Understanding the IRS Insolvency Form, specifically Form 982, can be crucial for individuals and businesses navigating financial difficulties. This form serves multiple purposes, primarily to report the exclusion of certain discharged debts from gross income, which can significantly affect tax liabilities. It facilitates the reduction of tax attributes arising from the discharge of indebtedness, allowing taxpayers to minimize their taxable income during insolvency. The form includes sections that require taxpayers to specify the reasons for debt discharge, whether related to insolvency, qualified farm debts, or real property. Moreover, it allows for a detailed account of how the discharged amounts impact various tax attributes, such as net operating losses or capital losses. Taxpayers must carefully consider their situation and the potential tax implications of these elections. Completing Form 982 requires attention to detail; it can directly influence future tax credits, basis adjustments, and property values. Additionally, appropriate attachments and adherence to the most current IRS regulations are vital for compliance. Overall, Form 982 is an essential tool for managing the financial complexities around insolvency.

Form 982 |

|

Reduction of Tax Attributes Due to Discharge of |

|

OMB No. |

|

|

|

||||

|

Indebtedness (and Section 1082 Basis Adjustment) |

|

|

||

(Rev. March 2018) |

|

▶ Attach this form to your income tax return. |

|

Attachment |

|

Department of the Treasury |

|

|

|||

|

▶ Go to www.irs.gov/Form982 for instructions and the latest information. |

|

Sequence No. 94 |

||

Internal Revenue Service |

|

|

|||

Name shown on return |

|

|

Identifying number |

||

|

|

|

|

|

|

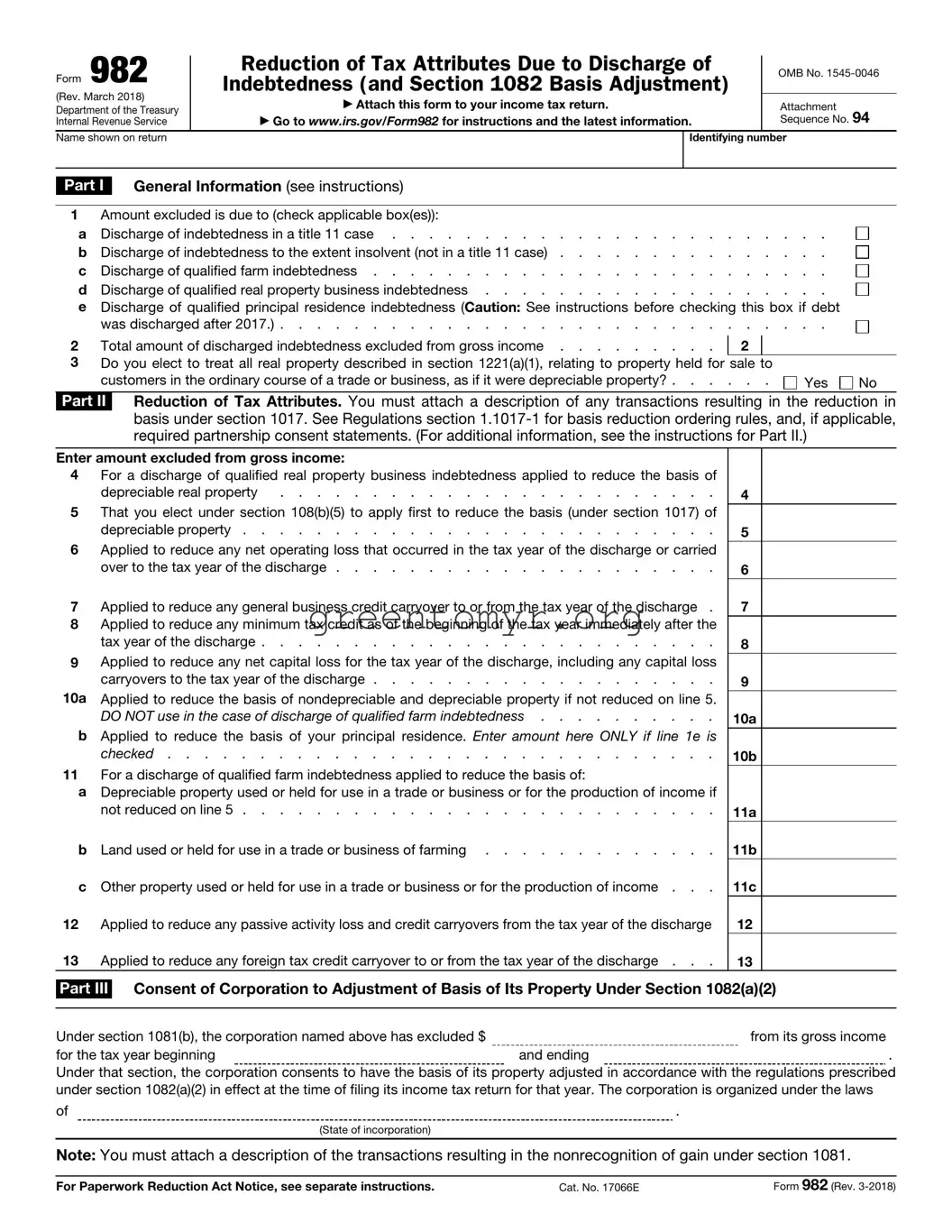

Part I General Information (see instructions)

1Amount excluded is due to (check applicable box(es)):

a |

Discharge of indebtedness in a title 11 case |

b |

Discharge of indebtedness to the extent insolvent (not in a title 11 case) |

c |

Discharge of qualified farm indebtedness |

d |

Discharge of qualified real property business indebtedness |

eDischarge of qualified principal residence indebtedness (Caution: See instructions before checking this box if debt

was discharged after 2017.) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

2 Total amount of discharged indebtedness excluded from gross income |

2 |

3Do you elect to treat all real property described in section 1221(a)(1), relating to property held for sale to

customers in the ordinary course of a trade or business, as if it were depreciable property? |

Yes |

No |

Part II Reduction of Tax Attributes. You must attach a description of any transactions resulting in the reduction in basis under section 1017. See Regulations section

Enter amount excluded from gross income:

4For a discharge of qualified real property business indebtedness applied to reduce the basis of

depreciable real property |

. . . . . . . . . . . . . . . . . . . . . . . . |

5That you elect under section 108(b)(5) to apply first to reduce the basis (under section 1017) of

depreciable property . . . . . . . . . . . . . . . . . . . . . . . . . .

6Applied to reduce any net operating loss that occurred in the tax year of the discharge or carried

over to the tax year of the discharge . . . . . . . . . . . . . . . . . . . . .

7 |

Applied to reduce any general business credit carryover to or from the tax year of the discharge . |

8Applied to reduce any minimum tax credit as of the beginning of the tax year immediately after the

tax year of the discharge . . . . . . . . . . . . . . . . . . . . . . . . .

9Applied to reduce any net capital loss for the tax year of the discharge, including any capital loss

carryovers to the tax year of the discharge . . . . . . . . . . . . . . . . . . .

10a Applied to reduce the basis of nondepreciable and depreciable property if not reduced on line 5. DO NOT use in the case of discharge of qualified farm indebtedness . . . . . . . . . .

bApplied to reduce the basis of your principal residence. Enter amount here ONLY if line 1e is

checked . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

11For a discharge of qualified farm indebtedness applied to reduce the basis of:

aDepreciable property used or held for use in a trade or business or for the production of income if

not reduced on line 5 . . . . . . . . . . . . . . . . . . . . . . . . . .

b |

Land used or held for use in a trade or business of farming |

c |

Other property used or held for use in a trade or business or for the production of income . . . |

12Applied to reduce any passive activity loss and credit carryovers from the tax year of the discharge

13 |

Applied to reduce any foreign tax credit carryover to or from the tax year of the discharge . . . |

4

5

6

7

8

9

10a

10b

11a

11b

11c

12

13

Part III Consent of Corporation to Adjustment of Basis of Its Property Under Section 1082(a)(2)

Under section 1081(b), the corporation named above has excluded $ |

|

from its gross income |

for the tax year beginning |

and ending |

. |

Under that section, the corporation consents to have the basis of its property adjusted in accordance with the regulations prescribed under section 1082(a)(2) in effect at the time of filing its income tax return for that year. The corporation is organized under the laws

of |

. |

|

(State of incorporation) |

Note: You must attach a description of the transactions resulting in the nonrecognition of gain under section 1081.

For Paperwork Reduction Act Notice, see separate instructions. |

Cat. No. 17066E |

Form 982 (Rev. |

| Fact Name | Fact Detail |

|---|---|

| Form Purpose | Form 982 is used to reduce tax attributes due to the discharge of indebtedness. |

| Governing Law | The form is governed by the Internal Revenue Code, specifically sections 108 and 1017. |

| Filing Requirement | This form must be attached to your income tax return. |

| Form Update | The current version of Form 982 was revised in March 2018. |

| Exclusion Types | There are specific types of exclusions available including discharge from title 11 cases and qualified farm indebtedness. |

| Discharge Amount | The total amount of discharged indebtedness must be reported on the form. |

| Real Property Election | Taxpayers can elect to treat all real property as depreciable property under certain conditions. |

| Attribute Reduction | Part II of the form details how tax attributes are reduced due to discharge. |

| Passive Activity Losses | Discharges may also apply to reduce passive activity loss and credit carryovers. |

| Corporate Consent | Certain corporations may need to consent to basis adjustments under specific sections. |

Filling out the IRS Insolvency Form can seem daunting, but taking it step by step will make the process manageable. Begin by gathering the necessary information and start filling out the details accurately. Once completed, you will attach this form to your income tax return. You'll also find it helpful to make sure you have any required documentation ready for submission.

IRS Form 982 is used to reduce tax attributes due to the discharge of indebtedness. Taxpayers can use this form to exclude certain amounts of discharged debt from their gross income. The form specifically addresses situations such as bankruptcy (Title 11 cases), insolvency, and certain qualified indebtedness.

Individuals, businesses, and corporations that have had their indebtedness discharged should file Form 982. This includes those in bankruptcy proceedings, those who have become insolvent, or those who have qualified debt related to farming or real property. It is important to attach this form to the relevant income tax return.

There are several types of discharged indebtedness that can be excluded, including:

To determine your total amount of discharged indebtedness, review your financial records for any debts that were forgiven or canceled during the tax year. Be sure to include any debts directly related to your business or property that qualify for exclusion under the guidelines of the form.

Insolvency, as it pertains to Form 982, refers to a situation where your total liabilities exceed your total assets. If you are insolvent at the time your debt is discharged, you may qualify to exclude that debt from your gross income. Documenting this insolvency is critical for the proper completion of the form.

When discharged debt is related to your principal residence, certain exclusions may apply. If you check the box for qualified principal residence indebtedness on the form, specific rules govern how that amount is treated. Be cautious, especially for debt discharged after 2017, as different rules may impact your tax situation.

In addition to Form 982, you must include a description of any transactions that result in a reduction of basis under Section 1017. This helps the IRS understand how your financial situation changed due to the discharge of indebtedness. Make sure to follow any additional instructions provided for the specific sections of the form.

Completing the IRS Insolvency Form (Form 982) can be a tricky process for many people. Several common mistakes often lead to errors or delays in processing. Below, ten frequent pitfalls are outlined to help individuals navigate their way through filling out this important form.

1. Failing to Attach the Form: One of the most significant oversights occurs when individuals forget to attach Form 982 to their income tax return. This form is crucial, and failing to include it can result in rejected claims.

2. Incorrectly Marking the Boxes: Applicants often check the wrong boxes in Part I regarding the discharge of indebtedness. Each box corresponds to a specific situation. Misunderstanding the categories can lead to inaccurate reporting of one’s financial status.

3. Failing to Calculate Total Amount Accurately: Many people miscalculate the total amount of discharged indebtedness excluded from their gross income. Precision is key here, and using a calculator can help ensure accuracy.

4. Ignoring Instructions for Property Depreciation: A common error emerges when individuals neglect to read the guidance about electing treatment for real property as depreciable property. Misunderstandings may affect potential tax benefits.

5. Omitting Required Descriptions: Form 982 requires a description of transactions that result in the reduction in basis under Section 1017. Leaving out this information can impede the processing of the form.

6. Misunderstanding the Reduction of Tax Attributes: In Part II, applicants often confuse the various reductions of tax attributes. Each line item must be approached with care, as oversights can invalidate parts of the submission.

7. Missing Information on Non-depreciable Property: When reducing the basis of non-depreciable and depreciable property, applicants sometimes fail to reference the correct lines. It’s essential to follow the instructions closely to ensure compliance.

8. Not Considering Foreign Tax Credits: For those who have foreign tax credits, missing information related to foreign tax credit carryover can be a critical oversight. This can lead to complications in tax filings.

9. Ignoring Corporate Consent Requirements: For corporations filling out Part III, failing to obtain the necessary consents for adjustments of asset bases can hinder the completion process. Corporate tax obligations differ from individual requirements.

10. Submitting Without a Review: Finally, individuals often submit their forms without thoroughly reviewing their entries. A final check can catch simple mistakes that could affect the outcome.

By keeping these common mistakes in mind, individuals can better navigate the process of completing and submitting Form 982. Careful attention to detail helps ensure that tax filings are processed smoothly and accurately.

The IRS Form 982 is crucial for taxpayers who have encountered debt discharge due to insolvency or bankruptcy. However, it is often used alongside several other forms and documents, each serving a specific purpose in the reporting and tax adjustment process. Understanding these forms can assist in navigating the complexities of financial recovery after insolvency.

Filing the correct forms and understanding their implications is essential after experiencing debt discharge. Each document plays a vital role in accurately reporting financial status and ensuring compliance with the IRS's regulations. Thorough preparation and attention to detail can mitigate potential tax liabilities and lead toward effective financial recovery.

The IRS Insolvency form, also known as Form 982, serves specific purposes related to tax and insolvency. Several other tax-related forms share similar functionalities regarding debt discharge, income exclusion, and tax attribute adjustments. Here are eight such documents and how they relate to Form 982:

Filling out the IRS Insolvency Form (Form 982) involves careful consideration of the following key points: