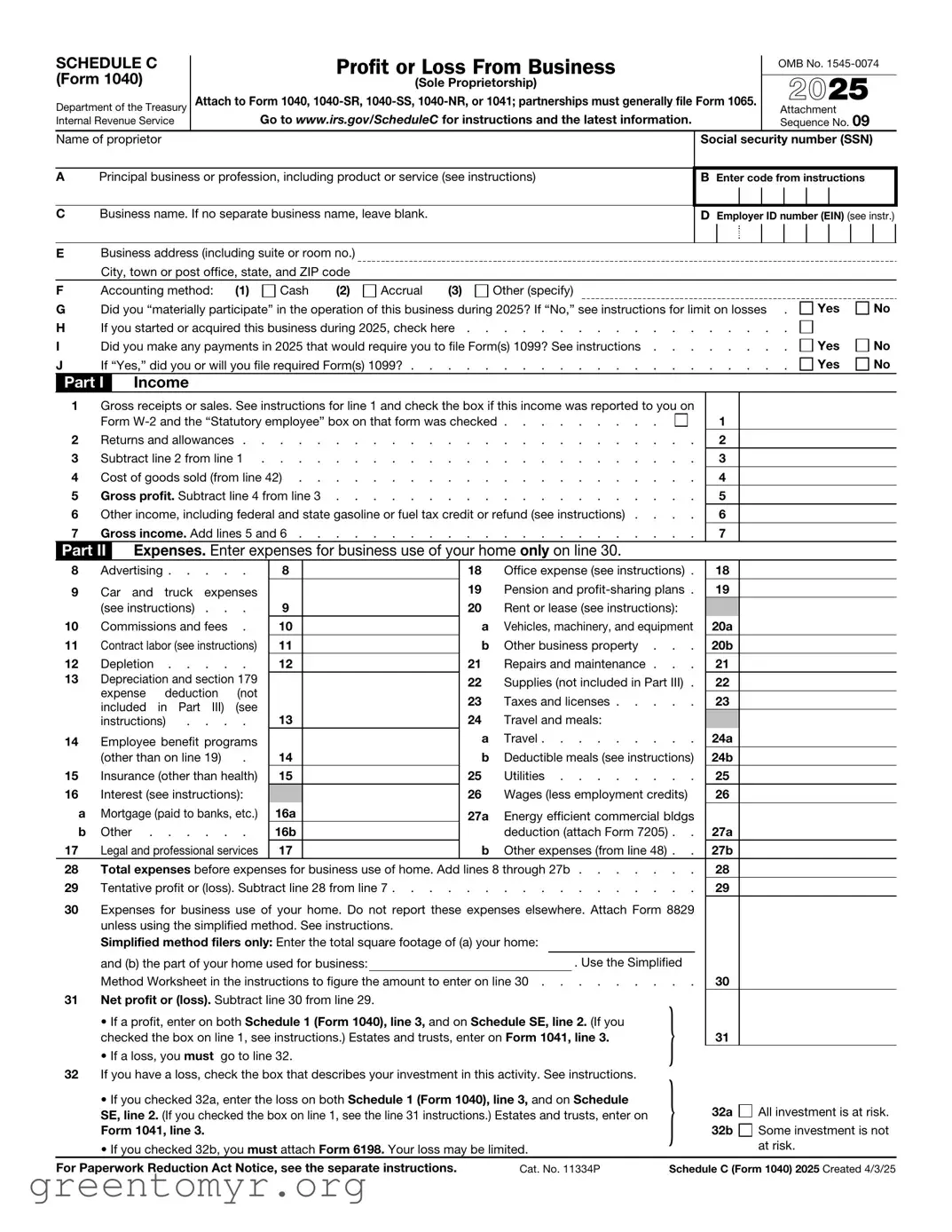

The IRS Schedule C (Form 1040) is a crucial document for self-employed individuals and small business owners, serving as a detailed report of income and expenses for the tax year. This form allows taxpayers to calculate their net profit or loss from their business activities, which ultimately impacts their overall tax liability. It requires the reporting of various types of income, including sales revenue and service fees, alongside a comprehensive list of deductible expenses such as supplies, utilities, and vehicle costs. Additionally, the Schedule C form provides sections for reporting cost of goods sold, home office deductions, and other pertinent information that can influence the taxpayer's financial standing. Understanding how to accurately complete this form is essential for compliance with tax regulations and for maximizing potential deductions, ensuring that self-employed individuals can maintain financial health while meeting their obligations to the IRS.

SCHEDULE C (Form 1040)

Department of the Treasury Internal Revenue Service

Profit or Loss From Business

(Sole Proprietorship)

Attach to Form 1040,

Go to www.irs.gov/ScheduleC for instructions and the latest information.

OMB No.

2025

Attachment Sequence No. 09

Name of proprietor

APrincipal business or profession, including product or service (see instructions)

CBusiness name. If no separate business name, leave blank.

Social security number (SSN)

BEnter code from instructions

DEmployer ID number (EIN) (see instr.)

EBusiness address (including suite or room no.) City, town or post office, state, and ZIP code

F |

Accounting method: |

(1) |

Cash |

(2) |

Accrual |

(3) |

Other (specify) |

G |

Did you “materially participate” in the operation of this business during 2025? If “No,” see instructions for limit on losses . |

||||||

H |

If you started or acquired this business during 2025, check here |

||||||

I |

Did you make any payments in 2025 that would require you to file Form(s) 1099? See instructions |

||||||

J |

If “Yes,” did you or will you file required Form(s) 1099? |

||||||

Yes No

Yes No

Yes No

Part I |

|

Income |

|

|

|

|

|

|

|

||

1 |

Gross receipts or sales. See instructions for line 1 and check the box if this income was reported to you on |

|

|

||||||||

|

Form |

. . . . . . . . . |

1 |

|

|||||||

2 |

Returns and allowances |

. . . . . . . . . . . |

2 |

|

|||||||

3 |

Subtract line 2 from line 1 |

. . . . . . . . . . . |

3 |

|

|||||||

4 |

Cost of goods sold (from line 42) |

. . . . . . . . . . . |

4 |

|

|||||||

5 |

Gross profit. Subtract line 4 from line 3 |

. . . . . . . . . . . |

5 |

|

|||||||

6 |

Other income, including federal and state gasoline or fuel tax credit or refund (see instructions) . . . . |

6 |

|

||||||||

7 |

Gross income. Add lines 5 and 6 |

. . . . . . . . . . . |

7 |

|

|||||||

Part II |

|

Expenses. Enter expenses for business use of your home only on line 30. |

|

|

|||||||

8 |

Advertising |

8 |

|

18 |

Office expense (see instructions) . |

18 |

|

||||

9 |

Car |

and |

truck expenses |

|

|

19 |

Pension and |

19 |

|

||

|

(see instructions) . . . |

9 |

|

20 |

Rent or lease (see instructions): |

|

|

||||

10 |

Commissions and fees . |

10 |

|

a |

Vehicles, machinery, and equipment |

20a |

|||||

11 |

Contract labor (see instructions) |

11 |

|

b |

Other business property . . . |

20b |

|||||

12 |

Depletion |

12 |

|

21 |

Repairs and maintenance . . . |

21 |

|

||||

13 |

Depreciation and section 179 |

|

|

22 |

Supplies (not included in Part III) . |

22 |

|

||||

|

expense |

deduction |

(not |

|

|

|

|||||

|

|

|

23 |

Taxes and licenses |

23 |

|

|||||

|

included in Part III) (see |

|

|

|

|||||||

|

instructions) . . . . |

13 |

|

24 |

Travel and meals: |

|

|

||||

14 |

Employee benefit programs |

|

|

a |

Travel |

24a |

|||||

|

(other than on line 19) |

. |

14 |

|

b |

Deductible meals (see instructions) |

24b |

||||

15 |

Insurance (other than health) |

15 |

|

25 |

Utilities |

25 |

|

||||

16 |

Interest (see instructions): |

|

|

26 |

Wages (less employment credits) |

26 |

|

||||

a |

Mortgage (paid to banks, etc.) |

16a |

|

27a |

Energy efficient commercial bldgs |

|

|

||||

b |

Other |

16b |

|

|

deduction (attach Form 7205) . . |

27a |

|||||

17 |

Legal and professional services |

17 |

|

b |

Other expenses (from line 48) . . |

27b |

|||||

28 |

Total expenses before expenses for business use of home. Add lines 8 through 27b |

28 |

|

||||||||

29 |

Tentative profit or (loss). Subtract line 28 from line 7 |

. . . . . . . . . . . |

29 |

|

|||||||

30Expenses for business use of your home. Do not report these expenses elsewhere. Attach Form 8829 unless using the simplified method. See instructions.

Simplified method filers only: Enter the total square footage of (a) your home:

|

and (b) the part of your home used for business: |

|

|

. Use the Simplified |

|

|

|

|

Method Worksheet in the instructions to figure the amount to enter on line 30 |

. . |

30 |

|

|||

31 |

Net profit or (loss). Subtract line 30 from line 29. |

|

|

} |

|

|

|

|

• If a profit, enter on both Schedule 1 (Form 1040), line 3, and on Schedule SE, line 2. (If you |

|

|

||||

|

checked the box on line 1, see instructions.) Estates and trusts, enter on Form 1041, line 3. |

31 |

|

||||

|

• If a loss, you must go to line 32. |

|

|

|

|

||

32 |

If you have a loss, check the box that describes your investment in this activity. See instructions. |

} |

|

|

|||

|

• If you checked 32a, enter the loss on both Schedule 1 (Form 1040), line 3, and on Schedule |

32a |

All investment is at risk. |

||||

|

SE, line 2. (If you checked the box on line 1, see the line 31 instructions.) Estates and trusts, enter on |

||||||

|

Form 1041, line 3. |

|

|

32b |

Some investment is not |

||

|

• If you checked 32b, you must attach Form 6198. Your loss may be limited. |

|

|

at risk. |

|||

For Paperwork Reduction Act Notice, see the separate instructions. |

Cat. No. 11334P |

Schedule C (Form 1040) 2025 Created 4/3/25 |

|||||

Schedule C (Form 1040) 2025 |

Page 2 |

|

Part III |

Cost of Goods Sold (see instructions) |

|

33 |

Method(s) used to |

|

|

|

|

|

|

|

value closing inventory: |

a |

Cost |

b |

Lower of cost or market |

c |

Other (attach explanation) |

34Was there any change in determining quantities, costs, or valuations between opening and closing inventory?

If “Yes,” attach explanation |

Yes |

No

35 |

Inventory at beginning of year. If different from last year’s closing inventory, attach explanation . . . |

35 |

36 |

Purchases less cost of items withdrawn for personal use |

36 |

37 |

Cost of labor. Do not include any amounts paid to yourself |

37 |

38 |

Materials and supplies |

38 |

39 |

Other costs |

39 |

40 |

Add lines 35 through 39 |

40 |

41 |

Inventory at end of year |

41 |

42 |

Cost of goods sold. Subtract line 41 from line 40. Enter the result here and on line 4 |

42 |

Part IV Information on Your Vehicle. Complete this part only if you are claiming car or truck expenses on line 9 and are not required to file Form 4562 for this business. See the instructions for line 13 to find out if you must file Form 4562.

43 |

When did you place your vehicle in service for business purposes? (month/day/year) |

/ |

/ |

44Of the total number of miles you drove your vehicle during 2025, enter the number of miles you used your vehicle for:

a Business |

b Commuting (see instructions) |

c Other |

45 Was your vehicle available for personal use during

46 Do you (or your spouse) have another vehicle available for personal use?. . . . . . . . . . . . . .

47a Do you have evidence to support your deduction? . . . . . . . . . . . . . . . . . . . .

b If “Yes,” is the evidence written? . . . . . . . . . . . . . . . . . . . . . . . . .

Part V Other Expenses. List below business expenses not included on lines

Yes

Yes

Yes

Yes

No

No

No

No

48 |

Total other expenses. Enter here and on line 27b |

48

Schedule C (Form 1040) 2025

| Fact Name | Details |

|---|---|

| Purpose | The IRS Schedule C (Form 1040) is used by sole proprietors to report income or loss from their business. |

| Filing Requirement | Individuals must file Schedule C if they have net earnings from self-employment of $400 or more. |

| Business Expenses | Taxpayers can deduct various business expenses, including supplies, advertising, and home office costs. |

| Net Profit or Loss | The form calculates the net profit or loss, which is then reported on the individual's Form 1040. |

| Self-Employment Tax | Net earnings from Schedule C are subject to self-employment tax, which funds Social Security and Medicare. |

| State-Specific Forms | Some states require additional forms for reporting business income, governed by state laws such as California Revenue and Taxation Code. |

| Filing Deadline | Schedule C is typically due on April 15, coinciding with the federal income tax return deadline. |

Filling out the IRS Schedule C (Form 1040) is an important step for self-employed individuals to report income and expenses from their business. Completing this form accurately ensures that you provide the IRS with the necessary information about your business activities.

Once you have completed Schedule C, you will attach it to your Form 1040 when you file your taxes. Make sure to keep a copy for your records.

IRS Schedule C is a form used by sole proprietors to report income and expenses from their business. It is filed along with Form 1040, the individual income tax return. This form helps the IRS understand your business's financial performance and determine your tax liability.

Individuals who operate a business as a sole proprietor must file Schedule C. This includes freelancers, independent contractors, and anyone earning income from self-employment. If your business earned a profit, you are required to report it, regardless of the amount.

Report all income earned from your business activities on Schedule C. This includes:

Make sure to include all sources of income to ensure accurate reporting.

You can deduct a variety of business expenses on Schedule C, which may include:

Keep detailed records of your expenses to substantiate your deductions.

To calculate your net profit or loss, subtract your total expenses from your total income. The formula looks like this:

Net Profit/Loss = Total Income - Total Expenses

If your income exceeds your expenses, you will report a profit. Conversely, if your expenses are higher than your income, you will report a loss.

Schedule C is due on the same date as your individual income tax return, Form 1040. Typically, this is April 15th of each year. If you need more time, you can file for an extension, but be aware that any taxes owed are still due by the original deadline.

Filling out the IRS Schedule C (Form 1040) can be a straightforward process, but many individuals make common mistakes that can lead to issues down the line. One significant error is failing to report all income. Every dollar earned from a business must be included. Omitting even a small amount can raise red flags with the IRS and result in penalties.

Another frequent mistake is misclassifying expenses. Business owners often confuse personal expenses with business-related costs. For instance, if someone uses their car for both personal and business purposes, they must accurately separate those expenses. Failing to do so can lead to deductions that are not allowed, which could affect the overall tax return.

Many individuals also overlook the importance of keeping thorough records. Inadequate documentation can lead to disputes with the IRS. Receipts, invoices, and bank statements serve as proof of income and expenses. Without proper records, it becomes challenging to substantiate claims made on the Schedule C form.

Another common mistake is neglecting to report business losses. If a business incurs losses, these can be deducted from other income. However, some people may not realize they can report these losses, potentially missing out on valuable tax benefits. It’s essential to understand how to report losses accurately to maximize potential deductions.

Additionally, failing to claim all eligible deductions is a mistake that can cost taxpayers. Common deductions include home office expenses, supplies, and travel costs. Many business owners do not take full advantage of these deductions due to a lack of awareness or understanding of what qualifies.

Lastly, errors in calculations can lead to significant problems. Simple arithmetic mistakes or incorrect entries can result in an inaccurate tax return. It is crucial to double-check all figures and ensure they align with supporting documentation. Taking the time to review the completed form can prevent unnecessary complications with the IRS.

The IRS Schedule C (Form 1040) is essential for reporting income or loss from a business you operated or a profession you practiced as a sole proprietor. To ensure accurate reporting and compliance, several other forms and documents often accompany Schedule C. Here’s a list of these important documents:

Gathering these forms and documents ensures a smoother tax filing process. Accurate reporting not only helps in compliance but also maximizes potential deductions, ultimately benefiting your financial situation.

The IRS Schedule C (Form 1040) is a crucial document for self-employed individuals, allowing them to report income or loss from their business. Several other forms and documents share similarities with Schedule C, either in purpose or structure. Here is a list of nine documents that are comparable to Schedule C:

Each of these documents serves a specific purpose in the tax reporting process, yet they share common elements with Schedule C, particularly in their focus on income reporting and financial disclosure.

When filling out the IRS Schedule C (Form 1040), it's important to be careful and thorough. Here are some things you should and shouldn't do:

Following these tips can help ensure that your Schedule C is completed accurately and efficiently. Good luck!

The IRS Schedule C (Form 1040) is a critical document for self-employed individuals and small business owners. However, several misconceptions can lead to confusion and mistakes. Here are five common misunderstandings:

Many believe that only businesses registered as corporations or LLCs can use Schedule C. In reality, anyone who earns income from self-employment, including freelancers and sole proprietors, can file this form.

While it is true that self-employment income should be reported, some individuals think that all income sources must go on Schedule C. Income from investments or wages from a traditional job should be reported on different forms, such as the W-2 or 1099.

There is a common belief that only expenses with receipts can be deducted. However, while receipts are important for documentation, taxpayers can also deduct reasonable estimates of expenses based on other records, such as bank statements or logs.

Some individuals think that every expense related to their business can be fully deducted. This is not the case. Certain expenses, like meals and entertainment, have limitations on how much can be deducted.

Many believe that filing Schedule C will automatically result in a tax refund. However, whether a refund is received depends on overall income, deductions, and tax liabilities. Simply filing the form does not ensure a refund.

Understanding these misconceptions is essential for accurate tax reporting and compliance. Proper use of Schedule C can help individuals manage their tax obligations effectively.

Filling out the IRS Schedule C (Form 1040) is essential for individuals who are self-employed or operate a sole proprietorship. Here are some key takeaways to consider when approaching this important tax document: