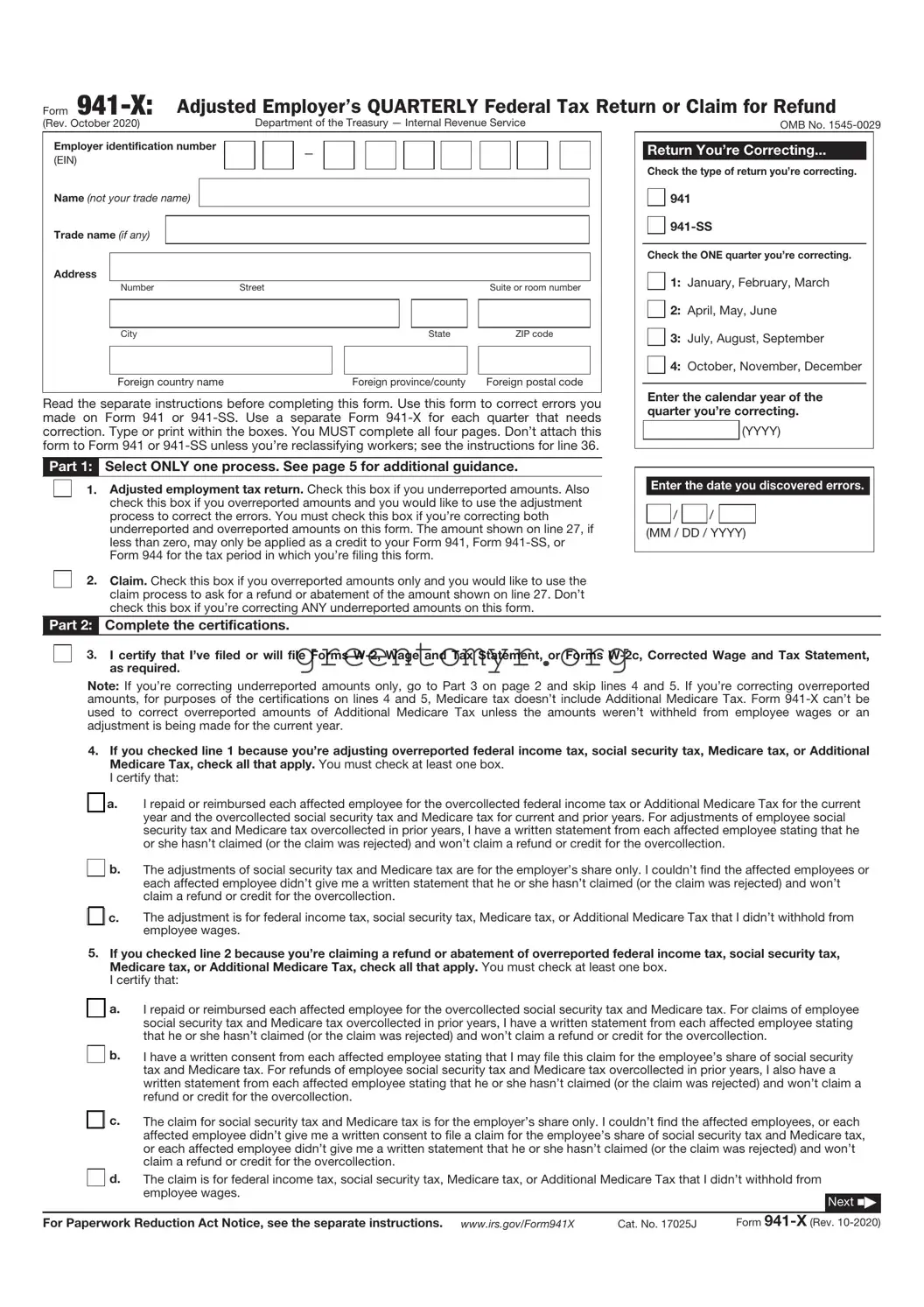

The IRS 941-X form plays a crucial role for employers who need to make corrections to their previously filed IRS Form 941, which reports employment taxes. Understanding how and when to use Form 941-X can help ensure that your payroll information is accurate and compliant with federal regulations. This form can be used to amend or correct errors in reporting wages, tax withheld, or even adjustments related to credits. Whether you've underreported or overreported taxes, Form 941-X allows you to rectify those mistakes. Additionally, the form also provides a process for obtaining refunds if an employer has overpaid their payroll taxes. Filing this form accurately is essential to avoid potential penalties and to maintain a good standing with the IRS, making it an important tool for businesses of all sizes. Being aware of the specific requirements and timelines for submission will help facilitate a smooth correction process, ensuring that all employment tax obligations are met correctly.

Form

(Rev. October 2020) |

Department of the Treasury — Internal Revenue Service |

OMB No. |

Employer identification number |

|

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

(EIN) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name (not your trade name) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Trade name (if any) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Number |

Street |

|

|

|

Suite or room number |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

|

|

State |

|

ZIP code |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Foreign country name |

Foreign province/county |

Foreign postal code |

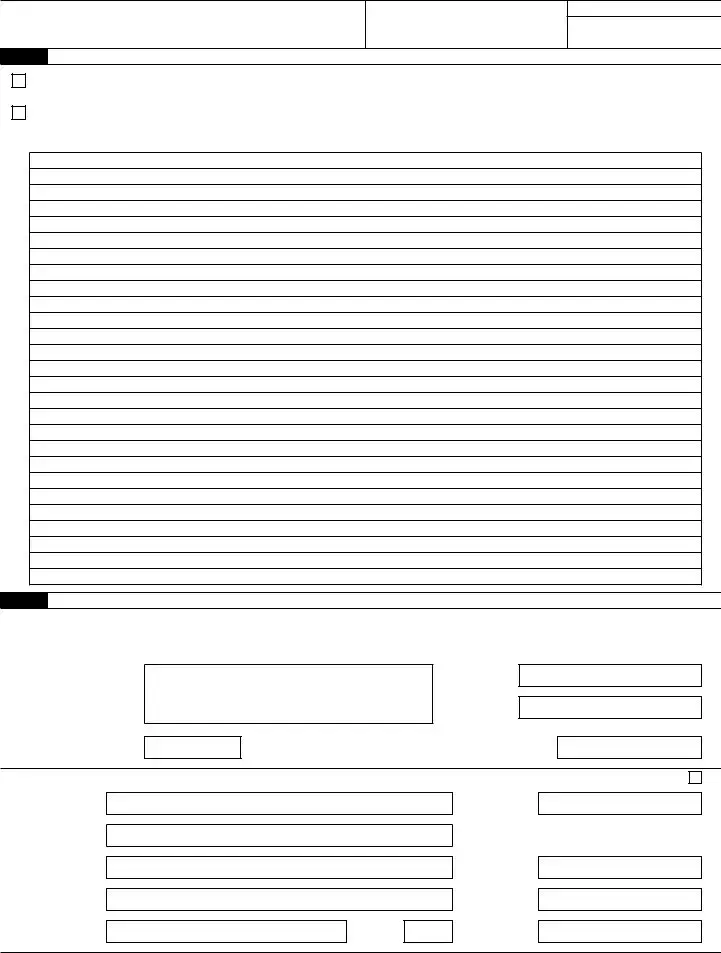

Read the separate instructions before completing this form. Use this form to correct errors you made on Form 941 or

Return You’re Correcting...

Check the type of return you’re correcting.

941

Check the ONE quarter you’re correcting.

1: January, February, March

2: April, May, June

3: July, August, September

4: October, November, December

Enter the calendar year of the quarter you’re correcting.

(YYYY)

Part 1: Select ONLY one process. See page 5 for additional guidance.

1. Adjusted employment tax return. Check this box if you underreported amounts. Also check this box if you overreported amounts and you would like to use the adjustment process to correct the errors. You must check this box if you’re correcting both underreported and overreported amounts on this form. The amount shown on line 27, if less than zero, may only be applied as a credit to your Form 941, Form

2. Claim. Check this box if you overreported amounts only and you would like to use the claim process to ask for a refund or abatement of the amount shown on line 27. Don’t check this box if you’re correcting ANY underreported amounts on this form.

Enter the date you discovered errors.

/ |

|

/ |

(MM / DD / YYYY)

Part 2: Complete the certifications.

3. I certify that I’ve filed or will file Forms

Note: If you’re correcting underreported amounts only, go to Part 3 on page 2 and skip lines 4 and 5. If you’re correcting overreported amounts, for purposes of the certifications on lines 4 and 5, Medicare tax doesn’t include Additional Medicare Tax. Form

4.If you checked line 1 because you’re adjusting overreported federal income tax, social security tax, Medicare tax, or Additional Medicare Tax, check all that apply. You must check at least one box.

I certify that:

a. I repaid or reimbursed each affected employee for the overcollected federal income tax or Additional Medicare Tax for the current year and the overcollected social security tax and Medicare tax for current and prior years. For adjustments of employee social security tax and Medicare tax overcollected in prior years, I have a written statement from each affected employee stating that he or she hasn’t claimed (or the claim was rejected) and won’t claim a refund or credit for the overcollection.

b. The adjustments of social security tax and Medicare tax are for the employer’s share only. I couldn’t find the affected employees or each affected employee didn’t give me a written statement that he or she hasn’t claimed (or the claim was rejected) and won’t claim a refund or credit for the overcollection.

c. The adjustment is for federal income tax, social security tax, Medicare tax, or Additional Medicare Tax that I didn’t withhold from employee wages.

5.If you checked line 2 because you’re claiming a refund or abatement of overreported federal income tax, social security tax, Medicare tax, or Additional Medicare Tax, check all that apply. You must check at least one box.

I certify that:

a. I repaid or reimbursed each affected employee for the overcollected social security tax and Medicare tax. For claims of employee social security tax and Medicare tax overcollected in prior years, I have a written statement from each affected employee stating that he or she hasn’t claimed (or the claim was rejected) and won’t claim a refund or credit for the overcollection.

|

|

b. |

I have a written consent from each affected employee stating that I may file this claim for the employee’s share of social security |

|||

|

|

|

tax and Medicare tax. For refunds of employee social security tax and Medicare tax overcollected in prior years, I also have a |

|||

|

|

|

written statement from each affected employee stating that he or she hasn’t claimed (or the claim was rejected) and won’t claim a |

|||

|

|

|

refund or credit for the overcollection. |

|

|

|

|

|

c. |

The claim for social security tax and Medicare tax is for the employer’s share only. I couldn’t find the affected employees, or each |

|||

|

|

|||||

|

|

|

affected employee didn’t give me a written consent to file a claim for the employee’s share of social security tax and Medicare tax, |

|||

|

|

|

or each affected employee didn’t give me a written statement that he or she hasn’t claimed (or the claim was rejected) and won’t |

|||

|

|

|

claim a refund or credit for the overcollection. |

|

|

|

|

|

d. |

The claim is for federal income tax, social security tax, Medicare tax, or Additional Medicare Tax that I didn’t withhold from |

|||

|

|

|

employee wages. |

|

|

|

|

|

|

|

|

Next N |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

For Paperwork Reduction Act Notice, see the separate instructions. www.irs.gov/Form941X |

Cat. No. 17025J |

Form |

||||

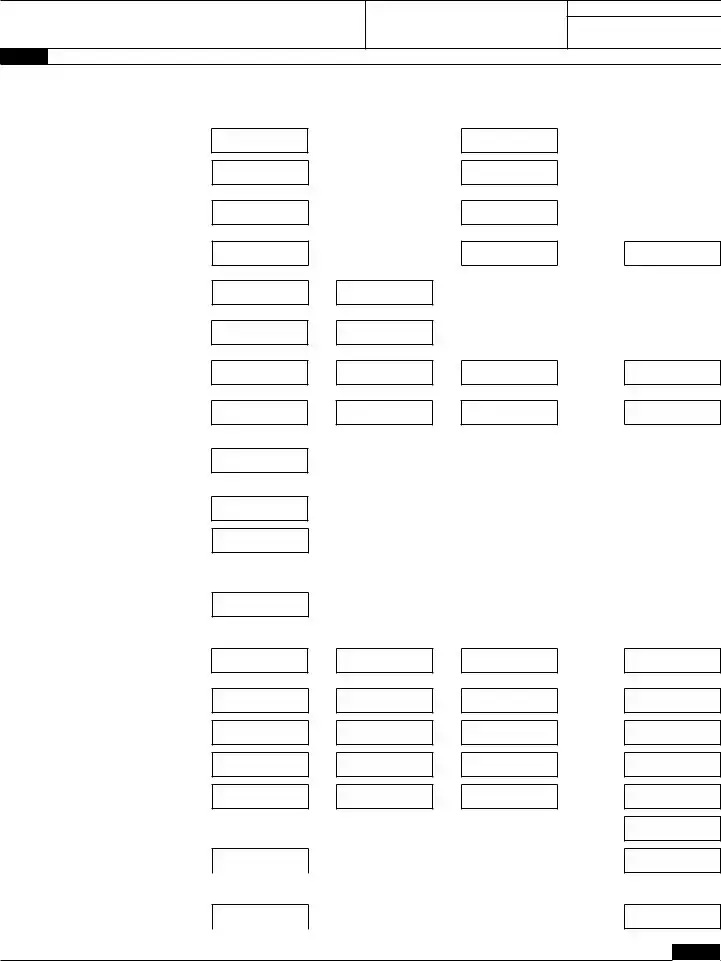

Name (not your trade name)

Employer identification number (EIN)

Correcting quarter |

(1, 2, 3, 4) |

Correcting calendar year (YYYY)

Part 3: Enter the corrections for this quarter. If any line doesn’t apply, leave it blank.

Column 1

Column 2

Column 3 |

Column 4 |

6. |

Wages, tips, and other |

|

compensation (Form 941, line 2) |

7. |

Federal income tax withheld |

|

from wages, tips, and other |

|

compensation (Form 941, line 3) |

8. |

Taxable social security wages |

|

(Form 941 or |

|

Column 1) |

Total corrected amount (for ALL employees)

.

.

.

Amount originally reported or as previously corrected

— (for ALL employees) |

||

— |

|

. |

— |

|

|

|

. |

|

— |

|

|

|

. |

|

=

=

=

=

Difference

(If this amount is a negative number, use a minus sign.)

.

.

.

Tax correction

Use the amount in Column 1 when you prepare your Forms

Copy Column |

|

. |

3 here |

|

|

|

|

|

× 0.124* = |

|

. |

9. |

Qualified sick leave wages |

|

(Form 941 or |

|

Column 1) |

.

— |

|

. |

|

|

|

* If you’re correcting your employer share only, use 0.062. See instructions.

= |

. |

× 0.062 = |

. |

|

10.Qualified family leave wages (Form 941 or

11.Taxable social security tips (Form 941 or

.

.

—

—

.

.

= |

|

|

. |

× |

0.062 = |

|

. |

|

|

|

|||||

= |

|

|

|

|

|

|

|

|

. |

× |

0.124* = |

|

. |

||

|

|

|

|||||

* If you’re correcting your employer share only, use 0.062. See instructions.

12.Taxable Medicare wages & tips (Form 941 or

.

—

.

= |

. |

× 0.029* = |

. |

|

* If you’re correcting your employer share only, use 0.0145. See instructions.

13.Taxable wages & tips subject to Additional Medicare Tax withholding (Form 941 or

14.Section 3121(q) Notice and

15.Tax adjustments (Form 941 or

16.Qualified small business payroll tax credit for increasing research activities (Form 941 or

17.Nonrefundable portion of credit for qualified sick and family leave wages (Form 941 or

.

.

.

.

.

—

—

—

—

—

. |

= |

. |

× 0.009* = |

. |

|

* Certain wages and tips reported in Column 3 shouldn’t be multiplied by 0.009. See instructions.

|

. |

= |

|

. |

Copy Column |

|

. |

|

|

|

|

|

3 here |

|

|||

|

|

= |

|

|

Copy Column |

|

|

|

|

. |

|

. |

|

. |

|||

|

|

|

|

3 here |

|

|||

|

|

|

= |

|

|

See |

|

|

|

. |

|

|

. |

|

. |

||

|

|

|

|

instructions |

|

|||

|

|

|

= |

|

|

See |

|

|

|

. |

|

|

. |

|

. |

||

|

|

|

|

instructions |

|

|||

18.Nonrefundable portion of employee retention credit (Form 941 or

19.Special addition to wages for federal income tax

20.Special addition to wages for social security taxes

21.Special addition to wages for Medicare taxes

22.Special addition to wages for Additional Medicare Tax

.

.

.

.

.

—

—

—

—

—

.

.

.

.

.

=

=

=

=

=

.

.

.

.

.

See instructions

See instructions

See instructions

See instructions

See instructions

.

.

.

.

.

23.Combine the amounts on lines 7 through 22 of Column 4

24.Deferred amount of social

security tax* (Form 941 or |

. |

|

|

|

25.Refundable portion of credit for

qualified sick and family leave |

. |

wages (Form 941 or |

|

|

|

13c) |

|

.

—

—

. . . . . . . . . . . . . . . . . .

|

. |

= |

|

|

. |

See |

|

|

|

instructions |

|||

|

|

= |

|

|

|

See |

|

. |

|

. |

|||

|

|

|

instructions |

|||

.

.

.

Next N

Page 2 |

Form |

Name (not your trade name)

Employer identification number (EIN)

Correcting quarter |

(1, 2, 3, 4) |

Correcting calendar year (YYYY)

Part 3: Enter the corrections for this quarter. If any line doesn’t apply, leave it blank. (continued)

Column 1

Total corrected amount (for ALL employees)

26.Refundable portion of employee

retention credit (Form 941 or |

. |

|

Column 2

Amount originally reported or as previously corrected

—(for ALL employees)

—.

=

=

Column 3

Difference

(If this amount is a negative number, use a minus sign.)

.

See instructions

Column 4

Tax correction

.

27. Total. Combine the amounts on lines 23 through 26 of Column 4 . . . . . . . . . . . . . . . . .

If line 27 is less than zero:

.

•If you checked line 1, this is the amount you want applied as a credit to your Form 941 or

•If you checked line 2, this is the amount you want refunded or abated.

If line 27 is more than zero, this is the amount you owe. Pay this amount by the time you file this return. For information on how to pay, see Amount you owe in the instructions.

28.Qualified health plan expenses allocable to qualified sick leave wages (Form 941 or

.

—

.

=

.

29.Qualified health plan expenses allocable to qualified family leave wages (Form 941 or

30.Qualified wages for the employee retention credit (Form 941 or

31.Qualified health plan expenses allocable to wages reported on Form 941 or

32.Credit from Form

33a. Qualified wages paid March 13 through March 31, 2020, for the employee retention credit (use this line to correct only the second quarter of 2020) (Form 941 or

33b. Deferred amount of the employee share of social security tax included on Form 941 or

34.Qualified health plan expenses allocable to wages reported on Form 941 or

.

.

.

.

.

.

.

—

—

—

—

—

—

—

.

.

.

.

.

.

.

=

=

=

=

=

=

=

.

.

.

.

.

.

.

Next N

Page 3 |

Form |

Name (not your trade name)

Employer identification number (EIN)

Correcting quarter |

(1, 2, 3, 4) |

Correcting calendar year (YYYY)

Part 4: Explain your corrections for this quarter.

35. Check here if any corrections you entered on a line include both underreported and overreported amounts. Explain both

your underreported and overreported amounts on line 37.

36. Check here if any corrections involve reclassified workers. Explain on line 37.

37.You must give us a detailed explanation of how you determined your corrections. See the instructions.

Part 5: Sign here. You must complete all four pages of this form and sign it.

Under penalties of perjury, I declare that I have filed an original Form 941 or Form

✗Sign your name here

Date

/ /

Print your name here

Print your title here

Best daytime phone

Paid Preparer Use Only

Preparer’s name

Preparer’s signature

Firm’s name (or yours if

Check if you’re

PTIN

Date |

/ |

/ |

EIN

Address

Phone

City

State

ZIP code

Page 4 |

Form |

Type of errors you’re correcting

Form

Underreported |

Use the adjustment process to correct underreported amounts. |

|

• Check the box on line 1. |

||

amounts |

||

ONLY |

• Pay the amount you owe from line 27 by the time you file Form |

Overreported amounts

ONLY

The process you use depends on when you file Form

If you’re filing Form

Choose either the adjustment process or the claim process to correct the overreported amounts.

Choose the adjustment process if you want the amount shown on line 27 credited to your Form 941, Form

OR

Choose the claim process if you want the amount shown on line 27 refunded to you or abated. Check the box on line 2.

If you’re filing Form |

You must use the claim process to correct the |

WITHIN 90 days of the |

overreported amounts. Check the box on line 2. |

expiration of the period of |

|

limitations on credit or refund |

|

for Form 941 or Form |

|

BOTH underreported and overreported amounts

The process you use depends on when you file Form

If you’re filing Form

Choose either the adjustment process or both the adjustment process and the claim process when you correct both underreported and overreported amounts.

Choose the adjustment process if combining your underreported amounts and overreported amounts results in a balance due or creates a credit that you want applied to Form 941, Form

•File one Form

•Check the box on line 1 and follow the instructions on line 27.

OR

Choose both the adjustment process and the claim process if you want the overreported amount refunded to you or abated.

File two separate forms.

1.For the adjustment process, file one Form

2.For the claim process, file a second Form

If you’re filing Form

You must use both the adjustment process and the claim process.

File two separate forms.

1.For the adjustment process, file one Form

2.For the claim process, file a second Form

Page 5 |

Form |

| Fact Name | Description |

|---|---|

| Purpose | The IRS Form 941-X is used by employers to correct errors on previously filed Form 941, which reports payroll taxes withheld from employees. This form ensures that the IRS receives accurate payroll tax information. |

| Eligibility | Any employer who discovers an error on their previously submitted Form 941 is eligible to use Form 941-X. This includes mistakes in reporting wages, tax calculations, or employment tax credits. |

| Filing Deadline | Form 941-X must be filed to correct errors within three years of the original Form 941's due date. Timely corrections help avoid penalties and maintain compliance with tax regulations. |

| State-Specific Considerations | While Form 941-X is federal, some states may have their own versions or additional forms related to payroll tax corrections, governed by state-specific employment tax laws. |

Filling out the IRS 941-X form is a straightforward process, but attention to detail is essential. Follow these steps carefully to ensure accuracy. Completing this form allows businesses to claim corrections for previously reported employment tax errors on Form 941.

After sending the form, keep a copy for your records. Be prepared for potential follow-up from the IRS, as they may require additional clarification. Monitoring the status of your amendment can help ensure timely processing.

The IRS 941-X form is a document taxpayers use to correct errors on the previously filed Form 941, which is the Employer’s Quarterly Federal Tax Return. Employers must file Form 941 to report income taxes, Social Security tax, and Medicare tax withheld from employees’ paychecks, as well as their portion of Social Security and Medicare taxes. If an employer realizes they made a mistake on their original Form 941, they should use Form 941-X to rectify it.

Any employer who has filed Form 941 and later identifies errors, whether in wages paid, taxes withheld, or credits claimed, should consider filing Form 941-X. This applies to businesses of all sizes, including those that may employ part-time or seasonal workers. If mistakes were made that affect the reported amounts, using Form 941-X is necessary to correct the record.

Form 941-X can address a variety of mistakes, including:

Essentially, it is for correcting virtually any error found after filing the original Form 941.

To file Form 941-X, follow these steps:

The deadline for filing Form 941-X is generally within three years from the date you filed the original Form 941 or within two years from when the taxes were paid, whichever is later. It is important to keep track of these timelines to ensure that corrections can be made within the permissible period.

Yes, filing Form 941-X may affect your tax liabilities. If the corrections reduce the amount of tax you owe, you may receive a refund. Conversely, if the corrections increase your tax liabilities, you will need to pay the additional amount owed. Properly completing the form is essential, as it impacts your financial responsibilities and compliance with tax laws.

No, Form 941-X is designed to correct errors for one specific quarter at a time. If you need to make corrections for multiple quarters, you must file a separate Form 941-X for each quarter in which an error occurred. This ensures clarity and accuracy in the correction process.

Currently, the IRS does not provide a direct way for taxpayers to check the status of their submitted Form 941-X. However, you can contact the IRS directly for updates. It is beneficial to maintain records of your submission, including tracking numbers if you sent it by mail, to have information handy when inquiring about the status.

Filling out the IRS 941-X form, which is used to amend quarterly payroll tax returns, can be a complex process. Mistakes are common, and each error can lead to complications for both employers and the IRS. Here are eight frequent mistakes people make when completing this form.

First, many individuals overlook the importance of providing accurate taxpayer identification information. Errors in the Employer Identification Number (EIN) can result in significant delays and may even cause the IRS to reject the form. Ensuring that this number is correct is crucial for proper processing.

Another common mistake involves failing to thoroughly read the instructions that accompany the 941-X form. The IRS provides detailed guidance on how to complete each section. Neglecting to review these instructions can lead to omissions or incorrect entries, ultimately complicating the amendment process.

People often forget to report all corrected amounts. If you amend earlier reported wages, taxes withheld, or credits, it is essential to accurately reflect these changes. Leaving out any adjustments creates discrepancies that can trigger audits or further inquiries from the IRS.

Additionally, errors in the calculation of payroll taxes are not uncommon. Individuals may mistakenly calculate the tax amounts owed when amending their returns. Simple addition or subtraction mistakes can lead to overpayments or underpayments, causing future complications.

It is also crucial to remember that the IRS 941-X form must be filed for the correct quarter. Submitting an amendment for the wrong quarter can create confusion and may result in additional penalties. Always double-check the tax period you are amending before submitting.

Another mistake involves failing to provide adequate documentation. Supporting documents, such as proof of tax payments or payroll records, help substantiate the claims made in the 941-X. Without these documents, the IRS may seek further clarification, delaying the process.

People frequently neglect to sign and date the form. While it may seem like a minor detail, a missing signature can halt the processing of an amendment. Ensure that all necessary signatures are present before submission.

Finally, many fail to keep copies of the amended form and any submitted documents. Retaining a record of what was sent helps protect you in case of future inquiries. This missing documentation can be a considerable setback if you need to refer back to the original amendment.

By recognizing these common mistakes and taking proactive steps to avoid them, individuals can ensure a smoother experience when amending their payroll tax returns with the IRS 941-X form.

The IRS 941-X form is used by employers to correct errors made on previously filed Form 941, which reports employment taxes. However, several other documents often accompany this form to ensure compliance with tax regulations and to provide a clearer picture of an employer's tax situation. Below are some important forms and documents that are commonly used alongside the IRS 941-X.

Using these forms and documents in conjunction with the IRS 941-X can help clarify any corrections needed and support accurate reporting of employment taxes. Each of these forms addresses different aspects of payroll and tax reporting, making them crucial for employers to manage their tax responsibilities effectively.

The IRS 941-X form is designed to allow employers to correct errors on previously filed Form 941. Several other IRS forms serve similar purposes in various contexts. Here’s a list of documents that share similarities with the IRS 941-X:

When completing the IRS 941-X form, keep these important points in mind to ensure accuracy and compliance.

Following these guidelines can help minimize errors and streamline your filing process.

The IRS 941-X form is a critical tool for employers who need to correct errors on their previously filed IRS Form 941. However, there are many misconceptions surrounding this form. Understanding the truth behind these myths can help you navigate the correction process more efficiently.

This is not entirely true. While the 941-X is primarily for correcting payroll tax-related inaccuracies, it can also be used to amend employee tax liabilities or any other information reported on Form 941.

This is a common misunderstanding. If you realize there is an error after filing your original Form 941, you don’t need to submit a new one. Instead, you can simply file Form 941-X to make the necessary corrections.

While there is a time frame to consider, the specifics can vary. Generally, you should file Form 941-X within three years from the due date of the original return to ensure you receive any potential refund.

This isn’t quite accurate. Minor errors that do not impact tax liability may not need a form to be filed. It is advisable to review the nature of the error before deciding on this course of action.

Currently, the IRS does not allow electronic filing for Form 941-X. This means that you will need to complete the form and send it through traditional mail.

This is misleading. You can submit multiple 941-X forms for a single quarter, especially if you discover additional errors after filing one.

This misconception arises from the complexity of the form itself. In reality, any employer, regardless of size, may find it necessary to file Form 941-X when corrections are needed.

While the form can appear daunting at first glance, it is designed to be accessible. With careful attention to detail and proper instructions, many employers can complete it without professional help.

This is a significant oversimplification. While you may correct errors that could lead to a refund, the IRS will review your submission. A refund is not guaranteed simply by filing the form.

Understanding these misconceptions can make the process of addressing payroll tax errors much easier. Take the time to familiarize yourself with Form 941-X, and consult with a tax professional if you need further guidance.

When filling out and using the IRS 941-X form, certain key points can help ensure an accurate process. Consider the following important takeaways:

These points serve as a reminder of the important considerations when addressing tax form corrections. Thorough preparation can lead to a smoother experience and minimize potential complications.