The IRS Power of Attorney (Form 2848) is a crucial tool for individuals and businesses seeking to authorize someone to act on their behalf in tax matters. This form allows taxpayers to appoint an individual or organization to represent them before the IRS, ensuring that their interests are protected and effectively communicated. By completing Form 2848, taxpayers can grant their designated representative the authority to receive and inspect confidential tax information, make decisions regarding tax matters, and even sign documents on their behalf. The form is essential for navigating complex tax situations, such as audits or appeals, and can streamline communication with the IRS. Additionally, it is important to understand the specific limitations and responsibilities that come with granting power of attorney, as well as the process for revoking it if necessary. Understanding these aspects will empower taxpayers to make informed decisions about their representation and help them maintain control over their tax affairs.

Check Form for Common Errors & Reminders

Form 2848 |

|

Power of Attorney |

For IRS Use Only |

|||||

|

|

|

|

OMB No. |

||||

(Rev. January 2021) |

and Declaration of Representative |

|

|

|

|

|

||

Received by: |

|

|||||||

Department of the Treasury |

|

|

|

|||||

▶ Go to www.irs.gov/Form2848 for instructions and the latest information. |

|

|

|

|

|

|||

Internal Revenue Service |

Name |

|

|

|||||

|

|

|

||||||

Part I |

Power of Attorney |

Telephone |

|

|

||||

|

Caution: A separate Form 2848 must be completed for each taxpayer. Form 2848 will not be honored |

Function |

|

|

||||

|

for any purpose other than representation before the IRS. |

Date |

/ / |

|||||

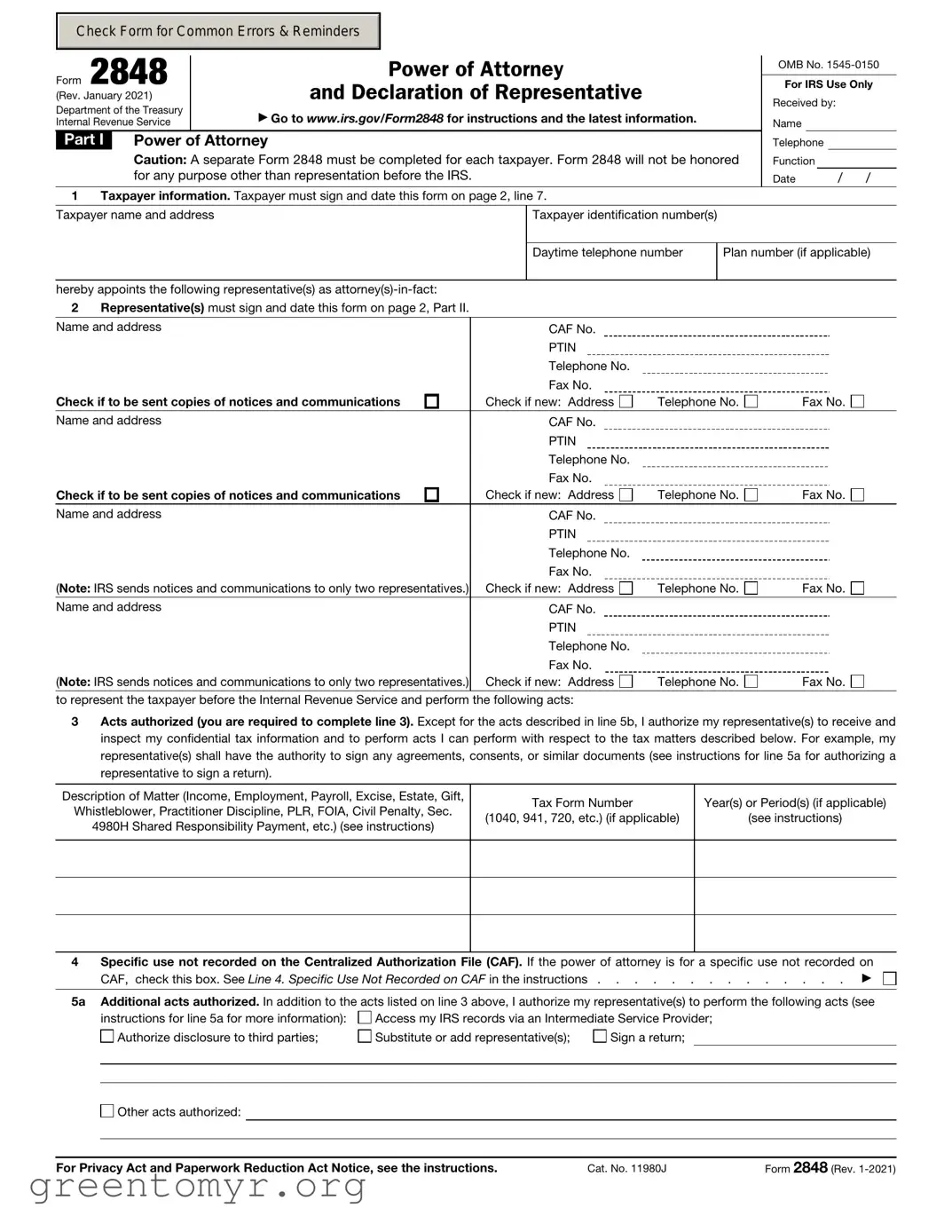

1Taxpayer information. Taxpayer must sign and date this form on page 2, line 7.

Taxpayer name and address |

Taxpayer identification number(s) |

Daytime telephone number

Plan number (if applicable)

Name and address |

CAF No. |

|

|

|

PTIN |

|

|

|

Telephone No. |

|

|

|

Fax No. |

|

|

Check if to be sent copies of notices and communications |

Check if new: Address |

Telephone No. |

Fax No. |

Name and address |

CAF No. |

|

|

|

PTIN |

|

|

|

Telephone No. |

|

|

|

Fax No. |

|

|

Check if to be sent copies of notices and communications |

Check if new: Address |

Telephone No. |

Fax No. |

Name and address |

CAF No. |

|

|

|

PTIN |

|

|

|

Telephone No. |

|

|

|

Fax No. |

|

|

(Note: IRS sends notices and communications to only two representatives.) |

Check if new: Address |

Telephone No. |

Fax No. |

Name and address |

CAF No. |

|

|

|

PTIN |

|

|

|

Telephone No. |

|

|

|

Fax No. |

|

|

(Note: IRS sends notices and communications to only two representatives.) |

Check if new: Address |

Telephone No. |

Fax No. |

to represent the taxpayer before the Internal Revenue Service and perform the following acts:

3Acts authorized (you are required to complete line 3). Except for the acts described in line 5b, I authorize my representative(s) to receive and inspect my confidential tax information and to perform acts I can perform with respect to the tax matters described below. For example, my representative(s) shall have the authority to sign any agreements, consents, or similar documents (see instructions for line 5a for authorizing a representative to sign a return).

Description of Matter (Income, Employment, Payroll, Excise, Estate, Gift, |

Tax Form Number |

Year(s) or Period(s) (if applicable) |

|

Whistleblower, Practitioner Discipline, PLR, FOIA, Civil Penalty, Sec. |

|||

(1040, 941, 720, etc.) (if applicable) |

(see instructions) |

||

4980H Shared Responsibility Payment, etc.) (see instructions) |

|||

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

Specific use not recorded on the Centralized Authorization File (CAF). If the power of attorney is for a specific use not recorded on |

|||

|

CAF, check this box. See Line 4. Specific Use Not Recorded on CAF in the instructions . |

. . . . . . . . . . . . . ▶ |

||

|

|

|

||

5a |

Additional acts authorized. In addition to the acts listed on line 3 above, I authorize my representative(s) to perform the following acts (see |

|||

|

instructions for line 5a for more information): |

Access my IRS records via an Intermediate Service Provider; |

||

|

Authorize disclosure to third parties; |

Substitute or add representative(s); |

Sign a return; |

|

|

|

|

|

|

|

|

|

|

|

Other acts authorized:

For Privacy Act and Paperwork Reduction Act Notice, see the instructions. |

Cat. No. 11980J |

Form 2848 (Rev. |

Form 2848 (Rev. |

Page 2 |

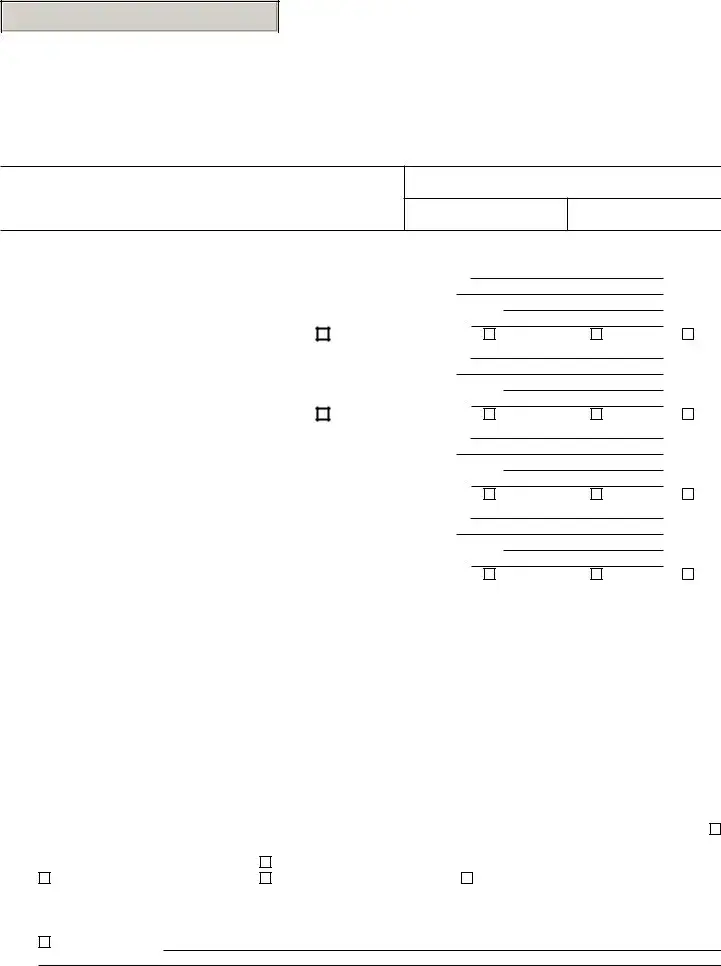

bSpecific acts not authorized. My representative(s) is (are) not authorized to endorse or otherwise negotiate any check (including directing or accepting payment by any means, electronic or otherwise, into an account owned or controlled by the representative(s) or any firm or other entity with whom the representative(s) is (are) associated) issued by the government in respect of a federal tax liability.

List any other specific deletions to the acts otherwise authorized in this power of attorney (see instructions for line 5b):

6Retention/revocation of prior power(s) of attorney. The filing of this power of attorney automatically revokes all earlier power(s) of attorney on file with the Internal Revenue Service for the same matters and years or periods covered by this form. If you do not want to

revoke a prior power of attorney, check here . . . . . . . . . . . . . . . . . . . . . . . . . . . ▶

YOU MUST ATTACH A COPY OF ANY POWER OF ATTORNEY YOU WANT TO REMAIN IN EFFECT.

7Taxpayer declaration and signature. If a tax matter concerns a year in which a joint return was filed, each spouse must file a separate power of attorney even if they are appointing the same representative(s). If signed by a corporate officer, partner, guardian, tax matters partner, partnership representative (or designated individual, if applicable), executor, receiver, administrator, trustee, or individual other than the taxpayer, I certify I have the legal authority to execute this form on behalf of the taxpayer.

▶ IF NOT COMPLETED, SIGNED, AND DATED, THE IRS WILL RETURN THIS POWER OF ATTORNEY TO THE TAXPAYER.

Signature |

Date |

Title (if applicable) |

Print name |

|

Print name of taxpayer from line 1 if other than individual |

Part II Declaration of Representative

Under penalties of perjury, by my signature below I declare that:

•I am not currently suspended or disbarred from practice, or ineligible for practice, before the Internal Revenue Service;

•I am subject to regulations in Circular 230 (31 CFR, Subtitle A, Part 10), as amended, governing practice before the Internal Revenue Service;

•I am authorized to represent the taxpayer identified in Part I for the matter(s) specified there; and

•I am one of the following:

a

bCertified Public

cEnrolled

d

e

fFamily

gEnrolled

hUnenrolled Return

kQualifying Student or Law

rEnrolled Retirement Plan

▶IF THIS DECLARATION OF REPRESENTATIVE IS NOT COMPLETED, SIGNED, AND DATED, THE IRS WILL RETURN THE POWER OF ATTORNEY. REPRESENTATIVES MUST SIGN IN THE ORDER LISTED IN PART I, LINE 2.

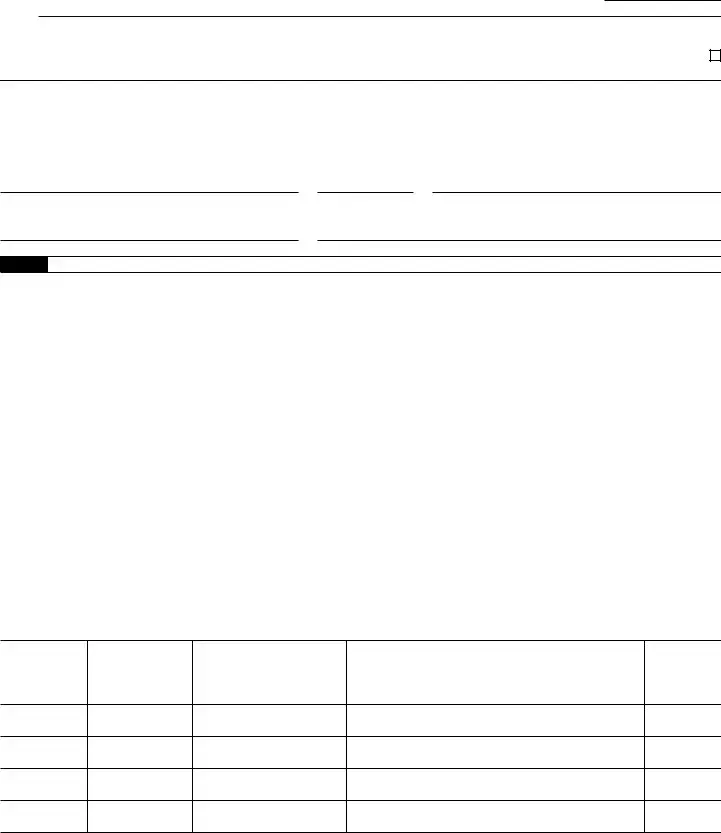

Note: For designations

Designation—

Insert above

letter

Licensing jurisdiction

(State) or other

licensing authority

(if applicable)

Bar, license, certification, registration, or enrollment number (if applicable)

Signature

Date

Form 2848 (Rev.

| Fact Name | Description |

|---|---|

| Purpose | The IRS Power of Attorney (Form 2848) allows individuals to designate someone to represent them in tax matters. |

| Who Can Use It | Any taxpayer can use Form 2848 to appoint an individual or organization as their representative. |

| Authorized Actions | The form grants the representative the authority to perform various actions, including signing tax returns and discussing tax issues with the IRS. |

| Validity | Once filed, the Power of Attorney remains in effect until revoked or until the taxpayer's death. |

| Revocation Process | To revoke the Power of Attorney, a taxpayer must submit a written statement to the IRS, specifying the revocation. |

| State-Specific Forms | Some states have their own Power of Attorney forms. For example, California uses Form FTB 3520. |

| Governing Law | State-specific forms are governed by state tax laws, which vary by jurisdiction. |

| Submission Methods | Form 2848 can be submitted electronically or mailed to the appropriate IRS office, depending on the circumstances. |

| Multiple Representatives | Taxpayers can designate multiple representatives on Form 2848, but each must be listed separately. |

| Signature Requirement | The taxpayer must sign the form for it to be valid, indicating their consent to the representation. |

Completing the IRS Power of Attorney (Form 2848) is an important step in designating someone to represent you before the IRS. After filling out the form, you will need to submit it to the IRS for processing. Ensure that all information is accurate and complete to avoid delays.

The IRS Power of Attorney (Form 2848) is a document that allows an individual or entity to designate another person to represent them before the IRS. This form grants the appointed representative the authority to handle tax matters on behalf of the taxpayer, including receiving confidential information and making decisions regarding tax issues.

Any individual who is authorized to practice before the IRS can be appointed as a representative. This includes attorneys, certified public accountants (CPAs), enrolled agents, and certain other professionals. Additionally, taxpayers can also appoint a family member or friend, but that person must meet specific requirements to represent them effectively.

Form 2848 can be used for a variety of tax matters, including but not limited to:

However, the form must specify the types of tax matters and the tax years involved for the authority to be valid.

Completing Form 2848 involves several key steps:

It is crucial to ensure all information is accurate to avoid delays in processing.

The validity of Form 2848 generally lasts until the taxpayer revokes it, the representative withdraws, or the IRS accepts a new Form 2848 that supersedes the previous one. Taxpayers can also specify a termination date on the form if they wish for the authority to end at a certain time.

Yes, taxpayers can revoke Form 2848 at any time. To do so, they must submit a written statement to the IRS that includes their name, address, taxpayer identification number, and the name of the representative being revoked. It is advisable to keep a copy of the revocation for personal records.

Form 2848 can be submitted to the IRS by mailing it to the address listed in the form instructions or by faxing it to the appropriate IRS office. The submission method may vary depending on the specific tax matter and the representative’s credentials. Taxpayers should ensure that the form is sent to the correct IRS office to avoid processing delays.

While there is no fee charged by the IRS for submitting Form 2848, representatives may charge fees for their services. The costs can vary widely based on the complexity of the tax issues and the representative's experience. It is advisable for taxpayers to discuss fees upfront with their appointed representative.

Filling out the IRS Power of Attorney (Form 2848) can seem straightforward, but many people make common mistakes that can lead to delays or complications. Understanding these pitfalls can help ensure that your form is filled out correctly and efficiently.

One frequent mistake is failing to provide complete information about the taxpayer. This includes not only the taxpayer's name and Social Security number but also the correct address. Omitting any of these details can cause the IRS to reject the form, leaving the taxpayer without the representation they need.

Another error occurs when individuals do not specify the exact powers they wish to grant their representative. The IRS allows taxpayers to choose specific areas of representation, such as audits or appeals. If the form is filled out too broadly or lacks clarity, it may not be accepted, or the representative may not be able to act on behalf of the taxpayer effectively.

Additionally, some people forget to sign the form. A signature is crucial, as it verifies that the taxpayer authorizes the representative to act on their behalf. Without this, the IRS will not process the Power of Attorney, and the intended representation will not take effect.

Another common mistake is using outdated versions of the form. The IRS updates its forms periodically, and using an old version can lead to confusion or rejection. Always ensure you are using the most current version of Form 2848, which can be found on the IRS website.

Some individuals also overlook the importance of including the representative's information accurately. This includes the representative's name, address, and phone number. If any of this information is incorrect, it can hinder communication between the IRS and the representative, causing unnecessary delays.

Moreover, people sometimes forget to indicate the tax matters for which the Power of Attorney is being granted. Without specifying the relevant tax years or types of tax involved, the IRS may not recognize the authority granted to the representative, leading to confusion and potential issues down the line.

Another mistake is neglecting to check for additional requirements that might apply to specific situations. Certain circumstances, such as representing a deceased taxpayer or a business entity, may have unique requirements that must be followed. Failing to adhere to these can complicate the process further.

Lastly, many individuals do not keep a copy of the completed form for their records. Having a copy is essential for both the taxpayer and the representative. It serves as proof of the authority granted and can be useful for future reference, especially if any questions arise regarding the representation.

The IRS Power of Attorney (Form 2848) allows a designated individual to represent a taxpayer before the IRS. In addition to this form, there are several other documents that may be useful when dealing with tax matters. Here are four common forms that often accompany Form 2848:

Having these forms ready can streamline communication with the IRS and ensure that the taxpayer's needs are met effectively. Each document serves a specific purpose and can assist in resolving tax issues more efficiently.

When filling out the IRS Power of Attorney (Form 2848), it's essential to follow some key guidelines to ensure your submission is correct and effective. Here are six things you should and shouldn't do:

The IRS Power of Attorney form, known as Form 2848, is a crucial document for taxpayers who wish to authorize someone to represent them before the IRS. However, several misconceptions surround this form. Below are six common misunderstandings:

Understanding these misconceptions can help taxpayers make informed decisions about their representation before the IRS. Proper use of Form 2848 ensures that individuals have the necessary support when navigating tax matters.

When filling out and using the IRS Power of Attorney (Form 2848), keep the following key takeaways in mind: