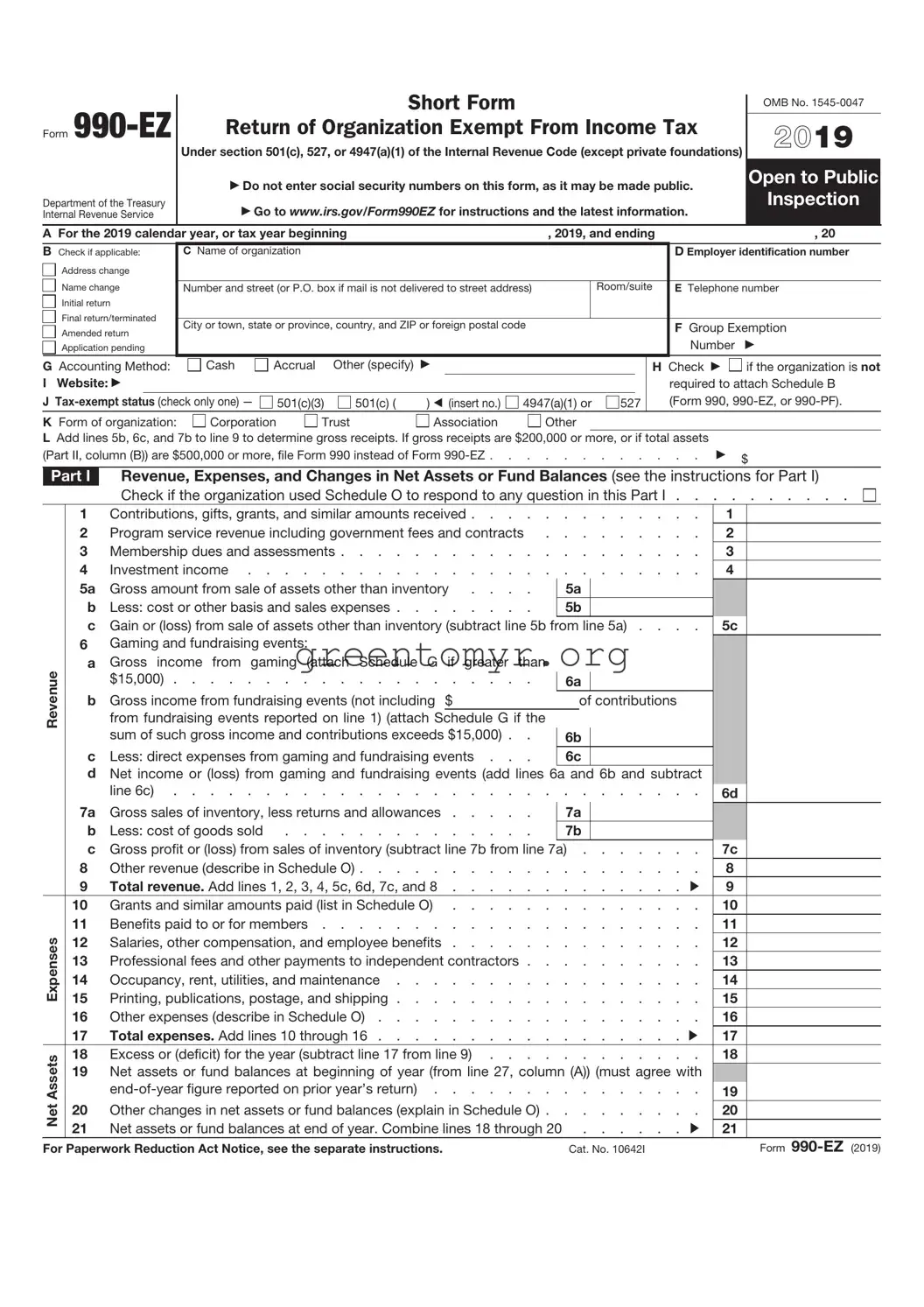

Navigating the world of nonprofit tax filings can be daunting, but understanding the IRS 990-EZ form simplifies that process significantly for many organizations. This streamlined version of the more comprehensive 990 allows smaller tax-exempt entities to report their financial activities and maintain compliance with federal regulations. The form includes essential sections that cover revenue sources, expenses, and changes in net assets, providing a clear snapshot of an organization’s financial health. Furthermore, it facilitates transparency by requiring disclosures about key personnel, governance practices, and contributions received. By filing the 990-EZ, nonprofits not only fulfill their obligation to the IRS but also enhance their credibility within their communities and among potential donors. If you’re involved with a qualifying organization, getting familiar with this form is crucial, as it serves not just as a tax document but as a vital tool in maintaining trust and accountability in your nonprofit’s mission.

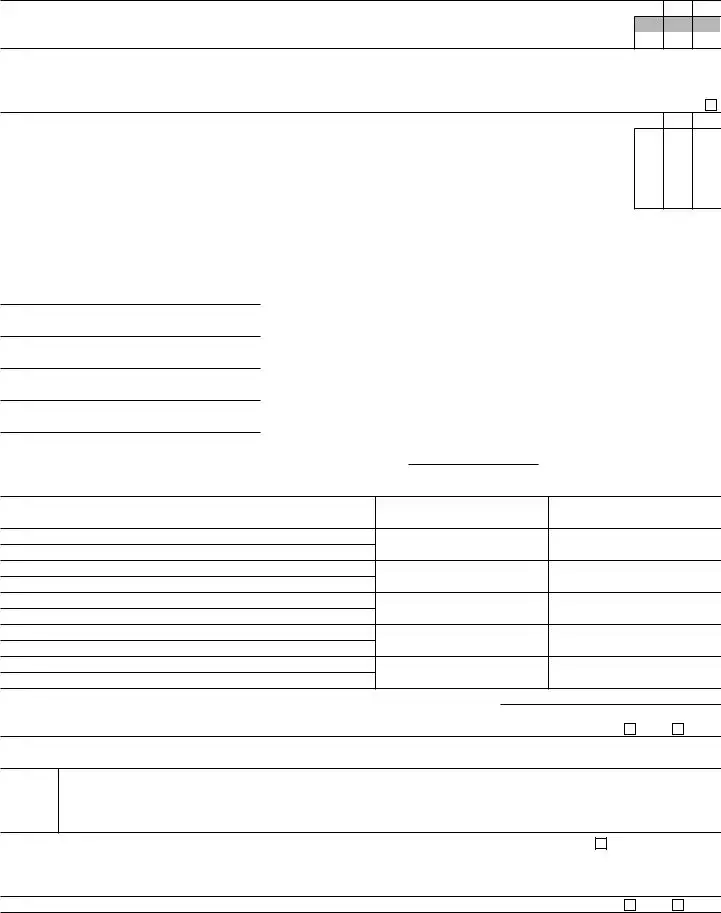

Form

Department of the Treasury Internal Revenue Service

Short Form

Return of Organization Exempt From Income Tax

Under section 501(c), 527, or 4947(a)(1) of the Internal Revenue Code (except private foundations)

Do not enter social security numbers on this form, as it may be made public. Go to www.irs.gov/Form990EZ for instructions and the latest information.

OMB No.

2019

Open to Public

Inspection

A For the 2019 calendar year, or tax year beginning |

, 2019, and ending |

, 20 |

||

B Check if applicable: |

C Name of organization |

|

|

D Employer identification number |

Address change |

|

|

|

|

|

|

|

|

|

Name change |

Number and street (or P.O. box if mail is not delivered to street address) |

|

Room/suite |

E Telephone number |

Initial return |

|

|

|

|

Final return/terminated |

|

|

|

|

City or town, state or province, country, and ZIP or foreign postal code |

|

|

F Group Exemption |

|

Amended return |

|

|

||

|

|

|

Number |

|

Application pending |

|

|

|

|

G Accounting Method: |

Cash |

Accrual |

Other (specify) |

|

|

|

|

|

|

I Website: |

|

|

|

|

|

|

|

|

|

J |

501(c)(3) |

501(c) ( |

) (insert no.) |

4947(a)(1) or |

527 |

||||

H Check |

if the organization is not |

required to attach Schedule B (Form 990,

K Form of organization: |

Corporation |

Trust |

Association |

Other |

LAdd lines 5b, 6c, and 7b to line 9 to determine gross receipts. If gross receipts are $200,000 or more, or if total assets

(Part II, column (B)) are $500,000 or more, file Form 990 instead of Form |

$ |

|

Part I Revenue, Expenses, and Changes in Net Assets or Fund Balances (see the instructions for Part I)

Check if the organization used Schedule O to respond to any question in this Part I . . . . . . . . . .

Revenue

Net Assets Expenses

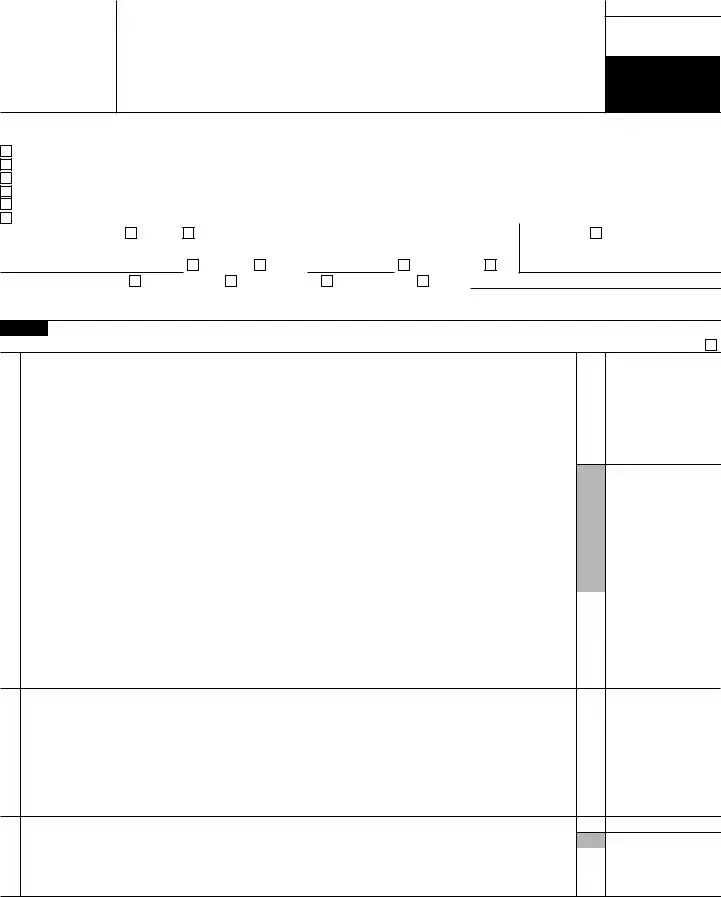

1 |

Contributions, gifts, grants, and similar amounts received . . . . |

. . . . . . . . . |

1 |

|

||

2 |

Program service revenue including government fees and contracts |

. . . . . . . . . |

2 |

|

||

3 |

Membership dues and assessments |

. . . . . . . . . |

3 |

|

||

4 |

Investment income |

. . . . . . . . . |

4 |

|

||

5a |

Gross amount from sale of assets other than inventory . . . . |

|

5a |

|

|

|

b |

Less: cost or other basis and sales expenses |

|

5b |

|

|

|

c |

Gain or (loss) from sale of assets other than inventory (subtract line 5b from line 5a) . . . . |

5c |

||||

6Gaming and fundraising events:

aGross income from gaming (attach Schedule G if greater than

|

$15,000) |

6a |

|

||

b |

Gross income from fundraising events (not including $ |

of contributions |

|||

|

from fundraising events reported on line 1) (attach |

Schedule G if the |

|

|

|

|

sum of such gross income and contributions exceeds $15,000) . . |

6b |

|

||

c |

Less: direct expenses from gaming and fundraising events . . . |

6c |

|

||

dNet income or (loss) from gaming and fundraising events (add lines 6a and 6b and subtract

|

line 6c) |

. . . . . . . . |

|

6d |

|

|

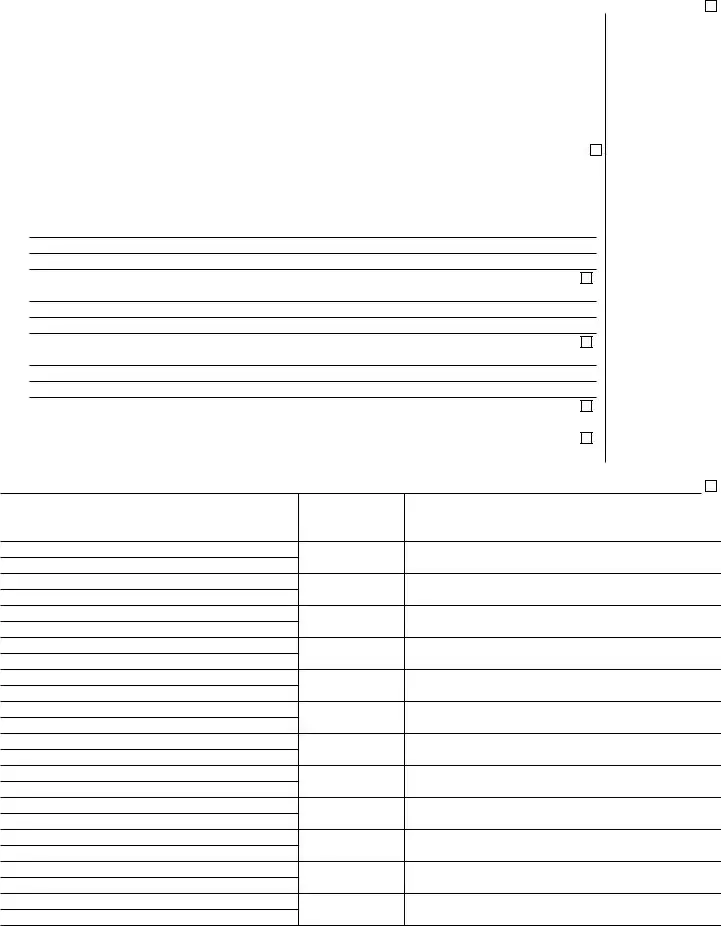

7a |

Gross sales of inventory, less returns and allowances |

7a |

|

|

|

|

b |

Less: cost of goods sold |

7b |

|

|

|

|

c |

Gross profit or (loss) from sales of inventory (subtract line 7b from line 7a) |

7c |

|

|||

8 |

Other revenue (describe in Schedule O) |

. . . . . . . . |

|

8 |

|

|

9 |

Total revenue. Add lines 1, 2, 3, 4, 5c, 6d, 7c, and 8 |

. . . . . . . |

|

9 |

|

|

10 |

Grants and similar amounts paid (list in Schedule O) |

. . . . . . . . |

|

10 |

|

|

11 |

Benefits paid to or for members |

. . . . . . . . |

|

11 |

|

|

12 |

Salaries, other compensation, and employee benefits |

. . . . . . . . |

|

12 |

|

|

13 |

Professional fees and other payments to independent contractors . . |

. . . . . . . . |

|

13 |

|

|

14 |

Occupancy, rent, utilities, and maintenance |

. . . . . . . . |

|

14 |

|

|

15 |

Printing, publications, postage, and shipping |

. . . . . . . . |

|

15 |

|

|

16 |

Other expenses (describe in Schedule O) |

. . . . . . . . |

|

16 |

|

|

17 |

Total expenses. Add lines 10 through 16 |

. . . . . . . |

|

17 |

|

|

18 |

Excess or (deficit) for the year (subtract line 17 from line 9) . . . . |

. . . . . . . . |

|

18 |

|

|

19Net assets or fund balances at beginning of year (from line 27, column (A)) (must agree with

|

19 |

|

20 |

Other changes in net assets or fund balances (explain in Schedule O) |

20 |

21 |

Net assets or fund balances at end of year. Combine lines 18 through 20 |

21 |

For Paperwork Reduction Act Notice, see the separate instructions. |

Cat. No. 10642I |

Form |

Form |

|

Page 2 |

||||

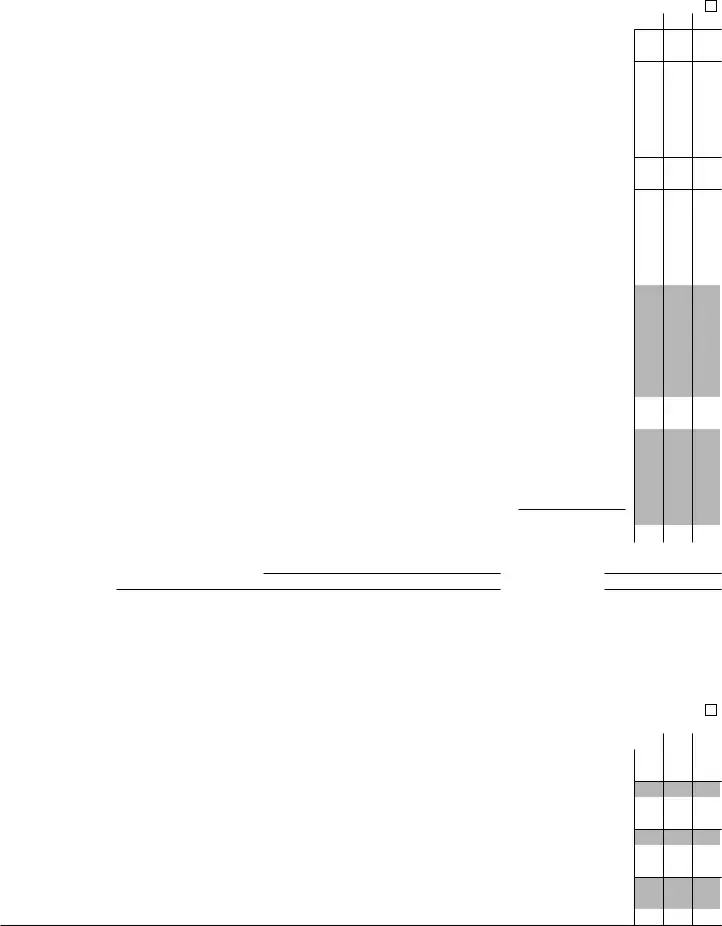

Part II |

Balance Sheets (see the instructions for Part II) |

|

|

|

||

|

|

Check if the organization used Schedule O to respond to any question in this Part II |

|

|||

|

|

|

(A) Beginning of year |

|

(B) End of year |

|

|

|

|

|

|

|

|

22 |

Cash, savings, and investments |

|

22 |

|

|

|

23 |

Land and buildings |

|

23 |

|

|

|

24 |

Other assets (describe in Schedule O) |

|

24 |

|

|

|

25 |

Total assets |

|

25 |

|

|

|

26 |

Total liabilities (describe in Schedule O) |

|

26 |

|

|

|

27 |

Net assets or fund balances (line 27 of column (B) must agree with line 21) . . |

|

27 |

|

|

|

Part III Statement of Program Service Accomplishments (see the instructions for Part III)

|

|

Check if the organization used Schedule O to respond to any question in this Part III . . |

|

Expenses |

|||||

|

|

|

|

|

|

|

(Required for section |

||

What is the organization’s primary exempt purpose? |

|||||||||

501(c)(3) and 501(c)(4) |

|||||||||

|

|

|

|

|

|

|

|||

Describe the organization’s program service accomplishments for each of its three largest program services, |

organizations; optional for |

||||||||

as measured by expenses. In a clear and concise manner, describe the services provided, the number of |

others.) |

||||||||

persons benefited, and other relevant information for each program title. |

|

|

|||||||

28 |

|

|

|

|

|

|

|

|

|

|

|

(Grants $ |

) |

If this amount includes foreign grants, check here . . . . |

28a |

|

|||

29 |

|

|

|

|

|

|

|

|

|

|

|

(Grants $ |

) |

If this amount includes foreign grants, check here . . . . |

29a |

|

|||

30 |

|

|

|

|

|

|

|

|

|

|

|

(Grants $ |

) |

If this amount includes foreign grants, check here . . . . |

30a |

|

|||

31 |

|

Other program services (describe in Schedule O) |

|

|

|||||

|

(Grants $ |

) |

If this amount includes foreign grants, check here . . . . |

31a |

|

||||

32 |

|

Total program service expenses (add lines 28a through 31a) |

32 |

|

|||||

Part IV List of Officers, Directors, Trustees, and Key Employees (list each one even if not

Check if the organization used Schedule O to respond to any question in this Part IV . . . . . . . . .

(a)Name and title

(b)Average hours per week

devoted to position

(c) Reportable |

(d) Health benefits, |

(e) Estimated amount of |

compensation |

contributions to employee |

|

(Forms |

benefit plans, and |

other compensation |

(if not paid, enter |

deferred compensation |

|

|

|

|

Form

Form |

Page 3 |

||

Part V |

Other Information (Note the Schedule A and personal benefit contract statement requirements in the |

||

|

instructions for Part V.) Check if the organization used Schedule O to respond to any question in this Part V . |

|

|

|

|

Yes No |

|

33Did the organization engage in any significant activity not previously reported to the IRS? If “Yes,” provide a

detailed description of each activity in Schedule O |

33 |

34Were any significant changes made to the organizing or governing documents? If “Yes,” attach a conformed copy of the amended documents if they reflect a change to the organization’s name. Otherwise, explain the

change on Schedule O. See instructions |

34 |

35a Did the organization have unrelated business gross income of $1,000 or more during the year from business |

|

activities (such as those reported on lines 2, 6a, and 7a, among others)? |

35a |

b If “Yes” to line 35a, has the organization filed a Form |

35b |

cWas the organization a section 501(c)(4), 501(c)(5), or 501(c)(6) organization subject to section 6033(e) notice,

reporting, and proxy tax requirements during the year? If “Yes,” complete Schedule C, Part III |

35c |

36Did the organization undergo a liquidation, dissolution, termination, or significant disposition of net assets

|

during the year? If “Yes,” |

complete applicable parts of Schedule N |

. . . . . . |

|

|

36 |

|

||||||

37a |

Enter amount of political expenditures, direct or indirect, as described in the instructions |

37a |

|

|

|

|

|

||||||

b |

Did the organization file Form |

. . . . . . |

|

|

37b |

|

|||||||

38a |

Did the organization borrow from, or make any loans to, any officer, director, trustee, or key employee; or were |

|

|

|

|||||||||

|

any such loans made in a prior year and still outstanding at the end of the tax year covered by this return? . |

38a |

|

||||||||||

b |

If “Yes,” complete Schedule L, Part II, and enter the total amount involved . . . . |

38b |

|

|

|

|

|

||||||

39 |

Section 501(c)(7) organizations. Enter: |

|

|

|

|

|

|

|

|

|

|||

a |

Initiation fees and capital contributions included on line 9 |

39a |

|

|

|

|

|||||||

b |

Gross receipts, included on line 9, for public use of club facilities |

39b |

|

|

|

|

|||||||

40a |

Section 501(c)(3) organizations. Enter amount of tax imposed on the organization during the year under: |

|

|

||||||||||

|

section 4911 |

|

; section 4912 |

|

; section 4955 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

bSection 501(c)(3), 501(c)(4), and 501(c)(29) organizations. Did the organization engage in any section 4958

excess benefit transaction during the year, or did it engage in an excess benefit transaction in a prior year |

|

|

|

that has not been reported on any of its prior Forms 990 or |

|

40b |

|

c Section 501(c)(3), 501(c)(4), and 501(c)(29) organizations. Enter amount of tax imposed |

|

|

|

on organization managers or disqualified persons during the year under sections 4912, |

|

|

|

4955, and 4958 |

|

|

|

|

|

|

|

d Section 501(c)(3), 501(c)(4), and 501(c)(29) organizations. Enter amount of tax on line |

|

|

|

40c reimbursed by the organization |

|

|

|

eAll organizations. At any time during the tax year, was the organization a party to a prohibited tax shelter

|

transaction? If “Yes,” complete Form |

|

40e |

|

|||||

41 |

List the states with which a copy of this return is filed |

|

|

|

|

|

|

|

|

42a |

The organization’s books are in care of |

Telephone no. |

|

|

|

|

|

||

b |

Located at |

ZIP + 4 |

|

|

|

|

|

||

At any time during the calendar year, did the organization have an interest in or a signature or other authority |

over |

|

|

Yes |

No |

||||

|

a financial account in a foreign country (such as a bank account, securities account, or other financial account)? |

|

42b |

|

|

||||

|

If “Yes,” enter the name of the foreign country |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

See the instructions for exceptions and filing requirements for FinCEN Form 114, Report of Foreign Bank and |

|

|

|

|

||||

|

Financial Accounts (FBAR). |

|

|

|

|

|

|

||

c |

At any time during the calendar year, did the organization maintain an office outside the United States? . |

|

42c |

|

|

||||

|

If “Yes,” enter the name of the foreign country |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

43 |

Section 4947(a)(1) nonexempt charitable trusts filing Form |

|

|||||||

|

and enter the amount of |

. . . . |

43 |

|

|

|

|

||

|

|

|

|

|

|

|

|

Yes |

No |

44a |

Did the organization maintain any donor advised funds during the year? If “Yes,” Form 990 must be |

|

|

|

|

||||

|

completed instead of Form |

|

44a |

|

|||||

bDid the organization operate one or more hospital facilities during the year? If “Yes,” Form 990 must be

completed instead of Form |

44b |

c Did the organization receive any payments for indoor tanning services during the year? |

44c |

dIf “Yes” to line 44c, has the organization filed a Form 720 to report these payments? If “No,” provide an

explanation in Schedule O |

44d |

45a Did the organization have a controlled entity within the meaning of section 512(b)(13)? |

45a |

bDid the organization receive any payment from or engage in any transaction with a controlled entity within the meaning of section 512(b)(13)? If “Yes,” Form 990 and Schedule R may need to be completed instead of

Form |

45b |

Form

Form |

Page 4 |

46Did the organization engage, directly or indirectly, in political campaign activities on behalf of or in opposition to candidates for public office? If “Yes,” complete Schedule C, Part I . . . . . . . . . . . . .

Yes No

46

Part VI Section 501(c)(3) Organizations Only

All section 501(c)(3) organizations must answer questions

Check if the organization used Schedule O to respond to any question in this Part VI . . . . . . . . .

Yes No

47Did the organization engage in lobbying activities or have a section 501(h) election in effect during the tax

|

year? If “Yes,” complete Schedule C, Part II |

47 |

48 |

Is the organization a school as described in section 170(b)(1)(A)(ii)? If “Yes,” complete Schedule E . . . . |

48 |

49a |

Did the organization make any transfers to an exempt |

49a |

b |

If “Yes,” was the related organization a section 527 organization? |

49b |

50Complete this table for the organization’s five highest compensated employees (other than officers, directors, trustees, and key employees) who each received more than $100,000 of compensation from the organization. If there is none, enter “None.”

|

(b) Average |

(c) Reportable |

(d) Health benefits, |

(e) Estimated amount of |

|

(a) Name and title of each employee |

contributions to employee |

||||

hours per week |

compensation |

||||

benefit plans, and deferred |

other compensation |

||||

|

devoted to position |

(Forms |

|||

|

|

|

compensation |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

f Total number of other employees paid over $100,000 . . . .

51Complete this table for the organization’s five highest compensated independent contractors who each received more than $100,000 of compensation from the organization. If there is none, enter “None.”

(a)Name and business address of each independent contractor

(b)Type of service

(c)Compensation

d Total number of other independent contractors each receiving over $100,000 . .

52Did the organization complete Schedule A? Note: All section 501(c)(3) organizations must attach a completed Schedule A . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Yes

No

Under penalties of perjury, I declare that I have examined this return, including accompanying schedules and statements, and to the best of my knowledge and belief, it is true, correct, and complete. Declaration of preparer (other than officer) is based on all information of which preparer has any knowledge.

Sign

Here

Paid

Preparer

Use Only

|

F |

|

|

|

|

|

|

|

|

|

|

|

Signature of officer |

|

|

|

|

Date |

|

|

|

||||

|

F |

|

|

|

|

|

|

|

|

|

|

|

Type or print name and title |

|

|

|

|

|

|

|

|

|

|

||

|

Print/Type preparer’s name |

|

Preparer’s signature |

|

Date |

|

Check |

if |

|

PTIN |

||

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Firm’s name |

|

|

|

|

Firm’s EIN |

|

|

|

|||

|

Firm’s address |

|

|

|

|

Phone no. |

|

|

|

|||

May the IRS discuss this return with the preparer shown above? See instructions . . . . . . . . . .

Yes

No

Form

| Fact Name | Description |

|---|---|

| Purpose | The IRS Form 990-EZ is used by certain tax-exempt organizations to provide annual financial information to the IRS. |

| Eligibility | Organizations with gross receipts between $200,000 and $500,000 and total assets under $2.5 million can file this form. |

| Filing Deadline | The form is due on the 15th day of the 5th month after the end of the organization’s fiscal year. |

| E-Filing | Form 990-EZ can be filed electronically through the IRS web portal or paper mailed. |

| State-Specific Requirements | Some states may require additional forms or reports. The governing laws vary by state. |

| Public Disclosure | The form is publicly accessible and must be available for viewing by anyone upon request. |

Once you have gathered your financial records and organizational information, you are ready to begin completing the IRS 990-EZ form. This form is an essential document for many tax-exempt organizations, as it provides a summary of financial information and helps fulfill the annual reporting requirements with the IRS. Follow the steps below to ensure you complete the form accurately.

Completing the IRS 990-EZ form may seem daunting, but by following these steps methodically, you can organize your information and ensure compliance. Remember to keep a copy of the filed form for your records and maintain records of financial activities throughout the year.

The IRS 990-EZ form is a simplified version of the Form 990 used by small tax-exempt organizations to report their income, expenses, and activities. This form provides the IRS with necessary information about an organization’s financial health, allowing them to determine compliance with tax regulations.

Typically, organizations that have gross receipts between $200,000 and $500,000 and total assets of less than $2.5 million are required to file the 990-EZ. Additionally, certain organizations, like charities and educational institutions, may need to file even if they do not meet these thresholds.

The deadline to file the IRS 990-EZ is the 15th day of the 5th month after the end of your organization's fiscal year. If your fiscal year ends on December 31, for example, the filing deadline would be May 15. Extensions are possible, but you must file Form 8868 to request one.

The IRS 990-EZ requires various financial information including:

This information helps to provide a clear picture of the organization’s operations and finances.

Filing the IRS 990-EZ can impact an organization in several ways. It is vital for maintaining tax-exempt status and ensuring transparency with the public. Additionally, it can affect the organization’s ability to receive grants, as many funders require proof of compliance with filing requirements.

Failure to file the IRS 990-EZ can lead to serious consequences. The IRS may impose penalties, which can vary based on the size of the organization and the duration of non-compliance. Continued failure to file may result in automatic revocation of tax-exempt status, making it imperative to stay compliant.

Yes, organizations can file the IRS 990-EZ electronically. The IRS offers e-filing options which can make submitting the form quicker and easier. Be sure to check the IRS website for approved e-filing software and platforms.

Filing the IRS 990-EZ form is crucial for tax-exempt organizations to maintain compliance. However, many people make significant mistakes when completing this form. Understanding these common errors can help ensure accurate submissions.

One frequent mistake is failing to check the eligibility requirements. Organizations that do not meet the criteria for filing the 990-EZ must complete the full 990 form instead. It's essential to assess size, revenue, and other factors before proceeding.

Another common error involves incorrect financial reporting. Many filers misreport their total revenue or expenses. This can lead to discrepancies and trigger audits. Review the organization’s financial records carefully to ensure accuracy.

Omitting essential information is also a problem. Sections related to program service accomplishments often get overlooked. Providing detailed information demonstrates compliance and helps maintain public trust. Organizations should clearly articulate their mission and achievements.

Additionally, many organizations fail to include the correct signatures. An unsigned form is considered incomplete, leading to potential penalties. It's vital to ensure that all required signatures are present before submission.

Another pitfall is not adhering to the filing deadline. Late submissions can incur penalties and affect an organization’s tax-exempt status. Marking the calendar with reminders for these deadlines can help avoid this issue.

It's important to understand the implications of not providing required schedules. Some organizations mistakenly believe that they can skip certain schedules if they don’t apply. However, all pertinent schedules must be completed to provide a comprehensive view of the organization’s financial health.

Finally, neglecting to keep a copy of the completed form leads to future complications. Having a record can help in referencing past filings or responding to inquiries from the IRS. It’s advisable to store a copy in an easily accessible location.

The IRS 990-EZ form is an essential document for many non-profit organizations, but it often accompanies other forms and documents that help to provide a complete financial picture. Understanding these additional forms can ensure that you meet all compliance requirements while clearly presenting your organization’s activities and financial health.

Keeping track of these forms, along with the IRS 990-EZ, is essential for ensuring smooth operations for your non-profit. By managing your paperwork effectively, your organization can focus more on its mission and less on compliance worries.

The IRS Form 990-EZ is a key document for non-profit organizations, providing a simplified way to report financial information to the Internal Revenue Service. It's important to understand how it compares to other forms related to nonprofit reporting. Here are eight documents that share similarities with the Form 990-EZ:

When filling out the IRS 990-EZ form, it is essential to follow certain guidelines to ensure accuracy and compliance. Here’s a helpful list of what you should and shouldn't do:

By adhering to these guidelines, you can facilitate a smoother filing process for your IRS 990-EZ form.

When it comes to the IRS 990-EZ form, several misconceptions can lead to confusion for nonprofit organizations. Understanding the facts can help ensure compliance and transparency. Here are four common misunderstandings:

Awareness of these misconceptions can empower organizations to meet their obligations confidently. Proper understanding fosters trust and accountability in the eyes of donors, stakeholders, and the community.

The IRS 990-EZ form is a streamlined version of the full Form 990, designed for smaller tax-exempt organizations. Here are important points to consider when filling out and using this form: