The IRS 943 form is particularly significant for agricultural employers who pay their workers in agricultural operations. It serves as a means for reporting annual payroll taxes specifically related to wages paid to farm employees. This form highlights the employer's responsibilities, ensuring compliance with federal tax regulations. Key information includes total wages paid, the number of employees, and the amount withheld for social security and Medicare taxes. Additionally, the IRS 943 form is notable for its utility in calculating credits for hiring seasonal or temporary agricultural workers. Completing this form accurately is essential for employers to avoid potential penalties, and it plays a crucial role in determining the overall tax obligations tied to farm employment. Understanding the nuances of the IRS 943 form can greatly assist agricultural businesses in fulfilling their tax responsibilities while also recognizing benefits available to them.

Form 943 |

Employer’s Annual Federal Tax Return for Agricultural Employees |

OMB No. |

|||||||||||

|

|

|

|

||||||||||

|

2019 |

|

|||||||||||

Department of the Treasury |

Go to www.irs.gov/Form943 for instructions and the latest information. |

|

|

|

|||||||||

Internal Revenue Service |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name (as distinguished from trade name) |

|

Employer identification number (EIN) |

|

|

|

|

|

||||

|

Type |

|

|

|

|

|

|

|

|

|

|

|

|

|

or |

Trade name, if any |

|

|

|

|

|

|

|

If address is |

|||

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

different from |

||||

|

Address (number and street) |

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

prior return, |

|

||

|

|

|

|

|

|

|

|

|

|

check here. |

|

||

|

|

City or town, state or province, country, and ZIP or foreign postal code |

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

If you don’t have to file returns in the future, check here |

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|||

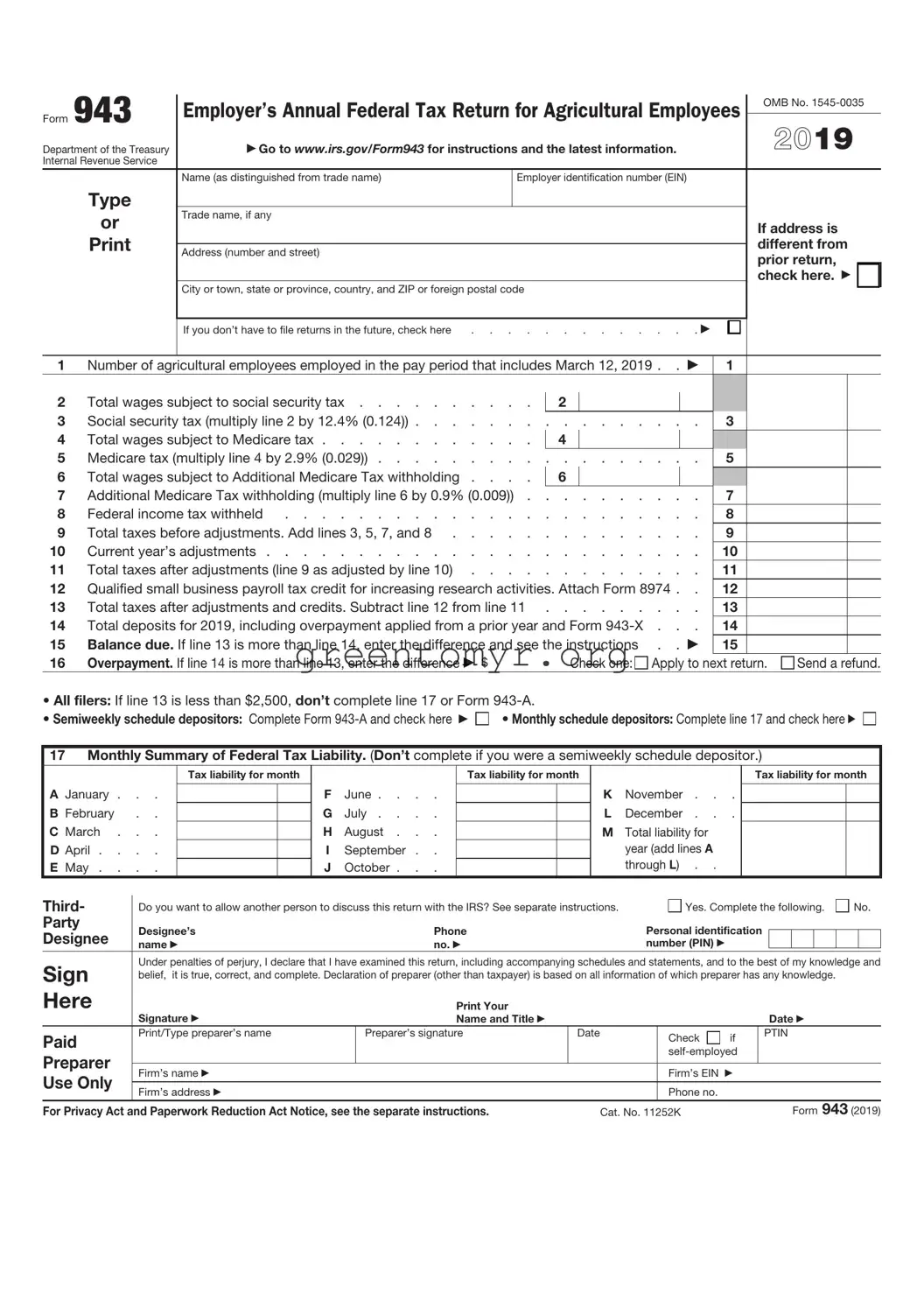

1 |

Number of agricultural employees employed in the pay period that includes March 12, 2019 . . |

1 |

|

|

|

|

|||||||

2 |

Total wages subject to social security tax |

. . |

|

2 |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

||||||

3 |

Social security tax (multiply line 2 by 12.4% (0.124)) |

3 |

|

|

|

|

|||||||

4 |

Total wages subject to Medicare tax |

. . |

|

4 |

|

|

|

|

|

|

|

||

5 |

Medicare tax (multiply line 4 by 2.9% (0.029)) |

5 |

|

|

|

|

|||||||

6 |

Total wages subject to Additional Medicare Tax withholding . . |

. . |

|

6 |

|

|

|

|

|

|

|

||

7 |

Additional Medicare Tax withholding (multiply line 6 by 0.9% (0.009)) |

7 |

|

|

|

|

|||||||

8 |

Federal income tax withheld |

8 |

|

|

|

|

|||||||

9 |

Total taxes before adjustments. Add lines 3, 5, 7, and 8 |

9 |

|

|

|

|

|||||||

10 |

Current year’s adjustments |

10 |

|

|

|

|

|||||||

11 |

Total taxes after adjustments (line 9 as adjusted by line 10) |

11 |

|

|

|

|

|||||||

12 |

Qualified small business payroll tax credit for increasing research activities. Attach Form 8974 . . |

12 |

|

|

|

|

|||||||

13 |

Total taxes after adjustments and credits. Subtract line 12 from line 11 |

13 |

|

|

|

|

|||||||

14 |

Total deposits for 2019, including overpayment applied from a prior year and Form |

14 |

|

|

|

|

|||||||

15 |

Balance due. If line 13 is more than line 14, enter the difference and see the instructions . . |

15 |

|

|

|

|

|||||||

16 |

Overpayment. If line 14 is more than line 13, enter the difference $ |

|

|

|

Check one: Apply to next return. |

Send a refund. |

|||||||

• All filers: If line 13 is less than $2,500, don’t complete line 17 or Form |

|

|

|

|

|

|

|

|

|

||||

• Semiweekly schedule depositors: Complete Form |

• Monthly schedule depositors: Complete line 17 and check here |

||||||||||||

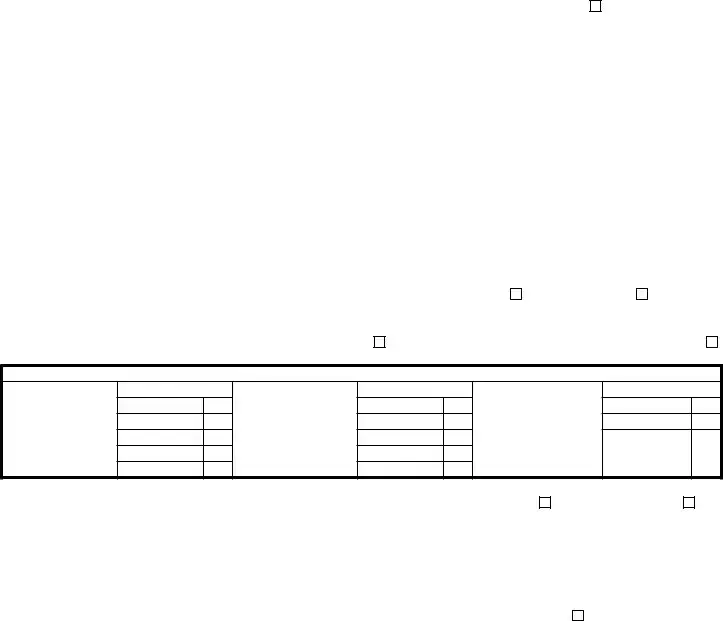

17Monthly Summary of Federal Tax Liability. (Don’t complete if you were a semiweekly schedule depositor.)

A January . . .

B February . . C March . . .

D April . . . .

E May . . . .

Tax liability for month

F |

June . . . . |

G |

July . . . . |

H |

August . . . |

I |

September . . |

J |

October . . . |

Tax liability for month

K November . . .

L December . . .

MTotal liability for year (add lines A

through L) . .

Tax liability for month

Third- |

Do you want to allow another person to discuss this return with the IRS? See separate instructions. |

|

Yes. Complete the following. |

No. |

|||||||||

Party |

Designee’s |

Phone |

|

Personal identification |

|

|

|

|

|

|

|||

Designee |

name |

no. |

|

number (PIN) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

Sign |

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and |

||||||||||||

belief, it is true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge. |

|

|

|||||||||||

Here |

Signature |

Print Your |

|

|

|

|

|

|

|

|

|

|

|

|

Name and Title |

|

|

|

|

|

|

Date |

|

|

|||

Paid |

Print/Type preparer’s name |

Preparer’s signature |

Date |

|

Check |

if |

|

PTIN |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|||

Preparer |

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Firm’s name |

|

|

|

Firm’s EIN |

|

|

|

|

|

|

|

|

|

Use Only |

|

|

|

|

|

|

|

|

|

|

|

||

Firm’s address |

|

|

|

Phone no. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

For Privacy Act and Paperwork Reduction Act Notice, see the separate instructions. |

Cat. No. 11252K |

|

|

|

|

Form 943 (2019) |

|||||||

Form

Purpose of Form

Complete Form

Making Payments With Form 943

To avoid a penalty, make your payment with your 2019 Form 943 only if:

•Your total taxes for the year (Form 943, line 13) are less than $2,500 and you’re paying in full with a timely filed return, or

Specific Instructions

Box

Box

Box

•You’re a monthly schedule depositor making a payment in accordance with the Accuracy of Deposits Rule. See section 7 of Pub. 51 for details. In this case, the amount of your payment may be $2,500 or more.

Otherwise, you must make deposits by electronic funds transfer. See section 7 of Pub. 51 for deposit instructions. Don’t use Form

FUse Form

CAUTION Form 943 that should’ve been deposited, you may be subject to a penalty. See Deposit Penalties in section 7 of Pub. 51.

•Enclose your check or money order made payable to “United States Treasury.” Be sure to enter your EIN, “Form 943,” and “2019” on your check or money order. Don’t send cash. Don’t staple Form

•Detach Form

Note: You must also complete the entity information above line 1 on Form 943.

Detach Here and Mail With Your Payment and Form 943. |

||||||||||

Form |

|

|

|

|

Payment Voucher |

|

OMB No. |

|||

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

Department of the Treasury |

|

|

|

Don’t staple this voucher or your payment to Form 943. |

|

|

2019 |

|||

Internal Revenue Service |

|

|

|

|

|

|

|

|

||

1 Enter your employer identification number (EIN). |

2 |

|

Enter the amount of your payment . . . |

|

|

Dollars |

|

Cents |

||

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

Make your check or money order payable to “United States Treasury” |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

|

Enter your business name (individual name if sole proprietor). |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Enter your address. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Enter your city or town, state or province, country, and ZIP or foreign postal code. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Fact Name | Description |

|---|---|

| Purpose of IRS 943 | The IRS 943 form is used by employers to report annual federal income tax withheld from the wages of agricultural workers. |

| Who Must File | Farmers and agricultural employers who pay wages to farm workers and have withheld taxes from those wages must file this form. |

| Filing Deadline | The IRS 943 form is typically due by January 31 of the following year. |

| Payment Requirements | Employers must make appropriate payments throughout the year. These might include quarterly estimated taxes. |

| State-Specific Considerations | Some states require specific forms in addition to the IRS 943. For example, California requires the DE 9 and DE 9C to report wages and taxes for agricultural workers. |

| Importance of Accurate Reporting | Accurate reporting on the IRS 943 helps ensure compliance with federal tax laws and can prevent penalties or audits from the IRS. |

Once you have collected the necessary information and documents, you can begin to fill out the IRS 943 form. This process involves entering details regarding your employment, taxes withheld, and other relevant financial information. Careful attention to each section will ensure that your form is filled out accurately.

After completing these steps, your IRS 943 form will be ready for submission. Be sure to keep a copy for your records before mailing it to the appropriate IRS address according to the instructions provided on the form.

IRS Form 943 is an essential document used by employers in the agricultural sector to report income tax withheld and FICA taxes for their farmworkers. This annual form helps farmers comply with federal tax laws by summarizing their payroll information, including wages paid and taxes withheld, for the year.

Employers who pay wages to farmworkers must file Form 943. Specifically, this applies to those who have employees working in agriculture, such as crop production, raising livestock, or other related activities. If you employ agricultural workers and your payroll exceeds certain thresholds, you are required to complete and submit this form.

Form 943 is typically due by January 31 of the year following the tax year it covers. For example, for the 2023 tax year, the form must be filed by January 31, 2024. If January 31 falls on a weekend or holiday, the due date is extended to the next business day. Timely submission is crucial to avoid penalties.

When completing Form 943, several key pieces of information are required:

Failing to file Form 943 by the deadline can result in substantial penalties. These penalties can vary depending on how late the form is filed and whether you owe taxes. Generally, the IRS imposes a penalty for late filing, which could be up to 5% of the unpaid tax for each month or part of a month that the return is late, up to a maximum of 25%. Additionally, interest may accrue on any unpaid taxes until they are paid in full. To avoid these consequences, timely submission is strongly advised.

Filling out the IRS 943 form can be challenging. Many people trip over common mistakes that can lead to complications down the line. One frequent error occurs with the employer’s identification number (EIN). Failing to enter the correct EIN not only causes delays but can also result in penalties. Always double-check this critical piece of information.

Another mistake is neglecting to report all wages. If someone forgets to include specific wages paid to seasonal farmworkers, it can lead to inaccuracies in tax calculations. Every bit of information is essential. Ensure all figures are accounted for completely.

People often miss the deadlines for submission. The IRS has strict timelines, and submitting the form late incurs penalties. Mark your calendar well in advance. This proactive measure helps avoid last-minute rushes or forgetfulness.

Using incorrect codes for occupational classifications is a common issue as well. These codes help in determining tax obligations for different types of farm work. Using the wrong code can lead to tax miscalculations that may require additional forms of correction later.

Many also underestimate the importance of signing the form. A signature is critical for validating the information provided. Omitting this could postpone processing and lead to challenges you don’t want to deal with.

Another common blunder is overlooking the importance of reviewing the entire form before submission. Taking the time to go over everything before sending can reveal simple mistakes or oversights that, if left uncorrected, could cause significant problems.

Failure to include all necessary attachments is another area of concern. Some people forget that certain documents must accompany the IRS 943 form. Ensure you are familiar with all requirements and gather the necessary paperwork to avoid this issue.

Lastly, not seeking professional help when needed can be a significant mistake. Tax laws can be complicated. If you’re unsure about certain aspects, consider consulting with a tax professional. Taking this step can save you time and money in the long run.

The IRS Form 943 is essential for agricultural employers who need to report income taxes withheld from their employees’ wages. While submitting this form, various other documents are often necessary to ensure accurate reporting and compliance with tax regulations. Below are five important forms and documents that frequently accompany the IRS 943. Understanding these forms is crucial for agricultural businesses managing payroll and tax responsibilities.

Collectively, these forms and documents work together, ensuring that agricultural businesses meet their tax obligations effectively. By understanding each of these components, employers can maintain compliance while minimizing errors in reporting to the IRS.

The IRS Form 943 is used primarily by agricultural employers to report income taxes withheld from employees and the employer's share of Social Security and Medicare taxes. It has certain similarities with other IRS forms designed for reporting various types of employment-related taxes. Below are seven documents that share similarities with Form 943:

The IRS 943 form is essential for agricultural employers, but misconceptions about it can lead to mistakes. Here are ten of those misconceptions, clarified to help better understand the form's purpose and requirements.

Understanding these misconceptions can lead to more accurate and compliant filing of the IRS 943 form. Addressing each point can help employers navigate their responsibilities with confidence.

The IRS Form 943 is specifically designed for agricultural employers to report wages paid to employees and the taxes withheld. Below are key takeaways regarding the form: