The IRS Schedule A, attached to Form 990 or 990-EZ, serves as a crucial document for tax-exempt organizations, enabling them to report their public charity status and demonstrate compliance with federal regulations. This form is essential for organizations seeking to maintain their tax-exempt status, as it provides detailed information about the organization’s public support, revenue sources, and activities. By requiring organizations to disclose their financial information and operational details, Schedule A helps ensure transparency and accountability in the nonprofit sector. Organizations must carefully navigate the requirements of this form, as it assesses their eligibility for certain tax benefits and outlines the thresholds for public support tests. Additionally, the form includes specific sections that address contributions, grants, and fundraising efforts, allowing the IRS to evaluate how well an organization meets the criteria for public charity classification. The completion of Schedule A is not merely a bureaucratic step; it plays a vital role in fostering trust between nonprofits and the communities they serve.

SCHEDULE A |

Public Charity Status and Public Support |

OMB No. |

|

|

|||

2024 |

|||

(Form 990) |

Complete if the organization is a section 501(c)(3) organization or a section 4947(a)(1) nonexempt charitable trust. |

||

|

|||

Department of the Treasury |

Attach to Form 990 or Form |

Open to Public |

|

Internal Revenue Service |

Go to www.irs.gov/Form990 for instructions and the latest information. |

Inspection |

|

|

|||

Name of the organization |

Employer identification number |

||

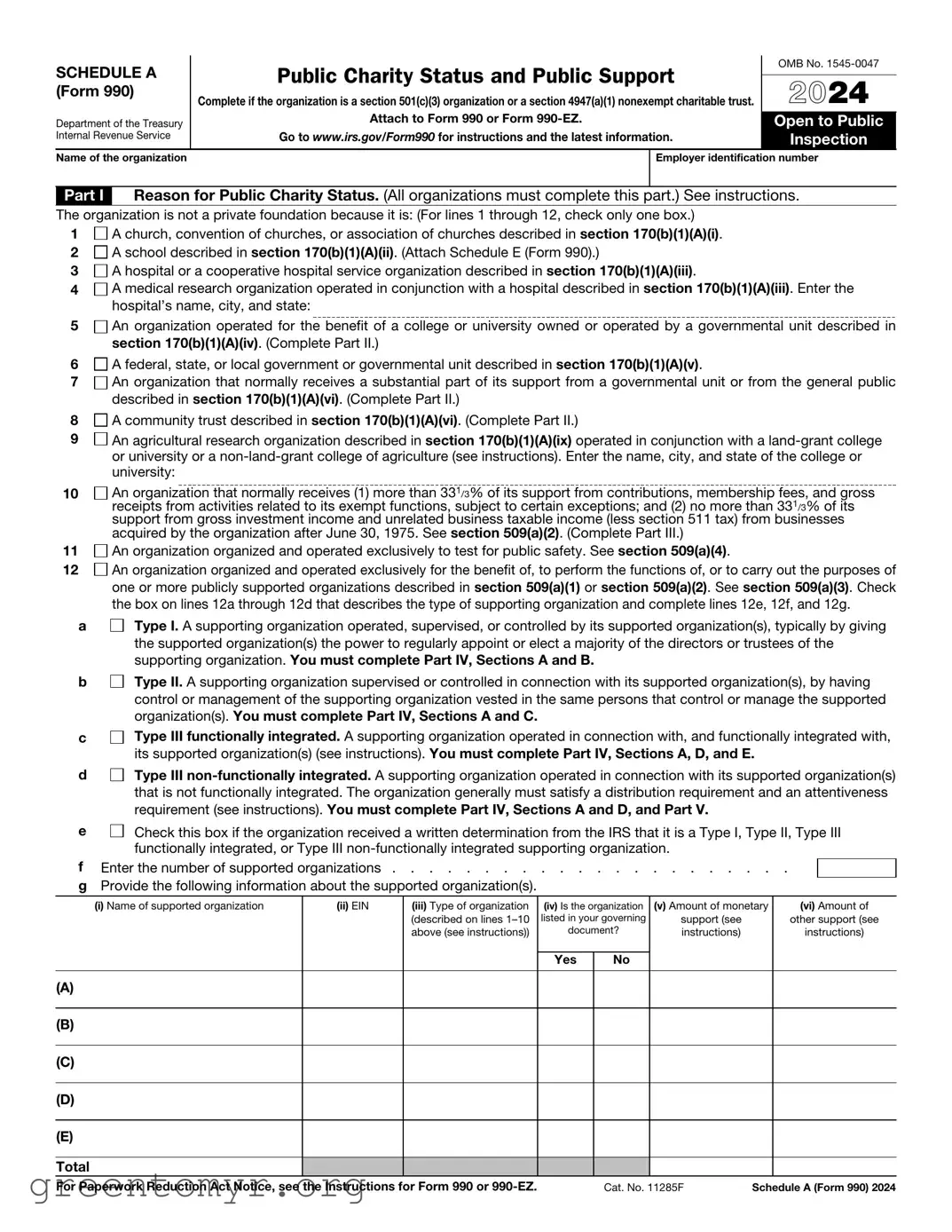

Part I Reason for Public Charity Status. (All organizations must complete this part.) See instructions.

The organization is not a private foundation because it is: (For lines 1 through 12, check only one box.)

1 A church, convention of churches, or association of churches described in section 170(b)(1)(A)(i).

2 A school described in section 170(b)(1)(A)(ii). (Attach Schedule E (Form 990).)

3 A hospital or a cooperative hospital service organization described in section 170(b)(1)(A)(iii).

4 A medical research organization operated in conjunction with a hospital described in section 170(b)(1)(A)(iii). Enter the hospital’s name, city, and state:

5 An organization operated for the benefit of a college or university owned or operated by a governmental unit described in section 170(b)(1)(A)(iv). (Complete Part II.)

6 A federal, state, or local government or governmental unit described in section 170(b)(1)(A)(v).

7 An organization that normally receives a substantial part of its support from a governmental unit or from the general public described in section 170(b)(1)(A)(vi). (Complete Part II.)

8 A community trust described in section 170(b)(1)(A)(vi). (Complete Part II.)

9 An agricultural research organization described in section 170(b)(1)(A)(ix) operated in conjunction with a

10

11

12

An organization that normally receives (1) more than 331/3% of its support from contributions, membership fees, and gross receipts from activities related to its exempt functions, subject to certain exceptions; and (2) no more than 331/3% of its support from gross investment income and unrelated business taxable income (less section 511 tax) from businesses acquired by the organization after June 30, 1975. See section 509(a)(2). (Complete Part III.)

An organization organized and operated exclusively to test for public safety. See section 509(a)(4).

An organization organized and operated exclusively for the benefit of, to perform the functions of, or to carry out the purposes of one or more publicly supported organizations described in section 509(a)(1) or section 509(a)(2). See section 509(a)(3). Check the box on lines 12a through 12d that describes the type of supporting organization and complete lines 12e, 12f, and 12g.

a

Type I. A supporting organization operated, supervised, or controlled by its supported organization(s), typically by giving the supported organization(s) the power to regularly appoint or elect a majority of the directors or trustees of the supporting organization. You must complete Part IV, Sections A and B.

b

c

d

Type II. A supporting organization supervised or controlled in connection with its supported organization(s), by having control or management of the supporting organization vested in the same persons that control or manage the supported organization(s). You must complete Part IV, Sections A and C.

Type III functionally integrated. A supporting organization operated in connection with, and functionally integrated with, its supported organization(s) (see instructions). You must complete Part IV, Sections A, D, and E.

Type III

e Check this box if the organization received a written determination from the IRS that it is a Type I, Type II, Type III functionally integrated, or Type III

f Enter the number of supported organizations . . . . . . . . . . . . . . . . . . . . . .

gProvide the following information about the supported organization(s).

(i) Name of supported organization |

(ii) EIN |

(iii) Type of organization |

(iv) Is the organization |

(v) Amount of monetary |

(vi) Amount of |

|

|

|

(described on lines |

listed in your governing |

support (see |

other support (see |

|

|

|

above (see instructions)) |

document? |

instructions) |

instructions) |

|

|

|

|

|

|

|

|

|

|

|

Yes |

No |

|

|

(A)

(B)

(C)

(D)

(E)

Total

For Paperwork Reduction Act Notice, see the Instructions for Form 990 or |

Cat. No. 11285F |

Schedule A (Form 990) 2024 |

Schedule A (Form 990) 2024 |

Page 2 |

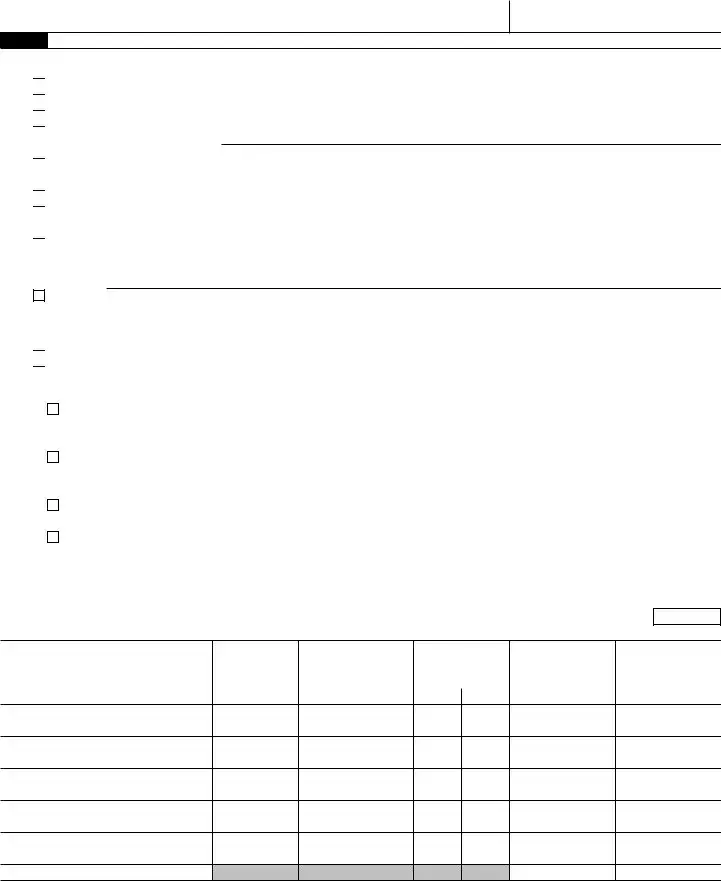

Part II Support Schedule for Organizations Described in Sections 170(b)(1)(A)(iv) and 170(b)(1)(A)(vi) (Complete only if you checked the box on line 5, 7, or 8 of Part I or if the organization failed to qualify under Part III. If the organization fails to qualify under the tests listed below, please complete Part III.)

Section A. Public Support

Calendar year (or fiscal year beginning in)

1Gifts, grants, contributions, and membership fees received. (Do not include any “unusual grants.”) . . .

2Tax revenues levied for the organization’s benefit and either paid

to or expended on its behalf . . .

3The value of services or facilities furnished by a governmental unit to the organization without charge . . . .

4 Total. Add lines 1 through 3 . . .

5The portion of total contributions by each person (other than a governmental unit or publicly supported organization) included on line 1 that exceeds 2% of the amount shown on line 11, column (f) . . . .

6Public support. Subtract line 5 from line 4

Section B. Total Support

(a)2020

(b)2021

(c)2022

(d)2023

(e)2024

(f)Total

Calendar year (or fiscal year beginning in) |

(a) 2020 |

(b) 2021 |

(c) 2022 |

(d) 2023 |

(e) 2024 |

(f) Total |

|

7 |

Amounts from line 4 |

|

|

|

|

|

|

8 |

Gross income from interest, dividends, |

|

|

|

|

|

|

|

payments received on securities loans, |

|

|

|

|

|

|

|

rents, royalties, and income from |

|

|

|

|

|

|

|

similar sources |

|

|

|

|

|

|

9Net income from unrelated business activities, whether or not the business is regularly carried on . . . . . .

10Other income. Do not include gain or loss from the sale of capital assets (Explain in Part VI.) . . . . . . .

11 |

Total support. Add lines 7 through 10 |

|

|

|

|

12 |

Gross receipts from related activities, etc. |

|

(see instructions) |

12 |

|

13First 5 years. If the Form 990 is for the organization’s first, second, third, fourth, or fifth tax year as a section 501(c)(3)

organization, check this box and stop here . . . . . . . . . . . . . . . . . . . . . . . . . .

Section C. Computation of Public Support Percentage

14 |

Public support percentage for 2024 (line 6, column (f), divided by line 11, column (f)) . . . . |

14 |

|

% |

15 |

Public support percentage from 2023 Schedule A, Part II, line 14 |

15 |

|

% |

16a |

331/3% support |

1/3% or more, check this |

|

|

|

box and stop here. The organization qualifies as a publicly supported organization |

|

||

b331/3% support

this box and stop here. The organization qualifies as a publicly supported organization . . . . . . . . . . . .

17a

b

organization . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

18Private foundation. If the organization did not check a box on line 13, 16a, 16b, 17a, or 17b, check this box and see

instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Schedule A (Form 990) 2024

Schedule A (Form 990) 2024 |

Page 3 |

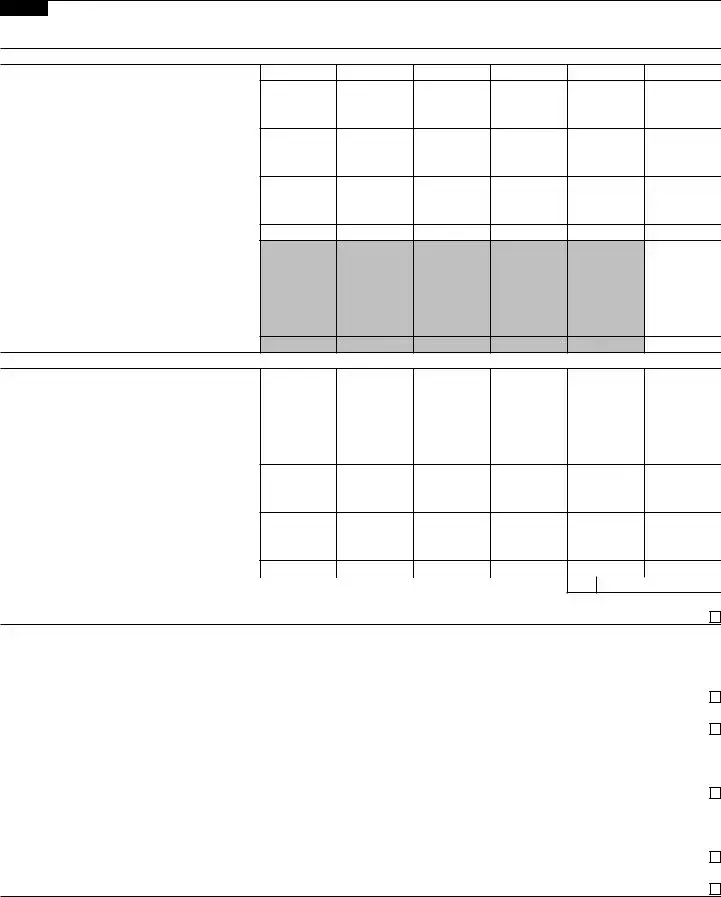

Part III Support Schedule for Organizations Described in Section 509(a)(2)

(Complete only if you checked the box on line 10 of Part I or if the organization failed to qualify under Part II. If the organization fails to qualify under the tests listed below, please complete Part II.)

Section A. Public Support

Calendar year (or fiscal year beginning in)

1Gifts, grants, contributions, and membership fees received. (Do not include any “unusual grants.”)

2Gross receipts from admissions, merchandise sold or services performed, or facilities furnished in any activity that is related to the organization’s

3Gross receipts from activities that are not an unrelated trade or business under section 513

4Tax revenues levied for the

organization’s benefit and either paid to or expended on its behalf . . .

5The value of services or facilities furnished by a governmental unit to the organization without charge . . . .

6Total. Add lines 1 through 5 . . . .

7a Amounts included on lines 1, 2, and 3

received from disqualified persons .

bAmounts included on lines 2 and 3 received from other than disqualified persons that exceed the greater of $5,000 or 1% of the amount on line 13 for the year

c Add lines 7a and 7b . . . . . .

8Public support. (Subtract line 7c from line 6.) . . . . . . . . . . .

Section B. Total Support

(a)2020

(b)2021

(c)2022

(d)2023

(e)2024

(f)Total

Calendar year (or fiscal year beginning in) |

(a) 2020 |

(b) 2021 |

(c) 2022 |

(d) 2023 |

(e) 2024 |

(f) Total |

|

9 |

Amounts from line 6 |

|

|

|

|

|

|

10a |

Gross income from interest, dividends, |

|

|

|

|

|

|

|

payments received on securities loans, rents, |

|

|

|

|

|

|

|

royalties, and income from similar sources |

|

|

|

|

|

|

bUnrelated business taxable income (less section 511 taxes) from businesses acquired after June 30, 1975 . . . .

c Add lines 10a and 10b . . . . .

11Net income from unrelated business activities not included on line 10b, whether or not the business is regularly carried on

12Other income. Do not include gain or loss from the sale of capital assets (Explain in Part VI.) . . . . . . .

13Total support. (Add lines 9, 10c, 11, and 12.) . . . . . . . . . .

14First 5 years. If the Form 990 is for the organization’s first, second, third, fourth, or fifth tax year as a section 501(c)(3)

organization, check this box and stop here . . . . . . . . . . . . . . . . . . . . . . . . . .

Section C. Computation of Public Support Percentage

15 |

Public support percentage for 2024 (line 8, column (f), divided by line 13, column (f)) |

16 |

Public support percentage from 2023 Schedule A, Part III, line 15 |

Section D. Computation of Investment Income Percentage

15

16

%

%

17 |

Investment income percentage for 2024 (line 10c, column (f), divided by line 13, column (f)) . . . |

17 |

|

% |

18 |

Investment income percentage from 2023 Schedule A, Part III, line 17 |

18 |

|

% |

19a |

331/3% support |

|

||

|

17 is not more than 331/3%, check this box and stop here. The organization qualifies as a publicly supported organization . . |

|

||

b331/3% support

line 18 is not more than 331/3%, check this box and stop here. The organization qualifies as a publicly supported organization .

20 Private foundation. If the organization did not check a box on line 14, 19a, or 19b, check this box and see instructions .

Schedule A (Form 990) 2024

Schedule A (Form 990) 2024Page 4

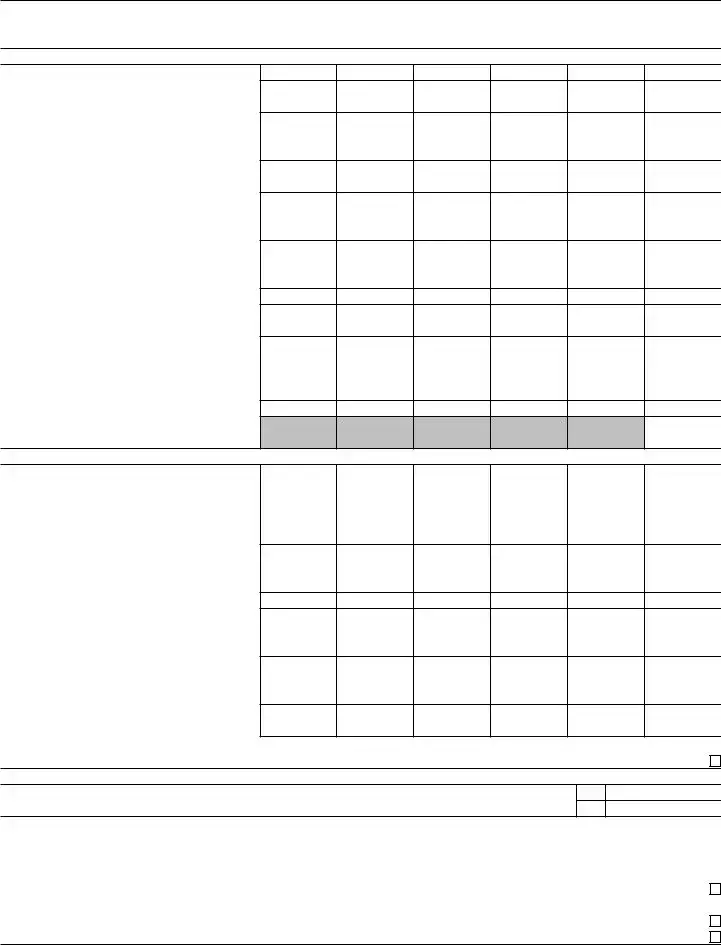

Part IV Supporting Organizations

(Complete only if you checked a box on line 12 of Part I. If you checked box 12a, Part I, complete Sections A and B. If you checked box 12b, Part I, complete Sections A and C. If you checked box 12c, Part I, complete Sections A, D, and E. If you checked box 12d, Part I, complete Sections A and D, and complete Part V.)

Section A. All Supporting Organizations

1Are all of the organization’s supported organizations listed by name in the organization’s governing documents? If “No,” describe in Part VI how the supported organizations are designated. If designated by class or purpose, describe the designation. If historic and continuing relationship, explain.

2Did the organization have any supported organization that does not have an IRS determination of status under section 509(a)(1) or (2)? If “Yes,” explain in Part VI how the organization determined that the supported organization was described in section 509(a)(1) or (2).

3a Did the organization have a supported organization described in section 501(c)(4), (5), or (6)? If “Yes,” answer lines 3b and 3c below.

bDid the organization confirm that each supported organization qualified under section 501(c)(4), (5), or (6) and satisfied the public support tests under section 509(a)(2)? If “Yes,” describe in Part VI when and how the organization made the determination.

cDid the organization ensure that all support to such organizations was used exclusively for section 170(c)(2)(B) purposes? If “Yes,” explain in Part VI what controls the organization put in place to ensure such use.

4a Was any supported organization not organized in the United States (“foreign supported organization”)? If “Yes,” and if you checked box 12a or 12b in Part I, answer lines 4b and 4c below.

bDid the organization have ultimate control and discretion in deciding whether to make grants to the foreign supported organization? If “Yes,” describe in Part VI how the organization had such control and discretion despite being controlled or supervised by or in connection with its supported organizations.

cDid the organization support any foreign supported organization that does not have an IRS determination under sections 501(c)(3) and 509(a)(1) or (2)? If “Yes,” explain in Part VI what controls the organization used to ensure that all support to the foreign supported organization was used exclusively for section 170(c)(2)(B) purposes.

5a Did the organization add, substitute, or remove any supported organizations during the tax year? If “Yes,” answer lines 5b and 5c below (if applicable). Also, provide detail in Part VI, including (i) the names and EIN numbers of the supported organizations added, substituted, or removed; (ii) the reasons for each such action;

(iii)the authority under the organization’s organizing document authorizing such action; and (iv) how the action was accomplished (such as by amendment to the organizing document).

bType I or Type II only. Was any added or substituted supported organization part of a class already designated in the organization’s organizing document?

cSubstitutions only. Was the substitution the result of an event beyond the organization’s control?

6Did the organization provide support (whether in the form of grants or the provision of services or facilities) to anyone other than (i) its supported organizations, (ii) individuals that are part of the charitable class benefited by one or more of its supported organizations, or (iii) other supporting organizations that also support or benefit one or more of the filing organization’s supported organizations? If “Yes,” provide detail in Part VI.

7Did the organization provide a grant, loan, compensation, or other similar payment to a substantial contributor (as defined in section 4958(c)(3)(C)), a family member of a substantial contributor, or a 35% controlled entity with regard to a substantial contributor? If “Yes,” complete Part I of Schedule L (Form 990).

8Did the organization make a loan to a disqualified person (as defined in section 4958) not described on line 7? If “Yes,” complete Part I of Schedule L (Form 990).

9a Was the organization controlled directly or indirectly at any time during the tax year by one or more disqualified persons, as defined in section 4946 (other than foundation managers and organizations described in section 509(a)(1) or (2))? If “Yes,” provide detail in Part VI.

bDid one or more disqualified persons (as defined on line 9a) hold a controlling interest in any entity in which the supporting organization had an interest? If “Yes,” provide detail in Part VI.

cDid a disqualified person (as defined on line 9a) have an ownership interest in, or derive any personal benefit from, assets in which the supporting organization also had an interest? If “Yes,” provide detail in Part VI.

10a Was the organization subject to the excess business holdings rules of section 4943 because of section 4943(f) (regarding certain Type II supporting organizations, and all Type III

bDid the organization have any excess business holdings in the tax year? (Use Schedule C, Form 4720, to determine whether the organization had excess business holdings.)

Yes No

1 |

2 |

3a

3b

3c

4a

4b

4c

5a

5b

5c

6

7

8

9a

9b

9c

10a

10b

Schedule A (Form 990) 2024

Schedule A (Form 990) 2024 |

Page 5 |

|

Part IV |

Supporting Organizations (continued) |

|

11Has the organization accepted a gift or contribution from any of the following persons?

aA person who directly or indirectly controls, either alone or together with persons described on lines 11b and 11c below, the governing body of a supported organization?

bA family member of a person described on line 11a above?

cA 35% controlled entity of a person described on line 11a or 11b above? If “Yes” to line 11a, 11b, or 11c, provide detail in Part VI.

Section B. Type I Supporting Organizations

Yes No

11a

11b

11c

1Did the governing body, members of the governing body, officers acting in their official capacity, or membership of one or more supported organizations have the power to regularly appoint or elect at least a majority of the organization’s officers, directors, or trustees at all times during the tax year? If “No,” describe in Part VI how the supported organization(s) effectively operated, supervised, or controlled the organization’s activities. If the organization had more than one supported organization, describe how the powers to appoint and/or remove officers, directors, or trustees were allocated among the supported organizations and what conditions or restrictions, if any, applied to such powers during the tax year.

2Did the organization operate for the benefit of any supported organization other than the supported organization(s) that operated, supervised, or controlled the supporting organization? If “Yes,” explain in Part VI how providing such benefit carried out the purposes of the supported organization(s) that operated, supervised, or controlled the supporting organization.

Section C. Type II Supporting Organizations

Yes No

1

2

1Were a majority of the organization’s directors or trustees during the tax year also a majority of the directors or trustees of each of the organization’s supported organization(s)? If “No,” describe in Part VI how control or management of the supporting organization was vested in the same persons that controlled or managed the supported organization(s).

Section D. All Type III Supporting Organizations

Yes No

1

1Did the organization provide to each of its supported organizations, by the last day of the fifth month of the organization’s tax year, (i) a written notice describing the type and amount of support provided during the prior tax year, (ii) a copy of the Form 990 that was most recently filed as of the date of notification, and (iii) copies of the organization’s governing documents in effect on the date of notification, to the extent not previously provided?

2Were any of the organization’s officers, directors, or trustees either (i) appointed or elected by the supported organization(s), or (ii) serving on the governing body of a supported organization? If “No,” explain in Part VI how the organization maintained a close and continuous working relationship with the supported organization(s).

3By reason of the relationship described on line 2, above, did the organization’s supported organizations have a significant voice in the organization’s investment policies and in directing the use of the organization’s income or assets at all times during the tax year? If “Yes,” describe in Part VI the role the organization’s supported organizations played in this regard.

Section E. Type III Functionally Integrated Supporting Organizations

Yes No

1

2

3

1Check the box next to the method that the organization used to satisfy the Integral Part Test during the year (see instructions).

a The organization satisfied the Activities Test. Complete line 2 below.

b The organization is the parent of each of its supported organizations. Complete line 3 below.

c The organization supported a governmental entity. Describe in Part VI how you supported a governmental entity (see instructions).

2 Activities Test. Answer lines 2a and 2b below. |

Yes No |

aDid substantially all of the organization’s activities during the tax year directly further the exempt purposes of the supported organization(s) to which the organization was responsive? If “Yes,” then in Part VI identify those supported organizations and explain how these activities directly furthered their exempt purposes, how the organization was responsive to those supported organizations, and how the organization determined

that these activities constituted substantially all of its activities.

bDid the activities described on line 2a, above, constitute activities that, but for the organization’s involvement, one or more of the organization’s supported organization(s) would have been engaged in? If “Yes,” explain in Part VI the reasons for the organization’s position that its supported organization(s) would

have engaged in these activities but for the organization’s involvement.

3Parent of Supported Organizations. Answer lines 3a and 3b below.

aDid the organization have the power to regularly appoint or elect a majority of the officers, directors, or

trustees of each of the supported organizations? If “Yes” or “No,” provide details in Part VI. |

3a |

|

b Did the organization exercise a substantial degree of direction over the policies, programs, and activities of each |

|

|

of its supported organizations? If “Yes,” describe in Part VI the role played by the organization in this regard. |

3b |

|

Schedule A (Form 990) 2024

Schedule A (Form 990) 2024 |

Page 6 |

|

Part V |

Type III |

|

1 Check here if the organization satisfied the Integral Part Test as a qualifying trust on Nov. 20, 1970 (explain in Part VI). See instructions. All other Type III

Section |

(A) Prior Year |

(B) Current Year |

||

(optional) |

||||

|

|

|

||

|

|

|

|

|

1 |

Net |

1 |

|

|

2 |

Recoveries of |

2 |

|

|

3 |

Other gross income (see instructions) |

3 |

|

|

4 |

Add lines 1 through 3. |

4 |

|

|

5 |

Depreciation and depletion |

5 |

|

|

6Portion of operating expenses paid or incurred for production or collection of gross income or for management, conservation, or maintenance of

|

property held for production of income (see instructions) |

6 |

|

|

7 |

Other expenses (see instructions) |

7 |

|

|

8 |

Adjusted Net Income (subtract lines 5, 6, and 7 from line 4) |

8 |

|

|

Section |

(A) Prior Year |

(B) Current Year |

||

(optional) |

||||

|

|

|

||

1Aggregate fair market value of all

a |

Average monthly value of securities |

1a |

b Average monthly cash balances |

1b |

|

c |

Fair market value of other |

1c |

d Total (add lines 1a, 1b, and 1c) |

1d |

|

eDiscount claimed for blockage or other factors (explain in detail in Part VI):

2 |

Acquisition indebtedness applicable to |

2 |

3 |

Subtract line 2 from line 1d. |

3 |

4Cash deemed held for exempt use. Enter 0.015 of line 3 (for greater amount,

|

see instructions). |

4 |

|

|

5 |

Net value of |

5 |

|

|

6 |

Multiply line 5 by 0.035. |

6 |

|

|

7 |

Recoveries of |

7 |

|

|

8 |

Minimum Asset Amount (add line 7 to line 6) |

8 |

|

|

Section |

|

|

Current Year |

|

|

|

|

|

|

1 |

Adjusted net income for prior year (from Section A, line 8, column A) |

1 |

|

|

2 |

Enter 0.85 of line 1. |

2 |

|

|

3 |

Minimum asset amount for prior year (from Section B, line 8, column A) |

3 |

|

|

4 |

Enter greater of line 2 or line 3. |

4 |

|

|

5 |

Income tax imposed in prior year |

5 |

|

|

6Distributable Amount. Subtract line 5 from line 4, unless subject to

emergency temporary reduction (see instructions). |

6 |

7 Check here if the current year is the organization’s first as a

Schedule A (Form 990) 2024

Schedule A (Form 990) 2024 |

|

|

|

|

Page 7 |

|||

Part V |

Type III |

|

||||||

Section |

|

|

|

|

Current Year |

|||

|

|

|

|

|

|

|||

1 |

Amounts paid to supported organizations to accomplish exempt purposes |

|

1 |

|

||||

2 |

Amounts paid to perform activity that directly furthers exempt purposes of supported |

|

|

|||||

|

organizations, in excess of income from activity |

|

|

2 |

|

|||

3 |

Administrative expenses paid to accomplish exempt purposes of supported organizations |

3 |

|

|||||

4 |

Amounts paid to acquire |

|

|

4 |

|

|||

5 |

Qualified |

5 |

|

|||||

6 |

Other distributions (describe in Part VI). See instructions. |

|

|

6 |

|

|||

7 |

Total annual distributions. Add lines 1 through 6. |

|

|

7 |

|

|||

8 |

Distributions to attentive supported organizations to which the organization is responsive |

|

|

|||||

|

(provide details in Part VI). See instructions. |

|

|

8 |

|

|||

9 |

Distributable amount for 2024 from Section C, line 6 |

|

|

9 |

|

|||

10 |

Line 8 amount divided by line 9 amount |

|

|

10 |

|

|||

|

|

|

|

(i) |

(ii) |

|

(iii) |

|

Section |

(see instructions) |

Underdistributions |

Distributable |

|||||

Excess Distributions |

||||||||

|

|

|

|

|

|

Amount for 2024 |

||

1 |

Distributable amount for 2024 from Section C, line 6 |

|

|

|

|

|||

2 |

Underdistributions, if any, for years prior to 2024 |

|

|

|

|

|||

|

(reasonable cause |

|

|

|

|

|||

|

instructions. |

|

|

|

|

|

||

3 |

Excess distributions carryover, if any, to 2024 |

|

|

|

|

|||

a |

From 2019 |

|

|

|

|

|

||

b |

From 2020 |

|

|

|

|

|

||

c |

From 2021 |

|

|

|

|

|

||

d |

From 2022 |

|

|

|

|

|

||

e |

From 2023 |

|

|

|

|

|

||

f |

Total of lines 3a through 3e |

|

|

|

|

|

||

g |

Applied to underdistributions of prior years |

|

|

|

|

|||

h |

Applied to 2024 distributable amount |

|

|

|

|

|||

i |

Carryover from 2019 not applied (see instructions) |

|

|

|

|

|||

j |

Remainder. Subtract lines 3g, 3h, and 3i from line 3f. |

|

|

|

|

|||

4 |

Distributions for 2024 from |

|

|

|

|

|

||

|

Section D, line 7: |

$ |

|

|

|

|

||

a |

Applied to underdistributions of prior years |

|

|

|

|

|||

b |

Applied to 2024 distributable amount |

|

|

|

|

|||

c |

Remainder. Subtract lines 4a and 4b from line 4. |

|

|

|

|

|||

5 |

Remaining underdistributions for years prior to 2024, if |

|

|

|

|

|||

|

any. Subtract lines 3g and 4a from line 2. For result |

|

|

|

|

|||

|

greater than zero, explain in Part VI. See instructions. |

|

|

|

|

|||

6 |

Remaining underdistributions for 2024. Subtract lines 3h |

|

|

|

|

|||

|

and 4b from line 1. For result greater than zero, explain in |

|

|

|

|

|||

|

Part VI. See instructions. |

|

|

|

|

|

||

7 |

Excess distributions carryover to 2025. Add lines 3j |

|

|

|

|

|||

|

and 4c. |

|

|

|

|

|

||

8 |

Breakdown of line 7: |

|

|

|

|

|

||

a |

Excess from 2020 . . . |

|

|

|

|

|

||

b |

Excess from 2021 . . . |

|

|

|

|

|

||

c |

Excess from 2022 . . . |

|

|

|

|

|

||

d |

Excess from 2023 . . . |

|

|

|

|

|

||

e |

Excess from 2024 . . . |

|

|

|

|

|

||

Schedule A (Form 990) 2024

Schedule A (Form 990) 2024 |

Page 8 |

|

Part VI |

Supplemental Information. Provide the explanations required by Part II, line 10; Part II, line 17a or 17b; Part |

|

|

III, line 12; Part IV, Section A, lines 1, 2, 3b, 3c, 4b, 4c, 5a, 6, 9a, 9b, 9c, 11a, 11b, and 11c; Part IV, Section |

|

|

B, lines 1 and 2; Part IV, Section C, line 1; Part IV, Section D, lines 2 and 3; Part IV, Section E, lines 1c, 2a, 2b, |

|

|

3a, and 3b; Part V, line 1; Part V, Section B, line 1e; Part V, Section D, lines 5, 6, and 8; and Part V, Section E, |

|

|

lines 2, 5, and 6. Also complete this part for any additional information. (See instructions.) |

|

|

|

|

Schedule A (Form 990) 2024

| Fact Name | Description |

|---|---|

| Purpose | The IRS Schedule A 990 and 990-EZ forms are used by tax-exempt organizations to provide information about their activities, finances, and governance. |

| Filing Requirement | Organizations with gross receipts of $200,000 or more, or total assets of $500,000 or more, must file Form 990. Smaller organizations may file Form 990-EZ. |

| State-Specific Requirements | Many states require organizations to file additional forms based on their specific laws governing charitable organizations. For example, California requires Form RRF-1. |

| Public Disclosure | Both forms are public documents. This means that anyone can request to see them, promoting transparency in the operations of tax-exempt organizations. |

Filling out the IRS Schedule A 990 or 990-EZ form requires careful attention to detail. This form is essential for certain tax-exempt organizations to provide information about their activities and finances. Follow these steps to complete the form accurately.

The IRS Schedule A form is used by tax-exempt organizations to provide detailed information about their charitable activities. Organizations that are recognized as 501(c)(3) must file this form along with their annual Form 990 or Form 990-EZ. This schedule helps the IRS determine whether the organization is complying with tax regulations and maintaining its tax-exempt status.

Generally, any organization that qualifies as a public charity under section 501(c)(3) must file Schedule A. This includes:

Even if your organization has low income, if you are a 501(c)(3) public charity, you still need to file this schedule.

Schedule A requires various pieces of information, including:

This information helps the IRS assess the organization’s compliance with the rules governing public charities.

Failing to file Schedule A can lead to serious consequences. The IRS may impose penalties, which can include:

To avoid these issues, it’s crucial to file Schedule A on time and ensure that all information is accurate.

Filling out the IRS Schedule A for Form 990 or 990-EZ can be a daunting task for many. One common mistake is failing to include all required information. Organizations often overlook specific details about their activities or financials, which can lead to incomplete submissions. It's essential to double-check that all sections are filled out accurately and completely.

Another frequent error is miscalculating the organization's public support percentage. This percentage is crucial for determining whether an organization qualifies as a public charity. A simple math error can result in an incorrect classification, which may affect tax-exempt status. Take the time to verify calculations and ensure they align with the supporting documentation.

Many organizations also neglect to provide adequate documentation for contributions. When reporting donations, it's vital to maintain records that substantiate the amounts listed. This includes receipts, bank statements, and letters from donors. Without proper documentation, claims may be questioned by the IRS.

In some cases, organizations fail to report all sources of income. Even small amounts can add up, and all income streams must be disclosed to provide a complete financial picture. Missing out on reporting certain income can lead to discrepancies that may trigger audits or penalties.

Another mistake is not updating the organization's mission statement. The mission statement should reflect the current goals and activities of the organization. Failing to update this information can mislead the IRS about the organization's purpose and operations.

Many individuals also overlook the importance of signatures. The forms must be signed by an authorized person, and missing signatures can delay processing or result in rejection. Ensure that the appropriate individuals review and sign the forms before submission.

Some organizations may mistakenly classify their expenses. Properly categorizing expenses is essential for accurate reporting. Misclassifying expenses can distort financial statements and affect the overall assessment of the organization’s financial health.

Another common error involves incorrect or outdated contact information. Providing accurate contact details is crucial for communication with the IRS. If the organization changes its address or phone number, it’s important to update this information on the form.

Additionally, organizations sometimes fail to adhere to deadlines. Submitting forms late can result in penalties and interest charges. Mark important dates on the calendar and plan ahead to ensure timely filing.

Finally, many individuals do not seek help when needed. While some may feel confident in their ability to fill out the forms, consulting with a tax professional or accountant can provide valuable insights. They can help navigate complexities and ensure compliance with IRS regulations.

The IRS Schedule A 990 and 990-EZ forms are essential for tax-exempt organizations, providing detailed financial information and demonstrating compliance with federal regulations. Alongside these forms, several other documents are often required or beneficial for a complete understanding of an organization's financial health and operations. Below is a list of these documents, each described briefly.

These documents collectively help illustrate an organization's financial position and compliance with tax regulations. They provide transparency to stakeholders, including donors, members, and the public, about how an organization operates and manages its resources.

The IRS Schedule A (Form 990 or 990-EZ) is an important document for tax-exempt organizations, providing essential information about their operations and financial status. Several other forms and documents share similarities with Schedule A in purpose or structure. Here are seven such documents:

When filling out the IRS Schedule A 990 or 990-EZ form, there are important guidelines to follow. Here are four things to do and not do:

Many people have misunderstandings about the IRS Schedule A 990 and 990-EZ forms. Here are five common misconceptions:

Understanding these misconceptions can help organizations better navigate their filing requirements and maintain compliance with IRS regulations.

Filling out the IRS Schedule A 990 or 990-EZ form is essential for many organizations seeking tax-exempt status. Understanding the key components of these forms can help ensure compliance and proper reporting. Here are some important takeaways:

By focusing on these key points, organizations can navigate the complexities of IRS Schedule A more effectively.