 in the FUTA Taxable Wages box, multiply it by the Reduction Rate, and then enter the result in the Credit Reduction box.

Attach Schedule A to Form 940 when you file your return.

Page 2

| Fact Name | Details |

|---|---|

| Purpose | The Schedule A (Form 940) is for multi-state employers to report state unemployment taxes to the IRS. |

| FUTA Taxable Wages | Employers must include only FUTA taxable wages in the calculation, excluding wages exempt from state unemployment tax. |

| Credit Reduction States | For 2021, the only state with a credit reduction is the U.S. Virgin Islands. The rate is set at 3.3%. |

| Filing Requirement | This schedule must be filed alongside Form 940. Missing it could lead to penalties. |

| Abbreviations | Each state has a unique two-letter postal abbreviation used on the form, aiding in accurate reporting. |

| Calculation of Credit Reduction | The total of all credit reduction amounts must be added and reported. This is essential for accurate tax filings. |

Filling out IRS Form 940 Schedule A is essential for employers who operate in multiple states and need to report specific unemployment tax information. Upon completing the form, it must be submitted alongside Form 940 to ensure compliance with federal regulations. The following steps will guide you through the process of accurately completing Schedule A.

The IRS 940 Schedule A form is a supplemental form that must be filed by multi-state employers. It provides the Internal Revenue Service (IRS) with crucial information about state unemployment taxes and any applicable credit reduction. This form is part of the annual Federal Unemployment Tax Act (FUTA) return, specifically Form 940, and helps businesses report their unemployment tax obligations accurately.

Employers who have paid state unemployment taxes in multiple states during the year must complete Schedule A. This includes those who have employees working in states that have a credit reduction associated with the federal unemployment tax. It is essential to assess if any of the states where wages were paid require this additional reporting.

Completing Schedule A involves several straightforward steps:

Following the instructions carefully will ensure accuracy in your filing.

As of 2021, the only state that is subject to credit reduction is the U.S. Virgin Islands (USVI), with a credit reduction rate of 3.3%. It's important to stay informed about any changes to this status in future tax years.

Reporting FUTA taxable wages accurately is vital for several reasons. First, improper reporting can lead to incorrect tax calculations, potentially resulting in penalties or additional taxes owed. Second, accurate reporting ensures that your business receives proper credit for taxes paid on unemployment, avoiding unnecessary costs.

If you fail to file Schedule A when required, your business may face penalties from the IRS. Additionally, you could miss out on claiming eligible credits or reductions on your unemployment tax obligations. Filing timely and accurately helps protect your business from unnecessary complications.

Yes, seeking assistance is not only allowed, but it is encouraged. You might consider reaching out to a tax professional or accountant familiar with payroll taxes and unemployment reporting. Additionally, the IRS provides resources and instructions on their website that can guide you through the process.

Completing the IRS 940 Schedule A form can be a meticulous task, and many individuals make mistakes during this process. One common error occurs when people fail to mark all applicable states. It is crucial to place an “X” in every box representing a state where state unemployment taxes were paid. Omitting any state can lead to discrepancies in tax reporting, which may result in penalties or delays in processing.

Another frequent mistake is entering incorrect amounts in the FUTA Taxable Wages box. Individuals sometimes fail to deduct wages that are exempt from state unemployment tax. The form requires that only FUTA taxable wages be reported, so it is essential to calculate these figures accurately. Report the total amount after excluding any non-taxable wages to avoid complications with the IRS.

Some filers misunderstand the need for a state reporting number. If state unemployment taxes were paid, it is necessary to have an account with the state’s unemployment agency. Not securing this account can lead to challenges in fulfilling statutory obligations. Consequently, reaching out to the state agency prior to completing the form can help clarify requirements and ensure compliance.

Additionally, individuals occasionally overlook the requirement to add up all credit reduction amounts accurately. Missing this step or failing to keep a correct total can impact the final calculations on Form 940. Taking the time to double-check figures will help ensure that all amounts are correctly reported, avoiding potential issues with tax liabilities.

Finally, one of the biggest mistakes relates to the handling of wages that exceed the FUTA wage base. Filers sometimes count these excess wages in the FUTA Taxable Wages box when they should be aware that only wages up to $7,000 per employee are subject to reporting under FUTA. Understanding this limit is critical, as including excessive amounts can distort the tax figures on the form.

The IRS Form 940 Schedule A is an essential document for multi-state employers, particularly those dealing with credit reductions due to state unemployment taxes. Several other forms and documents complement this schedule, often necessary for a complete tax filing. Below are four other forms commonly used alongside the IRS 940 Schedule A.

Using these forms together helps ensure compliance with federal and state tax obligations. Accurate filing reduces the risk of penalties and ensures employees receive proper benefits.

The IRS Form 940 Schedule A serves a specific purpose in relation to federal unemployment tax for employers. Several other documents share similar functions or features with Schedule A. Here are six such documents:

When completing the IRS 940 Schedule A form, it’s important to be thorough and accurate. Here’s a list of things you should and shouldn’t do to ensure your form is filled out correctly.

Understanding the intricacies of the IRS 940 Schedule A form can help employers avoid common pitfalls. Here are six misconceptions that often arise regarding this important form:

Being aware of these misconceptions can significantly benefit employers in correctly filling out Schedule A, ensuring compliance with federal and state regulations.

The IRS 940 Schedule A form is essential for multi-state employers dealing with state unemployment taxes. Here are key takeaways to understand its use: