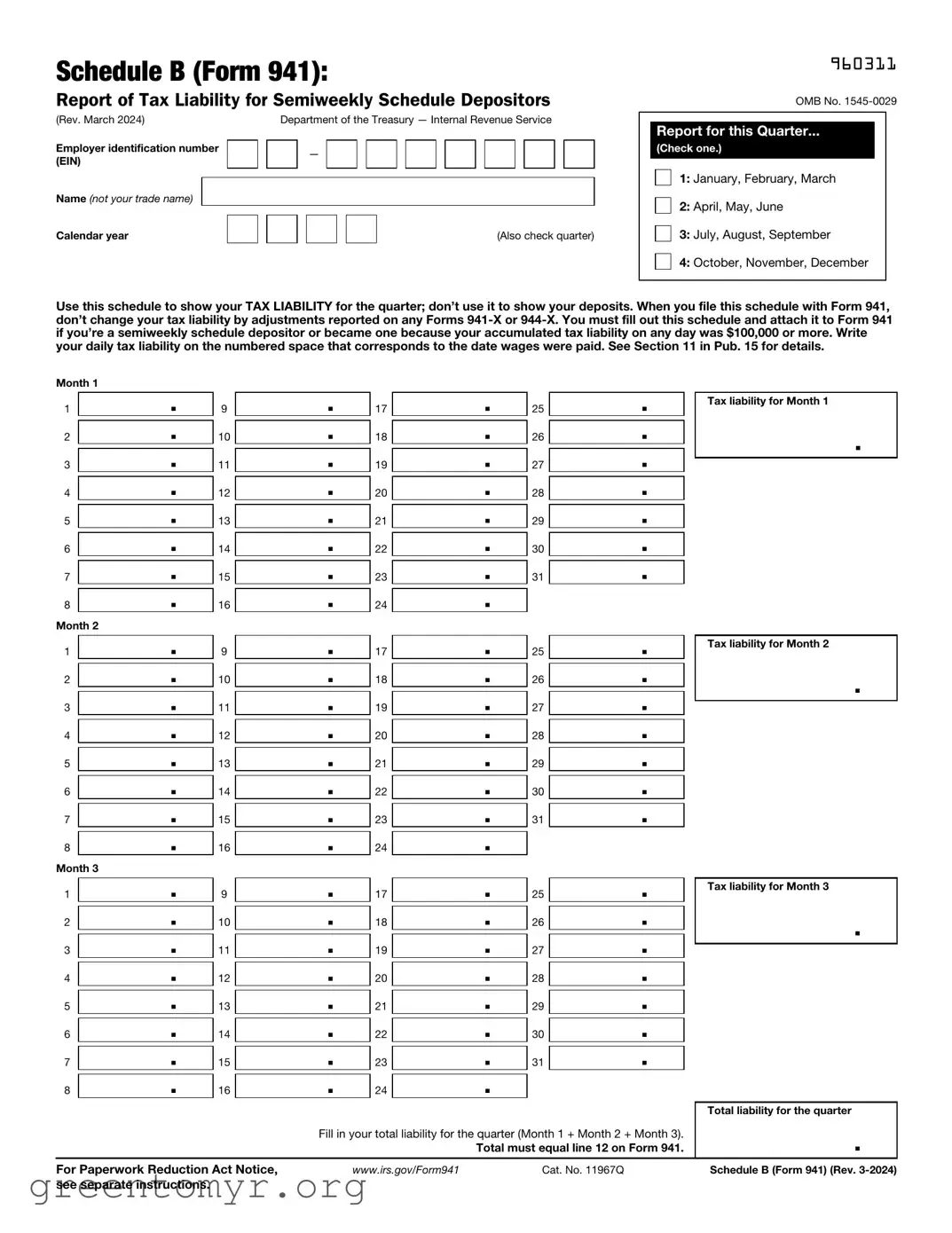

The IRS Schedule B (Form 941) is an important document for employers who need to report their federal tax obligations. This form specifically tracks the employment taxes owed for each quarter, helping businesses stay compliant with federal tax laws. Employers use Schedule B to report the total amount of wages paid and the corresponding taxes withheld from employees’ paychecks. This includes Social Security and Medicare taxes, which are crucial for funding these programs. Additionally, Schedule B provides a detailed breakdown of the tax liability for each pay period within the quarter. It is essential for employers to complete this form accurately to avoid penalties and ensure proper reporting of their tax responsibilities. Timely submission of Schedule B is vital, as it helps the IRS monitor compliance and assess whether employers are meeting their tax obligations consistently throughout the year.

Schedule B (Form 941):

Report of Tax Liability for Semiweekly Schedule Depositors

(Rev. March 2024) |

|

|

Department of the Treasury — Internal Revenue Service |

|||||||||||||||||||

Employer identification number |

|

|

|

|

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

(EIN) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Name (not your trade name) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Calendar year |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(Also check quarter) |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

960311

OMB No.

Report for this Quarter...

(Check one.)

1: January, February, March

2: April, May, June

3: July, August, September

4: October, November, December

Use this schedule to show your TAX LIABILITY for the quarter; don’t use it to show your deposits. When you file this schedule with Form 941, don’t change your tax liability by adjustments reported on any Forms

Month 1 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

|

. |

9 |

|

. |

|

17 |

|

. |

25 |

|

. |

|

Tax liability for Month 1 |

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

2 |

|

. |

10 |

|

. |

|

18 |

|

. |

26 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

|

. |

11 |

|

. |

|

19 |

|

. |

27 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

|

. |

12 |

|

. |

|

20 |

|

. |

28 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

|

. |

13 |

|

. |

|

21 |

|

. |

29 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6 |

|

. |

14 |

|

. |

|

22 |

|

. |

30 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

|

. |

15 |

|

. |

|

23 |

|

. |

31 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8 |

|

. |

16 |

|

. |

|

24 |

|

. |

|

|

|

|

|

Month 2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

|

. |

9 |

|

. |

|

17 |

|

. |

25 |

|

. |

|

Tax liability for Month 2 |

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

2 |

|

. |

10 |

|

. |

|

18 |

|

. |

26 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

|

. |

11 |

|

. |

|

19 |

|

. |

27 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

|

. |

12 |

|

. |

|

20 |

|

. |

28 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

|

. |

13 |

|

. |

|

21 |

|

. |

29 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6 |

|

. |

14 |

|

. |

|

22 |

|

. |

30 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

|

. |

15 |

|

. |

|

23 |

|

. |

31 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8 |

|

. |

16 |

|

. |

|

24 |

|

. |

|

|

|

|

|

Month 3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

|

. |

9 |

|

. |

|

17 |

|

. |

25 |

|

. |

|

Tax liability for Month 3 |

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

. |

2 |

|

. |

10 |

|

. |

|

18 |

|

. |

26 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

|

. |

11 |

|

. |

|

19 |

|

. |

27 |

|

. |

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

4 |

|

. |

12 |

|

. |

|

20 |

|

. |

28 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

5 |

|

. |

13 |

|

. |

|

21 |

|

. |

29 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6 |

|

. |

14 |

|

. |

|

22 |

|

. |

30 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7 |

|

. |

15 |

|

. |

|

23 |

|

. |

31 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

8 |

|

. |

16 |

|

. |

|

24 |

|

. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total liability for the quarter |

|

|

|

|

|

Fill in your total liability for the quarter (Month 1 + Month 2 + Month 3). |

|

. |

|||||||

|

|

|

|

|

|

|

|

|

Total must equal line 12 on Form 941. |

|

||||

For Paperwork Reduction Act Notice, |

|

www.irs.gov/Form941 |

|

Cat. No. 11967Q |

|

|

Schedule B (Form 941) (Rev. |

|||||||

see separate instructions. |

|

|

|

|

|

|

|

|

|

|

|

|

||

| Fact Name | Description |

|---|---|

| Purpose | The IRS Schedule B (Form 941) is used to report the number of employees and the amount of federal income tax withheld from their wages. |

| Filing Frequency | This form must be filed quarterly by employers who withhold federal income tax from their employees' wages. |

| Governing Law | The requirements for filing Schedule B are outlined in the Internal Revenue Code (IRC) and enforced by the IRS. |

| State-Specific Forms | Employers may also need to file state-specific payroll tax forms, which vary by state. Check your state's Department of Revenue for details. |

After gathering your information and ensuring you have the necessary documents, you’re ready to fill out the IRS Schedule B (Form 941). This form is crucial for reporting your tax obligations accurately. Follow the steps below to complete it correctly.

Once you have filled out the form, review it for accuracy. Ensure all calculations are correct. After that, submit it to the IRS by the due date to avoid penalties.

IRS Schedule B (Form 941) is a form used by employers to report their tax liability for federal income tax withholding and Social Security and Medicare taxes. It is an attachment to Form 941, which is the quarterly federal tax return that employers must file to report wages paid and taxes withheld.

Employers who have a tax liability of $100,000 or more on any day during the current quarter must file Schedule B. This requirement applies to both large employers and those who may have reached this threshold due to specific events, such as a one-time bonus payment.

Schedule B is due at the same time as Form 941. Employers must file Form 941 quarterly, and the due dates are typically the last day of the month following the end of the quarter. For example, for the first quarter (January to March), the due date is April 30.

Schedule B requires employers to report their tax liability for each month in the quarter. This includes:

To calculate your tax liability, you need to consider the total wages paid during the month, the applicable withholding rates, and any adjustments for overpayments or corrections from previous periods. Accurate payroll records are essential for this calculation.

If you discover an error after filing, you can correct it by filing an amended Form 941. Make sure to provide a clear explanation of the changes made. If the error involves the tax liability, it's crucial to pay any additional taxes owed to avoid penalties.

Yes, you can file Schedule B electronically if you are filing Form 941 electronically. Many payroll service providers offer e-filing options, which can simplify the process and help ensure accuracy.

Failure to file Schedule B when required can lead to penalties. The IRS may impose fines for late filing or failure to file, which can increase your overall tax liability. It is essential to comply with all filing requirements to avoid these consequences.

For more information, visit the IRS website or consult a tax professional. The IRS provides detailed instructions and resources related to Form 941 and Schedule B, which can help clarify any questions you may have.

Filling out the IRS Schedule B (Form 941) can be a complex task, and mistakes can lead to delays or issues with tax filings. One common error is not reporting all wages accurately. Individuals sometimes forget to include certain types of compensation, such as bonuses or overtime pay. Ensuring that all forms of income are accounted for is essential.

Another frequent mistake is miscalculating the taxes owed. Tax rates can change, and failing to apply the correct rate may result in underpayment or overpayment. It is important to double-check calculations and ensure that the latest tax rates are being used.

Some people neglect to sign and date the form. Without a signature, the IRS may consider the form incomplete. This can lead to processing delays or additional requests for information. Always remember to review the form for necessary signatures before submission.

Inaccurate identification information is another common issue. Errors in the employer identification number (EIN) or the business name can create confusion. It is vital to ensure that all identifying information matches IRS records to avoid complications.

Many individuals also fail to keep adequate records of their employment tax liabilities. Without proper documentation, it can be difficult to verify the information provided on the form. Maintaining organized records can prevent future discrepancies.

Another mistake is submitting the form late. The IRS has specific deadlines for filing, and failing to meet these can result in penalties. It is advisable to mark deadlines on a calendar and plan ahead to ensure timely submission.

Some people overlook the importance of checking for updates to the form itself. The IRS occasionally makes changes, and using an outdated version can lead to errors. Always verify that you are using the most current form available on the IRS website.

Additionally, individuals may not fully understand the instructions provided for the form. Skimming over the guidelines can lead to misinterpretation and mistakes. Taking the time to read and comprehend the instructions can help ensure accurate completion.

Finally, failing to consult a tax professional when needed can be a significant oversight. Complex tax situations may require expert guidance. Seeking assistance can help clarify any uncertainties and ensure compliance with IRS regulations.

The IRS Schedule B (Form 941) is a vital document for employers who report their payroll taxes. This form specifically helps track the number of employees and the amount of taxes withheld. Along with Schedule B, several other forms and documents are commonly used to ensure compliance with federal tax regulations. Here’s a list of some of those essential documents:

Understanding these forms and documents is crucial for maintaining compliance with tax obligations. Properly completing and submitting them can help avoid penalties and ensure that all payroll taxes are accurately reported and paid on time.

The IRS Schedule B (Form 941) is an important document for employers, specifically used to report their tax liabilities related to employee wages. Several other forms share similarities with Schedule B, primarily in their purpose of reporting employment taxes or providing information related to payroll. Here are seven documents that are similar to Schedule B:

When filling out the IRS Schedule B (Form 941), it's important to get it right. Here’s a handy list of things to do and avoid:

By following these guidelines, you can navigate the process with greater ease and confidence.

When it comes to the IRS Schedule B (Form 941), there are several misconceptions that can lead to confusion. Understanding these can help ensure proper filing and compliance.

This is not true. Any employer who has a tax liability for federal income tax withholding or social security and Medicare taxes must file Schedule B if they meet certain criteria, regardless of size.

In fact, Schedule B is required for employers who have a tax liability that exceeds a specific threshold. Failing to file it when required can lead to penalties.

Schedule B must be submitted quarterly along with Form 941. It provides important information about tax liabilities for each quarter.

In addition to wages, employers must report all applicable tax liabilities, including those for tips and sick pay. This ensures a complete overview of tax obligations.

Even if there is no tax liability for a quarter, Schedule B still needs to be filed. This keeps your records accurate and up to date.

The IRS Schedule B (Form 941) is an important document for employers who need to report their tax liabilities. Here are key takeaways to keep in mind when filling it out and using it:

Understanding these key points can help ensure compliance and avoid potential issues with the IRS.